New Trend Guarantees Higher Gold Prices 2014

Commodities / Gold and Silver 2014 Jan 02, 2014 - 08:58 PM GMTBy: Jeff_Clark

If you're like me, you've bought gold due to the money printing policies of most developed countries and the effect those policies will have on the future purchasing power of our paper money. Probably also because there's no viable way for governments to escape the consequences of all the debt they've piled up. And maybe because politicians can't be trusted to formulate a realistic strategy to avoid any number of monetary, fiscal, or economic crises going forward.

If you're like me, you've bought gold due to the money printing policies of most developed countries and the effect those policies will have on the future purchasing power of our paper money. Probably also because there's no viable way for governments to escape the consequences of all the debt they've piled up. And maybe because politicians can't be trusted to formulate a realistic strategy to avoid any number of monetary, fiscal, or economic crises going forward.

These are valid, core reasons to hold gold in a portfolio at this point in time. But a new trend is under way, and someday soon it will be just as much a driving force for gold prices as anything else: a good old-fashioned supply crunch.

A few metals analysts have mentioned it, but it escapes many and certainly is off the radar of the mainstream financial media. But unless several critical factors reverse course, a supply shortage is on the way with clear implications for the price of gold.

The following four factors are combining to diminish gold supply. While we've touched on some of them before, put together they're creating a perfect storm that will, sooner or later, impact the gold market in several powerful ways. As these forces gather steam, you'll want to make sure you've already built a substantial position in physical bullion.

Factor #1: Production Pullbacks, Development Delays, Exploration Cancelations

Gold producers don't operate in a vacuum. If the price of their product falls by 30% over a two-year period, they've got to make some adjustments. And those adjustments, more often than not, result in lower production, delayed mine development plans, and cuts in exploration budgets. The response is industrywide, and even low-cost producers are not immune.

The drop in metals prices means some mines can't operate profitably, and if the losses exceed the cost of closure (and possibly, restart in the future), these mines will be shut down. As operations come offline, global output falls.

While lower metals prices are not what any of us want, they're long-term bullish because, as they say, the cure for low prices is low prices. If prices drop further, a greater number of projects will be unable to maintain production levels. For example, we know of several operating mines that, in spite of large reserves, will be forced offline if the gold price falls to the $1,100 level.

The impact on development and exploration projects is even greater—it's easy to postpone construction on tomorrow's new mine when you're worried about cash flow today. As a result, many companies have cut drilling projects and laid off geologists.

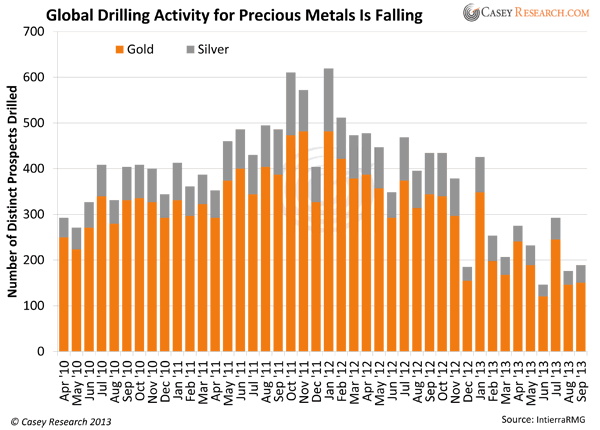

The chart below shows the precipitous decline in the number of drilling projects around the world.

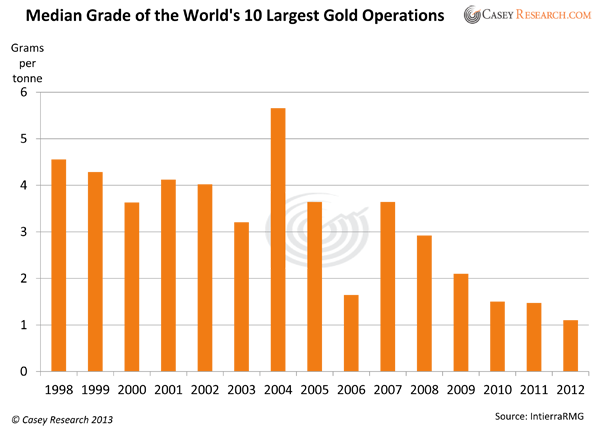

Through the first nine months of 2013, 52% fewer drills have been turning compared to the same period last year. And it's not just fewer holes being poked in the ground—ore grades are declining too.

As of last year, ore grades of the ten largest gold operations are less than a third of what they were just five years ago, and less than a quarter of what they were 14 years ago.

Here's the troubling aspect: This trend cannot be easily reversed.

It takes about a decade to bring new projects on line, and even shuttered, recently producing mines held on "care and maintenance" take time and money to get going again.

In other words, even when gold prices start rising again, new mine supply will take years to rebuild. Many companies will find themselves with a lack of readily available ore, and the market with fewer ounces.

Lower metals prices obviously have an impact on how much metal gets dug up. This alone is bad enough for supply, but unfortunately it's not the only factor…

Factor #2: Now You See 'Em, Now You Don't

Many mining projects have both low-grade and high-grade zones. When prices fall, a company can mine the richer ore and still make money. It may sound shortsighted, but it can be the right thing to do to stay profitable and be able to survive in a temporarily weak price environment.

But high-grading, as it's called, can make low-grade ore part of a disappearing act. Here's how:

When metals prices are low and companies focus on high-grade ore, the low-grade material is temporarily bypassed. It's still physically there, so one might assume the company will come back at a later time to mine it. But not only is it not economic at lower metals prices, it may never get mined at all.

That's because some low-grade ore only "works" when it's mixed with high-grade ore. Even when gold moves back up, it doesn't matter, because the high-grade ore is gone. So it's not just gone legally, as per regulatory definitions of mining reserves—it may be economically gone for good.

Miners could return to some of these zones in a very high gold price environment (something well north of $2,000), but that's a concern for another day. The point for now is that many of today's low-grade zones would be written off if the high-grade they need to work is gone.

Critical point: You may read reports early next year that global production is rising. However, to the degree that's due to high-grading, it virtually guarantees lower production is around the corner.

Factor #3: Greed Is Good—Says the Politician

It's become increasingly difficult for mining companies to navigate the political minefield. Many governments have become so rapacious that supply is already suffering.

We've mentioned this issue before, but take a look at how governments and NGOs (nongovernment organizations) put an effective halt to some of the biggest precious metals discoveries seen this cycle…

Pebble Project in Alaska. Anglo American (AAUKY) spent $540 million on one of the biggest copper/gold discoveries ever, but recently announced that it will walk away from it. The company said it wants to focus on lower-risk projects and is undoubtedly tired of putting up with ongoing environmental scares and regulatory delays.

Fruta del Norte in Ecuador. Kinross Gold (KGC) bought Aurelian shortly after what many called the discovery of the decade, but the politicos demanded such a big slice of the pie that Kinross stopped developing the project.

New Prosperity Mine in British Columbia. Taseko Mines (TGB) has been relentlessly challenged by environmental activists at the world's tenth-largest undeveloped gold/copper deposit and pushed politicians to continually delay permitting.

Pascua-Lama in Argentina & Chile. This giant deposit has been postponed for several years, largely due to environmental issues and unmet regulatory requirements. Some analysts think it may never enter production.

Navidad in Argentina. Pan American Silver (PAAS) was forced to admit that the Navidad silver deposit—one of the world's biggest silver-primary deposits—was "uneconomic at any reasonable estimate of long-term silver prices" when the local governor announced he wanted "greater state ownership" and increased royalties from 3% to 8%.

Minas Conga in Peru. Newmont's (NEM) multibillion-dollar project was put on the back burner last year when the government gave the company two years to develop a way to guarantee water supplies for residents of the Cajamarca region.

Certainly bigger projects attract greater attention and scrutiny, but as it stands now, none of the above projects are in operation.

This list is by no means exhaustive; large numbers of smaller projects all around the world face similar challenges.

The bottom line is that finding economic gold deposits in pro-mining jurisdictions is getting increasingly difficult. The result? The metal stays in the ground.

Factor #4: Implosion Explosion

As you've likely read, the gold mining industry in South Africa is imploding.

- Labor strife: Strikes are common, and layoffs have numbered in the thousands this year.

- Rising costs: Labor and power costs have doubled since 2009. Some projects have been taken off line due to the one-two punch of higher costs and lower metals prices.

- Maturing assets: Many mines in South Africa are past their heyday and have forced companies to dig deeper. The deepest mine is now 2.4 miles below surface and takes workers a full hour to reach the bottom.

- Power inefficiencies: Electricity shortages are at their worst in five years. Poor power supply has led to blackouts and mining stoppages, and has made expansion difficult.

- Political interference: The industry has faced frequent calls for nationalization. Miners were told earlier this year they can stay private, though in exchange they were forced to pay higher taxes. How gracious of the politicians.

The breakdown in South Africa is important because as recently as 2006, it was the world's top producing country; it's now #5. Unfortunately, there's every reason to expect this trend to continue, in many countries around the world.

The result is—you guessed it—fewer ounces come to market.

These four factors are already affecting gold supply. Gold production in the US was already 8% lower in the first half of 2013 vs. the first half of 2012. Through June of each year, output dropped from 655,875 ounces last year to 623,724 in 2013.

These four factors are already affecting gold supply. Gold production in the US was already 8% lower in the first half of 2013 vs. the first half of 2012. Through June of each year, output dropped from 655,875 ounces last year to 623,724 in 2013.

The net result of this perfect storm is that we should expect gold supply to decline until prices are much higher. Even when prices do rise, management teams will be reluctant to expand operations, reopen mines, or buy new projects until they feel the new price level is sustainable. As a result, this trend will almost certainly last several years.

Based on the research we've done, it is my opinion that after a bump in output early in 2014, the shortfall will become increasingly evident by the end of the year and reach fractious levels by 2015.

If demand remains at current levels, or even if it falls by less than the decrease in supply, gold and silver prices will be forced up. And in an environment of currency depreciation, we should see more demand, not less. We have the makings of a classic supply squeeze.

Higher metals prices are not the only ramification, however: Investors will be required to pay higher premiums on bullion. Further, we can expect a lack of available product, most likely resulting in delivery delays or even rationing.

That's why it's so important to buy bullion now, before the storm. Even if you need to sell a little to maintain your standard of living, the effects on you will be all positive. The product you sell will…

- Fetch much higher prices

- Return the premium you paid—perhaps more than you paid

- Have a steady stream of ready customers

All it takes to capitalize on this opportunity is to recognize the supply shortage that's on the way and act accordingly.

Critical point: Buy the physical gold and silver you think you'll need for the future NOW.

One of the best places I know has among the lowest premiums available in the industry, and also offers several international storage locations in case things get bad in your home country. This breakthrough program is as liquid as GLD and offers greater safety than storing bullion at home. Click here to find out more.

© 2013 Copyright Casey Research - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Casey Research Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.