China Yaun, Renminbi: Soon to Be a World Reserve Currency?

Currencies / China Currency Yuan Sep 29, 2013 - 10:49 AM GMTBy: John_Mauldin

I get the question all the time: when will the Chinese renminbi (RMB) replace the US dollar as the major world reserve currency? The assumption behind such questions is almost always that the coming crisis in US entitlement programs will force the Fed to monetize even more debt, thereby killing the dollar. Or some derivative line of that thought. Contrary to the thinking of fretful dollar skeptics, my firm belief is that the US dollar is going to become even stronger and will at some point actually deserve to be the reserve currency of choice rather than merely the prettiest girl in the ugly contest – the last currency standing, so to speak.

I get the question all the time: when will the Chinese renminbi (RMB) replace the US dollar as the major world reserve currency? The assumption behind such questions is almost always that the coming crisis in US entitlement programs will force the Fed to monetize even more debt, thereby killing the dollar. Or some derivative line of that thought. Contrary to the thinking of fretful dollar skeptics, my firm belief is that the US dollar is going to become even stronger and will at some point actually deserve to be the reserve currency of choice rather than merely the prettiest girl in the ugly contest – the last currency standing, so to speak.

But whether the Chinese RMB will become a reserve currency is an entirely different question. Of course it will, over time, but the question has always been when. There are some preconditions required for reserve currency status. Quietly, apart from anything that might happen to the US dollar, China is working to meet those conditions. Rather than wallowing in concerns about China's actions, we might opt for a more thoughtful and constructive response: to welcome the RMB to the reserve currency club and hope that it gets here soon. The world will be a better place when that happens. And off the radar screen, it may be happening right now. Today we look at global trade flows and international balances and try to imagine a world in which much "common wisdom" gets stood on its head. It should make for an interesting thought experiment, to say the least. (This letter will print a little longer than usual, as there are numerous chart s and graphs.)

One of the prerequisites for a true reserve currency is that there must be a steady and ready supply of the currency to facilitate global trade. The United States has done its part in providing an ample supply of US dollars by running massive trade deficits with the rest of the world, primarily with oil-producing nations and with Asia (most notably China and Japan), for all manner of manufactured products. The US consumer has been the buyer of last resort for several decades (I say, somewhat tongue in cheek). Those dollars typically end up in the reserve balances of various producing nations and find their way back to the US, primarily invested in US government bonds. In an odd sense, the rest of the world has been providing vendor financing to the US, the richest nation in the world.

The US Trade Deficit Turns Positive

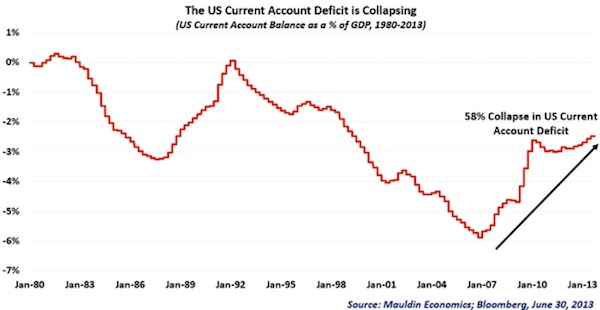

The US trade deficit (a key component of the current account deficit – see chart on next page) fell to an unprecedented percentage of GDP during the last decade, a development that normally heralds a significant drop in a currency. Fortunately, the "exorbitant privilege" of controlling the world's dominant currency in reserve holdings, international trade, and financial transactions has helped shield the US dollar from a hard correction; but that status quo is in danger. After flooding the world with US dollars for more than twenty years, the US has reduced its current account deficit by 58% since the 2007-2008 financial crisis began. Looking ahead, I and many other observers believe this measure can continue to improve, due two surprisingly positive factors:

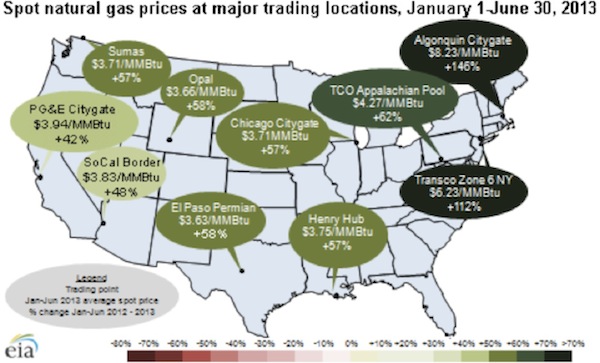

- The US energy boom in shale oil and gas. The US has caught an incredibly well-timed "lucky break" made possible by the combination of new exploration, production, and processing technologies (such as horizontal drilling and fracking) and by the serendipitous discovery of massive supplies of oil and gas, often in areas that already have significant infrastructure and/or are accessible at reasonable costs. This energy renaissance is part of the reality that has made Houston, Texas, the number one port in the United States, with even more growth coming in the near future when the Panama Canal expansion is completed in 2014. US manufacturers are turning less-expensive oil and gas into value-added fossil fuel products and exporting them to the world. This trend will become ever more important. Indeed, when the first LNG export terminal is opened in a few years, the additional exports will approach $80 billion a year, I am told. From one terminal! There are four in the process of being approved and more on the planning boards. The math is there for anyone to do. Spot prices in the US natural gas-producing areas are under $4. The Japanese are paying more than $14. Even I can do that arbitrage. Just for fun, the next graph, from the Energy Information Administration, shows the rise in spot gas prices over the last six months, from a level that had been far too low. It also shows the arbitrage potential that exists right here in the US.

- The consequent renaissance in US manufacturing. With cheaper energy and new technologies like advanced robotics and 3D printing, the US is producing more than we ever have – we're just doing it with fewer people.

These two trends are bullish for the US in general. But that's another story for another letter. The point today is that the US current account deficit is collapsing. A positive trade balance is not an unthinkable prospect today. It is quite possible that the US will be more or less energy self-sufficient by the end of the decade and could have a positive trade balance not long after that. I should note that exporting value-added chemicals made from less expensive energy will contribute even more to the positive balance than simply selling the raw natural gas.

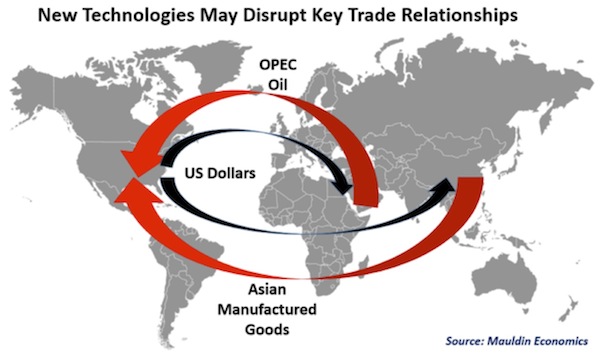

Should the US achieve a positive trade balance, that shift would have a BIG impact on the rest of the world. For starters, moving from a current account deficit to a current account surplus will disrupt the two most important trade relationships in the world today: (1) the exchange of US dollars for OPEC oil, and (2) the exchange of US dollars for Asian manufactured goods. And while the US will continue to import significant (one could even say huge) quantities of manufactured goods, the quantity of dollars moving permanently offshore will be significantly reduced.

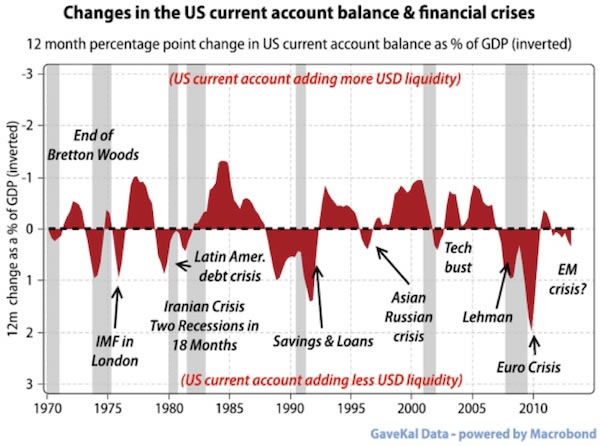

As a quick aside, by definition, a shrinking US current account deficit also means falling liquidity around the world (since the USD makes up one side of the trade in 87% of global currency transactions); and, as our friends at GaveKal have argued for years, a falling US current account almost always means that we will see a crisis somewhere in the world.

This is why the very same emerging-market central banks that complained about the Federal Reserve's quantitative easing under QE3 are now openly calling upon the Fed to reconsider its tapering stance. Now that Fed has hugely inflated the emerging-market balloon, these economies are more vulnerable to popping. I recently read that the Monetary Authority of Singapore (the Republic of Singapore's central bank) suggested rather strongly that the US Federal Reserve should consider its role to be that of central banker to the world and that it should thus make sure there is a sufficient supply of dollars to facilitate global trade. (Their suggestion may be due in part to the fact that they have lost $10 billion in the last year trying to keep the value of their currency from rising.)

With the US current account deficit continuing its fall, we need to be alert for the next crisis abroad. It is very difficult to predict exactly when, where, and how markets will panic, but taking US dollars out of the trading system is akin to losing a chair in a game of musical chairs. Someone is going to be left out. It could be Europe or Japan – there are more chapters to come in the sordid European and Japanese economic sagas – but more likely it will be emerging-market countries loaded with a lot of external debt denominated in US dollars who struggle to keep a seat at the table.

Emerging markets, particularly Asian and Latin American economies, took a beating during the 1990s precisely because of boom-and-bust credit cycles caused by hot capital inflows followed by rapid capital outflows. This volatile boom/bust cycle is precisely what emerging-market policy makers were hoping to forestall by holding larger foreign exchange reserves starting in the late '90s, but trading predominantly in the US dollar left them to vulnerable to swings in market interest rates and Fed policy.

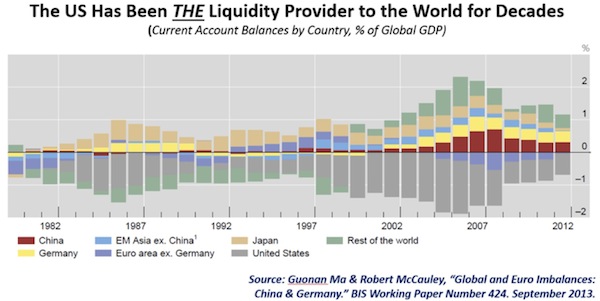

Let's review the current state of global trade imbalances. Fortunately for us, the Bank for International Settlements just released a paper that gives us the data on this very topic (BIS Working Paper No 424: "Global and Euro Imbalances: China and Germany," by Guonan Ma and Robert N McCauley).

You'll want to view following chart in color (if you printed this letter in black and white) in order to appreciate how important the US trade deficit has been to world trade in the past 15 years. Remember, by definition, if there is a surplus in one part of the world, there must be a deficit in another. World trade balances must even out. That can happen through adjustments in the value of currencies or through countries producing as much as they sell. The US is a special case, since 87% of world trade is denominated in dollars; and the demand for dollars is evidently high enough to keep the price up, despite massive quantitative easing.

China Moves to Float Its Currency

Now back to China. I did an extended interview with Louis Gave this past Monday on BNN, the national Canadian business network (part 1, part 2). Let me offer a rough transcription of what he said. I had just commented on my belief that the US is on its way to a positive trade balance, which will make the dollar remarkably strong. The corollary is that there will be fewer dollars available to the world for global trade. Then Louis jumped in:

I think it [a positive US trade balance] is a very important development for the part of the world I come from. I live in Hong Kong. Asia up to now has mostly been a US dollar zone. In Asia we basically produce manufactured goods, sell them to the US, and earn the US dollars we need to trade with one another. So when China trades with Indonesia, the trade is denominated in dollars. When Japan trades with Taiwan, that trade is denominated in dollars.

The big issue is, if we move into a world where the US current account deficit disappears – both through the energy revolution that the US is going through and the consequent manufacturing renaissance – then, all of the sudden, manufacturing in the US is a lot cheaper than elsewhere because the cost of energy is so much cheaper. If the US basically imports [brings back] all of its manufacturing and no longer exports US dollars, how will Asia trade with itself? And how will emerging-market trade grow if they don't earn the dollars?

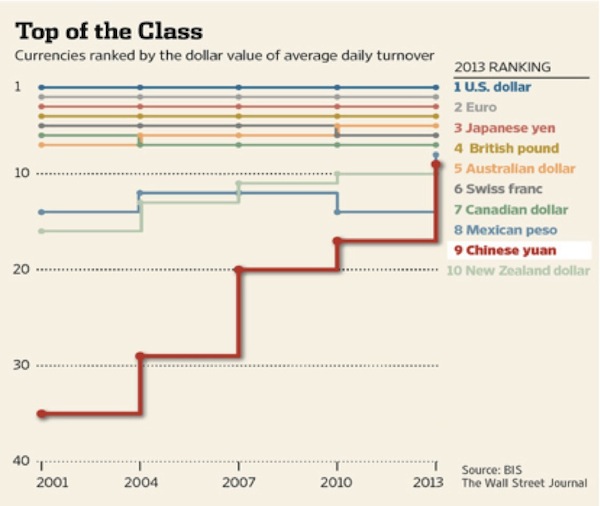

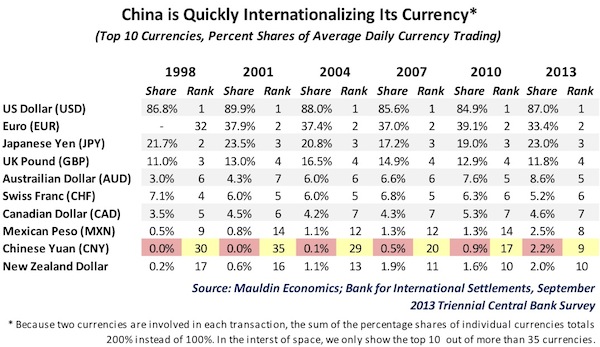

I think the answer to those very important questions will increasingly be the RMB. What you have witnessed in the past two to three years is China making a very apparent play to internationalize its currency. In just two years, China has gone from settling 0% of its exports in RMB to settling 18% of its exports in RMB. Two years ago, the RMB was a non-currency [in international trade/finance]. Nobody owned it. Nobody traded it. Today, the renminbi is already – in just two years – in the top ten traded currencies in the world…. [See the table my research staff found, below. –John]

I think this shift is taking place because China has a massive comparative advantage that most people never think of. If I asked, "What's China's comparative advantage?" 99 out of 100 people would say "cheap labor," but that's not true. Labor is not that cheap in China anymore. China's comparative advantage is that China – alone amongst emerging-market nations – has a deep and credible financial center. It takes 50 years to build a financial center – to, you know, have auditors, lawyers, accountants, judges. And China is very lucky, because in 1997 the Brits – who are quite good at building financial centers – basically built one in Hong Kong and told China, "Here it is. Try not to mess it up."

For twelve years, China did nothing with Hong Kong. It was kind of a deal of "You don't bother us, we won't bother you. We've got other fish to fry." And that worked well until all of a sudden, in the past two to three years, China has been internationalizing its currency through Hong Kong, and it is taking off like wildfire. We always talk about what you see and what you don't. Everybody talks about the China slowdown. Everybody talks about the impact this is going to have on commodities, on countries like Canada, on countries like Australia. Nobody talks about what you don't see. And what you don't see is that China is slowly but surely internationalizing its currency. It's slowly freeing capital controls. It's creating deep and liquid capital markets, and this is going to change the way that companies and individuals finance themselves among emerging markets. It's going to make for more stable emerging markets and hopef ully for higher growth.

Just as Louis predicted years ago, the Chinese RMB has continued to quickly climb the ranks from an internationally non-existent currency to number nine on the list!

This process is happening at lightning speed by historical standards, but we can still expect it to progress over the next 5-10 years. The renminbi is still only involved in 2.2% of foreign currency transactions, but this number can take a big jump when the RMB floats freely, though there is a big difference between the RMB and the true reserve currencies (USD, EUR, JPY, GBP) today. (Note that the renminbi is also called the yuan, abbreviated as CNY in the chart below.) As Louis mentioned, China stands alone among the emerging markets as having the only mature and credible financial center with deep and liquid capital markets, in Hong Kong. The building of a true global financial center typically takes about 50 years, so China is taking advantage of its lucky break to fast-track its currency to reserve status.

What may speed the process up is increasing cooperation between Chinese officials and the UK government to support RMB internationalization through London's FX markets. Gregory Clark, Financial Secretary to the UK Treasury, was in Hong Kong this past week and wrote an op-ed in the South China Morning Post. Let's look at a few telling sentences:

Over 50 percent of UK investment in Asia is in or flows through Hong Kong. That is a tremendous vote of confidence in Hong Kong by UK companies….

Bilaterial trade in goods between Hong Kong and the UK rose by 13.5% between 2009 and 2012, to a total value of £12.1 billion in 2012. This makes Hong Kong the UK's second biggest export market for goods in Asia Pacific….

According to the Society for Worldwide Interbank Financial Telecommunications (SWIFT), London now accounts for 28 per cent of offshore RMB settled transactions.

In London, the volume of Renminbi-denominated import and export financing has increased 100 per cent since 2011. This is delivering real benefits and savings for business. It is estimated that firms can reduce their transaction costs with China by up to 7 per cent by denominating their trade in Renminbi.

The Renminbi’s rise is being enabled not just in Hong Kong and London. Chinese banks have established clearing banks and accounts in more than 80 other countries in the last four years. But the story runs even deeper. It appears to me that China is getting ready to create another Hong Kong in the traditional financial center of China, Shanghai. My good friend and decades-long China expert Simon Hunt notes:

The proposed development of the Free Trade Zone (FTZ) in Shanghai, covering 28sq km, will have huge consequences for China's financial markets and that of the world. It will be a tax-free zone; the RMB will be fully convertible; the FTZ will have its own rules and regulations that cannot be trumped by central government; it will be legally outside the Chinese Customs, in fact a separate territory inside China; it has the effect of abolishing control over capital account investment, so allowing freedom to set up all kinds of companies and moving capital in and out of the FTZ, meaning in and out of China; it will become an international settlement centre for international trade and it will allow banks within the FTZ greater flexibility in conducting business. In short, the implications of the development of the FTZ, if the pilot scheme goes smoothly, will be humungous not just for China but for the global economy.< /p>

One near-term consequence will be that interest rate arbitrage can be more effectively conducted in the zone and will take business away from Hong Kong and Singapore. Chinese companies won't have to set up offshore companies in Hong Kong or Singapore to conduct this business. Already, Chinese and foreign companies are either renting space, putting up buildings or buying office space in the FTZ, just waiting for the final details to be publicised.

This move makes sense for China, as it is a large step toward eventually floating the currency, which is yet another requirement for a true reserve currency. I've written in the past that I think the initial move when the Chinese eventually float their currency will be for the RMB to go down against the dollar (although longer-term it should become quite strong), because there is a lot of money in China that would like to diversify. Setting up a free-trade zone, as they propose in Shanghai, is a way to slowly let the air out of the balloon and perhaps even avoid the dramatic dislocations that might occur if they were to float the currency all at once.

Even so, internationalizing the RMB carries a lot of risk, so why does China really want to globalize its currency? Summarizing from a recent report from DBS Bank (based in Singapore), we can piece the picture together:

- "China has experienced 35 years of relatively stable 10% GDP growth. It's 28 times bigger today than it was in 1978. Why risk this kind of success for a globalized RMB and an open capital account?

- The structure of the global economy has changed radically since 1978 while the financial architecture has changed barely at all.

- Between now and 2020, China's two-way trade will grow by $4 trillion. That's nearly the size of the entire of offshore eurodollar market.

- China doesn't just want a globalized RMB; it needs one. The Middle Kingdom's growth since the 1970s can largely be explained by mobilizing two key factors of production: land and labor. Now that economic growth is slowing in China as a whole (although there are still regional booms in some areas), Chinese policymakers hope they can regain momentum by mobilizing the last factor: capital.

For China to become a powerhouse exporter of its own products, it is eventually going to need to be able to offer financing to its ultimate customers in Indonesia, Vietnam, and the rest of Asia. If you are competing with Caterpillar and Komatsu, you not only need to have a less expensive product, you need to be able to offer financing. The same goes if you're selling telecom gear, power-generation equipment, automobiles, or bullet trains.

In order for a currency to achieve reserve status, there has to be something for the country receiving the currency to invest in. If a country receives US dollars, they can invest in our bonds and stock markets. Just a few years ago, China created the dim sum bond market in Hong Kong, which is beginning to provide a real investment alternative for emerging markets – particularly in Greater China and Southeast Asia, where trade is largely intraregional. With China's having the largest trading flows in the world (it just passed the US, by roughly $1 billion, in 2012), a free-floating RMB could quickly reach reserve status and, oddly enough, take FX market share from the USD, which could become be too strong and too scarce to work well in global trade.

China is on its way to becoming a reserve currency not because of weakness in the US dollar but precisely because the US dollar is going to get stronger and become less readily available. Countries are going to need to be able to trade in something besides dollars. It simply makes sense that if 20% of an emerging-market country's trade is with China, it should do the trades in RMB rather than in relatively scarcer dollars. Of course, this means that China needs to have a relatively stable monetary policy so that its trading partners will have confidence in the long-term RMB, but China realizes that. And of course the RMB will have to meet all the other requirements for being a reserve currency.

Note that there is a difference between a reserve currency and a safe-haven currency. A safe-haven currency must be immune from government confiscation, currency controls, taxation, rapid exchange-rate depreciation, etc.

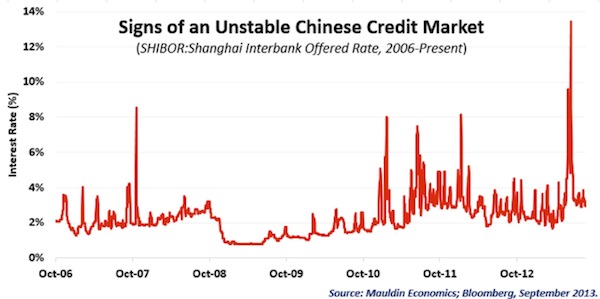

As I mentioned, the RMB will probably depreciate rather than appreciate when the currency floats freely. There is a lot of capital trapped behind China's capital-control wall that wants out, and party leaders know the trick is to make the transition to floating very gradually and without precipitating a crisis. The trouble (although the Chinese will not admit it) is that China is even more addicted to money printing than the US or Japan are. For years, the People's Bank of China has been injecting money into the system each time excess foreign capital flows into the region. (This is necessary as long as China wants to effectively peg the RMB to the USD). Recent rate volatility suggests the Chinese credit system is quite fragile. Quite simply, interest rates do not spike from 3% to 13% in a healthy economy, as they recently did in China (see chart below). This instability suggests there is more going on than we understand. It is also why the floating of the RMB will occur as a series of steps on a journey rather than one big leap. And frankly, that makes sense.

Finally, floating the RMB would also let China dive right into the global currency war that Japan launched last spring. After all, they would just be "giving in" to long-standing US demands that they not manage their currency. China would be able to simply say, "We did what you asked. Why are you complaining about what the free market says about the value of the RMB?" What a perfectly innocent way to escalate a currency war.

In less than a month I will have a new book in the bookstores (see below) on central bank policy and the major global currency war that I and co-author Jonathan Tepper see coming right around the corner. As the proverbial Chinese curse says, "May you live in interesting times."

I mentioned last week that Pat Cox has come to work for Mauldin Economics and that we will soon be launching a new letter called Transformational Technology Alert. I have spent a good deal of time with Pat over the last few years, talking about the technologies that are changing our future; and those discussions have become intense as we have worked out how to get that information to you. There's just so much happening around us every day that is hard to keep track of. I can't tell you how excited I am to finally have Patrick on board, where he can put into writing our shared belief that transformational technologies will build wealth, eradicate disease, extend lives, create jobs, and eventually help build a world of abundance. Rapid change is never easy for those in its path; but I would not want to go back to the "good old days" of the '60s or '70s and find myself once again mired in inefficient medical care, making do with snail's-pace communications, and wandering in an information desert. I had some good moments then, but I'm enjoying the world a great deal more today and expect to have even more fun in the future.

My team is working hard behind the scenes right now to get Pat's new website up and running. But I'm so excited to pull back the curtain on what we have planned for Transformational Technology Alert that I want you to have a clear view of Patrick's work today. You should start reading Patrick immediately – his research is that important. Click here to get access to his letter without delay.

Tucson, the Barefoot Ranch, and New York

I started this letter on the plane from New York and am finishing it at my apartment in Dallas. I'm wrapping up unusually early for me, as I want to go to good friend David Tice's birthday party this evening. (You may recognize him as the founder of the Prudent Bear Fund.) He is hosting us at the Dallas opening of the new film he invested in, called The Secret Lives of Dorks. It is family fare, with James Belushi and a funny part with Mike Ditka. It will open in LA and New York next week and will soon be available on iTunes. Having grown up as a dork before it was cool to be a dork, I will be interested to see what sorts of memories the film evokes.

Next Friday is my birthday, and I will spend it in Tucson with my friends from Casey Research and maybe even try to work in a round of golf. Then I'm back home for a day before driving out to East Texas to join Kyle Bass and a number of fascinating investment minds as we hash through the current economic environment. I will report back.

Later in the month I will return to New York, where we will launch my new book, called Code Red, co-authored with Jonathan Tepper (who also co-authored Endgame). The book is about the effects of unorthodox central bank policies and what we believe will be a quite serious currency war that has already begun and will escalate into the latter part of the decade. I will be doing a few presentations, as much media as I can, and taping a video webinar or two for the launch. Jonathan Tepper has promised to fly over from London, so it should be quite fun.

I got a text this week from my daughter Melissa, inviting me to a Dallas launch party for something called Lyft, an outfit that she is going to be working with part-time. Basically, it is on-demand ride sharing. They offer a web-based service that lets you arrange for a car and driver to come pick you up and take you to your next destination. Rather than charging a specific fare, they operate on the basis of donations. There is of course a phone app, and your donation is tracked remotely. There were 4,000 applications to be Lyft drivers in Dallas, and they chose 86 people. Lyft is in about seven major cities and seems to be rapidly expanding.

I mentioned this new service to my driver as he brought me home from the airport today. He said he had heard of it and then began to tell me about the drama unfolding at the Dallas City Council over the predecessor to Lyft, called Uber. It seems Uber (which is a service that helps you find a town car rather than call a taxi) is taking significant market share from the Yellow Cab franchise, which he says has 70% of the local taxi business. Now those taxis are sitting in a lot during the evenings, as the kids would rather call a town car than a taxi. Go figure. (And given that I prefer my driver service over a cab as I go to and from the airport, I completely understand.) So the Yellow Cab company went to city hall to get Uber banned. And Uber shot back that they don't need a city license because they are licensed by the state.

It turns out that the Yellow Cab owners make substantial donations to people running for city council, or at least that is what Mike (my driver) claims. An even more interesting, it turns out that the Dallas Police and Fire Pension Fund (remember them from last week?) is invested in the Yellow Cab company – but now the company is not quite the cash machine that it was. The lawyers are engaged. It will be interesting to see the response from both Yellow Cab and Uber to the new competition from Lyft. Lyft sees itself as a service to help friends help friends find a ride. Melissa just sees it as a way to make a little money to help pay for her auto insurance (which is a move Dad encourages), while she works on her studies and does freelance writing. (By the way, Melissa was the daugher who had the thyroid cancer 19 months ago. She is doing fine, and there appear to be no further problems.)

I should note that Lyft has raised $83 million from a group of serious venture capital funds. Mike tells me that Uber just got another $33 million from Google. Serious money, considering that $4 million bought 40% of Yellow Cab of Dallas just over 10 years ago.

As a codicil to the above story, when I arrived at the apartment, I stepped out of the car and heard a terrible crunching sound that could only be a serious car wreck. I ran a few feet to the cars, and amazingly both drivers seemed to be okay, although a little shaken up. A Chevy Suburban hit a Lincoln Town Car, so there was a little solid iron around both drivers. It turns out that the town car decided to turn left from the far right-hand lane, which meant it tried to cross four lanes to do so. Looking at the car and driver, Mike speculated, "That must have been an Uber driver. He got a call and was trying to get to the client quickly."

Maybe Dad needs to have a serious discussion about driver safety with Melissa before she goes out Lyfting people.

We had perfect weather in New York this week. And the conversations were even better. You have a great week and drive safely.

Oh, and take a look at our new Mauldin Economics home page! Our techies tell me that if it doesn't look right, you should hit refresh and/or clear your browser's cache. This is just part one of a two-part upgrade we're doing. In the next few weeks the site will be optimized for mobile, so those of you on phones or iPads will soon have a much better experience.

Your still thinking about China analyst,

China Yaun, Renminbi: Soon to Be a World Reserve Currency?

John Mauldin

subscribers@MauldinEconomics.com

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2013 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.