No End in Sight for Global Currency Wars

Currencies / Fiat Currency Feb 15, 2013 - 12:15 PM GMTBy: Gary_Dorsch

With frigid temperatures expected to hover between 15-degree and 23-degree Fahrenheit this weekend in Moscow, it’s a wonder why the world’s most powerful finance chiefs and central bankers would schedule their Feb 15-16th meeting in Vladimir Putin’s backyard. Instead, a better venue for the Group-of-20 would’ve been the Cayman Islands. The Islands are warm year-round, with average highs holding steady in the 80’s. January and February are the coolest months with lows averaging in the lower 70’s. However, Russia holds the presidency of the G-20 this year, - so finance chiefs will have to endure the frozen tundra.

With frigid temperatures expected to hover between 15-degree and 23-degree Fahrenheit this weekend in Moscow, it’s a wonder why the world’s most powerful finance chiefs and central bankers would schedule their Feb 15-16th meeting in Vladimir Putin’s backyard. Instead, a better venue for the Group-of-20 would’ve been the Cayman Islands. The Islands are warm year-round, with average highs holding steady in the 80’s. January and February are the coolest months with lows averaging in the lower 70’s. However, Russia holds the presidency of the G-20 this year, - so finance chiefs will have to endure the frozen tundra.

A January 16th warning issued by Russia’s central banker Alexei Ulyukayev has also set the narrative for the G-20 meeting. “The world is on the brink of a fresh “currency war.” Japan is weakening the yen and other countries may follow. If Japan continues to pursue a softer currency, reciprocal devaluations would hurt the global economy,” Ulyukayev warned. “We’re on a threshold of very serious and confrontational actions. The new government of Japan is a course towards a very protectionist monetary policy through a sharp depreciation of the yen. Other colleagues from respected central banks and governments already pursue this policy. This is not a path towards global coordination but rather a separation,” Ulyukayev declared.

Guido Mantega, Brazil’s finance minister, quickly chimed in, warning that the Federal Reserve’s “protectionist” gambit to roll out more quantitative easing (QE) would reignite “currency wars” with drastic consequences for the rest of the world. “It has to be understood that there are consequences. The Fed’s QE-program ($85-billion per month of money printing) will “only have a marginal benefit in the US as there is already no lack of liquidity. And that liquidity is not going into production. Furthermore, Japan’s decision to expand its own QE, coming on the heels of the Fed’s decision (to expand QE to $85-billion per month), is evidence of growing global tensions. That’s a currency war,” he declared.

Yi Gang, a deputy governor of the People’s Bank of China (PBoC), and chief of the State Administration of Foreign Exchange, said he’s worried about the fallout from QE and the Zero Interest Rate Policy (ZIRP), in the G-7 economies. “QE for developed economies is generating volatility in financial markets in terms of capital flows. Competitive currency devaluation is one aspect of it. If everyone is doing super QE, which currency will depreciate?” he asked.

As the European, Japanese, and US-governments sink deeper into a morass of debt, the ruling politicians are pressuring their central bankers to print more money, in order to finance their budget deficits. So far, five central banks, - the Federal Reserve, the European Central Bank, Bank of England, the Bank of Japan and the Swiss National Bank have effectively created more than $6-trillion of new currency over the past four years, and have flooded the world money markets with excess liquidity. The size of their balance sheets has now reached a combined $9.5-trillion, compared with $3.5-trillion six years ago.

In turn, the tsunami of ultra-cheap cash is inflating bubbles in the world’s bond and stock markets. On Feb 13th, hedge fund trader Jim Rogers commented, “The US-stock market is near its all-time highs because the Federal Reserve is printing staggering amounts of money. This is very artificial,’’ Rogers warns. And the willingness of the political puppets at the Fed and other central banks to keep buying hundreds of billions of dollars' worth of government bonds makes it easier for the ruling political elite to sustain the massive deficit spending that’s running up a record-breaking national debt. Rogers adds, “It’s a vicious cycle and it’s all insanity. No sound person in his sound mind would say, this is the way to run things. Of course, it’s going to lead to more inflation. But the government says we don’t have inflation. If you shop, you know that there’s inflation.’’

Global investors appear to be convinced that several more trillions worth of printed currencies will be flowing through the global pipeline in the years ahead. “It’s outrageous what they’re doing,” Jim Rogers, chairman of Rogers Holdings told CNBC television on Feb 8th. “The Federal Reserve is printing money as fast as they can, and the Bank of Japan says they’re going to print unlimited money. You know what the Federal Reserve said? ‘We’ll match you and we’ll print more money, too! “This is insane!” Regarding Fed chief Ben Bernanke, Rogers said, “He doesn’t understand economics, he doesn’t understand finance, he doesn’t understand currencies. All he understands is printing money,’” Rogers said.

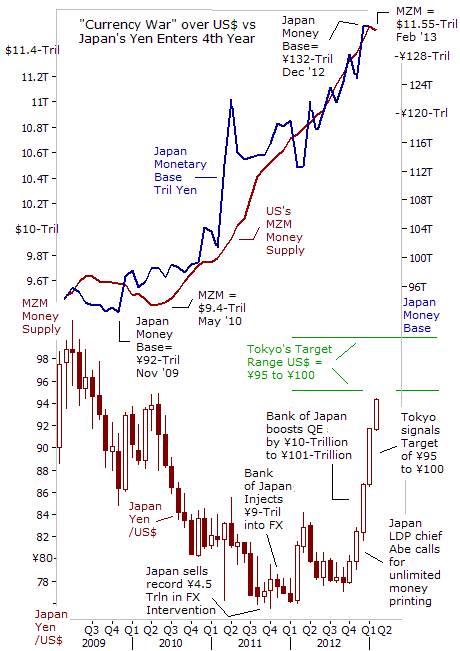

As the chart above shows, - the Bank of Japan (BoJ) and the Fed have been flying under the radar, - engaged in a “competitive currency devaluation,” since the middle of 2009. Both central banks have increased their local money supply, and used the freshly printed monies to purchase vast quantities of mortgage or government debt. For its part, the BoJ has increased the size of the monetary base in circulation to a record ¥132-trillion, - that’s up nearly +44% from ¥92-trillion three years earlier. Likewise, the Fed’s money printing spree has increased the size of the high octane MZM money supply by $2.15-trillion, or +23% since May of 2010, in a race to the Foggy Bottom with a “beggar thy neighbor” – “currency war.”

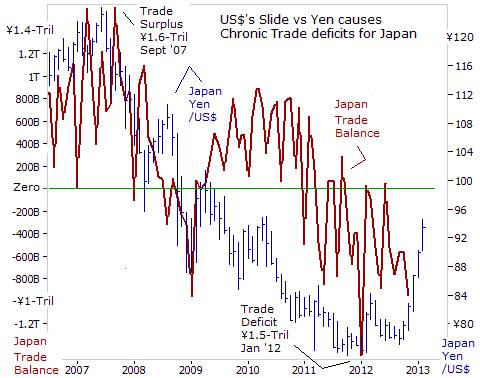

Until recently, Japan was losing the tug-of-war over the yen’s exchange rate versus the US-dollar. The sheer size of the Fed’s massive QE onslaught overpowered the BoJ’s counterattack. The US-greenback tumbled to a 15-year low of ¥76 in the second half of 2011. The BoJ was forced to step-up its intervention efforts on two occasions, when it injected ¥13.5-trillion of liquidity ($175-billion) in July and October of 2011 into the Tokyo currency market, its biggest intervention effort since 2004. Still, the BoJ’s herculean efforts couldn’t lift US-dollar above ¥82 for most of 2012. Largely as a result of the chronically weak US$ /yen exchange rate, Japan’s exports fell -5.8% last year, and the country logged a record annual trade deficit of ¥7-trillion ($78-billion) in 2012. It was second consecutive annual trade deficit recorded by Japan that for decades racked up hefty surpluses, helping to finance its ballooning debt.

Little more than 20-years ago, Japan’s economy was being held out as an exemplary model destined to become the wave of the future for global capitalism. Yet on Feb 14th, Tokyo announced that its economy, the third largest in the world after China and the US, had contracted for a third straight quarter. Japan has endured its fifth recession over the past 15-years, hobbled by the unrelenting strength of the Japanese yen, which undercuts its export opportunities and corporate earnings that are repatriated from overseas. Companies listed on the Nikkei-225 index said their net income had plunged -31% on average, in the July-to-September quarter compared with a year earlier.

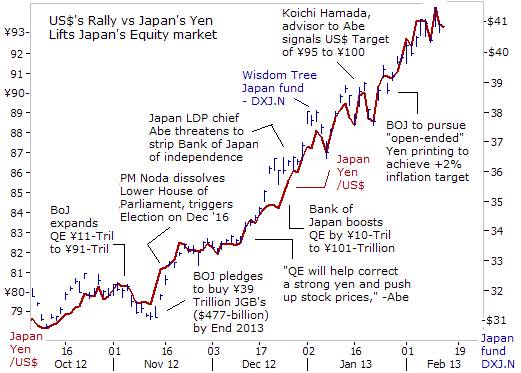

Former Prime Minister Noda acknowledged that the situation was “severe” and said the government would meet it with a “sense of crisis.” But his words only served to underscore the failure of successive governments to revive the Japanese economy since the collapse of the real estate and financial bubble at the beginning of the 1990’s. Noda announced he would dissolve the lower house of parliament on Nov 16th, triggering an election on December 16th that in turn, swept his Democratic Party of Japan from power.

Japan’s Liberal Democratic Party, (LDP) under the leadership of Shinzo Abe, reclaimed control of the government, and immediately began to exert maximum pressure on the BoJ to buy an “unlimited amount” of long-term government bonds (JGB’s), in order to weaken the yen, and thereby raise the cost of imported goods. The unlimited printing of yen would continue until Japan’s inflation rate rose to +2%. “We need to overcome the crisis that Japan is undergoing. We have promised to pull Japan out of deflation and correct a strong yen. The situation is severe. We need to do this. Quantitative easing by the BoJ will help to correct a too strong yen and it will push-up stock prices. That will help boost investment and lead to rises in wages, jobs and household revenues. We’d like to shorten the time needed for this to happen,” Abe said on Dec 16th. The Kyodo news agency said the LDP would draft an extra budget for 2012/13 worth up to 10-trillion yen and issue debt to pay for it.

A few days later, on Dec 20th, the BoJ agreed to expand its JGB-buying and lending program, by ¥10-trillion to ¥101-trillion ($1.1-trillion) by a unanimous vote, increasing its QE pipeline for the third time in the past four months. And even before the BoJ officially begins its Big-Bang QE counterattack sometime in April, Japan’s LDP chief has already managed to engineer a significant strengthening of the US$ to as high as 94-yen this week, simply through a bit of “Jawboning.” Koichi Hamada, a chief advisor to PM Shinzo Abe, helped to give the US$ a lift above the psychological barrier of ¥90 by saying on Jan 20th, “If the dollar goes above ¥110 there may be reason for worry, but at ¥100 yen or ¥95 yen, it’s OK,” he said.

As a result of a weaker yen across the board, - against the US-dollar, China’s yuan, the Korean won, and the Euro, Japan’s Nikkei-225 index turned in its strongest performance in seven years, surging more than +30% higher since Mr Noda’s government fell on Nov 16th. Likewise, Wisdom-Tree’s Japan Hedged Equity Fund (NYSEArca: DXJ) with its tilt towards Japanese exporters soared by $10 per share to as high as $41 this week. “The proof is in the pudding. Evidence is stronger than any talk,” LDP advisor Hamada remarked, citing the significant rally in the Nikkei-225 index as a result of a weaker yen.

Wisdom Tree’s fund, - DXJ is useful for US-investors, - it hedges its currency exposure to the Japanese yen by shorting yen futures and forward-contracts. It doesn’t necessarily carry a net short-yen exposure; rather, “the Index and the Fund seek to track the performance of equity securities in Japan that is attributable solely to stock prices without the effect of currency fluctuations.” On Nov 30th, DXJ started a new “revenue filter,” and removed companies that derive more than 80% of their revenues from Japan from the portfolio. For the top 10-holdings, 41% of their revenue is generated in Japan, down from 73% under the previous mix. Currently, the top-8 holdings in DXJ are (1) Mitsubishi UFJ Financial Group 5.8%, (2) Takeda Pharmaceutical 5%, (3) Canon 4.45%, (4) Honda Motor 4%, (5) Mitsui 3.4%, (6) Japan Tobacco 3.1%, (7) Nissan Motor 3%, and (8) Toyota Motor 3%.

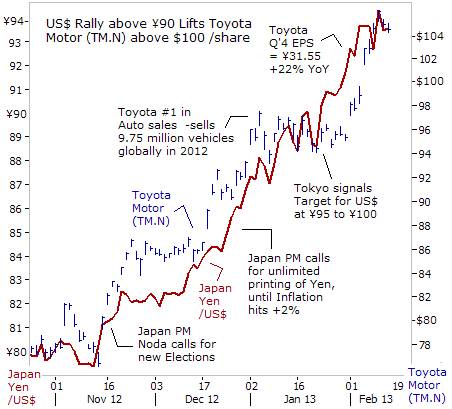

In New York, Toyota Motor (NYSE ticker: TM) has seen its stock price soar from roughly $77 in mid-November to around $105 in mid- February, its highest close in more than four years. The yen’s slide helps Japanese makers of cars and ships compete against their Korean rivals in markets such as Europe and the US. Also, Toyota’s annual operating profit increases by ¥35-billion for every 1-yen drop in the value against the US-dollar, according to the carmaker. At Toyota, the world’s biggest carmaker, net income for the quarter ended Dec 31st was ¥31.55 per share, up +22% from a year earlier. Even without the help of a weaker yen, Toyota recaptured its #1 sales crown from General Motors by selling 9.75-million vehicles globally in 2012, with impressive product lineups and marketing initiatives.

However, on January 30th, the French government began to complain loudly about Tokyo’s underhanded techniques to weaken the value of the yen. Not only did the Euro surge +26% higher to 127-yen, a 33-month high, but through the effects of cross currency trading, the Euro’s exchange rate versus the US$ also rose above $1.3500. That’s far above what some economists estimate to be the threshold of pain for French exporters at $1.2200. “The Euro is too high compared with what the European economy deserves,” said France’s Industry Minister Arnaud Montebourg. In response, the Group-of-7 clique of finance officials hastily crafted a communiqué, pledging to refrain from engaging in a currency war, responding to France’s allegations of the deliberate manipulation of the yen exchange rate.

G-7’s Phony Communiqué, “We, the G-7 finance ministers and central bank governors, reaffirm our longstanding commitment to market determined exchange rates and to consult close in regard to actions in foreign exchange markets. We reaffirm that our fiscal and monetary policies have been and will remain oriented towards meeting our respective domestic objectives using domestic instruments, and that we will not target exchange rates. We are agreed that excessive volatility and disorderly movements in exchange rates can have adverse implications for economic and financial stability,” the G-7 communiqué said.

If ten people read the same communiqué, each one may understand it differently. Perhaps, only one of them will interpret it correctly. As such, in the opinion of the Global Money Trends newsletter, the G-7 is skirting a fine line, - saying that outright buys and sells of currencies in the open market, and the use of “Jawboning” to influence foreign exchange rates is off limits. However, it’s permissible for central banks to print unlimited amounts of their respective currencies, if it’s used to monetize debt. Buying bonds is allowed, even though the scheme has the indirect effect of influencing foreign exchange rates.

Not surprisingly, Japanese Finance chief Taro Aso welcomed the communiqué, saying on Feb 12th that it recognized Tokyo’s threat to unleash Big-Bang QE, which could flood the world with as much as ¥100-trillion, - is not aimed at the foreign exchange markets. “It was meaningful for us that the G-7 properly recognizes that steps we are taking to beat deflation are not aimed at influencing currency markets,” Aso told reporters. The problem with this logic of course, is that the traders in the FX-markets view QE as the most lethal weapon in the central banks’ arsenal for influencing bond yields and currency exchange rates.

Russia Weighs in on Global Currency War, As tension over the Japanese yen’s exchange rates grows and G-7 central bankers try to head-off the outbreak of a full scale “currency war,” that could spread beyond the Tokyo and US-currency markets, - Alexei Moiseev, Russia’s Deputy Finance chief told the CNBC television network on Feb 14th, that the G-7, of which Russia is not a member, should not be making unilateral policy decisions or announcements on foreign exchange policies. “This kind of decision should have been discussed on the G-20 platform. This is G-20 week and the very reason that the focus in developing economic policy has shifted to the G-20 is that the G-7 no longer represents a sufficient proportion of the world’s financial markets and economies,” he said.

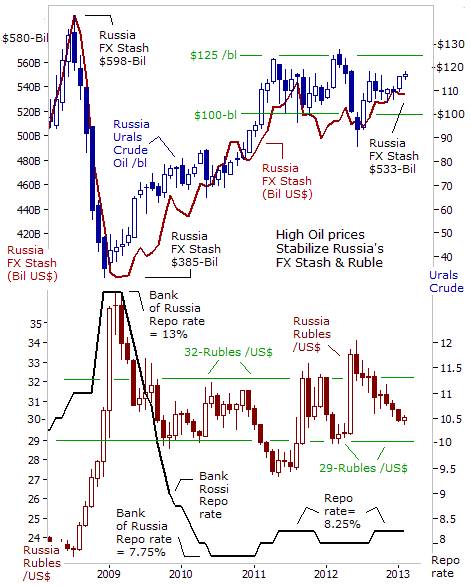

In regards to Moscow’s handling of the Russian rouble, Moiseev replied, “We are actively moving away from any manipulation of the currency. Last fall, the central bank officially declared that Russia is moving towards a flexible exchange rate so we have a target of 2015 to commit to make no interventions in the exchange market,” said Moiseev. On Feb 13th, Russia’s central bank (Bank Rossi) decided to hold its refinancing rate unchanged at 8.25% for the fifth month in a row, rebuffing a call by President Vladimir Putin to join the currency war bandwagon, by easing its monetary policy. The Russian economy is grappling with a +7.1% inflation rate, and Bank Rossi says its not in an enviable position to lower interest rates, until inflation cools off first. A stronger ruble has help contain the cost of imports.

However, the Kremlin shouldn’t be too upset if the BoJ and the Fed continue to print an extra $2-trillion of paper currency in the year ahead. Other central banks could join the currency war, including the People’s Bank of China, (PBoC), which on Feb 5th, injected 450-billion yuan ($72-billion) into the Shanghai money markets, its largest single-day injection ever conducted in the interbank market, in order to prevent the value of the Chinese yuan from rising against the US-dollar, and to artificially inflate Shanghai red-chips. As more central banks join the race to devalue their currencies, it could act to lift the price of Russia’s most important commodity.

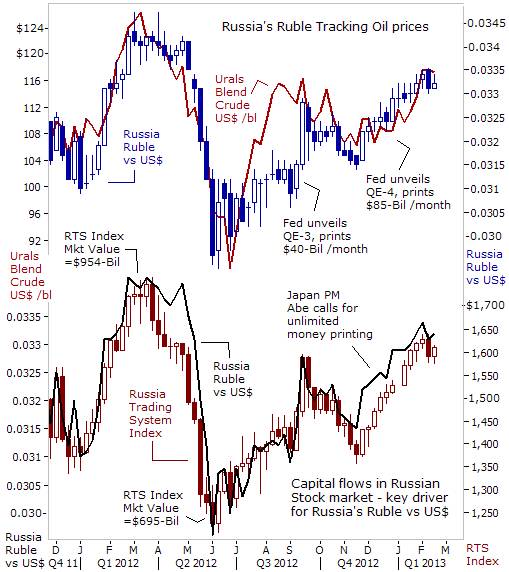

Moscow has high oil prices to thank for bolstering its stash of foreign currency reserves, reaching $533-billion this week, and in turn, high oil prices is supporting capital inflows into the Ruble and the local stock market. Two-thirds of the Russian Trading System (RTS) Index is made up of stocks in the energy sector, which are benefitting from high crude oil and natural gas prices around the globe (outside of the US). Exports of fuels and metals typically account for three-quarters of total Russian exports, and the natural gas and oil sector is responsible for as much as 60% of federal budget receipts. In order to fulfill its budget obligations in 2013, Moscow’s break-even point for Urals blend is around $117 per barrel.

Perhaps, Mr Putin’s most striking achievement is having fixed Russia’s fiscal mess. In contrast to persistent budget deficits in the 1990’s, and a default on its debts in 1998, Putin has taken advantage of bigger streams of revenues from crude oil and natural gas, to repay Russia’s external debt and built-up assets in a stabilization fund, which was recently used to inject fiscal stimulus into the local economy.As a result of budget surpluses and debt repayments, Russia’s public-debt-to-GDP ratio has declined to 6% of GDP, down sharply from 61% in the year 2000. But Russia’s budget balance is still heavily dependent on the oil price. Strip oil out and its public finances have been deteriorating since 2005.

Russia’s dependence on energy is greater today than in the mid-1990’s, when it represented less than half of exports. Russia’s output of crude oil climbed to 10.5-million barrels per day in November, a post-Soviet high. However, at current rates of production, Russia’s known oil reserves, including fields in the Arctic, could be depleted in just 20-years. Kazakhstan, by comparison, can sustain its current output for 60-years, Saudi Arabia for more than 70-years and the United Arab Emirates for more than 90-years.

For now, the fate of the Russian ruble is closely linked to the price of the Urals blend crude oil. Last year, the price of Urals blend suddenly plunged from $124 per barrel to as low as $90 per barrel. Likewise, Russia's ruble tumbled -15% to 2.9-US-cents, its lowest level since April 2009 as it tracked the falling price of crude oil. Russia’s stock markets also suffer when traders pull their money out of riskier, Emerging markets like Russia’s. Over a 3-month period, the RTS Index plunged by -30%, briefly wiping out $260-billion of market value. However, with the subsequent recovery of Ural crude oil to $117 per barrel, much of the ruble’s and the RTS index have been restored. The Fed’s QE-scheme and the effects of Tokyo’s “yen carry” trade are helping to fuel the recovery in the Russian financial markets.

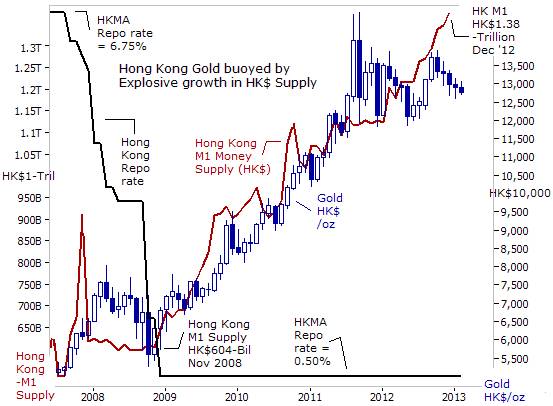

The Hong Kong Monetary Authority (HKMA) has intervened repeatedly in the currency market since October 20th, injecting a total of HK$107-billion, in order to defend an archaic and fixed currency peg with the US-dollar. Under the currency peg, the HKMA is obliged to intervene when the US- dollar hits HK$7.75 or HK$7.85 to keep the band intact. In reality, the HKMA can supply an unlimited amount of local notes for foreign currencies, albeit at the cost of higher consumer price inflation. Over the course of the past four years, the HKMA has more than doubled the size of the local M1 money supply, in a determined effort to counter the Fed’s QE onslaught. In turn, the increase in the M! money supply has helped to lift the price of Gold +125% higher to around HK$12,700 today.

Thanks to the peg, Hong Kong is forced to adopt the monetary policy of the US. The Fed’s policy of targeting the fed funds rate between zero-percent and 0.25% is matched by the HKMA targeting its overnight repo rate at an absurdly low 0.50%. As a result, the HKMA’s repo rate is pegged about -3% below the city’s inflation rate. Negative interest rates have encouraged traders to buy riskier assets, such as Gold or stocks listed in the Hang Seng Index. If the US$ peg were to disappear tomorrow, the HKMA could hike interest rates to combat inflation. Many analysts forecast that the Hong Kong dollar would appreciate by a minimum of +15%. In turn, the price of Gold and the Hang Seng could tumble sharply. This scenario is still several years away, but once the Chinese yuan becomes fully convertible, the ultimate endgame would be a Hong Kong dollar/yuan peg.

Looking forward, - the G-7’s call for a cease fire in the global currency war won’t take hold, if the BoJ and the Fed won’t agree to turn-off their printing presses. That’s not likely to happen anytime soon. The betting is that Tokyo’s Big-bang QE would contain sufficient firepower to push the US-dollar towards 100-yen and lift the Euro to 135-yen. Central banks in China and Hong Kong could respond by printing money, and other central banks, in Brazil and Korea might resort to various methods of capital controls, such as placing a stiff tax on foreign investment in their local bond and stock markets. There is simply no end in sight to the “Currency Wars,” as long as the BoJ and the Fed won’t stop monetizing debt.

When will the G-20 central banks finally agree to tighten the money spigots? Most likely, the End Game for the global “Currency War” will only arrive when the G-7 Bond Vigilantes are resurrected from the dead. It would take a significant decline in Treasury bond prices, and sharply higher bond yields, caused by the outbreak of hyper-inflation or record high crude oil prices, before central bankers are forced to recognize the folly of their dangerous game. In turn, sharply higher bond yields could be a catalyst for a synchronized global economic downturn, and the onset of a Bear market for equities. The Day of Reckoning is unknown, but it’s helpful to be on the lookout for the early warning signs.

This article is just the Tip of the Iceberg of what’s available in the Global Money Trends newsletter. Subscribe to the Global Money Trends newsletter, for insightful analysis and predictions of (1) top stock markets around the world, (2) Commodities such as crude oil, copper, gold, silver, and grains, (3) Foreign currencies (4) Libor interest rates and global bond markets (5) Central banker "Jawboning" and Intervention techniques that move markets.

By Gary Dorsch,

Editor, Global Money Trends newsletter

http://www.sirchartsalot.com

GMT filters important news and information into (1) bullet-point, easy to understand analysis, (2) featuring "Inter-Market Technical Analysis" that visually displays the dynamic inter-relationships between foreign currencies, commodities, interest rates and the stock markets from a dozen key countries around the world. Also included are (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, with the latest news on global markets, and view our updated model portfolio 2008. To order a subscription to Global Money Trends, click on the hyperlink below, http://www.sirchartsalot.com/newsletters.php or call toll free to order, Sunday thru Thursday, 8 am to 9 pm EST, and on Friday 8 am to 5 pm, at 866-553-1007. Outside the call 561-367-1007.

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab's Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR's and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, "Foreign Currency Trends" for Charles Schwab's Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

Copyright © 2005-2013 SirChartsAlot, Inc. All rights reserved.

Disclaimer: SirChartsAlot.com's analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources.

Gary Dorsch Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.