US Economy No Recovery Whilst Housing Bust Continues- Gold $1200

Commodities / Gold & Silver May 07, 2008 - 06:15 AM GMTBy: Jim_Willie_CB

Once every several months, an opportunity is presented on a silver platter to purchase a spectacular investment in a strong uptrend, with loud indications of continued upward trend in price. Gold is heading well past $1200 and silver is heading well past $25 in the next several months, despite the orchestrated annihilation of honest valid reporting. How many times have the clowns on Wall Street and the financial subservient media networks claimed that the worst was over for the US Dollar, gold, the US Economy, the housing market, and bank bond losses?

Once every several months, an opportunity is presented on a silver platter to purchase a spectacular investment in a strong uptrend, with loud indications of continued upward trend in price. Gold is heading well past $1200 and silver is heading well past $25 in the next several months, despite the orchestrated annihilation of honest valid reporting. How many times have the clowns on Wall Street and the financial subservient media networks claimed that the worst was over for the US Dollar, gold, the US Economy, the housing market, and bank bond losses?

My guess is about once per year for the last five years, all wrong, and still wrong, just louder wrong now in tone. Has anything been fixed on the economy, housing, mortgages, or banks? No! The flow of US Fed repo money to banks has improved, that is all. That is not a remedy, but a bandage tourniquet, grossly misinterpreted.

Some relief has come for the US Dollar My past article pointed out a pennant pattern and imminent breakdown that did not occur. Long-term corrections are difficult to call. Prospects for fundamental improvement are not visible, but the story has been sold, and sold vigorously. The embattled buck could easily see a couple months of reprieve, one month finished, one month more to come. The heavily oversold US$ condition needed to be cleansed in order to enable another powerful downleg. US bank dilution has provided needed cash, retail sales (especially cars) have been horrendous, housing prices and inventory have been miserable, foreclosures have more than doubled nationally versus last year, home builders are slashing prices amidst mammoth losses, business capital investment is on the wane, inventory levels are building, and gasoline prices (utility bills too) have put a major crimp on consumers.

Meanwhile, the US Dollar has rallied based upon hope, prayer, and marketing. If truth be known, the Plunge Protection Team has been busy doing what they usually do best, corrupting with crucial interference in certain markets. They have been propping up the bank stocks, the homebuilder stocks, Detroit carmaker stocks, the Fannie Mae stock, and more, enough to lead to moderate rallies in the S&P500 and Dow Jones Industrial stock indexes. If truth be known, a massive coordinated effort has followed the G7 Finance Meeting, as central banks have been conducting overnight operations to prop the US Dollar The crippled world reserve currency is inflicting damage on their domestic economies like an acid rain, as their floors fall out from higher consequent domestic currency exchange rates.

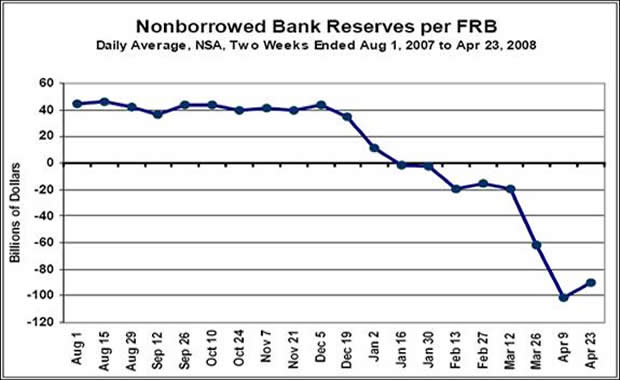

What has happened in the last few weeks, of real importance, which has made a difference? The US Federal Reserve has indeed plugged in their sizeable lending facilities. They have taken in some garbage AAA mortgage bonds, overpaid on refund prices, and had to rebalance their own bond portfolio. US banks do not face bankruptcy like several weeks ago, tied to insolvency plus illiquidity. The effect has been to improve the US bank portfolio mix, but their insolvent status remains on a non-borrowed basis. Banks in aggregate have a slightly better liquidity position, but still a negative overall condition. Big deal! The US banks have gone from minus $100 billion to minus $90 billion in non-borrowed reserves. Huh?!? The problem is fixed? Methinks not! Can banks proceed without further bond losses after housing prices have fallen during the last few months, and during the next few months? Methinks not! Another huge round of bank bond losses comes in just a few months. Be patient. The night of bond loss follows the foul day of continued home price declines.

What has happened in recent weeks seems clear. The US Govt and US Fed and US Treasury have made a deal with the devil. Primarily Arabs (much less so Asians) have been encouraged to add cash in order to keep US big banks solvent. In return, the agents from the not-so-hidden Plunge Protection Team led by the US Fed& Treasury have engineered a counter-trend rally in bank stocks and mainstream stocks. They have also solicited the cooperation of the Euro Central Bank and Band of Japan in order to engineer a counter-trend US Dollar rally, as feeble as it has been.

The smaller Bank of Canada has been very cooperative also. This all has occurred even though at the expense of UST Bonds, since something must give ground. They can corrupt most markets, but not all markets simultaneously. Lies offer cover to the portions they cannot control in concert. The BKX bank stock index has indeed risen in recent weeks. It faces some stern resistance here. It might make minor added gains. The reality of a profound wave of new bond losses will likely keep the bank stocks well chained to the mill posts. This too is covered in the upcoming May Hat Trick Letter.

The housing decline alone acts a powerful destructive force upon banks. The US Economic recession will be an equally powerful destructive force. Ordinary debts are defaulted outside the realm of housing. Vicious cycles with gripping feedback loops are at work. Bank loan portfolios on the household and commercial side are next to endure wreckage. Further monetary stimulus and federal stimulus are obvious next steps. Gold and silver will thrive. The US Dollar will be harmed much more. The only saving grace for the beleaguered buck is the triple faceted mess in England with housing, banks, and certain recession, and the imminent downturn in the European Union. Competitive currency devaluation soon will be far along. European leaders already consider the high euro to be a destructive influence. They have declared war on the US Dollar decline, and want it to recover.

USFED REBALANCE BACKFIRE

The US Federal Reserve has been forced to react to its massive underwriting of the insanity behind gutted US money center banks and investment banks, the latter of which function under different accounting rules and freedom to deceive. The effect has been to force the US Fed to issue more USTreasurys on the open market in their rebalance, since they gave away their more valuable UST Bonds in return for junk crapp bonds with AAA phony labels. The effect has been to lift US Treasury bond yields on both the 2-year and the 10-year maturity. The 2-yr TBill yield has risen from 1.50% in March to 2.40% here in May. The 10-yr TNote yield has risen from 3.40% in March to 3.90% here in May.

The rise in USTBond yields has helped the US Dollar, attracting foreign investment. The rise in the USTBond yields has led to the false notion that the US Economy is on the mend.

The US Dollar has not risen much, but it has risen. The fact that the buck has stopped falling has led many to conclude that the capital flows now favor the beleaguered buck. Foreigners still shun US Treasury auctions though. The signal of an end to US Fed official rate cuts has nothing to do with strength in the US Economy, nothing to do with restoring the fundamentals of national finances to health. It has to do with the US Fed recognizing that a falling US Dollar has been accompanied by a tragic rise in energy and food prices, along with all the carts attached. It has to do with recognizing they have used almost all their ammunition in rate cut capital.

The bull market in commodities is not over. At best it will take a breather. My contention is that major US banks are speculating in the energy market in order to repair their broken balance sheets. Certainly Goldman Sachs is. The entire story line of the worst over for the US Dollar and for the US Economy is patently false. Just one more chapter of plain propaganda by the Wall Street community, the US Federal Reserve, and the US Govt They are collectively worried to death, sweating bullets, even as precious capital blood has spilled in massive quantities. The entire US financial system has tragically turned insolvent. Inflation remains the only option left as an option, yet they cannot destroy the last standing asset group in US Treasury Bonds.

The most egregious backfire of banking flatulence has been the rise in long-term interest rates. This is precisely what the US Fed does not want, since it provides substantial headwinds for the housing & mortgage market, via higher mortgage rates. The bond market, via US Fed rebalancing, has properly priced the higher asset risk erosion from price inflation, as it should. Some have called this effect the next Bond Conundrum. Sure it is! In fact, the US Treasury complex is a maze of not just conundrums. It serves as a stark living breathing example of Goebbels (Nazi Information Minister) and Orwell (author of 1984 ) joined in a nightmarish marriage of deceit and fraud. The problem is that long-term bond yields should be over 10% since price inflation is even higher than that. Talk about an overvalued asset!!! The last bubble to burst is not crude oil and gold with the supporting cast of commodities. It is the USTBond complex. Its prices are way way way out of whack. Sure, the US Fed is trying to stimulate with lower rates. But why would any sane thinking person buy a US Treasury Bond when the real return is minus 7% to minus 8%?

GOLD OPPORTUNITY & SILVER PLATTER

The opportunities given today in gold & silver will be written about for another few years. The prices offered in early 2008 will be seen as tremendous bargains. Price bargains were last seen in August 2007, in September 2006, and in mid-2005. The breakout of gold past the elusive 700 mark foretold the rally not just to 1000 but to 2000 and higher. It unleashed a new era. Ditto for silver, which rose past the elusive 15.50 level. Doing so foretold a rally not just to 20 but to 50. Give it time. Things are unraveling. Systems are broken. Solutions are nowhere. All efforts have an inflation stench to them. Desperation has entered central banker offices.

The gold price has found support off the 200-day moving average in classic form. The triple leg correction off the 1020 high is also a classic long-term pattern. It guarantees a firm foundation for the assault on 1000 with stable success. Note how the 1000 mark was eclipsed, but from a base around 650 to 670. The next base will be 850 or so. The silver price movement and patterns are similar. However, silver is heading to the heavens in price, joining its platinum brother and palladium cousin. Gold will be stuck fighting political wars, but making strong gains. The gold/silver ratio will show pronounced improvement in favor of silver in the next two to three years. Silver is in default on a nearly global basis. COMEX delivery of silver is interfered with. Silver coin dealers have almost nothing to sell. Even the US Mint has halted production of silver eagles! So silver price has declined amidst profound shortages? The stage is set for huge up legs in the silver price. Gold will rise in concert.

The triggers for the US Dollar on the downside, and for gold & silver on the upside are more big bank bond losses. Nevermind the cause being the housing price declines. That has been ignored. When banks announce further big bond losses, the winds will change very rapidly, and with anger by the people. Rating agencies are cooperating in ways, but not offering ratings on debt securities in certain bond types. Yet they also are issuing huge downgrades of typically safe asset backed bonds. This summer will involve a very very rude awakening. The reality of recession, housing decline, and bank losses will undo the positive attitudes that are lifting the subprime US Dollar and stock prices broadly

WRONG CONCLUSION ON RECOVERY

So should we conclude that the US Economy has returned to health, evidence being a slight reversal of all that flight to safe haven into the US Treasury complex? The bond yields have risen, typical of what happens when the US Economy has recovered. In this case, if one reads the uptick in bond yields as a green light signal of economic vitality, then a totally wrong conclusion is reached. The USEconomy is slowing down noticeably, as seen below with retail sales. A repeat of the 2000-2001 slump is evident, but the current slump starts at a lower level.

The strange message is that US households can no longer burn home equity for purposes of consumption. Investment at the national level is insignificant at best, nonexistent at worst. Investment in financial engineering does not count!

Bond yields should rise for the basic reason of the climb in price inflation. The main debate now is how deep the recession will be. Only the obviously biased folks, like the diminutive president, the compromised Treasury Secy, the rookie USFed Chairman, the hack USGovt agency heads, and Wall Street felon executives debate whether a recession is in progress or not. Their combined track record of fraudulent behavior continues. Their false messages continue. Corporate welfare continues. Massive cost inflation without wage growth benefit continues. The destruction of the middle class continues. The insolvency of America continues. Further wreckage of US banks and households is a virtual certainty. The financial markets just cannot accept these facts yet. It will be a long hot summer, with Chinese Olympic Games as a climax.

Other key data indicates that the USEconomic recession is growing deeper. It is hard for me to write or speak the word ‘Recovery' without laughter. The only thing that has recovered is acceptance of falsehoods. Long recoveries (even if tainted) are followed by long painful recessions, especially with the credit abuse seen in recent years. This is the first leg in a powerful recession, the likes of which have not been seen in half a century. Even Sir Alan Greenspasm recognizes a recession when he sees one. “We are in a recession. But this is an awfully pale recession at the moment. The declines in employment have not been as big as you would expect to see.” Gee, Alan! Check the Birth-Death Model corruption to the Jobs Report. A loss of 280 thousand jobs in March and another 280 thousand jobs in April qualify as hefty employment declines. My prism removes all B-D Model adjustments, in pursuit of reality, removing the garbage clutter.

The obvious recession with horrible job loss screams of addition USFed rate cuts, much more accommodation with monetary accommodation (easy money), wave after wave of further home foreclosures, wave after wave of further bank losses, and new waves of bank failures, all of which will send gold and silver to the stratosphere.

The truth hurts, so revise the truth. George Orwell is chuckling in his grave. Joseph Goebbels roars with laughter in the fire & brimstone of hell.

Details on bank & bond developments are covered in the upcoming May Hat Trick Letter. It also covers the housing market, whose decline is nowhere near at an end. In fact, the lingering glut of oversupply across the board guarantees another 10% to 20% in price declines. How will bank bonds react? Easy, they will lose perhaps 50% of their value, even the AAA-rated. Huge swaths of debt downgrades are in progress still. That news is kept quiet.

If you want a guaranteed howl, check out the Treasury Investment Protection Security, the infamous TIPS, another fraud. It pays out 0% now, claiming to protect from inflation. What a joke! It should pay out at least 5%, and perhaps 7% or more, since prevailing price inflation is running at almost 12% and long-term bond yields pay out less than a 5% yield.

MORE STENCH IN RECENT NEWS

The recent news is so horrible that it defies logic how Wall Street can keep a straight face on its deception and ongoing marketing program songs. Start with the USGovt carnival, as the April Jobs Report was trotted out last week. It immediately was met with derision, doubt, and double takes. The claims come that the USEconomy and US financial system are resilient and have weathered the storm. The economy has faltered, tipping badly from the storm, into a recession obvious to all except those in power on Wall Street and the USGovt circus rings. This gang must be swept out in November, for colossal incompetent and widespread corruption, as stewards to an era of unprecedented loss of national wealth. The financial system has been rendered insolvent, with negative core reserve assets. How is that weathering the storm? Households are increasingly insolvent, hardly geared for economic participation. The only resilience detectable is from the USGovt and Wall Street carnival barkers, whose contributions are trumpeted wrong messages. They want your money even now, for yet another shift of wealth from the plebeians to the elite.

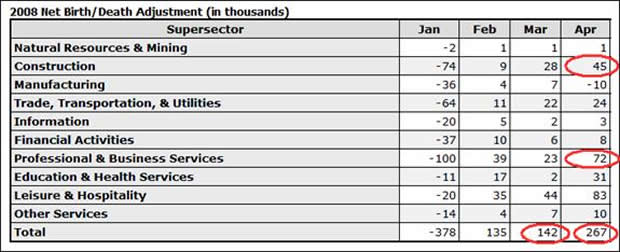

The April Jobs Data has once again brought attention to the Birth-Death Model, whose deception has come much more into the open, exposed to harsh light of scrutiny. The adjustment was openly discussed on financial networks, on the NYSE trading floor, and elsewhere. The fraudulent three-legged mangy dog is running in the open, in full view. Be sure that the scrutiny by many folks is lost almost immediately by the mainstream. Their attention span toward rays of light from reality is short. They quickly revert to headlines of news stories in the propaganda, recited by strained faces by guests in interviews. The April contribution to job creation from the Birth-Death Model was +267k jobs!!! Included are +45k construction jobs and +72k professional & business services jobs. The hacks at the Bureau of Labor Statistics either forgot to check the reality of job cuts from major corporations, or they are given marching orders by even bigger klutzes in management. Anger at the complete gang encompassing the Mussolini Fascist Business Model is not only warranted, it is demanded. Lee Iacocca, of former Chrysler CEO fame, recently delivered a speech wondering why outrage is not common and prevalent among the American populace, since the economic fabric of the nation has been destroyed by incompetence, corruption, and preoccupation with war. Here, Here, Lee!!! Never is any need felt on my part to justify my anger. If people asks me why, then they are most likely a contributor to the problem itself, or deaf dumb blind.

The reality of 280k job losses in March and another 280k job losses in April would have rattled the financial markets. The USFed and Wall Street desperately want to sell the idea of recovery. They want suckers to buy the billion$ in stock shares they wish to sell here. Reality reported with massive job loss, in an obvious loud indication of economic recession, would have spoiled their mission of grand deception.

If more official interest rate cuts were expected, that being the prevailing opinion, then the USDollar would not bounce like it has, the bank stocks would not bounce like they have, and a deeper USEconomic recession would be anticipated.

Gold would have risen from the anticipated policy response. As reality enters the room in the next few weeks and few months, all deceptions will be laid bare. Gold will catapult past 1000 easily when reality strikes hard.

Other horrendous news centers upon UBS and another $10.9 billion in credit related losses, will axe 5500 jobs mostly in the United States and United Kingdom . That is only fitting, since these two nations operate as centers of the most reckless economic models and home loan lending in modern history. In other mortgage finance news, Fannie Mae announced a giant $2.2 billion quarterly loss, and warns of severe weakness in the housing market. Don't forget that Fannie and its equally fat partner Freddie Mac are expected to serve as acidic foundations in any Resolution Trust platform for mortgages.

The housing market absolutely will not stabilize, and certainly not rise, unless and until a New Resolution Trust platform is in full gear operation.

Its functions will be to provide secondary mortgage funds as it securitizes mortgages, to bury badly damaged and completely dead mortgage bonds in their acidic basements, and to provide desperate assistance in renegotiated mortgage loans when passing the loan writedowns to federal agencies who pick up the heavy lunch tab. Expect the New RTC to begin operations no sooner than early 2009, thus permitting additional housing price declines. Mortgage bonds follow. Bank losses follow. The key is housing. It served as the phony cockeyed foundation to the USEconomy from 2002 to 2006. Now it is an albatross.

GOLDMAN SEEKS BUYERS OF ITS CRUDE OIL CONTRACTS

True to form, in yet another chapter in their corruption, Goldman Sachs has announced the likelihood of a future $200 crude oil price. Conclude quickly that they are eager to find buyers of their long crude oil positions, as its price heads down. GSax has standing profits in need of liquidation, but they need more dumb demand. In 2005 they shorted the mortgage bonds profitably, even as they sold mortgage securities laced with fraud. In November 2007, they heralded a flat year for gold, just before its price vaulted from 800 to over 1000. Now these criminal geniuses are touting a strong year for crude oil. Doesn't anyone ever question the clear biased motives of these guys? Simple conclusion is that crude oil is soon coming down. Watch gold rise as the pendulum swings from energy to precious metals.

JPMorgan might act as the chief corruption player behind the curtains, but without a doubt, Goldman Sachs acts as the chief corruption player on the open stage. JPMorgan was pulled onto the stage last month in its bold Bear Stearns raid. GSux continues to ply its trade. At least JPMorgan offered a straight interview in Germany , where CEO Jamie Dimon admitted the bank crisis in the Untied States is nowhere near at an end. He essentially denied that he would ever be really honest and forthright with his shareholders, especially if they were indeed broke. By the way, don't trust anyone who goes by the nickname Jamie. My name is James, and you can call me an expert on the name.

THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS.

From subscribers and readers:

“You are able to consume and regurgitate complicated information into layman's terms. It shows that you understand your subject well. It is very easy to take complicated material and repackage it as complicated material. You, however, have the ability to take the complicated and make it understandable to the common man.” (RickS in Californiaa)

“Keep up the good work, and stay safe- the world needs your interpretative skills. “From your radio interviews, I know that your quick wit and conviction are genuine. Your confidence and eloquence comes across just as strongly. You make specific, seemingly outrageous predictions with specific timing, and you are very often right. Really, can one offer any higher praise to an analyst?” (TomH in California )

“The unfortunate demise of Dr. Kurt Richebacher leaves Jim Willie, Bob Chapman, and Jim Sinclair as the finest financial minds on the scene today.” (DougR in Nevada )

“There are four writers that I MUST READ. You are absolutely one of those favorites!! William Buckler, Ty Andros, Richard Russell, and YOU!!” (BettyS in Missouri )

“Your newsletter caught my attention when the Richebächer report ended. Yours has more depth and is broader in coverage for the difficult topics of relevance today. You pick up where he left off, and take it one level deeper, a tribute.” (JoeS in New York )

By Jim Willie CB

Editor of the “HAT TRICK LETTER”

www.GoldenJackass.com

www.GoldenJackass.com/subscribe.html

Use the above link to subscribe to the paid research reports, which include coverage of several smallcap companies positioned to rise like a cantilever during the ongoing panicky attempt to sustain an unsustainable system burdened by numerous imbalances aggravated by global village forces. An historically unprecedented mess has been created by heretical central bankers and charlatan economic advisors, whose interference has irreversibly altered and damaged the world financial system. Analysis features Gold, Crude Oil, USDollar, Treasury bonds, and inter-market dynamics with the US Economy and US Federal Reserve monetary policy. A tad of relevant geopolitics is covered as well. Articles in this series are promotional, an unabashed gesture to induce readers to subscribe.

Jim Willie CB is a statistical analyst in marketing research and retaicl forecasting. He holds a PhD in Statistics. His career has stretched over 24 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com . For personal questions about subscriptions, contact him at JimWillieCB@aol.com

Jim Willie CB Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.