What Does QE Tapering Really Mean? What Will the Stock Market Do?

Stock-Markets / Stock Markets 2014 Dec 22, 2013 - 10:18 AM GMTBy: John_Mauldin

Now that we have begun tapering, we will soon see lots of analysis about whether QE has been effective. What will the stock market do? The US economy seems to be moving in the right direction, but the Fed has forecast Nirvana (seriously) – do we dare hope they can finally get a forecast right? Or have they jinxed us? This and a few other dark thoughts crossed my path on a beautiful day in San Diego; so in a very different Thoughts from the Frontline, I offer a number of small gifts rather than an overarching theme, and we will see if we can keep it short.

Now that we have begun tapering, we will soon see lots of analysis about whether QE has been effective. What will the stock market do? The US economy seems to be moving in the right direction, but the Fed has forecast Nirvana (seriously) – do we dare hope they can finally get a forecast right? Or have they jinxed us? This and a few other dark thoughts crossed my path on a beautiful day in San Diego; so in a very different Thoughts from the Frontline, I offer a number of small gifts rather than an overarching theme, and we will see if we can keep it short.

Let's start with a wicked-brilliant essay by Dr. Woody Brock. It is way too long and penetrating to cover fully in this letter, but we can glean some bits of wisdom.

The world has been focused on central banks and the ending of QE. But Woody muses about a second dimension to this issue. If the true winner under a zero-interest-rate policy (ZIRP) has been the shadow banking system (as many, including your humble analyst, have observed) what distortions are baked into the market? What will happen as ZIRP finally goes away?

Woody asks questions not unlike those Jonathan Tepper and I ask in Code Red:

But what about the second dimension to the unwinding of ultra-easy monetary policy, namely, higher Fed funds rates and an upward shift in the entire yield curve – for reasons having nothing to do with QE? This is seldom discussed. From the research we have carried out, it is this second dimension of the end of easy monetary policy that is the more important of the two. The nation has never experienced six years of hyper-low interest rates. What impact has this had on the restructuring of the balance sheets of insurers and banks? In striving to match assets and liabilities across 24 consecutive quarters of near-zero rates, what tricks might financial institutions have played (reaching-for-yield via derivative positions) that could backfire and occasion a financial crisis once the yield curve rises from the dead? In particular, what about the increased utilization of new "collateral and maturity transformation" schemes that could occasi on future panics?

And yet, the latest Fed papers are all about "forward guidance." They suggest that, rather than QE, it is forward guidance promising a low-rate regime that is far more effective in producing the Fed's desired ends. So if I read those papers and speeches correctly, we could be in a ZIRP-type policy for another three years. Where rates are starkly negative and investors are forced to seek yield in new and creative ways if they do not want to see their buying power eroded. But where we have little or no experience, and there might be a serious mismatch in duration.

Leverage Giveth and Leverage Taketh Away

Rewind to 2008-2009. What follows comes under the heading of full disclosure about painful lessons and a warning to those currently reaching for yield in new places. Without going into details, some (ok, a lot) of us had money invested in hedge funds that were part of the shadow banking system. There were all sort of creative funds invented to take private credit sources and circumvent normal banking functions. Life was good for a time, as "small" investors were able to get the returns normally reserved for banks. Except in cases of extreme leverage, we are not talking about lights-out numbers, just nice and steady high single-digit or low double-digit returns.

You could analyze the risks of the underlying investments and decide whether you were comfortable with the focus of the manager or fund. But as it turns out, the main risk you were taking had less to do with the actual investments but more to do with your fellow investors and their fetish for liquidity in times of stress.

Many of the funds in the shadow banking system had relatively short-duration money, which was invested in longer-term loans and financial structures. When everyone tried to redeem at once, the exits got crowded. Chaos ensued. It was not unlike – or maybe in some cases it was exactly like – an old-fashioned bank run.

Funds were forced to sell assets that were technically "good" but for which there were no buyers, except for investors who were picking up distressed debt. It was common to get assets at 50 cents on the dollar or less if you had ready cash. But those sales locked in significant losses for the sellers, and there was often modest leverage involved, which compounded the losses. Leverage giveth and leverage taketh away.

Other than the distressed-debt funds, which had a field day, there were only a few funds where the investors ended up OK. But those were funds where the investors' money was locked up so they were forced to sit through the crisis. Yes, if you looked at the mark-to-market returns over the short term, it was ugly (VERY ugly in some cases) on paper; but during the next few years, as price normalcy returned, valuations climbed back to normal and interest rates pushed returns over time to what should have been expected.

Two lessons here:

One is that you need to make sure the credit funds (and actually, any funds) you are invested in have the ability to match the duration risk of the source of their funds AND of their (your fellow!) investors, with their underlying investments. As an easy example, if you are invested in a fund that makes three-year loans and offers daily or monthly liquidity, if that fund has sudden demands for withdrawal, it will be forced to sell assets in the open market and take immediate losses to return that money. That is clearly not good!

But if there is a three-year hold or lock-up for withdrawals, the fund can manage withdrawal requests in a normal fashion as the underlying investments mature. Investors who want to stay in the fund do not suffer from the need for liquidity of their fellow investors.

In today's environment, the reach for yield is once again pushing investors into creative practices. Some funds are built to withstand a crisis, and others will get crushed. You must do your homework up front, and that includes thinking about what would happen to the underlying assets if another crisis comes along.

And the second lesson? You have to think about your own need for liquidity. If I came to you and told you that I loved your work, I might go on and on about the quality of your product, your work ethic, your productivity, etc., and then say I wanted to offer you a job. You might at least be interested and want to hear the offer. But if I then offered you minimum wage, you would just laugh and walk away, wondering what planet I was on.

But so many investors are willing to invest their money for minimum wage and maximum risk because of a personal fetish for liquidity. The last two bear markets have made us (appropriately) concerned about the safety of our money and left us keenly aware that we need to be able to run for the hills when the time comes to do so. But the pain of two bear markets has also caused us to seek protective mechanisms that might not be helpful in terms of our longer-term objectives. Liquidity is one of those protective mechanisms.

Liquidity costs money. Providers of liquidity have to provide either lower-return vehicles in the form of credit-type funds or increased risk in by way of equity-focused funds.

This is a theme I am going to visit a lot in 2014. You need to divide your investable assets into "liquidity or time buckets." Very few of us actually need access to all our funds at a moment's notice. We can take some of our funds and tie them up for longer periods of time; and if we think through what we invest in, we can get more than minimum wage for our investments.

In essence, for a portion of our money, we should be sellers of time or of liquidity risk. When you begin to think of your investment process as selling the time value of your money and seeking areas where people will pay you the most for your time, as we do in our work-related activities, I submit you might have more long-term success.

We are going to explore this idea at length in the next year and look at actual ways we can do this. I have been working for six months with a new associate, Worth Wray, developing a new focus on actual portfolio design; and shortly after the first of the year we will begin to publish. We are still dotting the final i's and crossing the last t's of the regulatory issues surrounding the process, but I am excited about what we will be able to do for you. What we hope to provide is a practical approach to investing in Code Red world.

What Does Tapering Really Mean?

But back to QE and ZIRP. After the Fed announcement last week, I was asked in one interview, "What will tapering really mean?" My honest answer is, I don't know, and I don't think the Fed does either, not in their heart of hearts. And if they think they really know – scout's honor – then they are delusional.

We can guess. Draw analogies. Play thought games. Try to "war game" the process. I have had some intense debates with people who are way smarter than I am, trying to come to some certainty. But at the end of the day, this has been an experiment without precedent. Has QE distorted foreign reserves in emerging markets, and will its withdrawal be an issue there? Is the stock market dependent on new reserves? We simply don't know. We are getting ready to find out. Does the Fed's buying of massive amounts of mortgages really make a difference? We don't REALLY know, although you can find people who will argue either side of any of those and another dozen questions. And make a lot of sense in doing so.

We are running the economy on an untested set of academic theories. Maybe they are right, although I do not think so. I am wary of actions that grossly distort market behavior, because a small group of people (central bankers) want 330 million (or maybe even billions) of people to change their self-interested actions, and offer us incentives to do so.

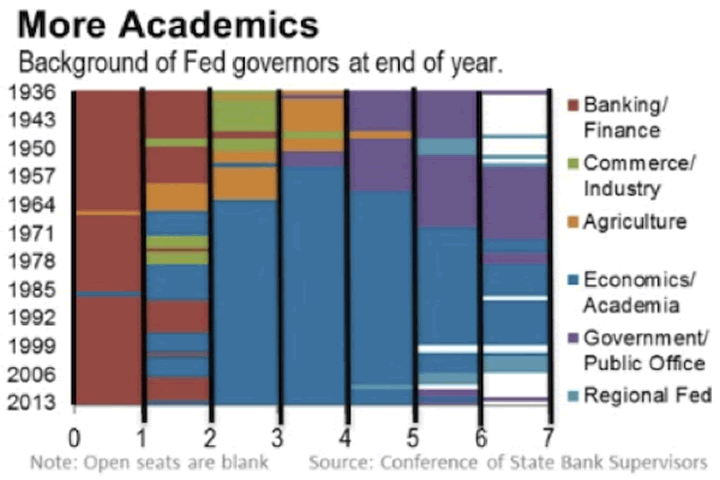

There has been almost total academic and bureaucratic capture of the Federal Reserve. When the Fed was established, bankers ran it (an approach that has its own set of issues), but now the process is driven by academics who mostly adhere to a group-think view of how economics works.

Look at the following chart from an article in this week's Wall Street Journal entitled "Fed Governors Increasingly Have Academic Backgrounds."

Quoting from the article:

The report flags the fact that the only current governor with direct regulatory experience is Sarah Bloom Raskin, who previously supervised banks as Maryland Commissioner of Financial Regulation. And she's likely on her way out after having been nominated to a position at the Treasury. Fed governor Jerome Powell has held a wide portfolio of jobs: lawyer, investor, private business and a stint at the Treasury under George H.W. Bush dealing with financial institutions. Fed governor Daniel Tarullo, after a series of government jobs, came to the Fed from Georgetown University Law Center, where he taught on banking issues.

The report categorizes governors going back to the founding of the Federal Reserve a century ago, and finds that the domination of the board by academics goes back some way. It's only until one rolls the clock back to the 1960s do those with governmental banking oversight profiles make a strong showing.

While the report doesn't analyze the current leaders of the regional Fed banks – they lead the institutions where most of the actual bank oversight takes place, even as it's controlled from Washington – those officials are also by and large academic economists. Only Boston's Eric Rosengren and Kansas City's Esther George have extensive direct experience in bank supervision. Meanwhile, Dallas Fed boss Richard Fisher has an extensive and successful background as an investor, while Atlanta Fed chief Dennis Lockhart was a long-time banker who also spent time in academia.

And what are they telling us about the future they have planned? It is going to turn out extremely well, they say. As a group they are forecasting economic Nirvana by at the end of 2016: a 3% GDP growth rate, 2% inflation, and a 5.5% unemployment rate. What would you expect the Fed funds rate to be in such a world? Might you assume that you would at least get some inflation premia?

Think again. They are forecasting a median Fed funds rate for 2016 of 1.75%, which is a 0.25% negative risk-free return!

I have highlighted in the past how truly abysmal the models are that the Fed uses to forecast economic conditions. It is almost statistically impossible, as numerous researchers have documented, to do as badly as Federal Reserve economic forecasts have done, although the Office of Management and Budget and other congressional forecasters give them a run for their money. The latter have the partial excuse of being economists employed by politicians. The Fed has no such excuse. Their models are just plain bad.

I truly hope these people are right. I really do. But eight years without a recession in an environment where interest rates have been aggressively repressed for all that time? What distortions are we creating? What shocks await as we adjust? Will this test of a theory end without tears? We have no choice but to wait and find out. And invest our portfolios for the uncertainty into which we are headed.

Which brings us back full circle to Woody. After highlighting the distortions in the shadow banking and financial systems of the world, he notes other research, such as that of Bill White, which I have written about at some length. White was at the BIS and posted a paper at the Dallas Federal Reserve that is an important critique of Fed policy. We should pay attention, because he is one of the academics who actually forecast the credit crisis of 2007-10 prior to its happening.

Let's jump to Woody's conclusion (emphasis mine):

The purpose of this PROFILE has been to examine some of the unintended consequences of the ultra-easy monetary policy we have experienced both here in the US and overseas since 2008. We have seen at least a dozen ways in which today's long period of very easy money and very low yields has distorted the workings of the financial system. This will cause unintended consequences in the near future as QE is ended, and as the funds rate is driven back up from near zero.

Many of these will be adverse consequences. The best note on which to end this paper is to restate what we have stressed repeatedly during recent years — as have many central bankers worldwide: Much too much has been asked of monetary policy in dealing with a very serious macroeconomic breakdown. Via the Tinbergen "controllability theorem" that we often cite, it is not that monetary policy does not help; it clearly does. Rather it is that no matter how "easy" monetary policy has been, it will never suffice to generate a normal recovery on its own. We emphasize that this is a theorem, not merely an opinion. Proper fiscal and regulatory policies are needed to complement the central bank's efforts.

Had all three of these policy knobs on the dashboard been jointly optimized, as is required in the Tinbergen-Arrow-Kurz theory, there would have been no need for monetary policy to have been ULTRA†easy. The Funds rate could have bottomed at 2%, and much less QE would have been required. As a result, many of the future "risks" we have detailed would not exist.

This last point has been perhaps the most central theme of our 2013 PROFILE essays: What matters is optimal macroeconomic policy and controllability. Accordingly, the market's obsession with the only game in town (monetary policy) is badly misplaced. What scholars such as William White and Jeremy Stein have done is to warn us that, aside from not serving to generate meaningful recoveries, ultra-easy monetary policy has created myriad new risks of the kind we have described. Historians will one day assess ex post whether this unprecedented monetary policy gamble was successful on a "net" basis.

What Will the Stock Market Do?

Finally, a brief note that I got from Ron Surz, setting out what stock market returns might be in 2014. I offer his words and chart and then a comment:

Now that this great 2013 is coming to an end, everyone is wondering what will follow in 2014. There is a formula that can help us couch our outlook. It goes like this:

Return = Dividend + (1 + Earnings Growth) X (1 + P/E expansion/contraction) – 1

The following table uses this formula to peek into 2014. The cell highlighted in yellow – earnings growth of 6% and an ending P/E of 15 – is the average long-term situation. In other words, if 2014 is "average," we'll see a 16% loss. But what if it's not average? The purple cells highlight a band around the average and indicate a performance range between a 13% gain and an 18% loss.

Earnings Growth |

||||||||

End P/E |

-4 |

-2 |

0 |

2 |

4 |

6 |

8 |

10 |

10 |

-49 |

-47 |

-46 |

-45 |

-44 |

-43 |

-42 |

-41 |

15 |

-24 |

-22 |

-21 |

-19 |

-18 |

-16 |

-14 |

-13 |

20 |

1 |

3 |

5 |

7 |

9 |

11 |

13 |

15 |

25 |

32 |

35 |

37 |

40 |

43 |

45 |

48 |

51 |

30 |

58 |

61 |

65 |

68 |

71 |

74 |

57 |

80 |

35 |

84 |

88 |

92 |

95 |

99 |

103 |

106 |

110 |

Source: PPCA Inc

I find this chart useful, in that to believe the stock market will rise next year you have to believe that we will see SIGNIFICANTLY above-forecast growth in earnings, which is hard to conclude from recent corporate financial releases, or that P/E ratios will rise. While I doubt the former, it is quite possible that we'll see a rise in earnings multiples if investors keep their optimistic, momentum-driven psychology in place. That sort of thing has happened a lot. What will actually happen? I have no idea that is better than your own, and mine could be worse (and probably is) because when I analyze the situation I probably way overthink it.

Corona del Mar, Dubai, Saudi Arabia, and Canada

I am in San Diego as I finish this letter and will drive up the coast in a bit to Corona del Mar to attend my friend Rob Arnott's annual Christmas party and watch the Newport Beach Parade of Lights, a nighttime parade of fabulously lit-up boats and yachts through the harbor. I was there a few years ago and was amazed at how spectacular it was. Tomorrow I will be home for the holidays until January 8, when I leave for Dubai and then Riyadh for a week. Then I am back home for a week before flying to Vancouver, Edmonton, and Regina for a three-day speaking tour at the respective cities' annual CFA forecast dinners. A note from a reader in Edmonton pointed out that it is already -30 there. I think I may try to find my thermal underwear.

I should note that Mauldin Economics Publisher Ed D'Agostino recently interviewed Grant Williams, editor of the wildly popular Things That Make You Go Hmmm... and Bull's Eye Investor, about global macroeconomic policy and how it relates to the Bull's Eye Investorportfolio. In this "warts and all" interview, Ed and Grant discuss what worked in 2013, what didn't work and why it didn't work, and how Bull's Eye Investorwill target opportunity in the coming year. As always, Grant's analysis, as you will see, is spot on. He has the unique ability to distill complex "big picture" perspectives into actionable investment ideas. Click here to see the video interview between Ed and Grant now.

I spent time with Jon Sundt and the newly announced Chief Investment Officer of Altegris Investments, Jack Rivkin. Jack and I first met years ago in Phoenix at a symposium conducted by the Thunderbird School. He is one of the intellectual thought leaders in the investment world and has been enormously successful in his career, heading up Neuberger Berman before his first retirement to a life of cutting-edge venture capital and private equity. I love hearing his stories of high-tech start-ups. We share a lot of the same interests and a fascination with the future.

The owners of Altegris enticed him out of retirement to come and take the reins of their investment process, and that makes me enormously happy. Jack is an investment force of nature and will help shape a direction that will give us ways to manage assets that make sense in a Code Red world. I spent an evening over a steak with him last night, and I really look forward to sharing his ideas and energy with you in the coming years.

In theory, when we get back to Dallas, the apartment will be 98% finished. I might even be given the iPad minis that control the electronics and allowed to play! There should be no more major construction crews, just people putting in door hardware when it shows up, some art here and there, etc. Reviews from friends are going well, but the credit all goes to my niece, who is responsible for the design and architecture. She is used to designing Ritz-Carltons and suites in Abu Dhabi, Macau, and Vegas and has recently gone out on her own. The timing was lucky for me, although she managed to destroy what I thought was my budget. But it has been totally worth it. The only limiting factors have been my personal tastes, which she has worked diligently to expand, and my budget. But she keeps pointing out that she has done a lot with little and helped me get good value. As a value investor, how could I argue?

It is time to hit the send button. I am at the Hyatt La Jolla, where we held the first seven of ten Strategic Investment Conferences. The place is home to so many good memories, and they were kind enough to give me the big suite for the night, which, perhaps because of those memories, is one of my favorite hotel rooms in the world. The gym next door is world-class, and I will spend a few hours working off that steak before driving on up to Rob’s soiree. And perhaps we'll engage in a little more investment talk, as he tends to attract some very talented friends in the industry. I guess that just happens when you manage $100 billion or so, as he does from his shop at Research Affiliates. (Rob is no stranger to longtime readers. You know him as the intellectual driver behind the extremely successful All-Asset Fund at PIMCO and through his patented Fundamental Indexes.)

Have a great week. I see Christmas dinner with all the kids and grandkids and friends, although it will be a smaller event than Thanksgiving was. I will shut down on Christmas Eve afternoon to go into chef mode for a few days, and then try and relax at home for a few weeks.

Your more optimistic than ever analyst,

Like Outside the Box?

Sign up today and get each new issue delivered free to your inbox.

It's your opportunity to get the news John Mauldin thinks matters most to your finances.

© 2013 Mauldin Economics. All Rights Reserved.

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.MauldinEconomics.com.

Please write to subscribers@mauldineconomics.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.MauldinEconomics.com.

To subscribe to John Mauldin's e-letter, please click here: http://www.mauldineconomics.com/subscribe

To change your email address, please click here: http://www.mauldineconomics.com/change-address

Outside the Box and MauldinEconomics.com is not an offering for any investment. It represents only the opinions of John Mauldin and those that he interviews. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with, Mauldin's other firms. John Mauldin is the Chairman of Mauldin Economics, LLC. He also is the President of Millennium Wave Advisors, LLC (MWA) which is an investment advisory firm registered with multiple states, President and registered representative of Millennium Wave Securities, LLC, (MWS) member FINRA, SIPC, through which securities may be offered . MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB) and NFA Member. Millennium Wave Investments is a dba of MWA LLC and MWS LLC. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Past performance is not indicative of future performance. Please make sure to review important disclosures at the end of each article. Mauldin companies may have a marketing relationship with products and services mentioned in this letter for a fee.

Note: Joining The Mauldin Circle is not an offering for any investment. It represents only the opinions of John Mauldin and Millennium Wave Investments. It is intended solely for investors who have registered with Millennium Wave Investments and its partners at http://www.MauldinCircle.com (formerly AccreditedInvestor.ws) or directly related websites. The Mauldin Circle may send out material that is provided on a confidential basis, and subscribers to the Mauldin Circle are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments. John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private and non-private investment offerings with other independent firms such as Altegris Investments; Capital Management Group; Absolute Return Partners, LLP; Fynn Capital; Nicola Wealth Management; and Plexus Asset Management. Investment offerings recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER. Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account managers have total trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor’s interest in alternative investments, and none is expected to develop.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.