Inflate or Die! When Leverage Fails and Market Hope Turns to Fear

Stock-Markets / Financial Markets 2014 Sep 26, 2014 - 02:11 PM GMTBy: Ty_Andros

In today's TedBits we will be outlining a lot of smoke signals. They signal fires burning and about to break out. As everyone is aware, the Federal Reserve has been tightening monetary policy for almost a year now and has been joined by the Chinese central bank. The Federal Reserve has been reducing its balance sheet expansion from $85 billion a month (85,000 million) to zero in mid-November. While the fed does not characterize it as a tightening, it is one. Numerous studies have put the amount of interest rate reduction to -3 % when QE3 was at full bore. Now that the reduction is approaching zero negative interest rates are ending, they have raised rates by about 3% in real terms. We are Austrians at TedBits and believe in all of the core truths from Ludwig Von Mises:

In today's TedBits we will be outlining a lot of smoke signals. They signal fires burning and about to break out. As everyone is aware, the Federal Reserve has been tightening monetary policy for almost a year now and has been joined by the Chinese central bank. The Federal Reserve has been reducing its balance sheet expansion from $85 billion a month (85,000 million) to zero in mid-November. While the fed does not characterize it as a tightening, it is one. Numerous studies have put the amount of interest rate reduction to -3 % when QE3 was at full bore. Now that the reduction is approaching zero negative interest rates are ending, they have raised rates by about 3% in real terms. We are Austrians at TedBits and believe in all of the core truths from Ludwig Von Mises:

"There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved." - Ludwig von Mises

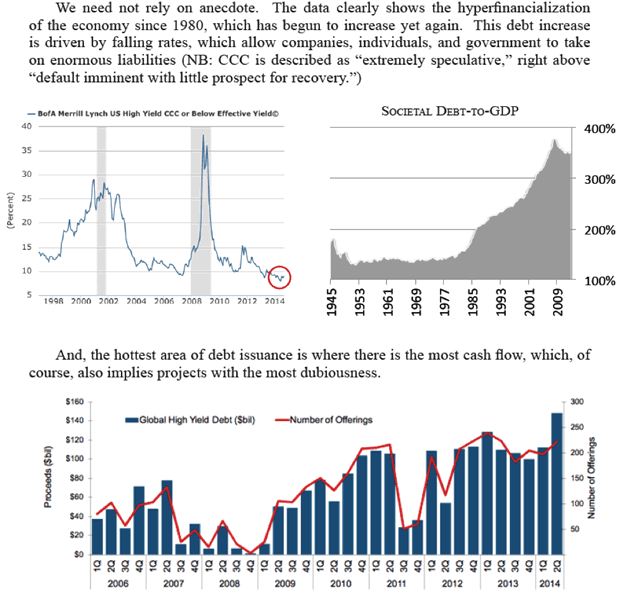

This is the state of the world today. The financial system and governments would collapse if credit could not expand and steal from the future. It is their lifeblood. They have created a world where they always can borrow, but have made no provision for the repayment. It is a Ponzi scheme. The math can no longer work anywhere you look. Since the math can't be made to work it is obvious that covert techniques of money printing are fully engaged and no one within the system dares yell, "Fire!" and call them out on their betrayals. Since Bretton Woods II in August 1971 when our leaders betrayed us by substituting IOUs for money, our world has become one big credit expansion, everywhere and always, REAL growth has INCREASINGLY ceased. If there wasn't lending for consumption called growth, the world's economies would rightly be called in a depression. It truly is INFLATE or DIE. Without it, our Ponzi economies and welfare states would collapse in the insolvency they inhabit. It is why our economies have become financialized to extract every penny in one way or another that they can from the public and transfer it to the government and the financial systems which control them (central banks and the their shareholders). We are debt slaves and serfs to global socialist elites, which are morally and fiscally bankrupt.

Easy money creation out of thin air has allowed politicians to cover up poor policy decisions and buy votes for decades, and the accumulated poison is now overwhelming the ability of the global economies to grow. Clearing out those DECADES of bad policies choices will be almost impossible. To do so has turned what would have been a roadside bomb of POLICY adjustment into a NUCLEAR BOMB of systemic changes. The governments that have put these anti-growth policies in place now have no memory of the policies required to create growth. Freedom and free markets, Capitalism (more for less) sound money and private property rights have all gone the way of the DODO bird: EXTINCT. Thus, the restoration of these things is INCONCEIVABLE to them. Nothing less will avoid the demise Von Mises speaks of. Debt cannot compound relentlessly without the economic growth to service it. It is called debt spirals and imminent leverage failures and it is everywhere. We will show you several today.

Janet Yellen has been on a honeymoon since becoming fed chairperson and that situation is about to change in my opinion. If you look back at the history of new fed chairmen they have always faced a challenge and Janet's challenge is coming to the plate. It will be Bigger than 2000 and 2008 I believe. Keep in mind one of Ben Bernanke's recent comments that he believes interest rates will not rise again in his lifetime. Why? You ask? Because the leverage in the system will collapse the very financial assets and governments which underpin the global financial systems. It is INFLATE or DIE and it provides the additional benefit of feeding insolvent welfare states and the socialist politicians to feed their Useful Idiot supporters. Today's missive will put some meaning into that observation.

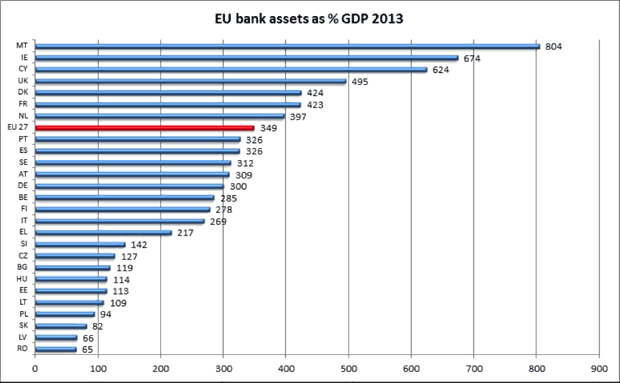

First, let's look at some parts of the global banking systems as a percentage of GDP in their respective economies:

Notice the average in the Eurozone is a GIGANTIC 349% of GDP in 2013 (600% in the Swiss banking giants). If those assets declined in value by a mere 10% (hardly a correction), the average checks those governments would have to write is 35% of a year's GDP. Where would that money come from as these countries have surrendered the printing press to the ECB (a political exercise to gather power). Their financial systems would collapse instantly. Since those same banks also have gorged on Eurozone debt, their toxic assets would be quite a bit larger. Although, keep in mind the Eurozone has passed laws calling sovereign debt risk free so it wouldn't cause them to have to raise reserves. But the falling prices of everything outside will. In reality, I believe some of that decline has already occurred and a regulatory approved cover up is underway.

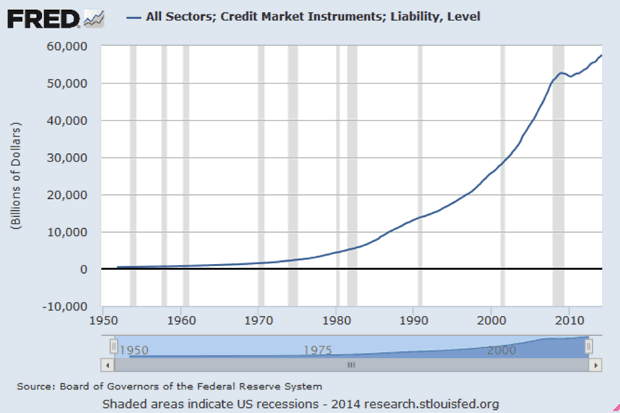

Since Bretton Wood II removed the shackles of semi-sound money redeemable in gold, growth has become a function of credit expansion as illustrated by this chart of all credit market debt from the St Louis Federal Reserve:

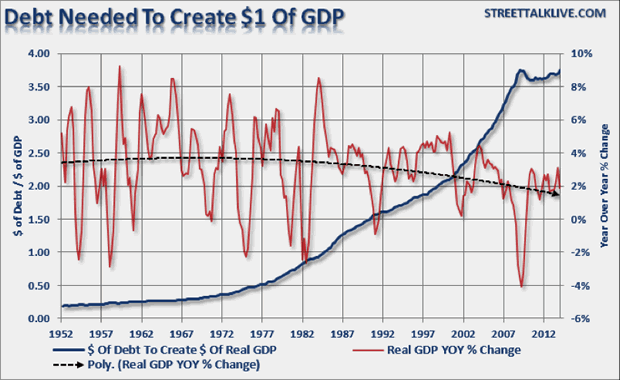

That brief downturn, which began in 2008, almost destroyed the global financial system, but those losses remain embedded in the system and RISKS have grown as the world has created another $30 Trillion dollars of debt according the Bank of international settlements. Yes, that is $57.5 trillion dollars ($57.5 million million) of debt (US only), spread equally among the US it is $183,300 per person. If the average interest rate on that debt is just 4% (I believe it is much higher) then the USA needs to generate $2.301 trillion just to pay the interest on it, not including principal payment. Debt creation for GDP expansion is dying as it now it prohibitively expensive and has reached the point of diminishing returns:

Now for every dollar of new debt the US gets 8 cents of GDP!

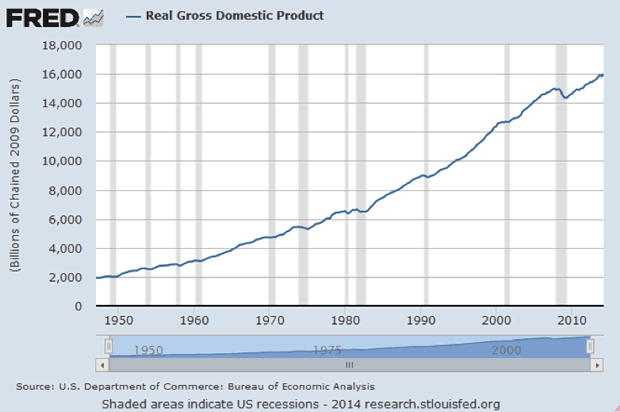

The reported GDP of the USA is now approaching $16 Trillion ($16 million million).

If you subtract phantom GDP, which is about 17% of this number you are looking at $13.3 trillion. (Phantom GDP is economic activity in which no money is exchanged, for example if you own your house free and clear but could rent it out for $2500 they call that GDP, or a free checking account which they may estimate would cost $200 dollars a year, unfunded pensions called paid wages, etc.) To service the debt using the previous calculation of interest due, that $13.3 trillion must generate 17.3% just to service the debt before any wealth can be created. That 17.3% is being paid into the financial systems (banksters) and the lenders to the government.

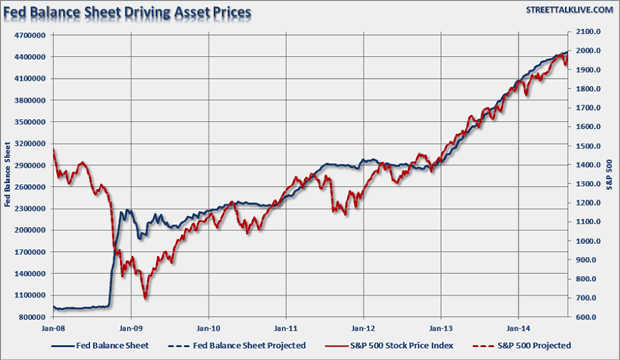

Next let's look at the stock market - in my opinion a levitation completely spawned by the feds balance sheet expansion, friendly HFT, leveraging corporate balance sheets with buybacks, and the plunge protection team at the Federal Reserve's headquarters on Liberty Street in New York. All working hand in hand to foster confidence in the private sector, which has not benefited from the expansion for the most part as the spoils have gone to the big banks and pension funds for the most part. Here is look from Lance Roberts and streetalklive.com:

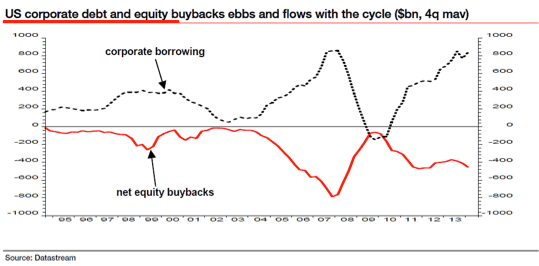

When you subtract the balance sheet expansion from stock prices, the bull market in stocks since 2009 would DISAPPEAR! It is an illusion provided by unsound money and debasement, stocks repricing to reflect the lower purchasing power of what they are denominated in. Look at the mountain of stocks bought back at the highs with LEVERAGE:

CORPORATIONS are more LEVERAGED than EVER, foolish CEOs and bitten the poison fruit and at previous lows they will be in negative equity. Think IBM!

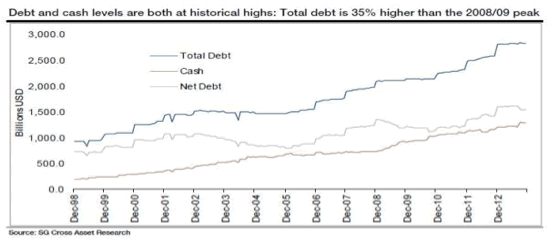

Earnings growth and stock markets on all time high are a MAIN STREAM MEDIA and WALL STREET MIRAGE. This leverage boosts earnings when revenues don't grow and reduces taxes as the interest is DEDUCTIBLE. FINANCIAL ENGINEERING to fool the fools among us. The stock market is out on a limb, once again of leverage. This chart from www.dshort.com lays out the tremendous amount of leverage underpinning the stock market:

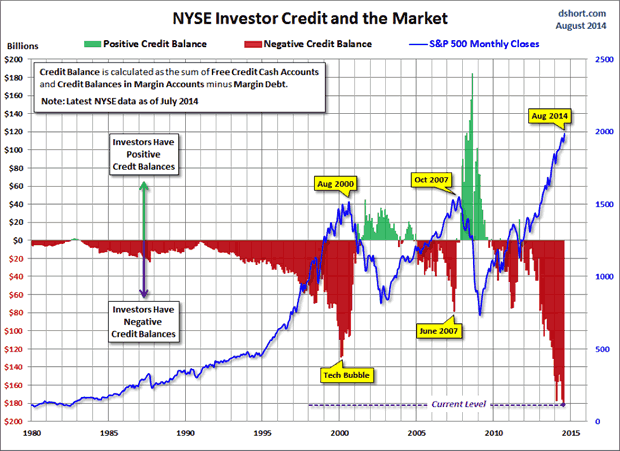

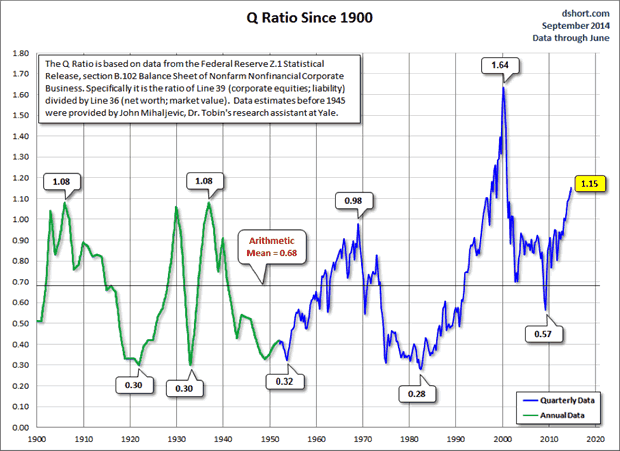

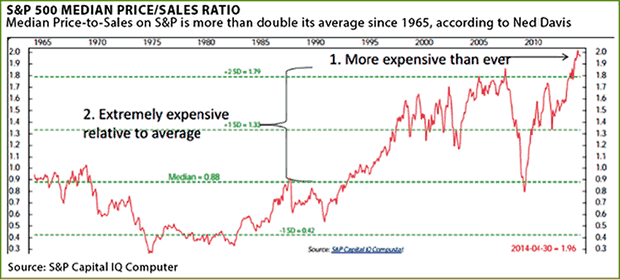

Stocks are AFLOAT on a SEA of LEVERAGE never before seen in HISTORY. I thought we had the final spike high last spring, but those highs in price were confirmed by many things such as advance decline lines, rsi and other internals. The most recent highs are all with bearish divergences across the board. This next chart is Tobin's Q ratio and it is also is at all-time highs excluding the mania high tech bubble in 2000:

Notice how previous highs preceded every major crash since 1900? When speaking of PRICE to sales ratios levels are at all-time highs and nosebleed levels!

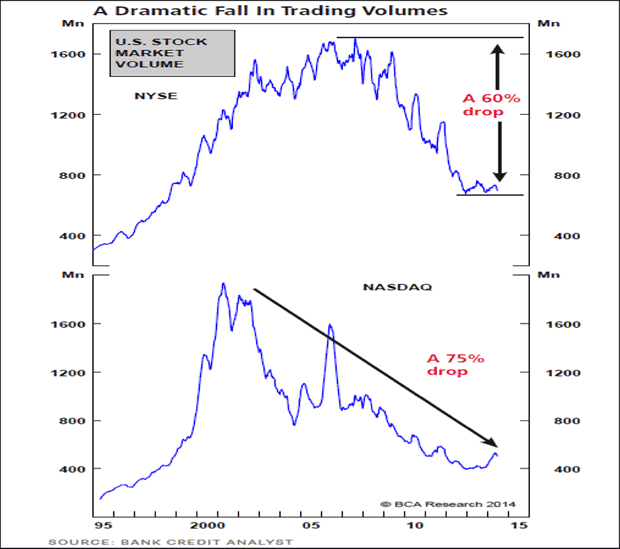

But the whole rally since 2009 has been on plummeting volume:

The cyclical bull market since March 2009 has occurred on declining volume. In true bull markets, volume accompanies price. Since this is purely a bull market that has been financial engineered by the powers that be, price is higher and volume has crashed. This says it all. To make this DOUBLY Dangerous, HFT (high frequency trading) has become 60 to 80% of all the trading during this period. In 2008-9 it was less than 25%. Thus the REAL trading (HFT trade last seconds, not minutes, hours or days, it is a ghost of real trading and the volume is an illusion) that is occurring is probably down 80% from the highs. The HFT industry says they are bringing liquidity but during a crash and disorderly markets you can expect them to TURN OFF until orderly markets resume. They won't show up when needed... I promise!

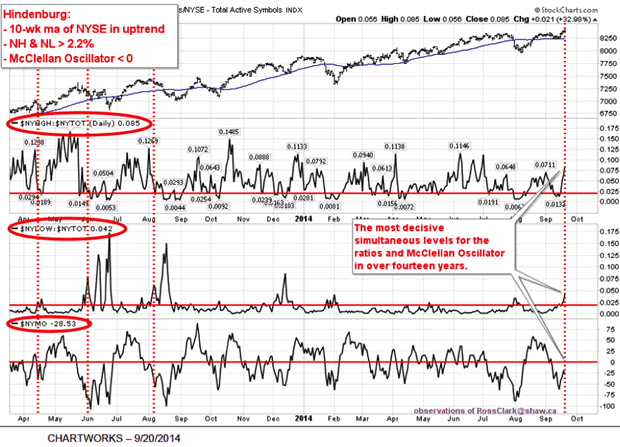

The next chart is courtesy of Bob Hoye and his institutional advisors (I subscribe and urge you to do the same) and it is giving a Hindenburg Omen signal similar in magnitude to that last seen in March 2000.

- 50 day moving average for the NYSE must be rising.

- The number of new 52 week lows must be at least 2.2% of issues that traded and changed in value. 4.2%

- The new 52 week highs must also be at least 2.2% of issues that traded and changed in value. 8.5%

- McClellan Oscillator (NYMO) must be negative on the day. -28

Quoting Bob: "These are hard facts based what happened previously based on two and a half decades of pure Hindenburg Omen history."

- Major Crash - 27% probability. (In the last 27 years there has never been a crash without a preceding Hindenburg).

- Selling panic of at least 10-15% - 39% probability

- Sharp decline of at least 8-10% - 54% probability

- Meaningful decline of at least 5-8% - 77% probability

- Mild decline of at least 2-5% - 92% probability

- The HO signal is an outright miss - 7.7% probability (one out of 13 times)

He goes on to state that the last time he saw these levels were February 29th to March 7th, 2000. Do you remember what happened then? Are we at the next episode of credit contraction?

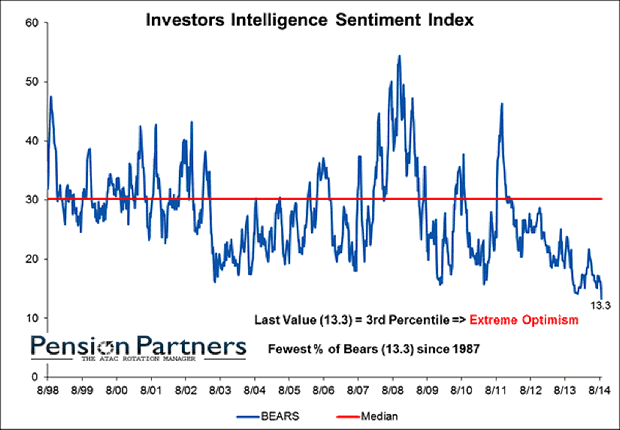

Now let's look at one last stock market chart that is set up at an extreme not seen since just before the CRASH of 1987:

Moral hazard is at superhuman levels courtesy of the Feds actions since 2008, levels rarely seen in history. This chart was self-explanatory, BEARISH sentiment is at multi decade lows... can you say be contrarian?

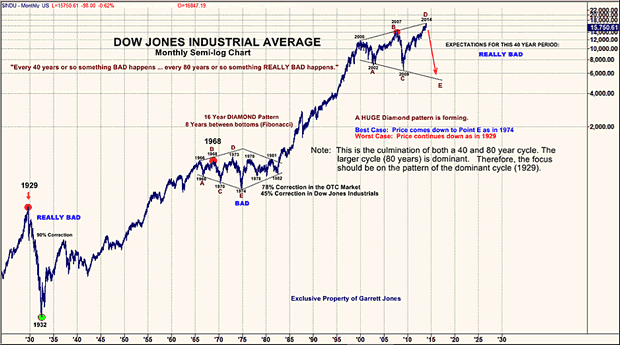

The markets are in a WOLF wave similar to the 1970s but to a much BIGGER degree (thank you Garrett Jones) and should soon plummet below the 2009 lows at it heads into the 2016 elections as the economy crumbles under the damage wrought by District of corruption in Washington and the chosen one since 2008:

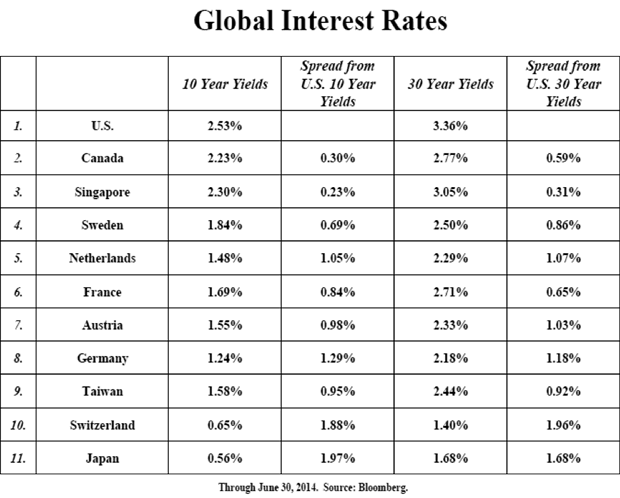

US rates are the highest in the developed world by a considerable margin, take a gander at this yield chart which is now 90 days old:

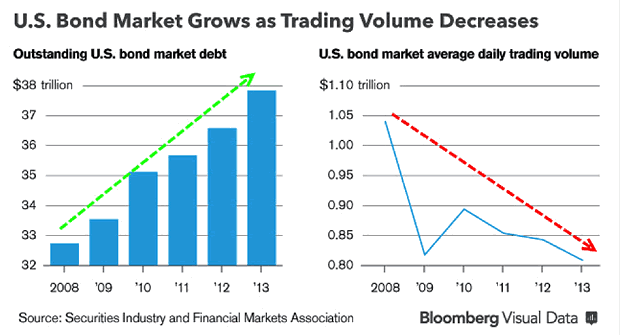

Most of those countries are quite a bit lower at this time but the US is virtually unchanged, the rotation into US treasury debt is ROARING. In many EU countries 2 year yield are at ZERO while 2 years in the US yield over 50 basis points. Can you say dollar friendly? As the bond bull off the 2000 lows has exploded in supply, Dodd frank has destroyed market liquidity:

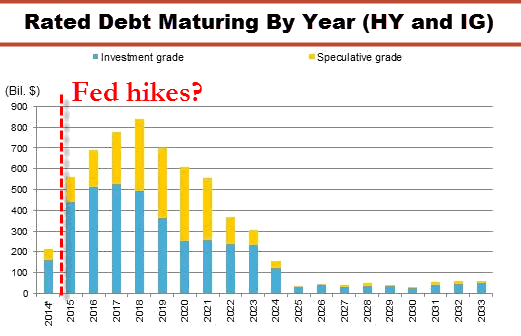

Meanwhile, Interest rates on non-government debts are TURNING higher, led by the JNK (junk). Lets look at an excerpt from the most recent Myrmikan update by Dan Oliver (I urge you to subscribe):

And the maturity wall that will have to be met into a rising interest environment courtesy of the Fed:

And let's underline it with some recent headlines/storys from www.zerohedge.com:

High-Yield Credit Crashes To 6-Month Lows As Outflows Continue High-Yield Bonds "Extremely Overvalued" For Longest Period Ever High Yield Credit Market Flashing Red As Outflows Surge

The Smart Money is getting out while the getting is good as they can read the TEA LEAVES! Would you want to be long at all-time highs heading into an ill-conceived tightening and maturity wall of that magnitude? The academics at the fed are about to learn a lesson: credit expansion IS NOT economic growth. Look no further that the aforementioned ETF of the JNK bonds, the duration mismatch of daily liquidity combined with the illiquidity of the bonds themselves at trading desks will be a debacle in my opinion. ETFs in general suffer from this malady and could be a big catalyst for market crashes when liquidity disappears but RETAIL sellers are anxious to exit! That is a prediction.

Now let's look at a MONTHLY Continues commodity index chart and what these issues are doing there going back to January 2004:

THIS IS A BIG CHALLENGE! Look at that HUGE Head and Shoulder top: under construction for 8 years!!!! And it became active THIS MONTH. Falling through the right shoulder and support is a BIG DEAL and signals DEFLATION. Those are 5 year lows with momentum, which does not symbolize a recovery in the GLOBAL economy, in fact just the OPPOSITE. This is not a chart signaling economic growth and recovery, it is just the opposite. Look when the deflation began again: when they started the TAPER! The rising trend line is the trend line since the 2000-2002 lows, so the secular bull is alive but the cyclical bear is going to put it to the test. If Yellen allows the rising trend line to be punctured, things could get out of hand very quickly!

To affirm this picture look no further than the US dollar since 2004, a huge MULTI YEAR bottom looks to be in place in my opinion:

The dollar is on a monthly buy signal and based on the chart should RUMBLE HIGHER! This is a picture of an unfolding disaster for the world economies; it is a freight train full of looming disasters pulling out of the station with lots of momentum yet to emerge. Every bit of debt issued outside the US, which is dollar denominated, is BECOMING a lot less SERVICABLE as the debtors must convert their local currencies into dollars to make payments to lenders. The higher it goes, the more they must pay! Dollar denominated debt is actually a short position equal to the size of the borrowing. An example is the Ukraine whose debt is over a quarter of a trillion dollars and whose currency is off 50% since January, thus their external debt in local currency terms is up 50% to $375 billion. Or Russia, with $650 billion in external debt and their currency is off 30% pushing their obligation near a trillion. Would you rather be the lender or the borrower? The lender is holding the bag, think banking systems and fools who believe bombs are RISK free. They are not risk free in a debt spiral world with no growth.

As the next phase of the crisis unfolds, and Yellen tightens (rush for yield in a yield less world) investor's worldwide will behave like Pavlov's dog and rush to the dollar for safety. This rush has already begun. With the dollar rallying those metrics is NOW playing itself out around the world. The principle export of the US for DECADES is and has been DOLLARS and many of the people off shore are short of them because of dollar denominated DEBT. That is why many markets crash when the dollar rises. They must liquidate other investments to SERVICE the debt, a margin call to levered economies. They are in a huge short squeeze globally. A rising dollar is ECONOMIC and FISCAL poison to a dollar debt denominated world. Can you hear the printing presses?

In closing: It's still Inflate or Die and it is now more imperative than ever. Everything is set to trigger a number of concurrent setbacks for investors caught in the matrix of misinformation and the mainstream media. I have been looking for the CREDIT expansion since 2009 to end this year as I have outlined since January when the taper really started to BITE. The FED can never remove the liquidity, ever. The ability to do so ended in 2008 when interest rates went to ZERO, the financial system died (now on life support known as QE) and have remained there. Tops are a process and look to be completing now as you can see. My latest missive on Bombs er bonds, debacle on the doorstep was done in May. The fed and Chinese tightening will not be a ENGINEERED soft landing it is hoped it will be, I believe an economic and market crash is imminent. The Alibaba IPO was a bell ringer for stocks; a close look at the corporate structures, and valuations spells recklessness rarely seen, and let's put a few cherries on top as the Russell 2000 just had a death cross and approximately 40% of all Nasdaq stocks are in bear markets. DING DING DING!

I have said many times that they can never end QE as it covers the negative cash flows of so many including Insolvent governments and have done a lot to move toxic assets to central bank balance sheets where they can die a quiet death. The fingerprints of the next contraction in the credit and global economic crash are all front and center. I have not touched on Europe but the TRAGEDY is in full bloom from Italy to France and many places in between.

The next crisis is clearly in front of us and it is much larger than the 2008 version. The elites have only expanded the economy by issuing DEBT; remember the boom brought on by credit expansion. Yellen will fail her tapering and ignite the next leg down in global economies; the markets are telling us so in macro! The world is at the edge of a knife and the tightening and dollar bottom is the trigger for the next contraction. Stock and bombs er bonds are on their highs, gold is on its lows, and reversals are at hand in my opinion.

The policies to revive the economy are inconceivable to those who control the World's economies as they are socialists. Capitalism, free markets and sound money (which they don't know the meaning of) is the boogeyman to be stopped at all costs. That is what their policies are designed to do, killing all three. It is the only solution to the world's problems, and the politicians are killing it. Those policies of PRIVATE sector growth where implemented by their grandfathers and they missed the history lessons. As I outlined in my last series Useful Idiots and the Something for Nothing Society, this is a societal suicide that all empires have gone through and there is no way to dodge the bullet as it is sociopaths and psychopaths leading us to our doom. The system is now made to create failure and create money out of thin air to cover it up. This will end. It is the greatest opportunity in the world as the greatest transfer of wealth in history looms from those that hold it in paper to those that don't. Von Mises quote looms dead ahead. May God Bless you all.

Author's Note: In my opinion the greatest manmade disaster and OPPORTUNITY in history is unfolding in every corner of the world. Are you diversified or operating with EYES WIDE SHUT? Are you prepared to turn it into opportunity by properly diversifying your portfolio? Adding absolute return investments which are designed with the potential to thrive (up and down markets) regardless of what unfolds economically or politically? This is what I do for investors; help them diversify into investments which are created to potentially thrive in the storm. For a personal consultation with me CLICK HERE!

Don't miss the next edition of TedBits or our weekly wrap subscriptions are free CLICK HERE! and check out the new TedBits AUSTRIAN Blog CLICK HERE!

May God Bless you all,

By Ty Andros

TraderView

Copyright © 2014 Ty Andros

Hi, my name is Ty Andros and I would like the chance to show you how to capture the opportunities discussed in this commentary. Click here and I will prepare a complimentary, no-obligation, custom-tailored set of portfolio recommendations designed to specifically meet your investment needs . Thank you. Ty can be reached at: tyandros@TraderView.com or at +1.312.338.7800

Tedbits is authored by Theodore "Ty" Andros , and is registered with TraderView, a registered CTA (Commodity Trading Advisor) and Global Asset Advisors (Introducing Broker). TraderView is a managed futures and alternative investment boutique. Mr. Andros began his commodity career in the early 1980's and became a managed futures specialist beginning in 1985. Mr. Andros duties include marketing, sales, and portfolio selection and monitoring, customer relations and all aspects required in building a successful managed futures and alternative investment brokerage service. Mr. Andros attended the University of San Di ego , and the University of Miami , majoring in Marketing, Economics and Business Administration. He began his career as a broker in 1983, and has worked his way to the creation of TraderView. Mr. Andros is active in Economic analysis and brings this information and analysis to his clients on a regular basis, creating investment portfolios designed to capture these unfolding opportunities as the emerge. Ty prides himself on his personal preparation for the markets as they unfold and his ability to take this information and build professionally managed portfolios. Developing a loyal clientele.

Disclaimer - This report may include information obtained from sources believed to be reliable and accurate as of the date of this publication, but no independent verification has been made to ensure its accuracy or completeness. Opinions expressed are subject to change without notice. This report is not a request to engage in any transaction involving the purchase or sale of futures contracts or options on futures. There is a substantial risk of loss associated with trading futures, foreign exchange, and options on futures. This letter is not intended as investment advice, and its use in any respect is entirely the responsibility of the user. Past performance is never a guarantee of future results.

Ty Andros Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.