Fed Interest Rate Cut Could Spark Bond Market Panic Selling

Interest-Rates / US Bonds Apr 20, 2008 - 05:03 PM GMTBy: Mick_Phoenix

Welcome to the Weekly Report. This week I have to highlight conditions in the bond markets as a priority, we maybe about to endure a bust of quite large proportions. I will also look at some longer term stock market indicators, confirmation that the Bank of England will follow the US and show why the current rally in stocks is due to a visit from an old friend, as readers at Livecharts.co.uk will know only too well.

Welcome to the Weekly Report. This week I have to highlight conditions in the bond markets as a priority, we maybe about to endure a bust of quite large proportions. I will also look at some longer term stock market indicators, confirmation that the Bank of England will follow the US and show why the current rally in stocks is due to a visit from an old friend, as readers at Livecharts.co.uk will know only too well.

Before we begin I need to comment on something I read this week. " Hedge funds played their part in the violent rise in spot prices early this year. To that extent they can be held responsible for the death of African and Asian children. Tougher margin rules on the commodity exchanges might have stopped the racket. Capitalism must police itself, or be policed."

Who wrote this, some socialist leaning European, a US Treasury/Fed spokesperson? Maybe it was the remnants of a socialist/communist government in the Caribbean? No, no one like that, it was none other than Ambrose Evans-Pritchard , International Business Editor at The Telegraph.

Here is how he describes his orientation to all things economic: "For the record, I am a Burkean conservative, aged 50, with a libertarian bent, and a penchant for Monetarist and Austrian economics - though Keynes had a point in the Slump."

Well at least he has all the bases covered, I suppose. Unfortunately all it shows is a confused methodology toward economic thinking. Some of his influences are in direct conflict (vitally about the Slump) and Ludwig von Mises is probably spinning in his grave.

What is more worrying is that AE-P is allowed to write such bilge as we see in his remarks about Hedge Funds. (I have no connection, in any way, to Hedge Funds.) Hedge Funds didn't cause the rise in soft commodities, they did not enable it. To say that they did (even partly) and are responsible for mass starvation shows a complete lack of understanding about the true nature of monetary inflation and Central Bank sterilisation methods and their destabilising effects on free markets. Yet thousands of readers will have taken that statement as a fact.

Without me saying this is the cause, a simple point about the rising costs of transportation of foodstuffs, shortages and pricing mechanisms blows his statement out of the water. He also seems to forget a very simple rule, for every buyer, there is a seller. Who sold to the buying hedge funds at prices that were acceptable? No mention of that I see.

Hedge Funds operate in a (supposedly) free market. They buy and sell as they feel fit, just like everyone else does. They make profits and when they make losses, they go bust, unlike certain banks or brokers who get centralist protection and bailouts. Capitalism polices Hedge Funds, they either survive or go under. If they do something illegal, fine, regulators should get the batons out and beat them to a pulp.

Instead what do we see in the mainstream media - shrill and hysterical statements pointing the blame at those funds operating correctly in a free market. Calls for more regulation and as I mentioned would happen not long ago, calls to restrict margin availability. If AE-P truly believes what he wrote, he needs to expand upon it. If he wrote it to garner readers he should change his "credentials".

Ambrose, if you read this and want to reply feel free.

I am seriously concerned that many are not ready for what is to come in the US bond markets, especially US Treasuries. As we have witnessed the Federal Reserve is happily swapping lower rated debt, stuff that no other lender wants as collateral, for US Treasuries to enable Bank and Broker credit to be continued.

Now, in a way this could be viewed as a neutral debt creation policy, a swapping of assets rather than new issuance. However that situation is about to change and bond markets are beginning to price in the effects: The Treasury's two-year note sale on April 23 may tally $30 billion, according to Jersey City, New Jersey-based Wrightson ICAP, which specializes in U.S. government finance. That would be the most ever sold for the maturity, according to the Treasury. The government may sell $20 billion of five-year notes the following day, which would be the most since 2003, according to Wrightson. The government announces the amounts April 21. (Bloomberg)

As discussed in the last 2 Occasional Letters this should come as no surprise, issuance of Government debt is required to lend credibility to increased inflation expectations. (You didn't think I did all that theoretical work for no reason did you?) It will not be the last surge of treasuries into the markets either.

Bond markets are faced with further supply, as we can see here: NEW YORK, April 18 (Reuters) - U.S. high-grade corporate bond issuance hit a record in April as companies took advantage of improving market sentiment and strong investor demand for new deals.

US investment-grade corporate bond volume totaled $50.7 billion through April 18, according to research firm Dealogic. The previous record for this month was in April 2001, when companies sold $47.35 billion of high-quality debt.

This week's issuance alone included a few marquee deals from a finance subsidiary of General Electric Co, JPMorgan Chase &, XTO Energy and Lehman Brothers. General Electric Capital Corp's $8.5 billion transaction was the fifth-largest U.S. corporate bond sale since 1995.

On top of all this is the new muscle beginning to be flexed by the GSE's, for example: WASHINGTON (AP) - Mortgage finance company Freddie Mac said Thursday it would buy up to $15 billion in home loans for higher-priced properties, using new flexibility granted by Congress earlier this year. Freddie Mac, the second-largest U.S. financier and guarantor of home mortgages, said it would buy the mortgages of up to nearly $730,000 from Wells Fargo & Co., JPMorgan Chase & Co., and Washington Mutual Inc.

Richard Syron, chief executive of the McLean, Va.-based-company said the move "shows how we can bring new liquidity to markets other investors have all but abandoned and make full use of the new tools Congress gave us to help restore stability during the current housing crisis."

I am not going to discuss all the ins and outs of the debt issuance and credit expansion again as it has been covered elsewhere. What we can see is the emergence of debt issuance has been reignited, thanks to the back stop provided by the Federal Reserve. Here is moral hazard writ large, as new debt is used not to shore up current positions but is creating further liabilities.

For the first time in many a year, it appears that the bond markets are reacting to this increased supply as confirmation that the US Govt and the Federal Reserve truly intend to inflate over the longer term and are decoupling from the Fed Fund Rate(2.25%) along with LIBOR.

Why do I think this is an inflation related move, rather than LIBOR reacting to tightness in credit conditions? Simple, supply of debt is increasing and the financial market is underwritten by the Fed. As Doug Noland puts it (and I agree): "When the Fed and Washington radically altered the rules of U.S. finance last month, they placed in jeopardy huge positions that had been put in place to hedge against and profit from systemic crisis. With the end of "Stage one" arises a major short squeeze in the Credit, equities, and derivatives markets. And when it comes to contemplating the scope and ramifications of today's "hedging" activities, we're clearly in Uncharted Waters. It is not beyond reason that a disorderly unwind of "bearish" Credit market positions could incite a mini bout of liquidity, speculation, and Credit excess that exacerbates Global Monetary Instability - while Setting the Backdrop for Stage Two of the Crisis."

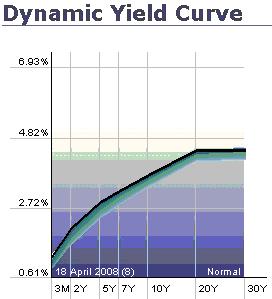

From my viewpoint I expect yields to go north and I may have something that shows this beginning:

Click on the image to view the live yield curve at Stockcharts.com. The black line is the latest curve, the green shadow is the recent past. Yield across the curve is rising, not just in the 2year-5year window. As Doug Noland said, if markets are set up for an anticipated scenario, in this case a recession and slowdown and have priced accordingly, then intervention will have a destabilising effect.

For bonds that means a sell off, and the possibility of the long end (30 year) yield climbing significantly. If the Fed cut at the next meeting, it could be enough to trigger a panic steepening trade, reinforced by stops being hit.

Here is the nasty bit.

To read the rest of the Weekly Report and view the new website, click here.

By Mick Phoenix

www.caletters.com

To contact Michael or discuss the letters topic E Mail mickp@livecharts.co.uk .

Copyright © 2008 by Mick Phoenix - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Mick Phoenix Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.