How Safe Are Unallocated Gold Bullion Accounts?

Commodities / Gold and Silver 2014 Jul 31, 2014 - 07:44 PM GMTBy: Submissions

Imagine you owned a small business. It’s a retail store and you sell a physical product which lines the shelves. You need to keep a variety of different products to ensure that customers who enter your store have plenty of choice. Not only do you have to stock a range of goods, but you have to keep a lot of each on hand as customers often purchase in bulk, due to fluctuating prices (they may buy large quantities when they believe it is well priced). As the store owner you have to hedge your exposure to the fluctuating price of the product you keep on hand to reduce the chance of getting caught on the wrong side of a price swing, this adds further complexity to managing your inventory.

Imagine you owned a small business. It’s a retail store and you sell a physical product which lines the shelves. You need to keep a variety of different products to ensure that customers who enter your store have plenty of choice. Not only do you have to stock a range of goods, but you have to keep a lot of each on hand as customers often purchase in bulk, due to fluctuating prices (they may buy large quantities when they believe it is well priced). As the store owner you have to hedge your exposure to the fluctuating price of the product you keep on hand to reduce the chance of getting caught on the wrong side of a price swing, this adds further complexity to managing your inventory.

The products you sell are expensive, this is no $2 store where your entire inventory only totals a few thousand dollars, almost all of your products cost over $20 each and up to $44,000 or more, remembering that you have to keep multiple of each in stock for those customers who want to purchase in bulk. The worst of it is you can only charge a small mark-up on the products (over cost price), otherwise your customers will go elsewhere. Obviously the capital you need for running this store will be substantial. Likely to be in the millions of dollars.

Now imagine there was a way to offer such a wide selection of expensive products, but have your customers fund the capital costs to do so… sounds too good to be true?! They will essentially pre-purchase your stock (allowing them to lock in the price they want), which provides substantial capital for putting product on your shelves. The customer can come in and use their store credit to make a purchase from your product range and take delivery at a time of their choosing. All you have to do as the store owner is promise your customers that you won’t take more funds from them than you have product on your shelves.

…you’ve probably worked out by now that I’m talking about the challenges faced by a bullion dealer. I have a lot of respect for those in the industry, it’s a cut-throat business with small margins and high volumes, lots of regulations to abide by and is littered with risks. However, as a consumer of their services, I have to think about the safety of my own capital first.

The solution I talk about above, where the customer can provide capital for stocking a larger product range, is unallocated bullion accounts. Unallocated accounts have become a popular offering from bullion dealers in Australia over the last few years, I suspect this is partially a result of an increase in the number of bullion dealers trading and also boosted by the closure of new funds to Perth Mint’s Unallocated Accounts (March 2011). The advance in functionality of bullion dealers online stores means the process to buy unallocated metal today is very easy, sign up an account, hit the buy button and transfer the money to the dealer’s bank account.

There are some benefits for a customer purchasing unallocated metal (as opposed to taking delivery of physical). There’s generally no cost charged for storage, the premium (over spot) charged will be lower allowing exposure to a larger number of ounces (e.g. $5000 buys 192 1 ounce silver coins at $26/oz, but buys 208 ounces of unallocated Silver at $24/oz), you don’t have to pay for delivery and it’s easier to trade (for example a dealer may offer Gold:Silver Ratio swaps or to buy it back at the click of a button). I have used unallocated accounts from two Australian bullion dealers in the past and may do so in the future, but I manage the risk by limiting my exposure to an amount I'd feel comfortable losing (the same amount that I'd risk placing any single order with a dealer).

This brings me to the problem I have with unallocated accounts. One of the reasons I own precious metals is that they have a lower level of counter-party risk compared with traditional assets such as shares. Buying precious metals in unallocated form potentially exposes the client to the solvency of the company offering the service, which is counterproductive to the reasons I hold precious metals.

The ownership (title) of the bullion in an unallocated account is a grey area and will likely differ depending on the specific setup for each dealer. I've had it explained that some bullion dealers in Australia have structured their unallocated products so that the client retains ownership of the metal in the event of bankruptcy, but I'm not an accountant or lawyer, so even if I was shown 'proof' of these claims I'd not trust myself to be confident that was definitely the case. I haven't seen any bullion dealer with a Product Disclosure Statement on their website outlining the offer, ownership structure, how the metal is treated and risks, most of them provide little more than a few sentences describing their unallocated products.

After reading the above you may be wondering how likely is the collapse of a well established bullion dealer offering an unallocated product?

It's not something that has occurred very often, the last recorded instance that I've been made aware of was back in 1996 with the collapse of "Perth Bullion Exchange" (of Sydney, not to be confused with any current trading entities with similar names). This particular case was highlighted in a Sunday Mail article where a couple had written to "The Fixer". They had purchased 20 bars of silver bullion totaling $12,900 (in 1993-1994) for which they had certificates showing ownership and when they went to redeem their metal in 1998 the business had vanished. The Fixer managed to track down the bankruptcy proceedings and the couple supposedly got around half their money back following the sale of the companies assets:

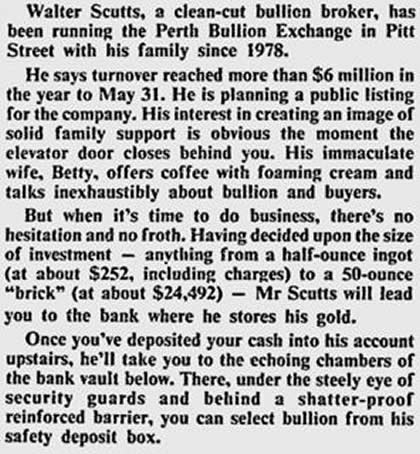

Perth Bullion Exchange had been trading for some 18 years at the time of their bankruptcy (via records of the bankruptcy proceedings). Over those years they had offered various services that would be comparable to some unallocated accounts today (keeping in mind that all dealers do things a little differently). Early on their certificates of ownership stated that "THE ABOVE INGOT IS BEING STORED BY THIS EXCHANGE - FULLY COVERED BY INSURANCE AND FREE OF STORAGE CHARGE UNTIL REQUIRED", other customers had received notification that "The Perth Bullion Exchange agrees to store these ingots free of charge under the best security available on the condition that we may use the physical bullion in the normal course of our business". As prices for bullion fell and the bankrupt's business deteriorated, the owner progressively sold all his stock of bullion. At the date of the sequestration order, the bankrupt was in possession of various giftware, jewellery, fixtures and fittings (but no bullion).

There was little warning of Perth Bullion Exchange's demise, in fact just several months prior the Sydney Morning Herald ran a positive article (read in full here) on the company describing a proprietor who was interested in floating the company publicly:

Another example, this time in New Zealand, was that of Goldcorp Exchange Ltd, Wikipedia summarises:

Goldcorp Exchange Ltd had a business of holding gold reserves in coins and ingots for customers wishing to invest in gold. Some gold was held for customers, but the levels varied from time to time. The company's employees also told customers that the company would maintain a separate and sufficient stock of each type of bullion to meet their demands, but in fact it did not. The Bank of New Zealand on 11 July 1988, being owed money by Goldcorp Exchange Ltd, petitioned for the business to be wound up. It transpired that Goldcorp had not held anywhere near enough money for the members of the public, around 1000 people, who had supposedly bought gold with it, even though in their contracts they were entitled to delivery of the gold (in 7 days, for a fee) if they wished. The company also lacked enough assets to satisfy the debts to the bank. The members of the public alleged that the gold that remained in stock was entrusted to them. The bank argued that because the gold stocks had never been isolated, it did not, that all the gold customers were unsecured creditors and that its security interest (a floating charge) took priority.

In this case, there was Gold remaining in stock at the time of their bankruptcy but the title of the metal hadn't been structured to verify ownership by the clients holding unallocated accounts. An early brochure read "Basically you agree to buy metal at the prevailing market rate and a paper transaction takes place. [The company] is responsible for storing and insuring your metal free of charge and you are given a 'Non-Allocated invoice' which verifies your ownership of the metal. In the case of gold or silver, physical delivery can be taken upon seven days notice and payment of nominal delivery charges." (via records of the bankruptcy proceeding), but the judgement was made:

The Privy Council advised that the customers had no property interest in the gold, and therefore the bank could use it to satisfy its debts. The customers' purchase contracts did not transfer title, because which gold specifically was to be sold was not yet certain. Although Goldcorp's brochures had promised title, a trust did not arise because there was no declaration of it. It was contrary to policy to imply a fiduciary duty simply because there was a breach of contract. It was also rejected that equity required any restitution of the purchase money.

Both of these examples are very dated. One might look at these precedents and think that recurrence is unlikely today. However, my current concern lies with the recent revelation of missing Gold and suspected tax fraud occurring as previously covered on this site in my article 'ATO & AFP Investigate Australian Gold Industry Fraud'.

I don't know what will come of this investigation and those companies named in the exposé by Chris Vedelago, but the potential for some of them to suffer losses (or potentially worse) as a result of these events seems worthy of consideration. As far as I know ATO garnishee notices take priority over other creditors, so unlike the New Zealand case detailed above, you'd want to be sure that the customer ownership of any metal in unallocated accounts was air tight if you have a substantial holding in this form.

This article was not written with the intent to panic those investors with unallocated accounts, but simply to draw attention to the risks associated with having another party store your precious metals. In the case of outright theft of customer metal, which seems to be what occurred in the case of Perth Bullion Exchange, allocated accounts aren't completely safe either. However, even if bullion dealers offering unallocated accounts do everything by the book and are a reputable long-standing business, they may inadvertently expose themselves to external risks that put their company and the unallocated accounts of their clients at risk.

I said in another recent article '7 Ways To Keep Your Gold And Silver Safe' that "there is no completely risk free way to own precious metals, as is the case with any other investment", it's just a matter of assessing the risks of the various options available and judging for yourself which you think is safest.

Bullion Baron

An Australian blogger (BullionBaron.com) & tweeting (;@BullionBaron) on various topics including precious metals, finance, property & the monetary system. A rational gold bug who seeks the truth (wherever that may lead), while attempting to avoid unverifiable conspiratorial content.

The above article originally published here: http://www.bullionbaron.com/2014/07/how-safe-are-unallocated-bullion.html

© 2014 Copyright Bullion Baron - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.