New 'LBMA Silver Price' - Still Not Transparent

Commodities / Gold and Silver 2014 Aug 15, 2014 - 08:47 PM GMTBy: GoldCore

Today’s LBMA silver price was USD 19.86 per ounce. Yesterday’s LBMA silver fix was USD 19.86 per ounce.

Today’s LBMA silver price was USD 19.86 per ounce. Yesterday’s LBMA silver fix was USD 19.86 per ounce.

Gold and silver remained in lockdown today and yesterday - gold rose a tiny $1.40 yesterday to $1,313.00/oz and silver a marginal 8 cents to $19.92/oz.

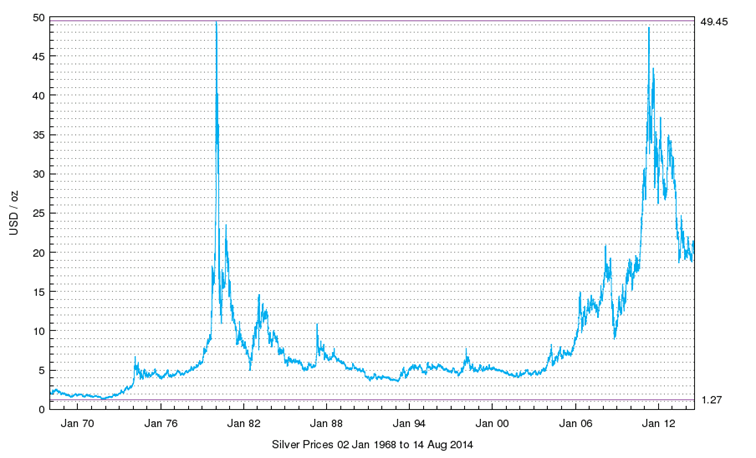

Silver in US Dollars (1970 to Today) - LBMA

Overnight, silver and gold in singapore were flat as they were in London prior and after the new ‘LBMA silver price’. Futures trading volume has picked up and was about average for the past 100 days this morning. Gold and silver remain in very tight ranges which usually precedes a sharp move higher or lower. Given the poor economic data recently and geopolitical backdrop we expect gold and silver to break higher in the coming days as we enter the seasonal sweet spot for gold and silver.

Silver for immediate delivery was flat at to $19.90 an ounce. Spot platinum fee 0.3% to $1,466 an ounce, while palladium moved 0.4% higher to $888 an ounce - closer to multi year nominal highs.

Geopolitical risk continues to support gold and silver at these levels. Macroeconomic risk was shown in the poor European growth data yesterday with the German and French economies still having severe difficulties.

New ‘LBMA Silver Price’ - Still Not Transparent

Executive Summary

- New LBMA Silver Price process began today at 1200 using electronic auction process run by CME

- LBMA Silver price today was $19.86/oz. LBMA silver fix price was $19.86.

- Only 3 participants to begin with -- HSBC, ScotiaMocatta and Mitsui

- Volumes stood at 525,000 ounces on sell side and 325,000 ounces on the buy side, Thomson Reuters

- Administration and governance of new LSP being managed by Thomson Reuters

- LBMA owns the intellectual property rights of LSP and will accredit market participants

- Silver market nervous as full list of participants is still unknown

- Traders nervous since new system/platform looks unwieldy and unintuitive

- Banks, other users of silver benchmark rushing through legal, compliance and IT changes

- LBMA consultation in last three months has not been transparent

- LBMA on-line survey results didn’t adequately explain the answers to the questions asked

- LBMA presentation seminar (June 20) held behind closed doors under Chatham House Rule

- Rationale for choosing CME/Reuters not adequately explained beyond generalisms

- “Independent” review of new silver price process conducted by ex-Barclays director while Barclays rigging gold price

- CME/Reuters declined to publicise winning submission slide presentation on LBMA site

- LBMA silver price consultation process was not transparent

- New electronic pricing mechanism not transparent and lacks regulatory oversight

- The last ever London silver fixing took place yesterday at 12 noon. After 117 years of being conducted in a consistent manner since 1897, today saw the introduction of new price discovery for the London silver price which at the last minute has been called the LBMA Silver Price.

Gold fixing at NM Rothschild and Sons began in September 1919 (Credit: courtesy NM Rothschild) “There are no flags, and we’re fixed.” Making money the old fashioned way with low frequency gold trading originated at N. M. Rothschild. The faces may change, but the furniture stays the same.

In fact, the new official name of the ‘process’ was to be the London Silver Price (LSP) as opposed to the previous title, the London Silver Fixing. Notably, the word fixing is no longer in the description for obvious reasons. The website of the London Silver Fixing Company (www.silverfixing.com) is down either due to an increase in traffic or have been switched off since it’s currently inaccessible.

The LBMA commenting on why the benchmark's name changed just today from the London Silver Price said that: "Unfortunately, that name was not able to be trademarked and therefore in order to protect the bullion market’s IP and ensure recognition that it is a daily silver spot price for the London Bullion Market, the name has been changed to the LBMA Silver Price. Thomson Reuters remains the benchmark administrator, the name is to reflect Loco London and the LBMA’s ownership of the IP."

End of the Silver Fix? When the London Silver Market Fixing Company announced on 14th May that they would cease to administer the existing Silver Fixing process on 14th August (a three month notice period), the London Bullion Market Association (LBMA) immediately stepped in on the same day (14th May) and announced that the LBMA would be launching a consultation “in order to ensure the best way forward for a London silver daily price mechanism”.

It’s not entirely clear how the LBMA could know to step in at such notice on 14th May and begin an uncontested consultation process less than a few hours after an entirely separate organisation, the London Silver Market Fixing Company Ltd, announced that they were bowing out of the process. Perhaps the two organisations are not as distinct as they maintain to be.

The overlap in bullion bank membership of the two organisations attests to some very close connections.

Throughout the new silver pricing “consultation” between mid-May and mid-August, the LBMA have maintained that they have been striving for transparency. But the process has been anything but transparent.

During the last few days it has become apparent that the entire formulation and implementation of the new silver pricing process appears to have been rushed through, with market participants now fearful that

a) they won’t understand the new system since it’s not user friendly,

b) there is no clear information about the number and type of market participants that will be contributing to the price setting process, and

c) it may not be able to provide a silver price benchmark for the myriad users who are depending on a silver price benchmark in order to price and hedge their silver products and act as a reference point for their contracts that previously used the existing London Silver Fixing price.

Indeed, the LBMA have just updated their website regarding the newly selected administrators and governors of the silver price process, CME/Thomson Reuters, stating that “the process has been undertaken quickly and efficiently but the tight schedule and the time of the year has imposed time constraints on some potential participants seeking internal signoff on the necessary credit, legal, compliance and IT requirements. This means that not all those who have participated in the live trails will be accredited in time to participate on 15th August.”

This in itself is ludicrous. Why, given the time of year and the tight schedule, have the LBMA tried to railroad these changes through right now? There has been no public explanation as to why they have continued to try to push through this new process, especially in the last two weeks.

This morning (August 15th) for the first time, the LBMA published the names of accredited participants in the new process. It is highly irregular that they have left the publication of the participants list until a few hours before the very first ever new silver price setting process. The LBMA states hopefully that they expect this participant list to grow over the coming weeks.

But the questions remains, why were the LBMA exclusively involved in this whole process in the first place from the 14th May, and why are they now rushing through a system that the market appears to have doubts about, using a consultation process that was far from transparent?

During the past week, silver market participants have been more than scathing about what they see as ill-preparedness by the LBMA and the winning bidder CME/Thomson Reuters.

For example, last Tuesday 12th August, Ross Norman, a veteran precious metals trader in the London markets and a colleague of many other experienced precious metals traders said that “it remains a mystery who will be taking the fix orders – with a deafening silence from market participants.”

Norman also highlighted the totally bizarre change in the standard unit of a silver order in the new system, which has gone from US dollars per ounce, to a unit of ‘lakh’ which is 100,000 ounces.

Ross, who began his career working for Sir Clive Sinclair of Sinclair Research in Cambridge, even likened the user interface of the new CME/Thomson Reuters silver trading platform to something from a command prompt MS-Dos user interface from the 1970s.

He also pointed out, what to us looks like a conflict of interest for Reuters, that to follow the new silver setting process in real time, one needs to purchase a subscription to the Reuters Eikon (or Elektron) platform, and given that Thomson Reuters is responsible for administration and governance of the new price setting process, they will also benefit from users signing up to these platforms in order to follow the silver auctions.

The new auction platform was not favourably received by various London based precious metals traders, as relayed by Ross Norman, but the language used was quite colourful so we will leave it to readers to search for these references.

On Wednesday last 13th August, Courtney Lynn, Treasurer at Coeur Mining, was interviewed by Kitco News on the new silver price process and said the following in relation to the market’s preparedness for the switchover; “We expected challenges in getting there, there’s a lot of legal documentation, IT challenges that need to be worked out, and I know that all the banks are working full steam ahead to get there by Friday."

Lynn explained that Coeur “use the silver fix in three different ways. We sell our metal on the fix, we hedge our metal against the fix, and we also use the benchmark in our royalty agreements for calculating royalty payments.”

Courtney Lynn went on to say that “A new process was needed, really to mitigate a lot of risk to the banks, and limit the regulatory, legal and reputational risk that they face. It’s similar to LIBOR where you had a small group of banks setting a benchmark for a large industry….. It was somewhat surprising, the timing I guess, and the abrupt transition, but it needed to happen.”

“In this sort of environment and consultation process, we’ve tried to talk through what’s important to us and communicate that to the industry and specifically the LBMA, because the LBMA represents largely banks and the banks have a big voice to begin with…we make sure…. that we had a seat at the table and made sure than our interests were met as well.”

Finally, Ross Norman stated succinctly on the new change, that “one is left to ponder whether this has done anything to address the requirement for efficiency and transparency”.

This is exactly our point in the discussion which follows.

Below, we illustrate using multiple examples, exactly why this LBMA silver price consultation process was far from transparent, even as the LBMA continues to maintain the fiction that the process has been transparent.

Part of the LBMA consultation consisted of an online survey which was launched on 16th May, two days after the LBMA became involved, the survey closing date of 30th May.

The LBMA online survey consisted of seven questions in three sections. The first section addressed the existing fixing process and asked three questions under the title ‘Feedback on use of Current Price”.

The remaining two sections solicited the participants’ opinions about the future of the silver fixing process. One of these sections with two questions was titled “Possible improvements to London Silver Price mechanism”, while the other section, also with two questions, was headed “Silver Price Contributors”.

On 23rd May, a week before the survey closing date, the LBMA published a press release providing an update on the online survey, saying that the survey had at that time received over 250 responses and that market respondents indicated “the need for transparency and wider participation in any future price discovery mechanism”.

On 5th June, the LBMA announced the final results of the survey, stating that based on over 440 survey responses:

“the general consensus was that the silver pricing mechanism should be an electronic, auction - based solution. The solution must be tradeable, with an increased number of direct participants. More specifically, the responses to each of the questions are summarised below:”

However, the LBMA press release then only proceeded to summarise the responses to four of the seven survey questions, these being the simple yes/no, multiple choice, and 1-10 ranking questions.

There was no reference in the press release to the fact that there had been three additional questions in the survey about the future of the silver fixing, and misleadingly, the LBMA listed their summarised questions/answers as Q1, Q2, Q3, and Q4, as if there had only ever been four questions in the survey.

More importantly, of the four questions that the LBMA’s answer summary did mention, three of these were related to the existing process “Feedback on use of current price”, and only one related to the future process, a quite innocuous question, namely “Would you consider acting as a contributor?”

The three questions that were arguably the most critical questions in the survey were simply not addressed or even mentioned by the LBMA. These three questions were:

“What new improvements would you like to see/recommend?”

“What are the essential features that you would like to see in any replacement?”

“Which market participants would be the ideal contributors to the pricing mechanism (e.g. bullion banks, government mints, refiners, miners, manufacturers, brokers, others)?”

Meet the new fix - Same as the old fix?

Not only was there no mention of the fact that these three questions even existed in the survey, but having the responses of over 440 survey respondents to three critical questions on the future of the silver pricing mechanism simply reduced to a few buzz words of a “general consensus” for an “electronic, auction - based solution” “tradable” with an “increased number of direct participants” is, in our view, not very transparent. In fact, it’s quite misleading.

What happened to the non-consensus views amongst the respondents?

What happened to the varied list of improvements and essential features which a sample of 440 respondents would surely have suggested?

And perhaps most importantly, what happened to the answers which would have identified which market participants would make ‘ideal contributors’?

It’s interesting that the LBMA phrased the question on ideal contributors as a leading question, prompting with some examples and listing ‘bullion banks’ first. This is quite ironic given that bullion banks are the very entities who perpetuated the downfall of the existing silver fixing process, and who have in other fixings, such as the gold fixing, been seen to be far from ‘ideal contributors’.

Without acknowledging any dissenting views on 5th June, the LBMA then proceeded full steam ahead, on the same day, to launch a ‘Request for Proposals’ (RfP) for companies that might be interested in ‘administering’ this new electronic, auction based, silver price discovery process.

They also announced on 5th June that a seminar would take place on 20th June so that LBMA members could give feedback on the proposals submitted by potential administrators.

On 19th June, the LBMA announced that the seminar, to take place the next day on 20th June, would be open to LBMA members, ISDA members, and other bullion market participants, and that the Bank of England and Financial Conduct Authority (FCA) would attend the seminar as ‘observers’.

Crucially, the LBMA statement said that the seminar would take place under the Chatham House Rule. According to Wikipedia, the Chatham House Rule “is a system for holding debates and discussion panels on controversial issues.”

“Under the Chatham House Rule, anyone who comes to the meeting is free to use information from the discussion, but is not allowed to reveal who made any comment.”

Hardly the makings of transparency. By holding the silver price seminar under the Chatham House Rule, how does this support the “need for transparency” that market participants in the survey indicated that they desperately desired?

And why the Bank of England needs to be at a silver price seminar when they hold little or no custody of silver is anybody’s guess. Perhaps the Bank of England still views silver as a monetary metal and as an important strategic asset?

Furthermore, on what basis did the LBMA think that the seminar might get into the discussion of controversial issues that would require the use of the Chatham House Rule? After all, they had stated only two week previously that there was a ‘consensus view’ on an ‘electronic, auction based system’.

In their statement on 19th June, the LBMA revealed that the seminar would host presentations by potential solution providers for the London Silver Price mechanism. Participants would be given a follow up survey in which to give their feedback, but, according to the press releases, only LBMA members would “be asked to confirm which solution they will be willing to participate in with effect from 15th August”.

This would seem to suggest that, in the eyes of the LBMA, only LBMA members actually had a real say in which system would be chosen and not the wider silver market.

It was on this day also that it was also revealed that there had been submissions to the LBMA from ten solutions providers that were interested in administering the silver price process, but that only seven of these ten had made the short list, and that only these seven would be presenting at the seminar.

There was no mention of who the three unsuccessful applicants were.

The short list consisted of the London Metal Exchange (LME), CME Group / Thomson Reuters, Intercontinental Exchange (ICE), ETF Securities, Bloomberg, Autilla Ltd (Cinnober Financial Technology of Sweden) and Platts.

The solutions of these seven applicants were said to have met the criteria of the LBMA’s Request for Proposal, which were revealed to be that a solution provider Proposal be electronic, auction-based and, ‘auditable’.

On 19th June, the LBMA also announced that “Executive summaries of the proposed solutions will be circulated to the press by the LBMA early next week”. More interestingly, they said that:

“Copies of (the next day’s) presentations will be posted on the Members’ Section of the LBMA website”.

Again, this does not sound very transparent, that all seven presentations of the seven solutions providers would only be made available to LBMA members and not to the wider market.

On Friday 11th July, the LBMA announced that CME Group and Thomson Reuters had been selected to ‘provide the solution’ for the London Silver Price mechanism “following the market consensus that has recently emerged”.

It appears that by 11th July, a ‘general consensus’ had suddenly turned into a ‘market consensus’ since, after “numerous meetings with market participants, solution providers and regulators”, “the second survey indicated a clear market consensus for the CME Group & Thomson Reuters proposal”.

The LBMA said that the CME/Reuters proposal met the Proposal criteria “as it is electronic, auction-based and auditable. It is also tradeable with an increased number of direct participants.”

But surely all seven shortlisted proposals met the Proposal criteria? In fact, all seven proposals did meet the criteria; that was why they were on the short list in the first place (see 19th June LBMA statement about the short list).

Stating that there was a “clear market consensus” for CME/Reuters without backing it up, is about as transparent as saying that there was initially a “general consensus” for an electronic auction platform; i.e. neither statement is transparent without publically available supporting evidence, of which there was none.

The LBMA statement on 11th July also said that the market consensus was supported by an “independent review” of the seven short listed companies by Jonathan Spall of G Cubed Metals Ltd.

This is the same Jonathan Spall who was a director of the London Gold Market Fixing Company until earlier this year, and who worked on the precious metals trading desk in Barclays commodities division in London until earlier this year, alongside precious metals trader Daniel Plunkett, and head of gold spot trading Marc Weber at Barclays.

Plunkett, it will be recalled, was fined by the FCA in May 2014 for manipulating the London gold price fixing process in 2012, and struck off the FSA Register, and also caused Barclays to be substantially fined.

Weber departed Barclays abruptly earlier this year. Barclays has the distinction of being the only bullion bank to have been fined by the FCA for gold market manipulation, and Plunkett has the dubious distinction of being the only gold trader in London to have been fined for manipulation of the gold price fixing.

The LBMA stated that feedback from the surveys, the submissions and “the conclusions of the independent review” “were presented directly to a meeting of the LBMA Management Committee, LBMA Market Makers and the Data Working Group.” Again, where is the transparency in this, and why was the wider market not privy to these presentations to the LBMA?

On 24th June, the LBMA published some presentation material from the proposals of the seven shortlisted solutions providers who had presented at the seminar on 20th June. Specifically, the LBMA stated “Seven proposals were presented at the seminar, executive summaries and/or slides (as appropriate) are set out below:”

However, when you view the selection of material that the LBMA published on its site for each of the seven applicants, it quickly becomes apparent that the material released by each applicant is not standardised or consistent.

Autilla allowed the LBMA to publish their slides and their executive summary. Platts allowed the publication of their slides. ETF allowed the publication of their slides and their original RfP response. However, Bloomberg, the LME, ICE and CME/Reuters only allowed publication of their executive summaries.

Recall from 19th June that the LBMA had said that “Executive summaries of the proposed solutions will be circulated to the press by the LBMA early next week”, but that “Copies of presentations will be posted on the Members’ Section of the LBMA website” (see reference below).

When asked last month as to why the slides of the LME, ICE, Bloomberg and CME/Reuters were not published on the public section (media centre) of their web site, the LBMA replied that the seven applicants were very specific about what they would allow be advertised on the LBMA web site and that the LBMA followed their instructions when posting the material.

For the winning entry, CME/Reuters, the LBMA reasoned that the CME/Reuters, by not publishing their slides, were protecting the specification and software of their offering. Given that the presentations all appear to have been “posted on the members’ Section of the LBMA website’, this again begs the question, where is the transparency in this new silver price setting process?

Conclusion

The entire process has been a bit of a shambles. The Gold Anti Trust Action Committee (GATA) and those concerned about price manipulation will allege that the LBMA and the western bullion banks are engaged in a rebranding and repackaging exercise in order to maintain a cosy gold and silver cartel of bullion banks and ultimately control over precious metal prices.

If the CME/Reuters aren’t willing to share with the public the presentation that they made at a closed door seminar, especially since they won the competition and are now running the process, what hope is there for transparency in this new process?

Sharelynx

Nobody really knows how this new CME auction system works, how it’s coded, who programmed it, and how the prices are really set. Also, nobody seems to know how the new system is administered and governed and how interested 3rd parties in the market can see the auction in action without signing up to a proprietary Thomson Reuters system.

It is difficult for the LBMA to claim that the new silver pricing process is transparent. Thomson Reuters need to be careful that they are not being used to rubber stamp the new LBMA silver pricing mechanism. Regulators need to look at the process and institute a new pricing mechanism and ensure that the price of silver is based on real physical precious metals supply and demand between government mints, refiners, miners, manufacturers, jewellers and of course investors.

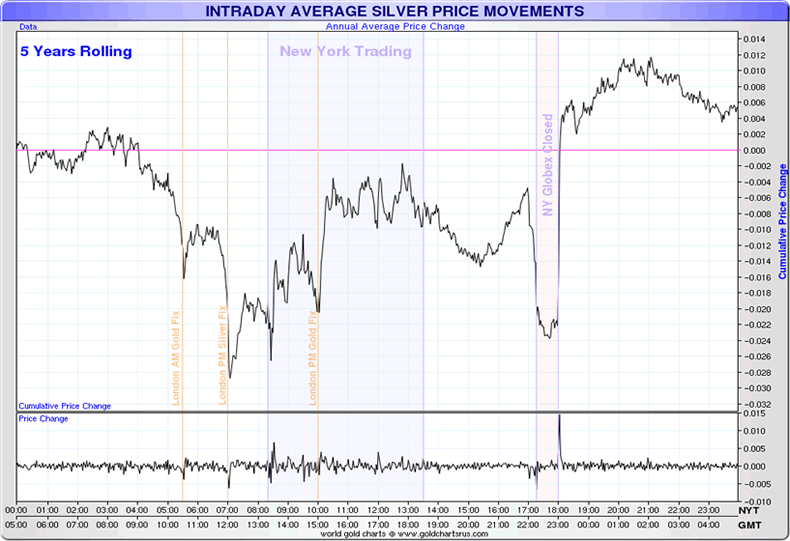

Silver in Dollars - 5 Years (Thomson Reuters)

As gold and silver moves East, western institutions are gradually losing their grip on the precious metals markets. The advent of new gold exchanges with physical gold settlement such as the new gold and silver exchanges in Dubai, Shanghai and of course Singapore will make price discovery more efficient and render price manipulation more difficult.

The physical market and the natural forces of supply and demand will soon overcome the paper and digital gold markets.

By Ronan Manley, GoldCore Consultant

References

London Silver Market Fixing Company Ltd announces end of silver fixing, 14th May

http://www.reuters.com/article/2014/05/14/idUSnMKWWsY3ca+1e8+MKW20140514

LBMA announcement on The London Silver Market, 14th May

http://www.lbma.org.uk/_blog/lbma_media_centre/post/the-london-silver-ma...

LBMA announces London Silver Price - market consultation, 16th May

http://www.lbma.org.uk/_blog/lbma_media_centre/post/MARKETCONSULTATION/

LBMA announces London Silver Price – consultation update, 23rd May

http://www.lbma.org.uk/_blog/lbma_media_centre/post/consultationupdate/

LBMA announces London Silver Price consultation survey results, 5th June

http://www.lbma.org.uk/_blog/lbma_media_centre/post/SILVER_SURVEY_RESULTS/

LBMA announcement about the 20th June silver price seminar, 19th June

http://www.lbma.org.uk/_blog/lbma_media_centre/post/seminarupdate/

LBMA silver price solution - CME Group and Thomson Reuters

http://www.lbma.org.uk/_blog/lbma_media_centre/post/silverpricesolution/

LBMA 2014 Silver Price Consultation Seminar

http://www.lbma.org.uk/_blog/lbma_media_centre/post/lbma-2014-silver-pri...

This update can be found on the GoldCore blog here.

Yours sincerely,

Mark O'Byrne

Exective Director

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information contained in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.