Do We Really Need the Federal Reserve Bank?

Politics / US Federal Reserve Bank Mar 26, 2013 - 01:23 PM GMTBy: Money_Morning

Keith Fitz-Gerald writes: Last week I spent two days speaking to senior government officials and business leaders in Bermuda, which is one of the world's leading international insurance and reinsurance hubs. The men and women in the room are responsible for hundreds of millions in assets worldwide.

Keith Fitz-Gerald writes: Last week I spent two days speaking to senior government officials and business leaders in Bermuda, which is one of the world's leading international insurance and reinsurance hubs. The men and women in the room are responsible for hundreds of millions in assets worldwide.

I spoke for over an hour on the implications and opportunities of the financial crisis (I'll have specifics for Money Morning readers next week).

As I was finishing up, I received one of the most provocative questions I've gotten in a long time from the darkness beyond the stage lights: "Does any nation really need a "Fed,'" asked one of the directors?

The answer is, unequivocally, "no." Especially if it's modeled after the United States Federal Reserve.

The individual depositors who were the protected class when the Fed was originally formed are little more than cannon fodder today. Instead, the banks the Fed supports have become the protected few.

To be honest, I didn't always think this way. For much of my career, I took the Fed for granted, believing like millions of Americans that it was acting in our country's best interest.

Then I sat down with legendary investor Jim Rogers in Singapore a few years back at the onset of the current financial crisis. During our discussion, he pointed out several things that really made me think about the Fed and its role in not only creating this crisis, but making it worse.

A 100 Year-Old Affront to Freedom

The American Fed as it operates today is an insult to anybody who believes in economic and political freedom. In an era of globally-linked finance, the very concept of a Fed is an abomination.

I realize that this may not sit well with you if this is the first time you've thought about the issue.

So let's walk you through a few things that will challenge your thinking...

The Fed was established in 1913. It's only 100 years old. And it's anything but an original part of America's economic machine.

Its original purpose was simple: To prevent banking failures.

At the time, the United States had just gone through the vicious bank panic of 1907. That crisis was significant because it saw the failure of Knickerbocker Trust, which sought -- but failed -- to receive financial support from its peers. Unable to obtain liquidity from any source, Knickerbocker Trust collapsed.

This affected public psychology deeply because Knickerbocker's peers not only chose not to rescue Knickerbocker, but also suspended payments to each other.

This boomeranged through the system and came to roost at the retail level when the public figured out that they didn't have access to their money, especially in "specie," meaning in gold. Bank runs and closures became the norm. The New York Stock Exchange fell 50% before financier J.P. Morgan famously locked banking executives in his personal library and formulated a liquidity injection that ultimately calmed everything down.

Loath to waste a good crisis, legislators stepped up to the plate by agitating for centralized banking as a means of restoring public confidence while providing the banking system with a source of liquidity that would prevent their wholesale collapse.

And they got it a few years later...in spades.

What's really interesting to me looking back using today's lens is how sophisticated the machinery of the time was. Powerful public and private figures worked together, often in great secrecy like they did at Jekyll Island, Georgia, to build the framework for the Fed. The Wall Street Journal published a 14-part series highlighting the need for a central bank. Citizen groups and trade organizations piled on.

And voilà...the Fed was born under the guise of a politically independent institution that would stabilize the financial system, protect the monetary supply against inflation, and maintain credit as needed by injecting stimulus when the economy flagged and withdrawing it when things were overheated. In the terminology of the day, this was viewed as giving elasticity to the dollar which would, in turn, establish more effective control over the banking system.

None other than the Comptroller of the Currency observed that the Fed would supply a circulating medium that is "absolutely safe." What irony.

Fast forward to today.

Every 1913 dollar is now worth $0.04 cents. Goods and services that cost a buck back then now will set you back $21. Where's the stability in that?

If that's not practical enough, consider wages.

According to the U.S. Census Bureau, the median income of male workers in 2010 was $32,137 while the median income of male workers in 1968 was $5,980. On the surface this isn't too shabby. It's a 437.4% increase over 42 years - or an average income gain of 10.41% a year, over the same time period.

However, if you run the numbers the other way, using 2010 dollars, a very different picture emerges. You quickly see that median earning male workers actually have less purchasing power today than they did 42 years ago ($32,844 vs. $32,137).

That's your Federal Reserve at work. It's robbing America by gradually sucking the life out of the financial system. Over time, it will cause the system to collapse -- just ask anybody in the former Soviet Union. They had a "Fed," and no Soviet bank ever failed per se. However, the state eventually took so much wealth from the people that the entire system broke.

Taxation Courtesy of the Printing Press

Legions of spend-it-while-you-can politicians and economists don't see it this way. And neither, perhaps more importantly, does sitting Federal Reserve Chairman Dr. Ben Bernanke.

He said explicitly on November 21st, 2002, in remarks to the National Economists Club that, "by increasing the number of dollars in circulation, or even by credibly threatening to do so, the U.S. government can also reduce the value of the dollar in terms of goods and services, which is equivalent to raising the prices in dollars of those goods and services."

In other words, he believes he can create economic value merely by printing money. It's no wonder that he continues to print money today (euphemistically calling it "quantitative easing") knowing full well that he is eviscerating the dollar. He believes that doing so is the same thing as raising prices by managing inflation.

In fact, inflation is actually defined as the artificial increase in the supply of money and credit. It's a tax by any other name. So what Bernanke is really doing is artificially taxing the American public by debasing its currency. It's no wonder that more people have less. But here's where it really hits home for me.

When the Fed was created, it was envisioned as a source of liquidity for the banking system. The presumption was that any specific failure in the banking system subject to the Fed's oversight would be offset by the available cash from the government because it had centralized the credit risks associated with their lending portfolios.

In today's environment, credit is diffused globally far beyond the Fed's reach. What's more, there's too much of it and the banking system is now so big that the risks it holds dwarf the Fed's liquidity capacity. For example, there are an estimated $600 trillion to $1.5 quadrillion in derivatives products worldwide at the moment. Global gross world product is approximately $79 trillion by comparison.

Contrary to what Bernanke and others who are so tightly involved in the system believe, this crisis was not caused by a lack of liquidity. Rather, it was caused by too much money sloshing around in some sort of unregulated mosh pit with inadequate supervision and inadequate regulatory oversight.

The real villain here is that excess liquidity is leveraged. This lets big banks buy derivatives for pennies on the dollar yet exposes them to hundreds of billions in market risk.

The sad reality is that Bernanke and his central banking buddies in "Feds" around the world could print money till the end of time and they still wouldn't be able to print enough to guarantee liquidity. Yet they will continue to try because that's the only way they keep the illusion going.

It's also the only way they keep a handle on their version of risk...to the system. And that brings us full circle.

Success by its very definition includes failure. People forget that the discipline of failure is integral to capitalism. When the Fed creates money out of thin air, the risk of failure does not exist. Without the risk of failure, the big banks know they can place one way bets and not worry about losses because they are literally "too big to fail."

In fact, management and traders are paid to do exactly this. If the monstrous one-way bets pay off, they get up to 50% of the profits. If the bets go bad, the stockholders, the Fed, and now the public eat the losses.

So they have every incentive to act in their own interests while reinforcing incompetent management, improper risk taking and inefficient operations. Politicians and regulators are incentivized the same way, since the Fed also makes it possible for them to skirt the issue of responsibility.

The Fallacy of Free Money

Which brings me to the last sacred cow I want to barbeque today: Interest rates.

The Fed spends a good deal of its time and our money promoting and maintaining low interest rates. It's doing so on the assumption that low rates prompt everyone to put money to work by making savings less appealing. But ask Japan how much demand there was when money was free - the answer is next to none.

The trillion-dollar problem is that this economic assumption presumes the savings are there in the first place. In reality, America and other "Fed" nations are flat broke. There is no savings pool to draw upon, which means the foregone assumption is a bust. At some point, people who do not have cash cannot pay for the goods and services they need -- no matter how much liquidity is in the system.

International capital markets actually exacerbate the problem because other governments and major trading firms purchase that very same excess liquidity which they, in turn, then begin using as collateral for their own expansion.

Congressman Ron Paul, a staunch Fed opponent, summed it up much more eloquently than I ever could in his book, "End the Fed," noting that "those who suffer [rarely] see the connection between Federal Reserve monetary policy and the suffering that comes as a consequence of financing" big government and big banking."

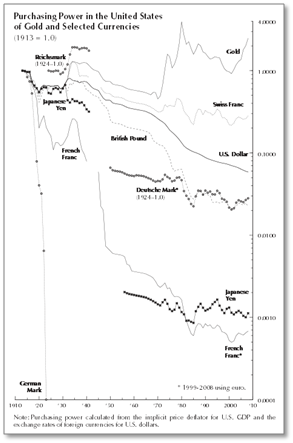

Under the circumstances, is it any wonder that almost every currency in recorded history that is controlled by a central bank has failed or is failing? Here's just a few since 1913 when the Fed was formed.

No. We do not need a Fed because dissolving it would:

■Force any government that has one to live within its means;

■Restore the appropriate level of risk to the global financial community; and,

■Nullify the risks involuntarily forced upon the public in the name of political priorities.

As for how we dissolve this mess, that's a subject for another time and another email.

Source :http://moneymorning.com/2013/03/26/do-we-really-need-the-federal-reserve/

Money Morning/The Money Map Report

©2013 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Money Morning Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.