Foolish Investment Ideas

Stock-Markets / Financial Markets 2014 Apr 02, 2014 - 04:44 PM GMTBy: Axel_Merk

With April Fools' Day behind us, it's time to get serious about investing. Don't be fooled by this week's non-farm payroll report; nor by the assertion that the U.S. may have the cleanest of the dirty shirts. And certainly don't be fooled into thinking the market has your interests in mind...

With April Fools' Day behind us, it's time to get serious about investing. Don't be fooled by this week's non-farm payroll report; nor by the assertion that the U.S. may have the cleanest of the dirty shirts. And certainly don't be fooled into thinking the market has your interests in mind...

Foolish to believe the job market drives the stock market?

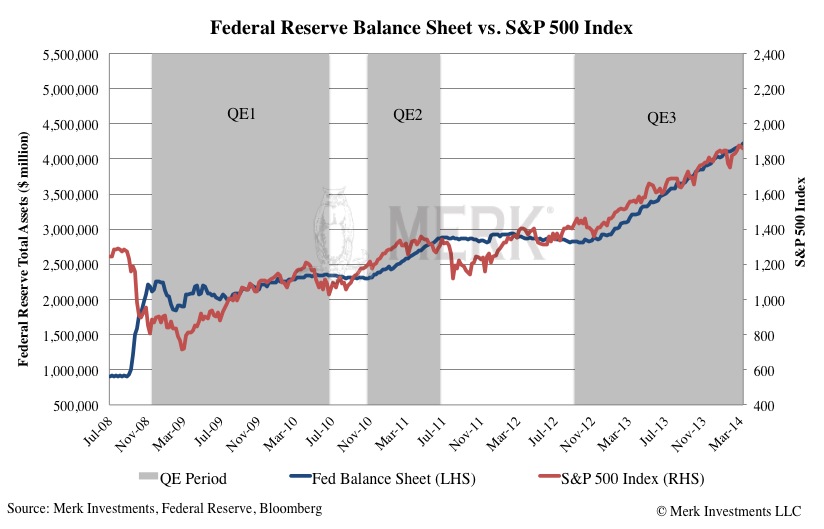

It may be foolish to put too much weight into this week's non-farm payroll report to decide whether to buy or sell. Since the onset of the financial crisis in 2008, the stock market has tracked the Federal Reserve's "printing press" rather closely. We allege that the rise in the stock market has a lot more to do with the Fed's asset purchases than a healing economy.

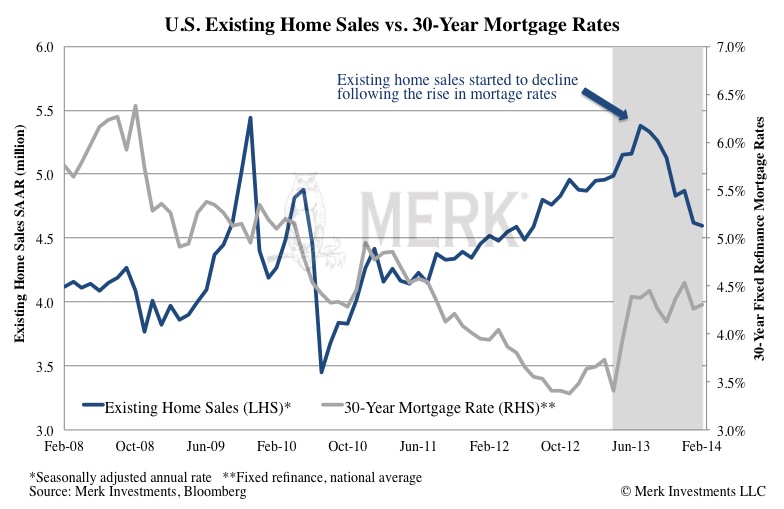

The Fed has had an interest in pushing up asset prices because "underwater" homeowners (homeowners that owe more on their home that it is worth) don't make for good consumers. By boosting home prices - and the stock market while they are at it - consumption, and economic, growth might be boosted as well. The problem with all this is that asset price inflation, especially in the stock market, can evaporate rather quickly. To prove this point, consider that the "taper talk" that started a year ago rocked not just the bond market, but also signaled to homebuyers that cheap mortgages may be a thing of the past. And although mortgage rates are still low by historic standards, housing market activity has been disappointing. The weather has been blamed, but if one slices the numbers into different geographic regions, our analysis clearly suggests that it is the anticipation of higher rates that is spoiling the party. Differently said, the Fed has been able to boost home prices, but if we truly had a rising interest rate environment, all the "progress" may quickly be undone. Below is a chart of seasonally adjusted annualized monthly existing home sales; other ways of looking at the housing market show the same loss of momentum starting a year ago:

Foolish to put your money with the "Cleanest of the Dirty Shirts"?

As much as we respect the wisdom emanating from Newport Beach, the quote that the U.S. may be the "cleanest of the dirty shirts" left the impression with many investors that the U.S. is the place to invest. By all means, we don't doubt there are investment opportunities in the U.S. But just as Apple, for example, may be a great company, it doesn't mean one necessarily makes money buying AAPL stock (this is not an investment recommendation). Investors learned the hard way that going with the perceived leader is not always a profitable investment strategy. All excited about the U.S. "clean shirt" many investors haven't realize that despite all the trouble in the Eurozone, the euro beat the greenback in 2012, then again in 2013, when the euro was the best performing major currency, and it is also up versus the dollar in the first quarter of 2014. There are plenty of challenges the Eurozone faces, but that doesn't mean investors have to stay away from the euro.

Similarly, there are lots of myths that have little to do with reality; among them that the dollar benefits from a rising interest rate environment, or that economic growth is needed for a strong currency. Please see our analysis Rising Dollar Myth for suggestions on how to avoid being fooled when it comes to assessing the value (or fragility?) of the dollar.

Foolish to believe the market is your friend?

There is a lot of talk about market manipulation, not just in the gold conspiracy camp, but also when it comes to alleged market manipulation by high frequency traders (HFTs). In any market there may be some players that break the rules; and they deserve to be prosecuted. However, let's not forget whom we are dealing with: the market. The market is not a friend you like on your favorite social media platform. No, the market is everyone else trying to make money off you.

If you take the gold market, there's a paper and a physical market. The "paper" market is one where derivatives rule, allowing investors to make leveraged bets. After 12 years of rising gold prices, it shouldn't have come as too much of a surprise that some investors geared up their gold exposure using leverage. A year ago, as volatility surged, partially driven by the Fed's taper talk, lots of de-leveraging took place, as volatility is the enemy of leverage. It's not surprising that this can lead to a disconnect between the paper and the physical market, as those interested in the physical metal are more likely to be non-levered players that have not received margin calls. What's different with commodities is that there is real demand for real things; conversely, financial products, even without leverage, are still "paper" products. As such, allegations of manipulation may be more likely to occur; however, the underlying drivers for potential dislocations of derivatives are not all that different. The concern many have is whether any de-leveraging can happen in an orderly fashion. For purposes of this analysis, though, we simply want to drive home the point that it shouldn't come as a surprise that markets behave in ways that can irritate the long-term investor. No regulation will ever change that; it may be better to embrace this in one's investment decisions.

Let me expand on another example on why it may be foolish to think the market is working on your behalf: when you place an order on an exchange for 100 shares, you might be able to get "best execution." But if you place a larger order, you better "work" that order. Why would someone give you your preferred price? To illustrate this, let's examine high frequency trading shops (HFTs): HFTs are in the market to make a buck for themselves; in the process, they provide liquidity for everyone. To look at an example, some of the good and bad can be seen in the foreign exchange markets: Historically, banks are the primary liquidity providers in foreign exchange. Foreign exchange trading is generally done "over the counter" (OTC), but there are platforms that provide various ways of trading. HFT shops try to beat banks at their own game. And HFTs might be good at taking advantage of idiosyncrasies of a particular trading platform. Banks realize they lose money on that platform because they get beaten by HFTs. They now have to choose whether to invest to also take advantage of the idiosyncrasies of that particular platform; or whether to stop providing liquidity there and focus on other platforms. Combined with a surge in regulatory overhead, there's an incentive in the industry to consolidate, i.e. concentrate on fewer platforms. As the big banks leave some platforms, other investors also desert the venue. So you tell me: are HFTs the bad guys because they scared away the banks? Or are the banks high frequency traders themselves, but with a better reputation (that's quite a statement in today's environment that someone has a worse reputation than banks) that were asleep as competition entered the market?

I'm not trying to justify banks for HFTs, but want to show that every investor is in the markets for their own profit. The role of regulators is to align incentives so that greed can play out without taking unfair advantage. Regulators cannot regulate away bad decision-making; however, regulators can help design a system where bad decisions of any one player (the failure of a player) does not wreck the system as a whole. But just because someone is screaming that someone else is eating his or her lunch does not yet mean there is abuse. Importantly, as regulators get involved, I'm not optimistic that investors or any other stakeholders (other than lawyers) will be better off.

For more on how to not be a fooled in the markets, please register to be notified when we hold a webinar; our next Webinar is Thursday, April 17, 2014. Also don't miss another Merk Insight by signing up for our newsletter.

Manager of the Merk Hard, Asian and Absolute Return Currency Funds, www.merkfunds.com

Rick Reece is a Financial Analyst at Merk Investments and a member of the portfolio management

Axel Merk, President & CIO of Merk Investments, LLC, is an expert on hard money, macro trends and international investing. He is considered an authority on currencies. Axel Merk wrote the book on Sustainable Wealth; order your copy today.

The Merk Absolute Return Currency Fund seeks to generate positive absolute returns by investing in currencies. The Fund is a pure-play on currencies, aiming to profit regardless of the direction of the U.S. dollar or traditional asset classes.

The Merk Asian Currency Fund seeks to profit from a rise in Asian currencies versus the U.S. dollar. The Fund typically invests in a basket of Asian currencies that may include, but are not limited to, the currencies of China, Hong Kong, Japan, India, Indonesia, Malaysia, the Philippines, Singapore, South Korea, Taiwan and Thailand.

The Merk Hard Currency Fund seeks to profit from a rise in hard currencies versus the U.S. dollar. Hard currencies are currencies backed by sound monetary policy; sound monetary policy focuses on price stability.

The Funds may be appropriate for you if you are pursuing a long-term goal with a currency component to your portfolio; are willing to tolerate the risks associated with investments in foreign currencies; or are looking for a way to potentially mitigate downside risk in or profit from a secular bear market. For more information on the Funds and to download a prospectus, please visit www.merkfunds.com.

Investors should consider the investment objectives, risks and charges and expenses of the Merk Funds carefully before investing. This and other information is in the prospectus, a copy of which may be obtained by visiting the Funds' website at www.merkfunds.com or calling 866-MERK FUND. Please read the prospectus carefully before you invest.

The Funds primarily invest in foreign currencies and as such, changes in currency exchange rates will affect the value of what the Funds own and the price of the Funds' shares. Investing in foreign instruments bears a greater risk than investing in domestic instruments for reasons such as volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, and relatively illiquid markets. The Funds are subject to interest rate risk which is the risk that debt securities in the Funds' portfolio will decline in value because of increases in market interest rates. The Funds may also invest in derivative securities which can be volatile and involve various types and degrees of risk. As a non-diversified fund, the Merk Hard Currency Fund will be subject to more investment risk and potential for volatility than a diversified fund because its portfolio may, at times, focus on a limited number of issuers. For a more complete discussion of these and other Fund risks please refer to the Funds' prospectuses.

This report was prepared by Merk Investments LLC, and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice. Foreside Fund Services, LLC, distributor.

Axel Merk Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.