Australia’s Metal Miners hitch a Ride to China’s Economy

Commodities / Metals & Mining Jan 24, 2013 - 12:02 PM GMTBy: Gary_Dorsch

Navigating a metals mining company through the treacherous seas of the global economy is no easy task. There are many headwinds that can capsize a mining company or steer it far off course, if the captain of the ship doesn’t read the signals of the marketplace correctly. And it’s not only shareholders that can get hurt from calamitous decisions, but also CEO’s, such as Rio Tinto’s boss, who was sacked last week, because of a string of $34-billion of write downs, stemming from ill-timed and over priced acquisitions of aluminum and coal mines.

Navigating a metals mining company through the treacherous seas of the global economy is no easy task. There are many headwinds that can capsize a mining company or steer it far off course, if the captain of the ship doesn’t read the signals of the marketplace correctly. And it’s not only shareholders that can get hurt from calamitous decisions, but also CEO’s, such as Rio Tinto’s boss, who was sacked last week, because of a string of $34-billion of write downs, stemming from ill-timed and over priced acquisitions of aluminum and coal mines.

Miners must juggle many moving parts while trying to deliver new supplies of metals to the marketplace at a profit. The costs of mining are many, including those for energy, labor demands, decreasing grades of ore, stricter environmental regulations, and transporting natural resources to foreign buyers. That, along with increasing royalties paid to governments has the power to squeeze miners’ profit margins. In Australia, there’s a new 30% tax on iron ore and coal mine profits. In Indonesia, the government is telling miners that they must cede 50% of their ownership to the government. Peru is placing a new windfall tax on the resource sector that could raise about 3-billion soles ($1.1-billion) a year.

Recently, BHP Billiton scrapped a $20-billion plan to expand its Olympic Dam copper mine in South Australia and a new harbor, which would’ve doubled its iron ore exports in Western Australia. BHP blamed soaring development costs, a high Australian dollar and weaker metal prices for pulling the plug on the projects. Indeed, the selling prices of various commodities such as energy coal, iron ore, and copper, are not just set by the costs. Rather, they are set by the supply and demand of the marketplace, including the fickle nature of speculators, who buy and sell metals for quick profits, and can obscure the true level of industrial demand. Over-production causes prices to fall, sometimes below the cost of production. Heightened demand causes higher prices and eventual shortages.

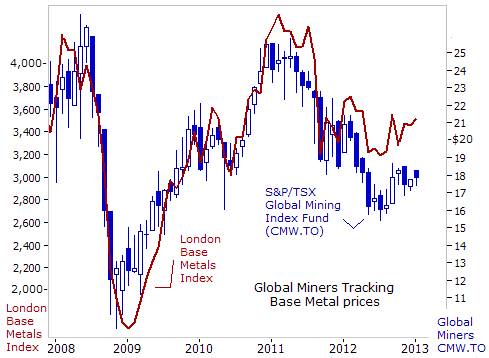

Following the two-year recovery in base metal prices in 2009-10, the world’s top-40 mining companies invested $98-billion in capital projects in 2011. They drew-up plans for a further $140-billion for 2012 in an effort to increase supply. But the unexpected plunge in base metal prices in the summer of 2011 caused many miners to nix those spending plans, against a backdrop of shareholder demands for heightened capital discipline. CEO’s of mining companies became even more cautious on capital spending, as the market price of the iShares S&P/TSX Global Mining Index Fund (Toronto ticker: CMW) lost more than a third of its value from the peak level at the start of 2011, before finding support at CD$16 /share.

The iShares Global Mining Index, traded in Toronto, has since stabilized from its nasty fall, and rebounded towards CD$18.50 per share, amid signs that China, - the world’s biggest buyer of base metals, sucking-up 40% of global supply, is experiencing an upturn in its economy, led by a rebound in its exports and industrial sector. Of all the variables that the CEO’s of mining companies must gauge, perhaps the most important is the outlook for China’s economy. That’s especially true for the big-3 miners of iron ore, - the key ingredient for making steel. In 2012, China produced 716-million tons of crude steel, or 46% of the world’s output. By 2015, Beijing aims to bring 60% of world’s output of steel under the control of its top 10 steel mills, while increasing its reliance on imports of iron ore from Australia’s miners.

China’s Economy – key Driver for Australia’s Miners

China’s economy grew at its slowest pace in 13-years in 2012. However, a year-end growth spurt, spearheaded by Beijing’s decision to spend 1-trillion yuan ($157-billion) on various infrastructure projects, lifted industrial output. Together with a surprising jump in exports, China ended Q’4 with a growth rate of +7.9-percent. Although the slowest since 1999, China’s economy was comfortably ahead of Beijing’s growth target of +7.5%, which just months ago seemed to be in jeopardy. Moreover, traders are optimistic that Beijing has the necessary tools and the know-how, to steer its economy away from a “hard landing” and can navigate the world’s #2 economy towards a healthy +8.5% growth rate in the year ahead.

If correct, Australia’s streak of exceedingly good fortune would extend for a 22nd year. Not since 1991, has Australia suffered through a recession, - defined as two straight quarters of economic contraction. Because of its recent “coupling” to the juggernaut Chinese economy, it’s been the only major industrialized country that was able to avoid the fallout from the “Great Recession” of 2008 that still haunts Europe to this very day, and badly wounded the US-economy. Today, Australia’s $1.37-trillion economy is ranked as the world’s 13th largest, despite being ranked 52nd in terms of population.

It used to be said that when the US-economy caught a cold, the rest of the world caught pneumonia. However, this is no longer the case. While it’s still the world’s biggest economy, the US-economy is not very important any longer for Australia. Instead, Australia’s fortunes have become increasingly linked to China’s. The view that Australia’s economy might actually have become “coupled” with China’s began to gain credibility in 2001. It was in that year that the Australian economy avoided the same fate as Europe, Japan, and the US, which fell into mild recessions, while Australia’s managed to squeak out a growth rate of +0.70-percent.

This was noteworthy because on the previous two occasions the US-economy had gone into recession, in the early 1980’s and the mild contraction after the Iraqi war in 1991, Australia’s economy was quick to follow. Empirical research has found that during the 18-year period ranging between Q’1 of 1983, and Q’1 of 2001, the correlation between the cyclical behavior of Australia’s economy and the US’s business cycle was extremely high at 82-percent. Since the turn of the century however, Australia’s economy became increasingly linked to China’s, and less in tune with cyclical swings in Japan and the Western world.

That became most apparent during the depths of the “Great Recession,” especially after the top-52 equity markets had lost a combined $ 30-trillion in market value from their peak levels in October 2007. The economies of Europe, Japan, and the US simultaneously plunged into severe downturns, yet Australia’s economy managed to escape the fallout, with just a minor scratch, - a single quarterly GDP loss of -0.7% in Q’4 of 2008. Yet even that loss in economic output was quickly recouped with a +0.8% gain in the subsequent Q’1 of 2009.

Even while unemployment in the 17 -countries that make up the Euro zone rose ratcheted-up to 11.8% in November, with the number of jobless workers hitting 18.8 million, and caused Germany’s economy to shrink by -0.50% in the fourth quarter of 2012, Australia’s economy didn’t skip a beat, expanding by an annualized +3.1%. Europe only buys 4% of Australia’s exports directly while China alone takes 26% of Australia’s exports. “I remain confident that Australia, with its strong government finances, resilient banking system, relatively low exposures to the troubled Euro-zone countries and strong links to the dynamic Asian region, is well placed to deal with events that may unfold,” said RBA deputy Governor Ric Battellino.

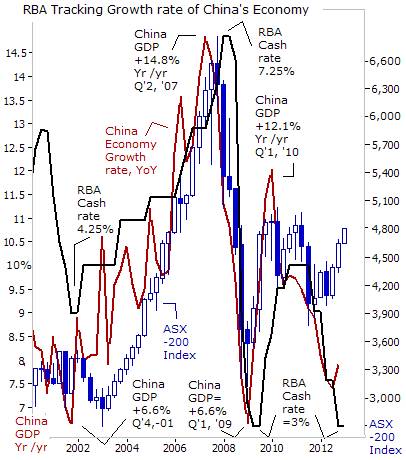

China’s $7.4-trillion economy was rocked by the severe fallout from the “Great Recession” in Europe, Japan, and the US. China’s economic growth rate has been quite volatile, ranging from as high as +14.8% to as low as +6.6% over the past dozen years, - growth rates that make politicians in recession ridden Europe and Japan quite envious. For the past 20-years, China’s economy has averaged +10% growth per year, roughly 3-times as fast as Australia’s has grown at an average annual rate of +3.6% for over 15-years. Highlighting the linkage between the two economies, the RBA has been emphasizing the growth rate of China’s economy, rather than its own economy, when setting its overnight cash lending rate.

China has also become the key driver for world commodity prices. In only 30-years, China would become the #1 consumer of copper, steel and iron ore in the world - consuming more them than Japan and the US combined, as well as the #2 user of crude oil and energy, agricultural goods and other non food commodities, such as rubber and cotton. This in turn had huge impacts on commodity rich countries, such as Australia, Brazil, Russia, Canada, Middle Eastern oil rich countries and South Africa.

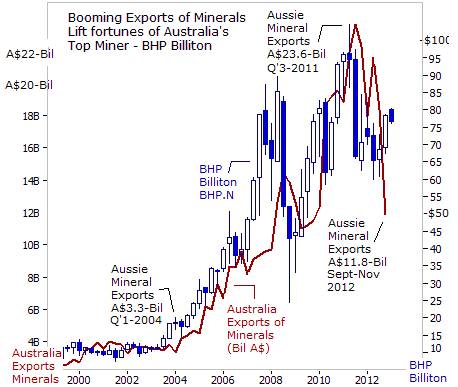

Mining exports, especially to China, have propelled the growth, and now account for 20% of Australian GDP. Investments in mines and related infrastructure account for 8-percent. The country also has resource projects worth A$425 billion under way or planned as miners try to meet demand from the urbanizing masses of China and India. Therefore, investors in Australian mining companies, such as BHP Billiton (BHP.N) and Rio Tinto (RIO.N), must be able to juggle several moving parts at any given moment in time. Key variables such as China’s volatile economic growth rate, the value of the US-dollar versus key currencies, central banks’ monetary policies, and an awareness of the break-even points for global miners, are just a few of the hot potatoes that investors must learn to juggle correctly.

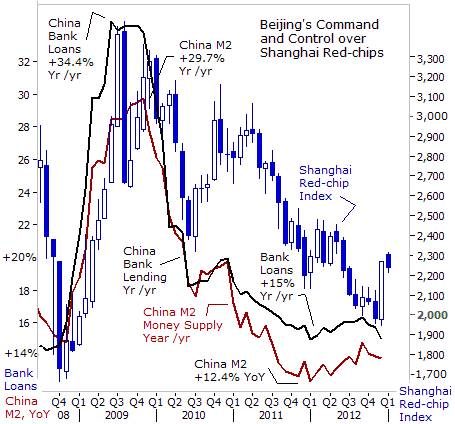

China’s “Command and Control” Economy, One of the defining characteristics of the Chinese economy is the centralized control that the ruling Politburo has over the key facets of the economy. Highly educated and skilled technocrats pull the various levers that can either accelerate or slow the growth rate of its juggernaut economy. For example, on Nov 9th, 2008, Beijing unveiled a massive 4-trillion yuan ($586-billion) spending program, earmarked for various infrastructure projects, – a vast sum equaling 16% of China’s total economic output, in order to reverse the sharp economic downturn, that had slowed its economic growth to just +6.6%, due to the fallout from the global banking crisis.

The People’s Bank of China's (PBoC), a key arm of the Politburo, flooded China’s capital markets with 1-trillion yuan ($146 billion) in excess liquidity. China’s banks were authorized to lend as much as 8-trillion yuan ($1.17-trillion) in new loans that year. As a result, the growth rate of Chinese bank lending exploded and was expanding at a +34% annualized rate. In turn, China’s broad M2 money supply had grown by +29.7% Beijing proved that its “command and control” strategy works. By Q’1 of 2010, China’s economy was growing at a +12.1% clip.

However, after a doubling of the value of the Shanghai red-chip market to the 3,300-level by Q’4 of 2009, aided by the explosive growth of Chinese banking lending and money supply growth, of +34% and +29.7% respectively, China’s economic planners began re-think their hyper stimulating policies. On Nov 18th, 2009, Fan Gang said the Chinese government would be reversing its policies, and would start aiming for a slower growth rate of +8%. Mr Gang emphasized that the PBoC would need to be alert to the danger of asset bubbles, and that managing inflation expectations would be a priority- code words for a tighter money policy.

Sure enough, the PBoC began clamping down on bank lending and reigning-in the growth of the money supply. During 2010 and the first half of 2011, the PBoC hiked the banks’ reserve requirement ratio (RRR) on 12 separate occasions, for a total of 600-basis points (bps). Each 50-bps increase in RRR’s drains about 300-billion yuan ($45-billion) from the banking system. As of June 2011, China’s bank RRR stood at an all-time high of 21.5%. In turn, by the start of 2012, the growth rate of China’s M2 money supply fell to +12.4%. In turn, Beijing whittled down the consumer inflation rate from a +6.5% in July ‘11 to +2% in Nov ’12.

China’s leaders were willing to pay the price of another epic drubbing in the Shanghai red-chip stock index, in order to rein-in the upward spiral of inflation, which if left unchecked, could lead to widespread social instability. The Shanghai red-chip index lost two-thirds of its market value from its 2009-high. Retail investors abandoned Chinese A-share stocks in droves - 50 million individual investors lost an average of 40,000-yuan last year, according to a People’s Daily report. That’s almost twice the annual average disposable income of an urban Chinese.

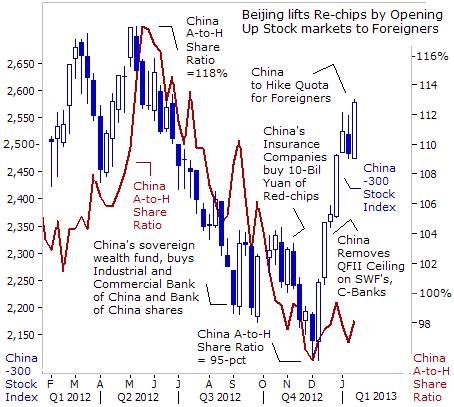

Highlighting the market’s deep state of despair, the China A-to-H share ratio, measuring prices of dually listed mainland companies (A-shares) compared to their H-share counterparts, listed in Hong Kong, fell to a discount of -2%, a stunning development. At the peak of the speculative frenzy in the Shanghai red-chip bubble in October of 2007, A-shares traded at a +80% premium to H-shares. However, with A-shares trading at a discount to H-shares, many traders who look for contrarian signals figured that the speculative froth had been completely knocked out of the Shanghai A-share market, and therefore primed for a rebound.

Chinese traders have become accustomed to gambling on PBoC policy moves, and were disappointed by Beijing’s refusal to pour more yuan into the Shanghai money market like it did during the 2008-09 global financial crisis. Chinese equities tend to react positively to massive liquidity injections by the central bank. However, many traders were caught off guard, when Beijing utilized a different tactic to jolt the Chinese stock market higher. In August, Beijing ordered the Central Huijin, - China’s sovereign wealth fund, to begin buying shares of Industrial and Commercial Bank of China (ICBC) and Bank of China, by 6.3-million shares and 18.8-million shares respectively, on the open market. In October, China's major insurance companies - China Life Insurance, Ping An Insurance, and PICC Property and Casualty followed suit by purchasing 50-billion yuan worth of red-chip company shares.

Then, on Dec 16th, Beijing “shocked the markets,” by inviting sovereign wealth funds and foreign central banks to invest in China’s bond and stock markets without limitation. On Jan 14th, the CSI-300 index, measuring the value of China’s top stocks traded in Shanghai and Shenzen surged sharply higher to the 2,600-level, following comments made by Guo Shuqing, chairman of China’s Securities Regulatory Commission, hinting he would allow foreign investment trusts to invest in China’s capital markets, beyond the current quota of $80-billion. “At the moment, money invested by foreigners in China’s stock and bond market accounts for 1.5% of the total. So we can increase the quota at least 10-times,” Guo said.

Thus, Beijing has engineered a +20% rebound in its local stock market since the start of December, by hinting at future moves to liberalize its markets, and open-up greater amounts of investment from foreign investors. Combined with news of a rebound in China’s GDP growth rate to +7.9%, Beijing has created the general impression in the media and the marketplace, that China’s economy is turning the corner, and poised to grow at a healthy +8% growth rate. In turn, base metal prices, and shares of global mining companies have also rebounded, with traders taking their cue from the gyrations in the Chinese stock markets.

Australia’s Metal Miners hitch a Ride with the Chinese Dragon,

Australia’s biggest mining boom since the gold rush of the 1860’s has led to a thriving economy, the country’s annual GDP (gross domestic product) growth rate has averaged +3.5% over the past few decades. However, industries outside of mining like tourism, retail and manufacturing are struggling mightily under the weight of a super-strong Aussie dollar. Beneath the surface, the floating currency, bolstered by trade with China, is widening a rift among Australia’s member states. Western Australia, the home of 10% of the country’s population, and most of its mining industry, is earning 60% of Australia’s foreign exchange. The other 90% of the country is saddled with an overly strong currency, and its exporters are running big trade deficits with the rest of the world.

Company earnings at the Australian Stock Exchange (ASX) also showcase the country’s two-tier economy. In 2011 for instance, BHP Billiton (BHP.N) the world’s largest mining company, posted a profit of $22-billion and Rio Tinto earned $15.5-billion. Together, the two mining giants earned more than half of the ASX-200’s profit total of $71.4-billion. Upon closer examination, the biggest money maker for BHP was its West Australian iron ore business, with a +122% gain in EBIT to $13.3-billion, at a profit margin of 65-percent. The next biggest earner was base metals, $6.8-billion, followed by petroleum, at $6.3-billion.

Likewise, Rio Tinto (RIO.N), the world’s #2 iron-ore miner by volume, which mines the majority of its ore in the Pilbara region of Australia and in Canada, posted record profits in 2011. Rio’s cash cow, - iron ore – accounts for 73% of its revenues, compared to a 40% contribution for #3 iron-ore miner BHP Billiton. Rio Tinto’s record cash flows of $27.4-billion from operations during 2011 allowed Rio’s Board of directors to pay $2.2-billion of dividends to its shareholders and arranged $5.5-billion of share buy-backs.

The value of Australia’s exports of commodities, including metals, natural gas, and wheat, soared to a record high of $175-billion, in the 12-months ending June 2011. The mining sector alone accounted for roughly 60% of the country’s total exports of goods, reaching a record high of A$23.6-billion in Q’3 of 2011. This bonanza of extra income led to a virtuous cycle of good fortune of higher profits, wages, and employment and fueled massive investment in the development of new mines. However, it came as a rude shock to Australia’s top metal miners, when the price of iron-ore, suddenly plunged below $100 /ton in Sept ’12, to a 3-year low. Mineral exports dropped in half during the Sept-Nov ’12 period, and that rattled the share prices of BHP.N, RIO.N, and other iron-ore miners, such as Brazil’s Vale.

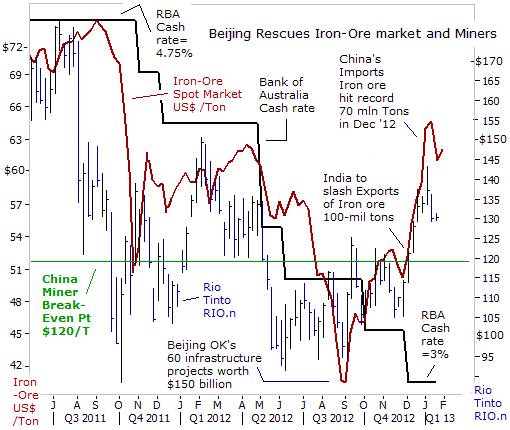

Beijing Rescues Iron Ore Miners, - The speed and scale of the slide in iron-ore prices came as a rude shock for Australia’s miners as they had thought there was a solid floor beneath the market in the $110 to $120 range because below that level, many Chinese miners of iron-ore become flat out unprofitable. Since Australia’s iron ore export earnings are running at over A$60-billion a year, a sustained decline below $100 /ton, would’ve led to a significant drop to export revenues of at least A$20-billion annually. In particular, Rio Tinto supplies 350-tons, or nearly a third of the world trade in iron ore, and would’ve taken the biggest hit.

It’s estimated that roughly 40% of Chinese miners become unprofitable when the price of iron-ore falls below $100 /ton. Chinese miners simply cannot compete on price with the top exporters in Brazil, Australia, and South Africa. The iron content of Chinese ore currently stands at only 20%, down significantly from 30% in 2004 and is well below the benchmark 58% and 62% ore from the likes of Rio Tinto, Vale, and BHP Billiton. Rio says its cost of producing iron ore is just $30 per ton, and $47 /ton, including royalties, the cost of shipping to China, and covering capital expenses. Australia’s #3 miner, - the Fortescue Metals Group FMG.AX has a break-even cost of around, $79 per ton. Thus, if iron-ore stayed below $100 /ton for a considerable period of time, RIO BHP.N, and FMG.AX could stay profitable, while more than half of China’s miners would spiral towards the brink of bankruptcy.

However, reminiscent of Q’4 of 2008, Beijing decided to stop the slide in iron ore prices on Sept 7th, ’12 and rescue its beleaguered miners. China engineered a V-shaped recovery for iron-ore prices, when it unveiled a plan to spend $150-billion on sixty different infrastructure projects. Share prices of Rio Tinto were quick to react, initially rebounding from $43 /share to $54 per share, and after a pullback, there was a secondary rally to $60.50 /share. Likewise, the spot price of iron ore rebounded above $120 /ton, the average break-even point for China’s miners. On Nov 12th, China’s powerful State Reserves Bureau (SRB) also said it would resume purchases of base metals such as copper, aluminum, and zinc, three years after the end of a buying spree that helped prop-up metal miners during the financial crisis of 2008-09.

But there was also an extraordinary stroke of good luck for Australia’s metal miners. On Nov 28th, the government of India said it would fully halt the production of its iron-ore mines, after a government-backed inquiry found that India’s iron-ore miners were operating illegally, and didn’t have the basic environmental permits to operate. The closure of India’s iron-ore mines is expected to reduce global supply by 100-million tons this year, costing India $15-billion in export earnings. The big-3 iron-ore miners Brazil’s Vale, (VALE) Rio Tinto, and BHP Billiton have already taken some of India’s market share in China, Japan and South Korea, and now are shipping the steel-making metal to India itself.

On Dec 4th, the Reserve Bank of Australia (RBA) lowered its cash lending rate -25-bps to a record low of 3%, stepping up its efforts to cushion the mining sector from the risk of a sharp slow down in China’s economy. Investment in mining projects was projected at A$109-billion for the year ended June ‘13, or nearly 8% of GDP, but that figure is now in doubt. The RBA’s easing campaign has been remarkable, lowering its cash rate 125-basis points since Oct ’11, and is now matching the trough hit during the darkest days of the global financial crisis. The RBA could lower its cash rate below 3%, in the event of a sharp slide in metal mining shares, or if the Aussie dollar becomes too strong, and approaches 100-yen.

Aussie Dollar – Yen Carry Trade, - Ultra-Rich in natural resources, Australia is perfectly situated as a key supplier of industrial commodities for Asia’s industrial powerhouses. Iron-ore, its biggest export earner, accounts for 28% of its total exports, followed by coking and thermal coal for 18% of exports, and crude oil and natural gas for 9-percent. Last year, Australia shipped 510-million tons of iron-ore abroad, earning A$63-billion. Coal is Australia’s second-largest export earner behind iron ore, worth about A$47-billion, with A$16-billion from exports of thermal coal used by power stations that generate electricity.

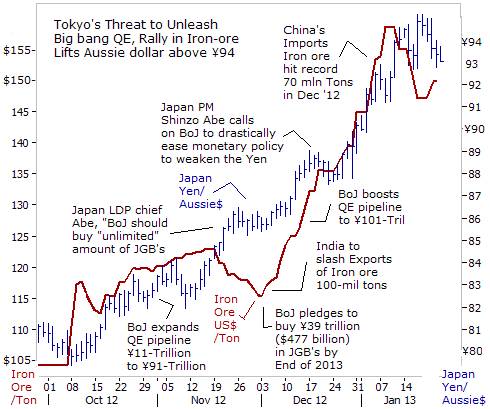

Japan is the second biggest buyer of Australia’s natural resources, behind China, with a 17% share of its Australian exports. For Japan’s steelmakers, the world's largest importers of coking coal, the cost of acquiring raw materials will become increasingly expensive. Today, Japanese importers must pay ¥94 to purchase 1-Aussie dollar, compared to just ¥80 at the start of October. The Bank of Japan is expected to flood the world money markets with $1-trillion worth of Japanese yen in the year ahead, (dubbed Big-Bang QE) which in turn, is fueling the Aussie Dollar – Japanese Yen Carry Trade. Simultaneously, the sharp rebound for iron-ore prices is giving a psychological boost to the Aussie dollar versus the yen, on ideas of an improving trade balance for Australia, albeit, mostly earned by the mining sector.

The future of Australia’s miners lies not in Europe, nor the US, nor Japan for that matter. Rather, mining looks to where its customers reside – in the rapidly growing China and the Emerging world. Even with the slowdown in China – from double digits to +7.4% growth – the IMF forecasts the Emerging world will expand at a +6% growth rate through 2016. One must not lose sight of the fact that the world’s population is rapidly increasing by a staggering 80-million persons each year, and this growth dynamic would drive greater demand for metals, and other commodities, regardless of swings in the business cycles.

Today, the world’s money markets are swamped with ultra-cheap liquidity. Traders turn a blind eye to negative macro-economic news. Markets are inflated by the hallucinogenic effects of “Quantitative Easing” (QE), Japanese yen carry trades, and global currency wars, - providing buoyancy that can lift many boats. Fueled by an expected rebound in China’s economy, a sustained rally in Asia’s stock markets, - and a full blown currency war between China, Japan, Korea, and the US’s Federal Reserve, - Australia’s metal miners are expected to hitch a ride to China’s centric Bullish bandwagon.

This article is just the Tip of the Iceberg of what’s available in the Global Money Trends newsletter. Subscribe to the Global Money Trends newsletter, for insightful analysis and predictions of (1) top stock markets around the world, (2) Commodities such as crude oil, copper, gold, silver, and grains, (3) Foreign currencies (4) Libor interest rates and global bond markets (5) Central banker "Jawboning" and Intervention techniques that move markets.By Gary Dorsch,

Editor, Global Money Trends newsletter

http://www.sirchartsalot.com

GMT filters important news and information into (1) bullet-point, easy to understand analysis, (2) featuring "Inter-Market Technical Analysis" that visually displays the dynamic inter-relationships between foreign currencies, commodities, interest rates and the stock markets from a dozen key countries around the world. Also included are (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, with the latest news on global markets, and view our updated model portfolio 2008. To order a subscription to Global Money Trends, click on the hyperlink below, http://www.sirchartsalot.com/newsletters.php or call toll free to order, Sunday thru Thursday, 8 am to 9 pm EST, and on Friday 8 am to 5 pm, at 866-553-1007. Outside the call 561-367-1007.

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab's Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR's and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, "Foreign Currency Trends" for Charles Schwab's Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

Copyright © 2005-2013 SirChartsAlot, Inc. All rights reserved.

Disclaimer: SirChartsAlot.com's analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources.

Gary Dorsch Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.