Why the World is Trapped with their U.S. Dollars

Currencies / US Dollar Jan 04, 2014 - 02:45 PM GMTBy: Sam_Chee_Kong

To a lot people a country with large foreign reserves is equivalent to a strong country. In a way it is true because a country can only accumulate foreign reserves when it is running a budget surplus. Having large foreign reserves has its advantages like enabling it to finance more imports and also acting as a cushion against an economic downturn. However there are also disadvantages associated with having a large foreign reserve. Besides generating inflation it also increases our dependence on the US$ which we are unable to get out from. A lot of people might thought I am nuts, saying that Malaysia and the rest of the world are trapped with their Dollar denominated foreign reserves. I shall show you why we can’t as a group but before that let us go through our country’s international reserves holdings.

To a lot people a country with large foreign reserves is equivalent to a strong country. In a way it is true because a country can only accumulate foreign reserves when it is running a budget surplus. Having large foreign reserves has its advantages like enabling it to finance more imports and also acting as a cushion against an economic downturn. However there are also disadvantages associated with having a large foreign reserve. Besides generating inflation it also increases our dependence on the US$ which we are unable to get out from. A lot of people might thought I am nuts, saying that Malaysia and the rest of the world are trapped with their Dollar denominated foreign reserves. I shall show you why we can’t as a group but before that let us go through our country’s international reserves holdings.

Below is the Breakdown of our International Reserves holdings as of September 2013.

From the above we can see that our Foreign Currency Reserves forms the majority of our International Reserves which currently stands at USD 123.7 Billion. On the surface it is indeed a commendable effort by our government thanks to the past policies that promote exports. But as I have already mentioned above there are also side effects in having a large foreign reserve. Some of the side-effects are being a source of inflation, too dependent on the U.S Dollar and the depreciating U.S Dollar.

Foreign Reserve and Inflation

Our country is able to increase its foreign reserves because we are continuously running a balance of payment surplus since 2008 as shown by the graph below.

The increase in the foreign reserves is a result of our Bank Negara buying up the excess supply of foreign currency from our trade surplus. But how does it cause inflation? To illustrate I shall use the following example.

When we run current account or trade surplus (exports > imports) our exporters will end up with more foreign currencies as foreigners are obliged to make foreign currency (USD) payments to us. This is a credit transaction to Malaysia because we increase our claim on foreign currency. What are our exporters going to do with their increased claimed on foreign currencies? They will sell it to the banks which will eventually end up in Bank Negara. To pay for this Bank Negara will print or create new Ringgit ‘out of thin air’ and then swap with the foreign currency. Eventually, this will increase the supply of money (new Ringgit) in the economy and hence will lead to a rise in prices of goods and services. This is a classic textbook inflation where too much money chasing too few goods.

Trapped with USD

The second side-effect of having a large foreign reserve denominated in the USD is foreigners as a group cannot get out of their USD holdings. Before I address this problem, let me explain the incentive for the Americans to run large current account deficits.

Firstly, prices of goods in the U.S will always be cheap. You may be asking how cheap goods relate to huge current account (imports > exports) deficits? To explain I shall use the following equation, also known as the Fisher Equation where,

Aggregate Demand (MV) = Aggregate Supply (PT)

M = Money Supply

V = Velocity of Money

P = Prices

T = Transaction or the amount of goods available

The equation can be re-written as,

P = MV/T

where the price P is dependent on either M,V or T.

Ignoring V, the Federal Reserve Bank of America or FED, can bring down the prices of goods and services by either increasing the M (Money Supply) or T (amount of goods available). It will be the interest of the FED to print as much as possible because there will always be demand for the USD. This is because the USD is not only the world reserve currency but also the currency of trade because most basic commodities like oil, wheat, soya beans, gold, tin, copper and etc, are quoted in USD. So when they increased their Money Supply (USD 85 Billion a month now), they can afford to buy more goods and services which is the T. Hence by increasing the denominator T, the price of goods and services or P will drop in this case. As long as the T is increasing faster than the M then P will always be low.

Secondly, being the world reserve currency also meant that it will be the currency of choice as foreign reserves for the world’s Central Banks. The following is the table of the currency composition in Central Banks in percentages. As you can see, the USD remains the currency of choice for most Central Banks since 1999 as their foreign reserves.

Source : IMF Annual Currency Composition Report (COFER)

In 2011 the USD constitutes 62.3% of all currencies as foreign reserves, up from 53.4% in 1995. So this practically explains why there is always a demand for the USD no matter how much they print or how large a deficit they will incur to their current accounts.

The chart below shows the current account of the U.S since 1970. Out of the 43 years, 35 of them are in deficits.

You may be wondering how the hell can they run deficits for so long? The main reason is the recycling of the Dollar back into the Dollar denominated assets like deposits, securities, real estates or other dollar denominated assets. Let me illustrate this with the following example.

When our electronics manufacturer exports a container of electronic goods to the U.S, he will be paid in USD. Our manufacturer will receive his payment in USD which he will then sell it his bank or Bank Negara for Ringgit. In the end everybody is happy because the importer got his goods, our exporter is paid in Ringgit and Bank Negara got the USD. The problem is that the more the Americans import the more dollar we will accumulate or the bigger our current account surplus is with them. So what is Bank Negara going to do with its growing foreign reserves?

Can we diversify and get out of our foreign reserve Dollar denominated Assets? The answer is as a group, it is almost impossible for foreign Central Banks to get out of dollars. Let’s look at some examples.

Say if Bank Negara sell some of its Dollars to the Japanese for Yen. In this case the Bank of Tokyo will end up owning our Dollars while we have their Yen. Again if the Japanese sell some of their U.S Treasury Bonds to the British, then the Japanese will have either Dollar or Yen in return. However, the Bank of England will now end up with the Dollar denominated U.S Treasury Bond.

Let’s look at another scenario where the seller asked to be paid in different currencies. Say, if the British thinks they are smart and sell their Treasury Bonds to an American Bank say Bank of America and request to be paid in Ringgit. Bank of America like a grocery store will have an inventory of foreign currencies and so will pay the British in Ringgit. Again, like a grocery store, Bank of America will have to replenish its Ringgit holdings. To do it, Bank of America will have to buy it from one of our Malaysian Banks and hence the Dollar gets recycle or end up in Malaysia. What happened here is that it is basically an inventory adjustment of the Dollar from one Central Bank to another. Bank Negara might end up with more dollars while the Bank of England ends up with less dollar denominated assets. Or in layman’s term money shuffling from the left pocket to the right pocket. At the end of the day the total demand and supply of dollars will be the same.

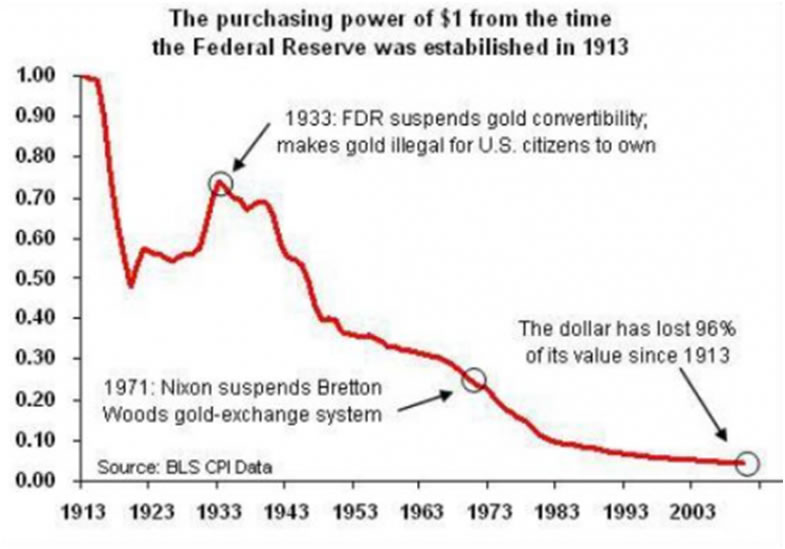

Thirdly, it concerns the depreciating of the U.S Dollar. Below is the chart of the Purchasing Power of the U.S. Dollar since 1913.

As can be seen a US$100 bill in 1913 is now only worth about US$ 4. This loss of purchasing power is mainly due to the increasing cost of living brought about by inflation. Inflation is also known as the ‘silent killer’ because it zapped your purchasing power slowly and most of the time it stealthily. This poses a big threat to all of us and not only to the retirees and our next generation in the future. Due to the erosion of the purchasing power of the dollar, it will affect the value of our Dollar denominated foreign reserves in the future. What are we going to do to protect ourselves?

You don’t need to be a rocket scientist to know that we should diversify our foreign reserves into other currencies or assets. But how? Even mighty China has a problem in getting rid of its huge Dollar denominated Foreign Reserves. Below I present to you a case study on China and its efforts to diversify from the Dollar.

China as a Case Study

China as we know commands the largest foreign exchange reserves in the world. The following chart shows the trend of China’s accumulation of its foreign exchange reserves. As can be seen the accumulation picked up speed since the middle of 2012. As of September 2013, China’s foreign exchange reserves held by the People’s Bank of China has increased to US$ 3.66 trillion.

China has been very vocal on its De-Americanization drive recently. China is very disappointed with America’s attitude on not doing enough to control its current account deficits, increasing debt mountain and the depreciating U.S Dollar. If you understand what I wrote earlier, you should know that the Chinese cannot do much to the Americans other than complaining passively. Who is willing be the buyer when China disposes its USD 3.6 trillion foreign exchange reserves? As we have seen if the Chinese were to liquidate their Foreign Exchange Reserves it will not benefit them because due to the avalanche of Dollars it will reduce its purchasing power further.

Exposure to U.S Securities

The following table shows China’s long term holdings of U.S Securities. From 2006 to 2010, the average amount of foreign reserves devoted to U.S Securities is 60%.

From the table above, it is evident that China tried to reduce its dependence on US Securities from the period 2007 to 2009. In 2006 the share of Chinese Reserves devoted to U.S securities is 84%. It started to drop from 2007 until 2009 when China tried to reduce its investment in U.S Securities. However in 2010, it again rose to 78% and this clearly shows that China has failed in its attempt to diversify its dollars.

Outward Foreign Direct Investment

China has also tried to diversify its huge foreign reserves by investing into real assets such as Oil & Gas, Mineral Extraction, Commodities and Forestry but somehow not very successful. These investments are mostly done by China’s estimated more than 100,000 SOEs or State Owned Enterprises.

State-Owned Enterprises or SOEs has always been giving headaches to the People’s Republic of China. Once these SOEs are the pride of China but now appear to be economic dinosaurs. They are now considered ‘a pain in the ass’, due to their inefficiency, high debt and loss making investments. Their mere existence is to provide jobs to more than China’s 200 million urban workforce. The Chinese Government realised that to move forward they cannot forever subsidize and bailout these loss-making SOEs.

There are efforts to scale down the number of SOEs to less than 10,000 by introducing free market practices and Western Management style as part of the corporate culture. Unprofitable enterprises are either closed down or forced to merge with profitable ones. As part of the reform, SOEs are permitted to raise capital by listing its shares in the Shanghai, Shenzhen and the Hong Kong Stock Exchange. Further liberalisation includes diversifying their ownership to local and foreigners. The chart below shows China’s transition from SOEs which is still considered slow. Despite much effort has been done, it only managed to transform about 11% of the SOEs.

China has been filling the vacuum left by the Americans and Europeans in Africa and South America. The table below shows China’s Outward Foreign Direct Investment from 2005 to 2011. As can be seen it gained momentum from 2005 and peaked in 2010. However during 2011 its outward FDI has somehow halved at a time its foreign reserves has been increasing rapidly.

The InfoChart below shows China’s outward FDI reach around the world. The two areas where China has been concentrating its investment recently is Africa and South America. China has been investing heavily in the Oil & Gas sector in these two countries as part of its drive to rely less on Middle Eastern Oil. Mineral extraction Investment in Australia and technical partnership with Eastern Europe is also on the rise. But if you were to add up all those FDIs it only amount to USD 378 billion or 10% of its total foreign exchange reserves.

Why China’s Outward FDI so low?

One of the main reasons why China has been hesitating to invest larger sums of its foreign exchange reserves overseas is mainly due to the risk of failed investments. Investing in foreign markets subjected not only to the normal risks associated with investments. There are other risks that needed to take into account such as geo-political, foreign exchange exposure, safety and logistics. China’s rate of success in its outward FDI has been a mixture of failure and success. In politically unstable regions like Africa, there are many failed projects due to internal rivalry and fighting among the different factions of the people. Below are the costs of failed projects in five countries that totalled USD 91 billion.

Wrapping Up

As can be seen from above even China has problem trying to diversify its Dollar denominated assets. Despite its rhetorical threat to dump its foreign reserves so as to punish the U.S, it has yet to do so. Because the Chinese knows that by dumping or selling the dollar for Yuan the buyers are most likely be the Chinese Banks. In other words, their action to dump the dollar will boomerang because it not only reduced the purchasing power of the dollar but also ended up in their own banks. How about all foreigners start dumping the dollar at the same time?

We must understand that even if all foreigners start dumping or raining their USD reserves at each other they still cannot get out of the Dollar. Why is this so? When they start selling dollars to each other it will increase the supply of dollar which will drive the value of the dollar down sharply. Again at the end of the day the foreigners will end up with dollars but at different amount that they began with. But they are worse off because the purchasing power of the dollar has declined.

Another effect of such a move will be a rise in the interest rate in the U.S. When there is a rise in the interest rate it will encourage a net capital inflow and the dollar will make its way back to the U.S. right? Another thing is that when the dollar is down and out where else can the foreigners spend their dollars other than in the United States? This is because the United States is the only country where the dollar will have its ultimate purchasing power. So is there any way that foreigners can get out of the dollar?

There are a couple of methods and one of them is when the U.S is running a trade surplus. It will be a time where the U.S exports more than it imports. When the U.S is running a surplus it’s claim on the USD will increase while foreigners will reduce their claims on the USD. Hence the dollar will make its way back to the U.S because foreigners will be paying their imports with dollar. I reckon we will not see the U.S running trade surplus in the next few decades given the size of its current account deficits and its debts. As for the other method, I will leave it to our policy makers to figure it out.

The sad truth is that we have all been suckered by the Americans to accept their toilet paper USD. They can now continue with their spending habits and they will not succumb to their mountain of debts as long all the Central Banks continue to use the Dollar as their Foreign Currency Reserve. This is because the larger their deficits the larger will be our surpluses and hence the more difficult to get rid of the dollar.

by Sam Chee Kong

cheekongsam@yahoo.com

© 2013 Copyright Sam Chee Kong - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2013 Copyright Sam Chee Kong - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.