Euro-zone Bashing Germany For Successful Economy, Game of Thrones – European Style

Politics / Euro-Zone Nov 24, 2013 - 07:10 PM GMTBy: John_Mauldin

In 2009-10 it seemed like this letter was all Europe all the time. There was a never-ending crisis from one corner of the Continent to the other. That time seems to have slowly faded from our collective consciousness, but the Eurozone crisis is not over, and it will not end quickly or soon. Even if it seems to unfold in slow motion – like the slow build-up in a Game of Thrones storyline to violent internecine clashes followed by more slow plot developments but never any real resolution, the Eurozone debacle has never really gone away. The structural imbalances have still not been fixed; politicians and central bankers have still not agreed to solve major fiscal problems; the overall economy still disintegrates; unemployment is staggeringly high in some countries and still rising; and the people are growing restless.

In 2009-10 it seemed like this letter was all Europe all the time. There was a never-ending crisis from one corner of the Continent to the other. That time seems to have slowly faded from our collective consciousness, but the Eurozone crisis is not over, and it will not end quickly or soon. Even if it seems to unfold in slow motion – like the slow build-up in a Game of Thrones storyline to violent internecine clashes followed by more slow plot developments but never any real resolution, the Eurozone debacle has never really gone away. The structural imbalances have still not been fixed; politicians and central bankers have still not agreed to solve major fiscal problems; the overall economy still disintegrates; unemployment is staggeringly high in some countries and still rising; and the people are growing restless.

Just as in the Game of Thrones, the Eurozone drama seems to drag on interminably. It seems to take forever to get to the next installment. I think GRR Martin (the wickedly brilliant creator of the series) should be confined to his Santa Fe villa until he finishes his epic – one of the few lapses in my personal belief that we should be allowed the freedom to control our own time. I read the first of the books in 1996 and the fifth when it came out in 2011, and he will need to finish at least two more. You can do the math, but it is clearly taking longer and longer between books – just as Europe seems to be taking longer and longer between successive peaks of its crisis. Perhaps we should confine the leaders of Europe to a far-northern Scandinavian hotel with hard beds and minimal amenities until they resolve their problems.

In the latest installment of the Eurozone crisis, deflation is back and winter is coming. This week we'll look at what is shaping up to be a very interesting year in Europe. I am going to visit a number of themes and offer links to readers who want to delve more deeply, as to develop each one would take several months' worth of letters. Next year it probably shall.

One of the continuing themes in the Game of Thrones is that a winter of epic proportions looms in the immediate future, and the world is not prepared for it. "Winter is coming" is whispered by worried wise men who urge various leaders to prepare, yet they put off the necessary in the face of the urgent. Signs that a European winter, too, is coming have lately been cropping up.

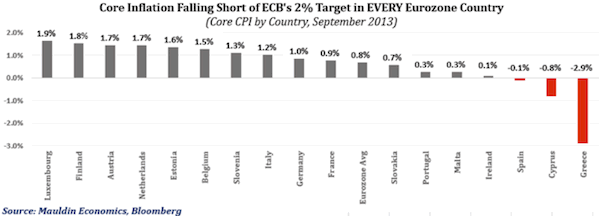

Key measures of inflation are decelerating across the Eurozone, and the region is as close as it has ever been to a deflationary bust. It's troubling enough that Eurozone headline CPI collapsed from 1.1% in August to 0.7% in September and that core CPI fell from 1.0% to 0.8% over the same period; but measures of Eurozone money supply (M1, M2, & M3) are also decelerating rapidly, suggesting that the deflationary trend will most likely continue without decisive action from the ECB, which has been strangely absent from the current rush by central bankers to print mountains of money. And the ECB could actually make a case for such action!

Even worse, this new round of borderline deflationary data is coming not just from a small number of lost causes like Greece or Cyprus. Ten out of the seventeen Eurozone countries experienced rapidly decelerating inflation rates over the past few months, including Italy and France. Spain officially fell into deflation for the first time since February 2010. In many ways, the situation is even worse than the CPI numbers suggest. Note that Italy, France, and Germany all hover barely above 1% inflation. And their numbers are falling.

There are two major problems associated with an extended period of ultra-low inflation or deflation in the Eurozone. First, peripheral countries will have a much harder time servicing and retiring their debts without the extra boost to nominal GDP that positive inflation provides. Even if you are working on lowering the absolute amount of your debt, it is impossible to improve your debt-to-GDP ratio when GDP is falling and your debts are growing. Moreover, outright deflation works to crush debtors (and debtor nations) by increasing the real weight of the debt and triggering the destructive debt-deflation cycle described in Irving Fisher's Debt Deflation Theory of Great Depressions (1933).

The second major problem is that currency appreciation always accompanies deflation – all else being constant – so that affected economies also become less competitive in terms of exports at the very moment that a positive trade balance is most important.

These are problems that I have written about for years. The effects of a common currency and monetary policy are spread around very unevenly in Europe, creating a boom in certain countries (chiefly Germany) and a sad bust in others. This disparity is the very predictable result of a currency union sans fiscal union. And trying to fix the Eurozone fiscal structure after the fact is akin to fixing the engine of an airplane while flying at 30,000 feet.

The rapidly weakening inflation we are seeing in Europe is a very big deal, because deflation can become a chronic, crushing condition, making it even harder to deal with excessive debt, undercapitalized banks, and runaway fiscal deficits in major countries like Spain, Italy, and France. Over time the masses begin to expect falling rather than rising prices, and these expectations can be very difficult to reverse without credible, decisive, and powerful action from the central bank.

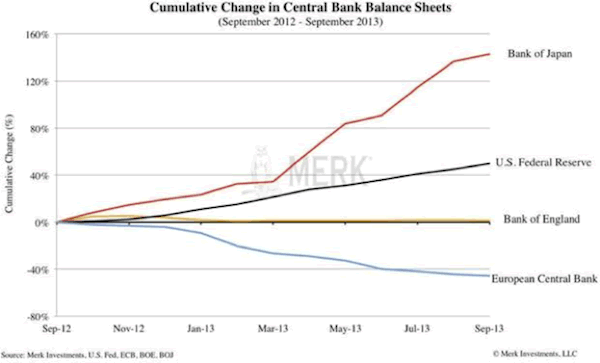

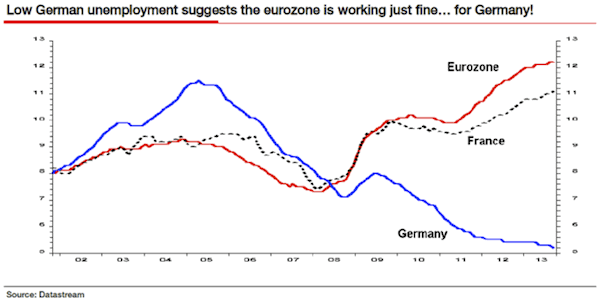

Up to this point, the ECB has been almost completely unwilling to squarely confront the issues at hand. The ECB balance sheet has been inexplicably shrinking for the past year (more on that in a moment). That is why ultra-low inflation readings should not come as a surprise. Not only has the ECB not been easing, it has actually tightened its balance sheet considerably over the past year. To many observers, this trend clearly demonstrates German dominance within the ECB.

"This is just like Japan," says Lars Christensen of Danske Bank. "The central bank thought money was easy when in fact it was much too tight. But effects could be much worse in Europe because unemployment is so much higher." In addition to a central bank seriously behind the curve, structural problems are holding back economies across the periphery, including Spain, Italy, and, yes, even France.

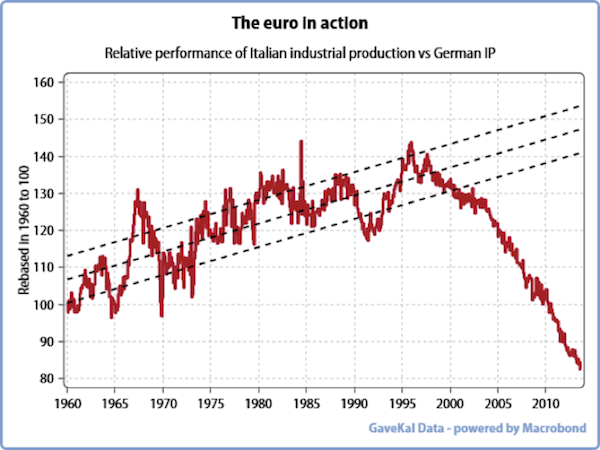

"Like Japan, necessary structural reforms prior to the crisis were delayed and now these will have to be implemented in an environment that is both economically and politically more fragile," said Takeo Hoshi & Anil Kashyap in a recent report for the IMF. Germany looks like an exception precisely because it undertook structural reforms well before the crisis, which is part of the reason that Germany is doing so well and much of the rest of Europe is not.

You can see the disastrous difference between German industrial production and Italian industrial production in this chart from my friends at GaveKal. This chart would look much the same whether it was France, Italy, Greece, Ireland, or any of the peripheral countries contrasted with Germany. Structural reform of labor policies requires massive social disruption in the best of times. I think we can all agree that for southern Europe this is not the best of times.

True, the risk of government funding crises has receded since Mario Draghi's July 2012 commitment to "do whatever it takes" to preserve the Euro; but debtor countries like Greece, Cypress, Spain, Ireland, Portugal, Italy, and France have been forced to bear most of the economic cost. Like Japan, the Eurozone has failed to adequately recapitalize its banking system, and troubled economies have failed to address structural problems through reforms.

Ambrose Evans-Pritchard recently noted, "While the risk of a Eurozone bond crisis has greatly receded since the ECB agreed to act as a lender of last resort in July 2012, this has been replaced by slow economic attrition."

Outright Monetary Transactions (or OMTs) by the ECB are limited by the size of its balance sheet, and the German Constitutional Court may further limit the ECB's capabilities when it rules on OMT in early 2014. No one really seems to be talking about this fact, but the ECB is losing firepower each and every month as its balance sheet contracts. This trend is going to require Germany to change its stance in the face of the next crisis, but the question is, what will Germany demand in return? Germany always seems to have a price for action. While the market was willing to give Draghi the benefit of the doubt in the last crisis without his really having to fire a shot, it is entirely possible that it will question the limits of his ability to find the funds necessary to solve multiple crises at once. And if France is one of those countries that needs aid? Mon Dieu, c'est une catastrophe!

How Much Is That Euro in the Window?

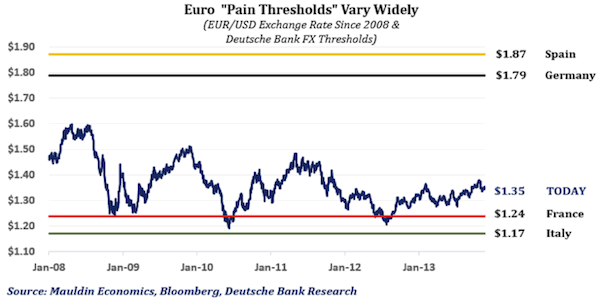

ECB restraint has kept the euro entirely too strong, at least for certain countries in the EZ, again showing the dysfunctionality of the common monetary union.

A 2013 study from Deutsche Bank says the "pain threshold" for the EUR/USD exchange rate (the level at which further appreciation impairs competitiveness and economic recovery) is $1.79 for Germany, $1.24 for France, and $1.17 for Italy.

Shown against the current EUR/USD exchange rate, the "pain thresholds" make it obvious that Germany is sitting pretty while France and Italy are getting crushed by the strong euro. Although Spain shows a higher threshold than Germany, gains in Spanish competitiveness are really attributable to mass unemployment and a major fall in unit labor costs. Spain has already taken a tremendous amount of pain, while France and Italy are just starting to absorb theirs.

Arnaud Montebourg, French industry minister, claims that each 10% rise in the EUR exchange rate costs France 150,000 jobs, and the trade-weighted EUR index has risen by 9% in the past 15 months. The strong euro is inflicting damage on the textile industry and other low-margin sectors across Southern Europe. As Ambrose Evans-Pritchard notes, "Any policy set at this stage for Club Med needs is destructive for Germany, and any policy set for German needs is destructive for Club Med. You cannot set a workable policy. The intra-EMU gap is already too wide."

Bashing Germany and Other Fun European Activities

Let's look at a few other comments on Germany in the last few weeks:

The pattern we have seen over the last decade has been the structural rise in German industrial output and a parallel decline in the industrial activity achieved by the rest of the Eurozone's man economies…. Too many houses in Spain, too many civil servants in France, too many factories in Germany…. This system is inexorably causing the destruction of the industrial bases in Italy, France, Spain, and the others. – Charles Gave, 9/12/2013

The European landscape has changed so that Germany is benefiting at the periphery's expense and the uncompetitive periphery is losing major export share to Asia. The European Union has broken down as a functioning system.

France, Italy, and Spain should together pound their fists on the table, but they are not doing so because they delude themselves that they can go it alone…. Today there is only one country and only one in command: Germany. – Romano Prodi, the Italian prime minister who prepared Italy for EMU membership in the 1990s and presided over the euro's launch as European Commission chief

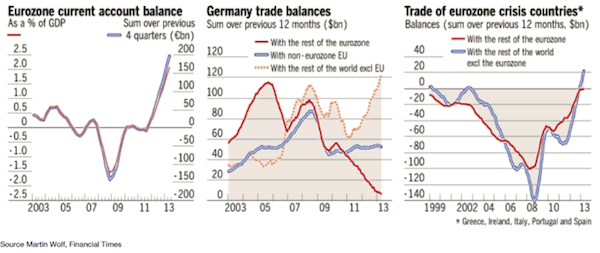

Germany is living in an Alice-in-Wonderland world of intellectual confusion, thinking that it can run a current account surplus of 7% of GDP (almost 3x China's surplus in % of GDP), with an inflation rate of almost zero, without at the same time blocking recovery." – Ambrose Evans-Pritchard

Martin Wolf writes in the Financial Times that the OECD is insisting that Europe's North-South gap in labor competitiveness cannot be closed by putting all the burden of adjustment on already depressed economies in the south.

While over in London, at Societe Generale, Albert Edwards offers the following chart:

And let's look at three more quotes from Ambrose (from separate columns over the past few weeks) that clearly illustrate the zeitgeist in Europe:

Conflicting narratives of the crisis are emerging, pitting creditor and deficit states against one another.

The central tenant of EMU doctrine is that countries will not reform unless they face a crisis, and their feet are held to the fire. There is a near religious belief in Berlin – evangelized by Brussels, and the EMU gang of five – that any let-up in austerity, any recourse to stimulus, let alone a new deal, is a gift to shirkers who want to dodge reform.

The policy regime has become maniacally restrictive because every decision is filtered through 'game theory' calculations, belief in Berlin that the naughty Latins will somehow cheat unless their feet are held to the fire…. Every week it seems that yet another towering figure of the European cause joins the rebels.

Yet the ECB surprised us all and cut its interest rates a few weeks ago. Does this signal potential rebellion within the ECB? A recognition that perhaps the crisis is coming to a new head? Mario Draghi denies that the Eurozone is slipping into a Japan-style deflation trap, but he admits the trend toward deflation is alarming (which is probably the most we can expect from a central banker trying to speak confidence into the markets). He claims the governing council is "wholly in agreement about the need to act," but does his statement reflect a better appreciation of the situation by German inflation hawks or a revolt by debtor countries (France, Spain, Italy, Portugal, Greece, Ireland, et al.)? The question is, who is in control now? Does this "agreement" signal a major policy shift or a limited compromise by credit countries?

The ECB had to do something. The rise of the euro was becoming deflationary and threatening to choke off growth…. It is very rare for a central bank to change its policy so dramatically from one month to the next, so something profound must have happened. – David Bloom, HSBC

Yet all this German bashing prompts a very spirited defense of prudence from my favorite irascible French curmudgeon, Charles Gave:

When Keynesian policies are failing, as they always do, proponents never fail to look for a scapegoat. Usually this is Germany, rebuked for the un-Keynesian practice of earning and saving. Our concern is that when German bashing reaches fever pitch, panic selling often follows….

So when I see the U.S. Treasury once again going after the Germans, and that sentiment immediately seconded by the International Monetary Fund, the European Commission and prominent financial commentators, then I start to worry. If these guys have gotten to the desperate stage of rebuking Germany for being prudent and productive, then perhaps it is time to panic.

The euro may be fairly valued versus the US dollar, but it is not "fair value" for Germany and Italy to have the same exchange rate. German industry is slowly but surely destroying the Italian economy (in the French and the Spanish industries). This is what has always happened in history when two countries with different productivity rates are joined by a fixed exchange rate. The trading goods sectors of the one country with the highest productivity destroy the trading goods sector of the one with the lowest productivity. It cannot be otherwise.

So the cashed-up Germans will keep doing what they do best: investing in their export industry, while the Italians are forced to stop investing. And since increases in salaries in Germany have been lower than increases in the country's productivity, then we have both a cost of capital and a unit labor cost that is more favorable than in Italy. One would have to be brain-dead to invest in the trade goods sectors in Italy.

As long as the euro is around, European economies will keep diverging from each other. It cannot be otherwise. There is not going to be a returned equilibrium. The solution proposed by the US Treasury or various columnists in the FT is for Germany to do like everybody else: start wasting capital and moving to lower productivity. An interesting idea, which the British government under Mr. Brown explored at length, but the end result was not that pretty. And for some strange reason, this idea is not very popular in Germany.

My convictions thus are that: this is not a stable system; the Germans will not change their policies; the French or the Italians will not reform; the European economies will keep diverging; and anti-euro political groups will continue to rise in the EMU. If even one country elects an anti-euro party to the majority, then all bets are off.

Stories are beginning to percolate all over Europe but especially in France about the crisis that will be brewing next year. President Hollande's approval rating has fallen to 15% (not a typo). This is a precipitous comedown for someone swept into power just last year by a small majority of French voters. Unemployment has risen to over 11%. A few months ago, the National Front party won handily in regional elections in liberal strongholds. Led by the fiery Marine Le Pen, it is very nationalist and anti-euro and favors protectionism and a different sort of socialism, but radical economic socialism nonetheless. This is not your father's conservative party.

Le Figaro (a leading French newspaper) recently reported that loss of confidence in the French government is becoming dangerous, based on a confidential report of surveys conducted by prefects (high government officials) in each department (prefecture). "All across the country, the prefects described the same picture of a society that is angry, exasperated and on edge. A mix of latent discontent and resignation is being expressed through sudden eruptions of fury, almost spontaneously."

Can Europe Handle One More Shock?

Europe is but one shock away from a true crisis. I think it will probably happen when it becomes clear to the bond vigilantes that France is not willing to deal with its deficit issue in any meaningful way. Yes, I know we're talking about France, but just a few years ago we thought Spain and Italy were invincible, too. There is a pattern here that even fixed-income investors may be able to recognize.

Will something else trigger a crisis even sooner? There is a good chance for foreign exchange crises across emerging markets if/when Janet Yellen's Federal Reserve starts to taper. We are already seeing signs of currency depreciation in Brazil and India. The reversal of balance of payments pressures following the Fed's "no taper" surprise is only a temporary reprieve. Pressures will be greater than ever when a shift in Fed policy disrupts capital flows to emerging markets. To think that such a development would not affect Europe is naïve. Borderline deflation leaves the Eurozone without buffers in the event of an imported deflation shock. And Japan is not helping. A significant thrust of our new book, Code Red, is that the latter half of this decade will be characterized by a currency war the likes of which we have not seen for 40 years. This will just compound the difficulty of the situation in Europe.

My friend Charles Gave, among many others, is convinced that the Eurozone cannot hold together. Forty percent of me agrees with him, yet the other sixty percent acknowledges the sincere desire among European leaders and many European citizens to maintain the union at all cost. And what a cost it will be. There must first be a serious banking union, and within the next year. If they can't create a banking union, how can they expect to create a fiscal union, which is far more contentious and will require every one of the Eurozone nations to give up a great deal of fiscal sovereignty?

A decisive moment is coming for Europe. If winter is coming, can a French spring be far behind? Will we once again hear the cries of "Aux barricades, mes amis!"? Stay tuned.

Navigating the Unknown: What Investors Need to Know for 2014

If you are an accredited investor or a licensed investment advisor, please join me for an exclusive Mauldin Circle webinar on Tuesday, December 3, at 1:00 p.m. EST/10:00 a.m. PST. This highly anticipated webinar, "Navigating the Unknown: What Investors Need to Know for 2014," will provide timely perspective for investors making 2014 portfolio decisions. I've invited my Code Red coauthor, Jonathan Tepper; economics giant Lacy Hunt; and alternatives expert Jon Sundt, CEO & President of Altegris Investments, to join me. This panel represents a terrific mix of economic and investment viewpoints with a practical bent towards investor solutions. My goal is for listeners to walk away with much greater clarity about the Code Red World and an actionable perspective on global markets and the upside potential of diversifying into alternative investments in 2014. Understanding and managing uncertainty shouldn't be any more complicated than necessary!

If you are a Mauldin Circle member, a webinar invitation will be sent directly to you by email. A replay will also be available to qualified registrants. If you are unable to listen to the live discussion, be sure to register so that you can receive the replay information. If you are not a member of the Mauldin Circle and are an accredited investor or a FINRA licensed advisor, please join today. The Mauldin Circle program provides exclusive access to alternative investment managers and other thought leaders. In addition, members receive exclusive access to special events and conferences. Upon qualification by my partners at Altegris, you will receive an email invitation. I apologize for limiting this discussion to accredited investors and investment advisors, but we must follow the rules and regulations. I look forward to having you at this exclusive Mauldin Circle event. (In this regard, I am president and a registered representative of Millennium Wave Securities, LLC, member FINRA.)

New York, Seattle, Geneva, Saudi Arabia, and Dubai

After the Thanksgiving weekend I head to New York for meetings and a keynote speech at the CIO Investment Summit, where I will also be on a panel with Jim Grant, whom I will actually get to meet for the first time. I've been a Jim Grant fan for decades, and it will be a delight to sit next to him and hear him speak live. My friend Mark Yusko has put together a powerhouse one-day conference that also includes Kyle Bass and John Paulson.

The following week features a quick trip to Seattle for my partners at Altegris Investments. Then I'll zip back to Dallas to change suitcases and head to Geneva for a few days before returning home for Christmas. Then in early January I leave for the Middle East to speak at MASIC's CSR Policy Forum and to meet investors and leaders in the area. I also plan to visit Dubai for a few days – I've been told it is a place I must see to believe. If you are in either town, drop me a note.

It looks like I should have taken the "under" on whether I would get to move in this weekend. The new apartment is still a swarming hive of workers, all focused on finishing up so that we can be in for a family Thanksgiving dinner. The actual move-in date will be a far more relaxed Monday or Tuesday, although as rooms are finished they are being filled with furniture and all the usual things that make a home look occupied. The kitchen is now installed and ready for the master chef to work his culinary magic for Thanksgiving. Which brings us to…

Thanks to help from my readers, I have elevated the art of preparing a prime rib to a fine science. About 10 years ago I asked readers to share their prime rib secrets. I settled on a consensus approach and have labored over the years to perfect the process. Today I share the results with you – but let's keep it in the family.

The first true secret is to start with a beautiful piece of meat. Find the best butcher in your area and ask for a bone-in standing prime rib. Have your butcher separate the bones from all but the back edge of the prime. I typically cook a 15- to 16-pound seven-rib roast.

Prior to cooking, I create a paste of large amounts of fresh ground pepper, coarse sea salt, very fresh chopped rosemary, freshly crushed garlic to taste, a couple of large chopped sweet onions, and a generous dollop of Cavender's Greek Seasoning, all mixed together with high-quality olive oil until it forms a thick paste. I then criss-cross slice the prime about ¼" deep on its top, bottom, and sides and lovingly knead the paste (and especially the onions) into the meat.

Then fold the prime back over the bones, stuffing any left-over paste into the middle. Place on a rack in a large roasting pan. You can throw in a few vegetables to cook in the juices if you like. Carrots and onions are specially nice, as is squash. (If you put in vegetables, coat the pan with olive oil to prevent sticking.)

The following is critical. Set the oven to no more than 200 degrees. Use a good oven thermometer. Do not trust your dial. Slow-cook the prime, typically about 20-25 minutes a pound. (Yes, that can be 5-6 hours.) Slow cooking is the key to a tender, juicy roast. Put a meat thermometer in the prime and STOP at 120 degrees. If the roast is getting done too rapidly, reduce the temperature. For a medium-rare center, do not go over 120 degrees! My new toy this year is a meat thermometer that can be read from my iPad or iPhone.

Bring out the meat when everything is ready, slice and serve hot with multiple mushroom dishes (my specialty), fresh yeast rolls, lots of different veggies, etc. Prepare for global acclaim.

Well, maybe. This year my brother, who is a master at smoking meat, is going to smoke a prime as well as a turkey. My brother is convinced his prime will be better than mine, and we'll just have to let the attendees judge. I expect some 40-50 friends and family to gather. There will be a deep-fried turkey. Maybe a honey ham. Salads. Cheeses. Dips. Multiple types of dressing. I am flying in pies from a bakery in Montana where some Mennonite ladies have rediscovered a long-lost recipe for pie crusts that are beyond belief. The night before, I will personally make the cakes (Banana Nut and Carrot) from my mother's ancient secret recipes. And guests will, of course, bring their favorites as well. I have 27 feet of counter space, but it will be full!

And while all this sounds fun, there is a bittersweet note. We are arranging an ambulance to bring my mother to the new place as the family gathers from all over the continent. All her children, grandchildren, and great-grandchildren will be in the room. She is slowing down after so many years and is now completely bed-ridden. At 96 she has savored a full lifetime of Thanksgivings, but now her body is gradually rebelling. There will be a sense of fin de siècle with her departure that afternoon, but we will be thankful for that one last moment in time around the Thanksgiving table together and then look to the future as the great-grandkids scamper underfoot.

It is time to hit the send button. Have a great week, and I hope you get to spend it with your family and treasure the moments. And I am thankful you are part of my larger reader family.

Your happily anticipating a few days of cooking analyst,

John Mauldin

subscribers@MauldinEconomics.com

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2013 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.