Smart Money, Dumb Money & Your Money - Bond Market End Game

Stock-Markets / Financial Markets 2014 Jun 26, 2014 - 01:34 PM GMTBy: Darryl_R_Schoon

Crime is far more common than logic. This is the refuge of bankers.

Crime is far more common than logic. This is the refuge of bankers.

In capitalism’s end game, leveraged debt fatally destabilizes the supply and demand dynamic necessary for stable economic activity. Understanding this is critical to understanding why capitalism today is failing.

In the banker’s ponzi-scheme of credit and debt, debt-based money is created through central bank credit. Usually, the central banks’ constant expansion of the money supply results in rising prices, i.e. inflation. In the end game, however, this is no longer true.

In the end game, when demand slows, excess supply forces prices lower resulting in a deflationary trend called low inflation. In the end game, low inflation continues until demand falls so low the velocity of money is no longer sufficient to support aggregate economic activity; a monetary phenomena that ends ina catastrophic deflationary depression similar to hypotension, a medical condition where blood pressure falls until fatal.

In June 2009 I wrote in my article, Bull Markets, Bullsh*t and Bubbles:

Deflation arises in the wake of extraordinary speculative bubbles and is caused by a collapse in demand which happens after such bubbles pop, when producers/sellers chase buyers hoping to turn inventories and soon-to-be illiquid assets into cash in order to pay down ever-compounding debts.

Deflation happened in the 1930s in the Great Depression, in the 1990s [through today] in Japan and is now again spreading in the US, the UK, [the EU] and other overly mature late-stage capitalist economies; and akin to a deadly economic cancer, deflation, once metastasized, is exceedingly difficult to eliminate.

…The serial dot.com and US real estate bubbles so distorted the global demand and supply dynamic that memories of the 1930s depression have now been re-awakened, memories that will soon become reality as deflation spreads around the world.

…Bubbles and busts have now replaced the expansions and contractions common to early stage capitalism. We are now in late-stage capitalism, where debt instead of credit is the critical factor and the bond markets, not equity markets, determine the economic future.

CONFUSION IN TODAY’S MARKETS

Today, when it looks like a bull, walks like a bull and acts like a bull, it's probably a bubble. –Bull Markets, Bullsh*t and Bubbles, DRS, 2009

In late-stage capitalism, stock market highs are like a tan on a dying man. Investors formerly seduced by higher stock prices abandon equities as chances of a bubble bursting increase. When this happens, investors move into bonds—capital’s safe haven of choice. In the end game, however, bond markets are where the final bloodbath of capitalism’s debt-based money will take place.

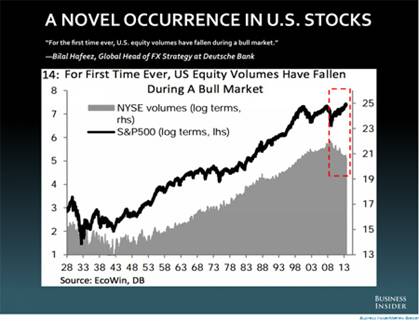

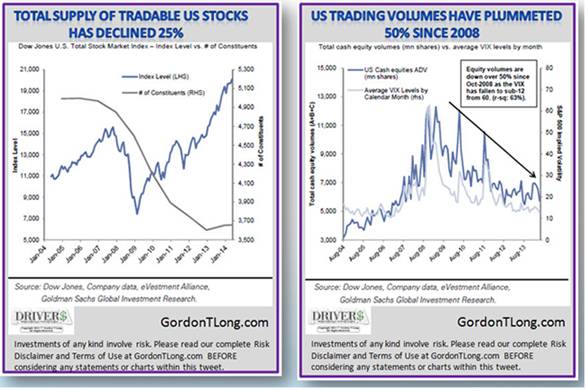

The current stock market bubble is like no other. Even though stock prices are reaching nominal highs, trading volumes are falling. This is the first time in history this has happened.

Two charts from über analyst Gordon T Long provide further evidence that stock markets today are radically different from previous markets.

Today, the Fed and other central banks are so desperate for economic growth they have exacerbated systemic instability by underwriting directly or indirectly the rise in today’s asset markets. On June 15th, the Official Monetary and Financial Institutions Forum, a central bank research and advisory group, noted that central banks and other public sector institutions have, to date, invested $29 trillion in global markets.

Regarding today’s unprecedented market conditions, on June 16th, Citigroup strategists led by Matt King in London wrote: We blame the wave of central-bank liquidity, which has pushed up asset prices irrespective of fundamentals…This creates a vicious circle: ever-higher prices, ever-less trading and liquidity.

Not only has the Fed’s unprecedented and artificial insemination of liquidity distorted equities, bonds, too, are grossly at variance with traditional metrics. On June 2nd, Bloomberg News reported: After unprecedented stimulus by the Fed and other central banks made many traditional models useless, investors and analysts alike are having to reshape their understanding of cheap and expensive as the global market for bonds balloons to $100 trillion.

On June 18th, Mohamed El-Erian, chief economic advisor to Allianz and former co-CEO of PIMCO, the world’s largest bond fund, warned investors of dangers regarding continued central bank support of markets. El-Erian advised: …rather than continuously increasing exposure to ever-rising markets, it is time for highly exposed investors to gradually take some chips off the table.

Instead of betting vast sums on an uncertain future in uncertain markets, smart money institutional investors are now, as El-Erian advised, taking some chips off the table. The dumb money, i.e. private/retail investors, however, are still, literally, buying the bull.

As the odds of systemic collapse rise, safety becomes paramount, even when such safety offers little or no returns. Since peaking in the 1980s, US Treasury interest rates have fallen to almost zero as central banks made credit increasingly cheaper, futilely hoping that with more and cheaper credit, markets can achieve exit speed. In the end game, they can’t.

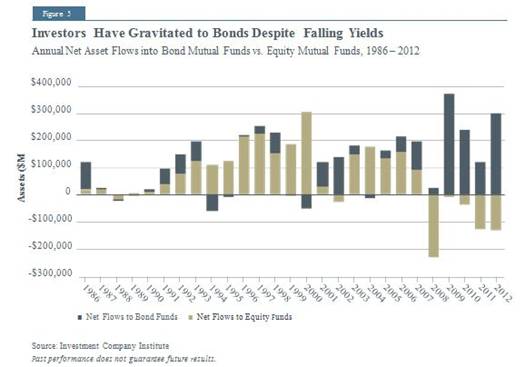

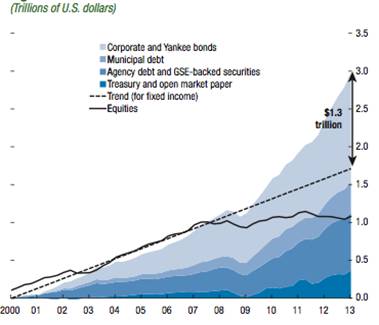

Despite today’s unprecedented lack of yield, growing distrust of liquidity-driven equity markets, investors are finding refuge in the perceived ‘safety’ of bonds.

Since 2000, investments in bonds are triple the amount invested in equities.

In the end game, the safety of bonds is as illusory as it is fatal.

THE END GAME: PANIC IN THE BOND MARKETS

In 2012, David Stockman, Ronald Reagan’s former budget director, was asked by the editors of The Gold Report what catalyst could bring the end game to a final resolution. Today, Stockman’s answer is even more relevant as the end game is even deeper into its final stage.

The Gold Report: If we are in the final innings of a debt super-cycle, what is the catalyst that will end the game?

David Stockman: I think the likely catalyst is a breakdown of the U.S. government bond market. It is the heart of the fixed income market and, therefore, the world's financial market.

Because of Fed management and interest-rate pegging, the market is artificially medicated. All of the rates and spreads are unreal. The yield curve is not market driven. Supply and demand for savings and investment, future inflation risk discounts by investors - none of these free market forces matter. The price of money is dictated by the Fed, and Wall Street merely attempts to front-run its next move.

As long as the hedge fund traders and fast-money boys believe the Fed can keep everything pegged, we may limp along. The minute they lose confidence, they will unwind their trades.

On the margin, nobody owns the Treasury bond; you rent it. Trillions of treasury paper is funded on repo: You buy $100 million (M) in Treasuries and immediately put them up as collateral for overnight borrowings of $98M. Traders can capture the spread as long as the price of the bond is stable or rising, as it has been for the last year or two. If the bond drops 2%, the spread has been wiped out.

If that happens, the massive repo structures - that is, debt owned by still more debt - will start to unwind and create a panic in the Treasury market. People will realize the emperor is naked.

TRAPPED IN THE HELL OF BOND MARKET ILLIQUIDITY

An illiquid asset is an asset which is not readily salable (without a drastic price reduction, and sometimes not at any price) due to uncertainty about its value or the lack of a market in which it is regularly traded.

http://en.wikipedia.org/wiki/Market_liquidity

The recent and spectacular growth of bond markets has brought with it an equally recent and dangerous downside, i.e. the inability of bond markets to sell what investors have bought. Should bond prices drop 2% as per David Stockman, a panic in the Treasury market will ensue as illiquid markets will prevent investors from selling their bonds as prices fall.

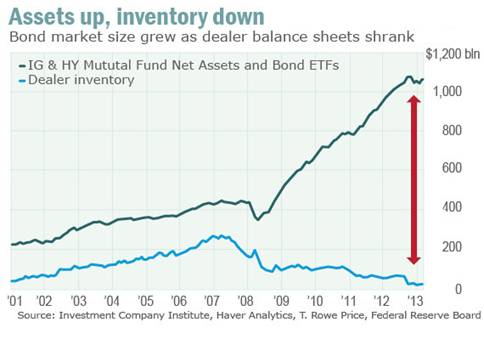

Traditionally, bond dealers provided the liquidity bond markets need to function. After the 2008 financial crisis, however, the ability of bond dealers to do so precipitously declined as the volume of bond purchases inversely grew.

In Mile wide, inch deep – bond market liquidity dries up, a MarketWatch commentary, Ben Eisen wrote: The combination of smaller holdings by dealers and a surge in the amount of outstanding corporate debt suggest that there’s more inventory to change hands with fewer institutions willing to facilitate those transactions. Whereas dealers once held about 4% of all corporate debt on their balance sheets, they now hold closer to 0.5%...

The increasing mismatch between rapidly growing markets and disappearing liquidity will end in a crisis of unprecedented proportions should interest rates rise, driving the value of previously issued bonds lower; resulting in a financial bloodbath where investors are trapped in markets unable to liquidate declining assets.

On June 24, a MoneyNews article, Bond Market Has $900 Billion Mom and Pop Problem When Rates Rise noted that …Investors have piled more than $900 billion into taxable bond funds since the 2008 financial crisis, buying stock-like shares of mutual and exchange traded funds to gain access to infrequently-traded [i.e. illiquid] markets…

If and when the Fed raises interest rates, the concern is that the price of bonds will plunge and mom and pop investors will exit bond funds, leading to an exodus that’ll cause credit markets to freeze up…and a free fall in prices.

On June 16th, the Financial Times reported: Federal Reserve officials have discussed whether regulators should impose exit fees on bond funds to avert a potential run by investors, underlining concern about the vulnerability of the $10 trillion corporate bond market…Officials are concerned that bond funds are becoming ‘shadow banks’, because investors can withdraw their money on demand, even though the assets held by the funds can be hard to sell in a crisis.

Today, credit and debt-based markets have reached their limits and no markets are safe from their coming collapse. Stocks, bonds and commodities will all fall, either serially or as one. This is the bankers’ end game.

GOLD AND SILVER AND THE COLLAPSE OF THE PRESENT PARADIGM

The banker’s house of cards is built on a foundation of paper money. In the beginning, gold and silver provided the stability that paper cannot offer. In 1971, gold was removed from the international monetary system and the cotter pin holding the bankers’ ever-towering edifice of credit and debt was no more.

We are in the end game, where paper promises have replaced the stability of gold and silver. The consequences are there for everyone to see. Equity markets, bond markets, commodity markets have all been poisoned by today’s excessive levels of credit and debt.

Gold and silver are the barometers of systemic financial distress. The bankers’ have done their utmost to disable the most telling indicators of their present disarray and imminent demise. Don’t be fooled, however. In the end game, gold and silver are not investments. They are life insurance policies and when the present system dies—and it will—the payout will justify your faith.

My present youtube video is the 3rd in my current series, Freedom and the Matrix. Once again, central banking is discussed, albeit from another angle. See http://youtu.be/sh5ljkCB5CE.

Take care of you and yours

Buy gold, buy silver, have faith.

By Darryl Robert Schoon

www.survivethecrisis.com

www.drschoon.com

blog www.posdev.net

About Darryl Robert Schoon

In college, I majored in political science with a focus on East Asia (B.A. University of California at Davis, 1966). My in-depth study of economics did not occur until much later.

In the 1990s, I became curious about the Great Depression and in the course of my study, I realized that most of my preconceptions about money and the economy were just that - preconceptions. I, like most others, did not really understand the nature of money and the economy. Now, I have some insights and answers about these critical matters.

In October 2005, Marshall Thurber, a close friend from law school convened The Positive Deviant Network (the PDN), a group of individuals whom Marshall believed to be "out-of-the-box" thinkers and I was asked to join. The PDN became a major catalyst in my writings on economic issues.

When I discovered others in the PDN shared my concerns about the US economy, I began writing down my thoughts. In March 2007 I presented my findings to the Positive Deviant Network in the form of an in-depth 148- page analysis, " How to Survive the Crisis and Prosper In The Process. "

The reception to my presentation, though controversial, generated a significant amount of interest; and in May 2007, "How To Survive The Crisis And Prosper In The Process" was made available at www.survivethecrisis.com and I began writing articles on economic issues.

The interest in the book and my writings has been gratifying. During its first two months, www.survivethecrisis.com was accessed by over 10,000 viewers from 93 countries. Clearly, we had struck a chord and www.drschoon.com , has been created to address this interest.

Darryl R Schoon Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.