The Story Behind Bear Stearns- Cliff Notes on Financial Maelstrom

Stock-Markets / Credit Crisis 2008 Mar 20, 2008 - 06:12 AM GMTBy: Jim_Willie_CB

As the financial markets stare at the abyss, contemplate the cliff, suffering massive falls in selective stocks, a review of ‘Cliff Notes' might be appropriate. The financial maelstrom is gathering force and fury. The Bear Stearns story has a story behind it, as usual in the Grand Manhattan Den, where violent financial battles give false appearances as desperate measures are played out behind the scenes. The drama on Wall Street will make history. These guys are killing each other, while they cooperate with each other. Like crows, they killed and devoured one of their own.

As the financial markets stare at the abyss, contemplate the cliff, suffering massive falls in selective stocks, a review of ‘Cliff Notes' might be appropriate. The financial maelstrom is gathering force and fury. The Bear Stearns story has a story behind it, as usual in the Grand Manhattan Den, where violent financial battles give false appearances as desperate measures are played out behind the scenes. The drama on Wall Street will make history. These guys are killing each other, while they cooperate with each other. Like crows, they killed and devoured one of their own.

BROKERAGE FIRMS REEL

Bear Stearns was fed to the wolves, an easy correct forecast from last early autumn. Denials nowadays constitute confirmations, from mere mention. Their refusal in 1998 during the Long Term Capital Mgmt bailout to act like a Wall Street team player was the hidden motive to carve them into pieces. One must ask why last Friday it traded around the $30/share price all day long after 10am . The answer is easy, as they wanted to give insiders a chance to sell most of the 186 million shares, a gift of $5 billion sure to anger many.

My view is that JP Morgan took its best assets at discount, tossed much of the damaged assets into their Wall Street garbage can, which is never emptied, never sees any balance sheet, blessed by the US Federal Reserve, protected to new security laws. If Bear Stearns share holders reject the JPM seizure takeover, then the gem Bear Stearns headquarter building in Manhattan can be bought by JPM for a song. Actually, JPM might have only started the bidding process, sure to result in JPM upping their own bid. BStearns has (or had) 14 thousand workers, most having been paid in stock share bonuses in recent months. The economy in New York City is sure to be badly harmed, worse than already. Wall Street jobs account for 35% of NY City wages.

The other story not told is that Bear Stearns was dissolved before the wrecked investment bank had a chance to take advantage of the Term Security Lending Facility . It will be made available by the US Fed at the end of March. The sleazy hogs on Wall Street wanted to remove one player at that window. The other story not told is that a liquidation of Bear Stearns would inevitably have resulted in a massive credit derivative meltdown. The consequences cannot be estimated. The derivative upside down pyramid is mammoth. No precedent exists for its partial unwind or dissolution. The pyramid holds together the entire US Treasury complex, attached to interest rate swaps, attached to credit default swaps of various types, and so on. This pyramid is leveraged 70 to 1.

The talk is funny though, since the US Fed has backstopped only $30 billion in Bear Stearns securities. What about the other $800 to $1500 billion rancid bonds floating within striking distance to Wall Street and major bank balance sheets? In truth, we might later learn that Bear Stearns helped to bail out JP Morgan, in helping to shore up its credit derivatives , in providing some emergency collateral, soon to bust, to prevent a JP Morgan failure!!! JP Morgan owns $7.778 trillion of credit derivatives, two and half times as much as Citigroup, the same toxic stuff that crippled Citigroup. JP Morgan skated on this one without publicity.

The other story is that Bear Stearns CEO Alan Schwartz assured just last week that all was well, liquidity was adequate, and the company was in good shape. Enron CEO Ken Lay said the same thing. And lest one forget, Enron and Bear Stearns have a common denominator in JP Morgan being a key player in the operations and agent during the demise of the two firms. JPM taught Enron everything they knew about offshore special purpose entity firms, yet they escaped all legal challenges by losing clients in court. When the US Fed frees JPM from liability on any losses from collateral submitted by Bear Stearns, one has to giggle since the US Fed is JP Morgan Think consolidation of the best bond assets in JP Morgan's hands. Think more damage and consolidation upon the next victim, like Lehman Brothers. Think building the Fed Reserve bank system. The Mussolini Fascist Business Model might be opening a new chapter.

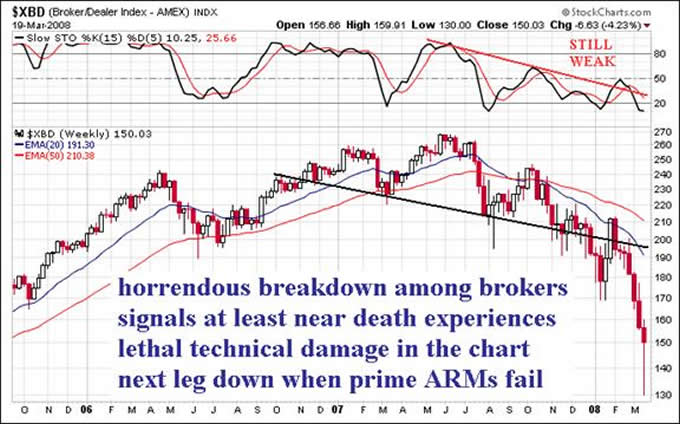

The XBD banker broker dealer stock index had a horrible day on Monday, with some repair on Tuesday and Wednesday. The XBD stock index fell 11% in a visit to hell and back, rendering big technical damage to many component stocks, especially Lehman Brothers. LEH fell by 19% on Monday. Goldman Sachs was down 10% early in the day, closing down 4%. Citigroup lost another 7% after being down almost 10%, UBS lost 11%, Morgan Stanley lost 8%, Merrill Lynch lost 4% after being down 8%.

The stock price action tells the wary observer to expect a challenge or near death experience for Lehman Brothers, possibly worse.

Their portfolio is similar to Bear Stearns, only larger. The mortgage bond damage will next shift to the prime adjustable mortgages, so reckless in their innovation. They will crater this summer upon rate reset, victims of their own written time bombs. Thus the deserved name of Exploding ARMs. Even US Fed Chairman Bernanke acknowledged last week that 40% of all mortgage defaults are prime, not subprime. On two days, the XBD broker dealers recovered most of the loss. The broker dealers play a significant role, to manage the execution of official policy, full of the requisite manipulation and corruption of markets. See the management of the credit derivative pyramid, the gold ambushes, the currency interventions, the collusion with the debt ratings agencies, and even possibly the intimidation of the monoline bond insurers to serve as the bagholders in the historically unprecedented international sale of fraudulent mortgage bonds. Can anyone defend against my claim that the Untied States upper echelons represent institutionalized and protected dishonesty???

My warning quip to the idealists among us has been often used lately, when people salivate over the prospect of chronic conmen suffering deep losses, enduring insolvency, incapable of shame, yet almost certain to end up in some form of bankruptcy. My stated line is “Beware when billionaires face bankruptcy, since they make a phone call and change the rules. Often those rules conflict with your strategy and plans.” This time the rules might be concerning gathering wealth from strategies that oppose the defense of a national financial integrity.

This time those attempting to secure their wealth and protect it from illicit national grabs and seizures might be labeled as unpatriotic. This time the system has been virtually broken by decades of destructive inflation, of misspent funds, of grand theft (see Fannie Mae and military contractors), of encouraged abandonment of the manufacturing sector, of destructive emphasis of a war economy footing, of irresponsible Medicare guarantees, of harmful demographic shifts, and lately of incredibly deep bond fraud. The bond fraud episode is the crowning finale of the US banking system, with toxic outlets to most global banking centers. One might wonder if it were planned.

REMINISCENT OF GREAT DEPRESSION

When Bear Stearns was dissolved and its assets rescued, the US Fed and JP Morgan invoked a feature of banking policies not used since the Great Depression. Too many other comparisons can be made to that dreaded era. The bank insolvency is the biggest commonality. The ability to print money, shovel printing press output from one room to another easily, permit phony accounting of balance sheets, hide within offshore subsidiaries, and extend the risk model to great heights, these are new & better innovations not available 70 years ago. Well tragically, these innovations are being unmasked as thin, flimsy, unable to withstand storms, and possibly even fraudulent.

As the stock market and bond market suffer blow after blow, fail to stabilize, fail to recover, only to endure more breakdown in the structure, memories come to the Great Depression, when recoveries only led to deeper losses as the catastrophe unfolded.

This time around, another catastrophe is expected in a bank system meltdown, a bond system total seizure, and a risk model system dissolved.

Amidst all this maelstrom, one must ask if wisdom prevailed during the Clinton Administration to repeal the Glass Steagall Law from the Great Depression era. That law created the Federal Deposit Insurance Corp for insuring individual banks and depositors, up to $100k per account. The law also blocked any attempt to merge banks, brokerage firms, and insurance companies. The legislation intended to protect a meltdown to spread to all critical structural elements of the financial system. With the Glass Steagall repeal, one has to wonder if some destruction was planned, or else a major consolidation was the ultimate goal. My belief is firm, that powers in Old Europe and London that control the US Fed more than is publicly known are restoring power back to Switzerland. They have resented the arrogant and reckless US bankers for two generations.

By the way, the FDIC insures bank accounts. But the SIPC guarantees participating brokerage accounts up to a $500k limit, plus $100k on cash accounts. People might soon hear more about their stock protection if giant financial conglomerates go bust. Some stock accounts might be frozen, as the courts sort it all out. When an SIPC member becomes insolvent, SIPC will ask the court to appoint a trustee to supervise the liquidation of firm assets and to process investor claims. Coverage of bank and brokerage accounts will be a popular topic soon.

3 SCARY GRAPHS: BANKS, MONEY & HOUSEHOLDS

Some have asked in private emails whether the bigger the bank, the safer their future. My answer is simple. The bigger the bank, the more likely they are to hold a much riskier portfolio, and thus the more likely their failure.

Most big Wall Street banks and broker dealers, along with a scattering of major US banks are in the same pickle, from owning too many mortgage bonds and related credit derivatives leveraged from them, even being saddled with bonds scheduled for interrupted private equity deals.

Bank assets have vanished. The neighborhood bank with branches of operation only within a corner of their resident state is probably much more insulated from the bond market debacle. They likely originated loans, own some, but might have recycled most of them through Fannie Mae in order to continue to earn fees on new loans. Some have asked if the US Fed can make unlimited number of bank bailouts, can refund on unlimited number of mortgage bonds submitted by banks. Well yes, sure, but the accumulating risk to the US Dollar is being recognized and felt. The US $ decline is not done; it is going lower.

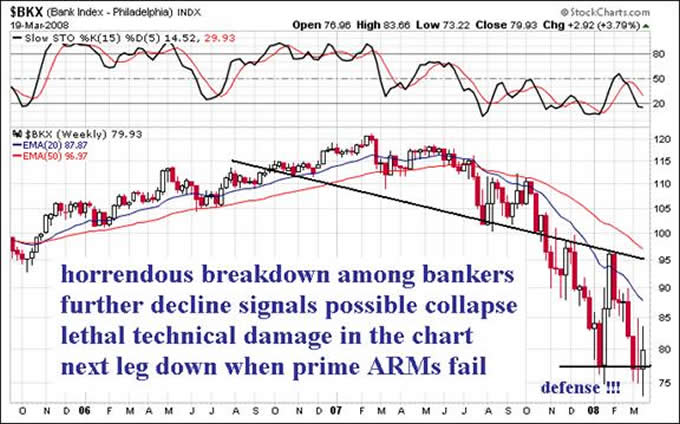

The US banking system is teetering at the precipice, the brink of collapse. Almost two years ago, in the Hat Trick Letter, my forecast was made crystal clear, that the housing crisis and mortgage debacle would topple and destroy the US banking system, just like what happened to Japan in the 1990 decade. The US banking system cannot withstand insolvency like the stronger Japanese banking system, which survived temporarily as vampire entities. Weekly events point to wrecked mechanisms in the US banking system. They will continue to worsen unfortunately.

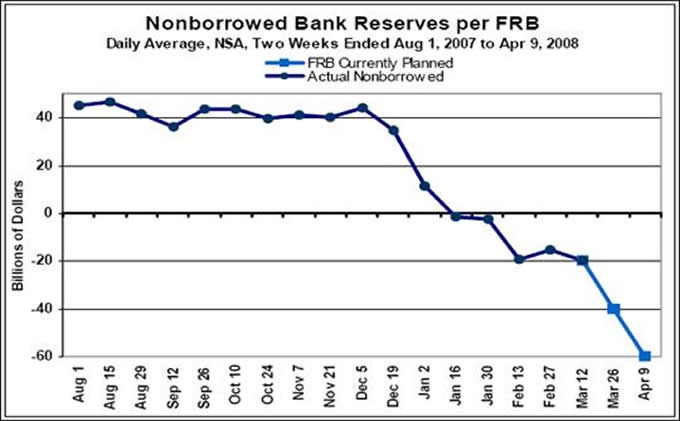

The financial condition of institutions within the US banking system has gone critical, with core assets gone negative. Total deposits held, free of borrowed US Fed reserves, have vanished. US banks have burned through their entire capital core, melted down from disastrous mortgage portfolios, their bonds, and related CDO leveraged bond derivatives. They must now rely upon borrowed reserves from the US Fed in order to continue to function as lending institutions. They have turned heavily to the US Fed Term Auction Facility and now the Term Security Lending Facility for resupplied capital. That is not injected, donated, free money. It must be returned, or such is the plan. With the TSLF, the US Fed now extends loans for AAA-rated mortgage bonds of private vintage, not just Fannie & Freddie type. They expanded to $200 billion per month and 28 days in duration, with a lowered 3.25% borrowing rate, and likely renewable feature. As we know, many AAA bonds are crappy. So banks might be unloading some rancid meat. The masters who control the US Fed cannot be happy.

The US banks by early December had about $43 billion in total reserves. The current statement by the Federal Reserve offers a daily average ‘Non-Borrowed Reserves' at MINUS $20 billion. Worse, the Fed Reserve estimates by early April that amount will be MINUS $60 billion. The US banks are living off borrowed money, and time. Be prepared for some high profile bank failures, a process already begun. Home loan defaults have combined with falling home collateral valuation to destroy mortgage bonds and related securities to the extent that banks have lost their entire capital. The only way to recover from this situation is for banks to find a way to make a lot of money really fast. The time has grown urgent to inflate rapidly, or else face an unstoppable chain reaction of bond failures followed by bank failures. Big banks do not have adequate loan loss reserves set aside. Money and wealth will be destroyed either from falling home portfolios and mortgage bond values, from reckless lending and much fraud at all levels.

The shocking reality is that the banking system has gone from a 10% reserve requirement to a minus 5% requirement. Still too much bank capital is in illiquid overvalued bonds. The US Fed is trying to increase the money supply faster than banks can write down losses. Keep in mind what New York University economics professor Nouriel Roubini says, “For every dollar loss of capital, you reduce lending by ten dollars.” The Shadow Govt Statistics folks do such great work in removing deceptive games and gimmicks. They report the US $ money supply is growing at an annual 18.0% rate, March 2007 over March 2007. The sitting Secy of Inflation Bernanke, when pressed in Congress recently to comment on the monetary inflation gone haywire, simply said they monitor the Consumer Price Inflation only. Wow! Talk about riding a horse while sitting backwards on the saddle! What a hack! What a lousy cowboy!

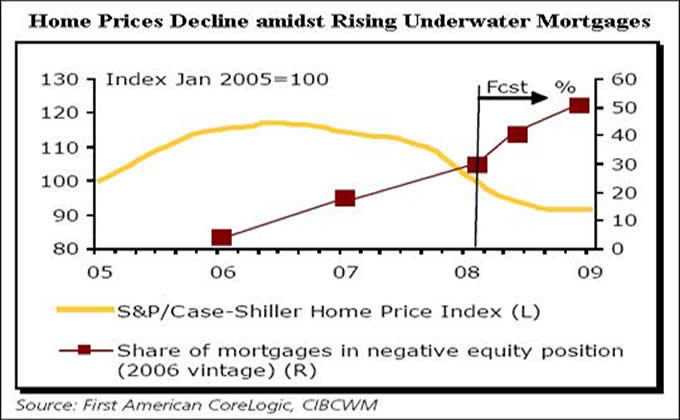

Many standing loans involve homeowners who owe a greater loan balance than the home is worth, the home equity having evaporated. And home prices are heading lower. Chronicling the Great American Tragedy, the New York Times writes, “Not since the Depression has a larger share of Americans owed more on their homes than they are worth.

With the collapse of the housing boom, nearly 8.8 million homeowners, or 10.3% of the total are underwater . That is more than double the percentage just a year ago.” To this date, US Fed, Dept Treasury, and US Govt efforts have not accomplished much toward reversing this trend. Tragically, of mortgages originated from 2006 onward in recent vintage, 30% are now burdened by negative equity. The ratio of under-water mortgages, those with negative equity, the ‘Upside Down' loans, for these more recent loans is forecasted to rise to more than 50%. The mortgages of older vintage are also rising in their negative equity ratio. They are catching up to the newer vintage home loans. The national housing foundation is going underwater. Contrast with falling home values, which might not stabilize in 2008 as the graph shows. Note two different scales describe the two series.

The latest data on home foreclosures, delinquencies, late payments, existing home inventory, new home inventory, and median home value does not indicate in any manner whatsoever that the housing market has even remotely stabilized. More mortgage bond pain and bank writeoffs are to be expected by anyone not hindered by rose colored glasses, banker public relations motives, or US Govt mental handicaps. California and Florida continue to bear more than their share of national foreclosures. The two states accounted for 30% of mortgages entering the foreclosure process. Arizona and Nevada are sure to increase sharply in the next couple quarters. The big new twist is voluntary foreclosures, abandonment of homes and their loans, in direct response to running under-water with home equity gone, perhaps negative. People are choosing not to service debt on a deflating failed asset.

CENTRAL BANK INTERVENTION NEXT

As the US Dollar continues to reel, to decline to low levels never seen before, support does not exist. Clearly, some form of central bank intervention is next. However, in order for such extraordinary action to be effective and not futile, monetary policy must be coordinated and cooperative. The major central banks must work together to support the US Dollar They must cut official interest rates in concert with the US Fed That means the Euro Central Bank must agree to an official cut in its rigid interest rate. They might employ an interim rate cut. Even a 25 basis point cut would be significant. They must publicly state that they are defending against a rising euro currency, and that price inflation will be a risk to stomach. The planned goal would be to end the US $ decline. The extra benefit would be seen in the bond market and banking system, from added liquidity and soon housing price stability. Without dispute, the underlying problem is the housing crisis and price declines in collateral.

My attention is squarely focused on the Euro Central Bank, which has the greatest potential to quickly change the awful sentiment plaguing the US Dollar The US Fed just cut interest rates again by 75 basis points. The US Dollar had moved down in anticipation of this latest cut. The Bank of Canada has cut twice its interest rate. The Bank of England has also cut its official rate, only once, and surely will again. The Bank of Japan is talking about a rate cut. But the Europeans are dominated by the Germans, who want no rate cut at all. The Germans warned of the precise problems seen right now, do not wish to fix a problem with more of the same actions that produced the problem, and resent having to foot the bill during the aftermath of these problems.

The gold price will not stop at the $1000 milestone. The silver price will not stop at the $20 milestone, and will vastly outperform gold. The crude oil price might go below the $100 milestone briefly, but will return and shoot past the century mark. No no no!!! All are heading much higher, because the banking problem is not to be soon fixed, the bond problem is not to be soon fixed, the economy is not to be soon fixed, household distress is not to be soon fixed. Maybe none can be fixed, even as money thrown at the problem accelerates parabolically.

The limited power of US Fed solutions, and limited arsenal of devices to treat the problem, will ensure that monetary inflation will be the main tool. Still, adding liquidity in rescues, repairs, and bailouts is not seen as the cause of the problem. It still is seen as the immediate solution. SUCH IS THE HERESY THAT HAS DESTROYED THE US BANKING SYSTEM. They operate under an objective to revitalize the housing market, and stop its price decline. They must enable the bank system to become solvent. All that administered inflation means much more gains to gold, silver, and even crude oil. Bigger problems than rising gold, silver, and crude oil come if Consumer Price Inflation starts to grow without bounds. The US Treasury Bond market will suffer heart attacks, the beneficiary being gold, silver, and crude oil!!!

Remarkably, when the US Fed was about to predictably cut the official interest rate again, gold mysteriously got hit on Monday. On the day of the rate cut Tuesday and the following day Wednesday, gold got hit again and the US Dollar rallied. The Boyz were busy. The smackdown of gold under $950 and of silver under $19 only managed to remove and cleanse these two important metals markets of their overbought situation. The Boyz have cleared the path for gold to reach $1100 and for silver to reach $26. Nothing has been solved yet on most critical battle fronts. The bigger moves up are yet to come!

THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS.

From subscribers and readers:

“Your financial commentaries are extremely insightful and have saved me a ton of money. The subscription has more than paid for itself. This should be an interesting year to say the least!” (RickF in Texas )

“The unfortunate demise of Dr. Kurt Richebacher leaves Jim Willie, Bob Chapman, and Jim Sinclair as the finest financial minds on the scene today.” (DougR in Nevada )

“There are four writers that I MUST READ. You are absolutely one of those favorites!! William Buckler, Ty Andros, Richard Russell, and YOU!!” (BettyS in Missouri )

“Your newsletter caught my attention when the Richebächer report ended. Yours has more depth and is broader in coverage for the difficult topics of relevance today. You pick up where he left off, and take it one level deeper, a tribute.” (JoeS in New York )

By Jim Willie CB

Editor of the “HAT TRICK LETTER”

www.GoldenJackass.com

www.GoldenJackass.com/subscribe.html

Use the above link to subscribe to the paid research reports, which include coverage of several smallcap companies positioned to rise like a cantilever during the ongoing panicky attempt to sustain an unsustainable system burdened by numerous imbalances aggravated by global village forces. An historically unprecedented mess has been created by heretical central bankers and charlatan economic advisors, whose interference has irreversibly altered and damaged the world financial system. Analysis features Gold, Crude Oil, USDollar, Treasury bonds, and inter-market dynamics with the US Economy and US Federal Reserve monetary policy. A tad of relevant geopolitics is covered as well. Articles in this series are promotional, an unabashed gesture to induce readers to subscribe.

Jim Willie CB is a statistical analyst in marketing research and retaicl forecasting. He holds a PhD in Statistics. His career has stretched over 24 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com . For personal questions about subscriptions, contact him at JimWillieCB@aol.com

Jim Willie CB Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.