Rent to Own - Don't Fall for This New Old Retail Sales Trick

Personal_Finance / Shopping Nov 15, 2013 - 02:54 PM GMTBy: Money_Morning

Keith Fitz-Gerald writes: Kmart has joined a long and "distinguished" list of retail chains who offer a rent-to-own program.

Keith Fitz-Gerald writes: Kmart has joined a long and "distinguished" list of retail chains who offer a rent-to-own program.

It's a sign of the times... Only, rather than being a sign of economic recovery, it's a sign of retail desperation.

Ostensibly, these programs are intended to benefit cash-strapped consumers who couldn't otherwise afford to buy big-ticket items. In reality, the program turns consumer goods like a $300 television into a $415 purchase, according to Bloomberg.

Talk about "the vig" ...The imputed interest rate is more than 100%, annually.

It's absolutely appalling, and it ranks right up there with the exploitive subprime lending practices that lead to the financial crisis.

And we're not falling for it...

A Deceptive New Twist on a Very Old Practice

Naturally, the "big box" retailers like Best Buy Co. Inc. (NYSE: BBY), and Kmart's owner Sears Holdings Corp.

(Nasdaq: SHLD), and others don't see the problem.

To their way of thinking, rent-to-own provides a valuable service for customers who "can't otherwise get credit," according to Jai Holtz, VP of Financial Services for Sears Holdings Corp. in remarks made to Bloomberg.

Yeah right... and sheep really want to be slaughtered.

Rent-to-own is not new. In fact, the practice dates back nearly two centuries, when cash-short customers figured out that they could buy goods that they would otherwise have to forego.

The concept is simple, if not alluring. The buyer contracts to pay "rent" monthly - or on some regular payment schedule - until he or she has made payments enough to cover the initial purchase price, plus interest. At that point, the buyer can actually purchase the item in question for a nominal sum, or walk away after returning it to its owner.

What makes rent-to-own really dangerous is the actual cost of long-term ownership, once the dotted line is signed. Payouts on big-ticket items can total two to three times the MSRP. That means that, for example, the $700 computer you want could cost 300% to even 500% more on a rent-to-own plan depending on how long you take to "pay" for it.

Worse still, the true costs of renting to own appear to be purposefully hidden from consumers.

Like the mortgage bankers who peddled billions in liar's loans and the hopelessly convoluted subprime securities that contributed significantly to the current financial crisis, retailers are counting on us not understanding this.

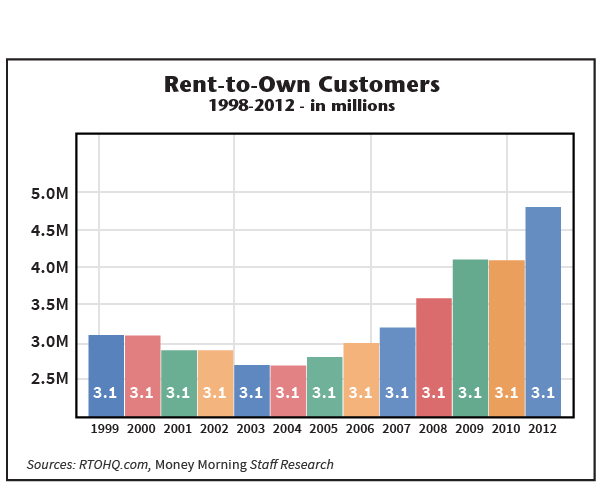

It's not by coincidence that the number of rent-to-own customers has risen sharply in recent years, to an estimated 4.8 million households in 2012 from only 3.1 million in 1999.

I think that's sad for three reasons:

- The fact that so many people rent-to-own is de facto proof that our country continues to be addicted to debt. By calling it rent, the payments may evade consumer loan regulations.

- It's a sign that our economy is not fine, no matter what the Ministry of Whitewash says. Millions of Americans are hurting, and they continue to live paycheck to paycheck despite trillions that have been injected straight into the pockets of fat cat bankers. As far as I'm concerned, Wall Street got bailed out while middle America got sold out.

- Retailers used to have ethics. Like lenders before the subprime mess, they actually cared about their customers and tried to do the right thing.

The concept of a neighborhood banker or store owner was very real. He or she took a vested interest in the local community and its families knowing that doing so provided the values needed for long-term success.

But no more...

Now it's all about the dollar. Any concerns for the customer have apparently been thrown out the window in a rush to pull money out of people's wallets as fast as possible.

One-upmanship in the Age of High Finance has pushed many stores to the point where consumers aren't valued at all, except to the extent they help make quarterly numbers which, in turn, feed big bonuses.

Like frogs in boiling water, cash-strapped consumers have been preconditioned for years by increasingly sophisticated marketing and targeted advertising to focus only on payments.

It doesn't matter whether you're talking appliances, cars, or houses. Everything now comes down to what how much cash something costs now - i.e., the payment. The future be damned.

Which ought to sound all too familiar, given that's what our politicians tell us about the government on the nightly news. "Pay no attention to the future," they say, "we've broken down what this will cost today!"

I just want to scream. But that's a story for another time...

This Can Destroy Peoples' Financial Lives

There's another twist in the rent-to-own story that catches people by surprise.

The rent-to-own industry notes with pride that the term "rent" itself is special because, in contrast to a lease, there's no financial obligation, and no debt incurred when you sign on the dotted line. That means no credit reports, no background checks and no nonsense. There are even automatic bank drafts available "for your convenience." At least that's how the industry wants what they do to appear to the public.

In reality, customers run a huge risk. If they cancel ahead of time and in good standing, there are no problems and no repercussions. But cross the line by even a day, they risk the wrath of the entire financial industry - from aggressive reps calling to collect to banks that pile on fees when those same automatic debit plans create overdraft situations. Not to mention credit report score damage.

So the customers for whom this was all so convenient can easily wind up having their bank accounts plundered and their credit trashed. Horror stories abound about banks refusing to block angry sellers from accessing their customers' bank accounts and creating still more fees.

Naturally, the banks cry foul, saying they're not to blame for consumers who can't account for their money. But I think the fact that they collected more than $32 billion in overdraft fees last year, up $700 million from the year before, has something to do with it.

And that speaks to the state of our economy.

Kmart's fancy new program is no more innovative or customer-driven than I am the man in the moon. It's a sign of desperation, and an unhealthy economy that remains more addicted to debt than ever before.

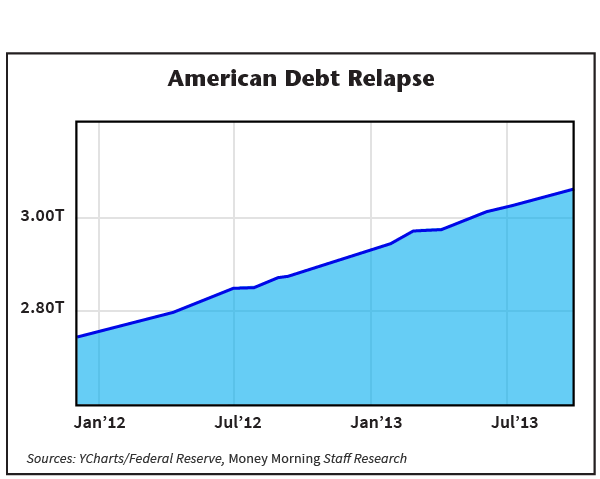

You see, total consumer debt has risen to $3.052 trillion, up 6.05% from $2.87 trillion a year ago as of September.

It seems that Americans are having a debt relapse.

So what's next?

For starters, be very leery of any retail numbers you hear this holiday season.

The National Retail Federation forecasts that average consumer spending will drop by 2% in 2013, while at the same time overall holiday spending will go up by nearly 3%. My guess is the 5% gap goes right into the pile labeled "money customers don't have."

Faced with higher taxes, chronically high unemployment, and another debt "debate" in short order, consumers are stepping back. That translates into lower earnings and still lower expectations ahead for many once-proud brands.

No matter who pays the rent.

Up Next: The Secret to Superior Returns

Taking an active role in your finances is vital, because if we don't control our own destiny, someone else certainly will. You can start now with "The Secret to Superior Returns," excerpted from Keith's book, The Money Map Method.

Source :http://moneymorning.com/2013/11/15/dont-fall-for-this-new-old-trick/

Money Morning/The Money Map Report

©2013 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Money Morning Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.