Ponzi Finance - Ponzi Wealth

Politics / Banksters Jan 06, 2013 - 12:42 PM GMTBy: Andrew_McKillop

WHAT GOES UP, GOES DOWN

WHAT GOES UP, GOES DOWN

Offically released on Jan 1, 2013 the Boston Consulting Group's "shock report" by Daniel Stelter and his colleagus on what 3 decades of Ponzi finance has done to real wealth in the developed-OECD group of countries has been available since mid-December but not widely commented. The title says it all: "Ending the Era of Ponzi Finance"

To be sure, equity and commodity markets kicked off Year 2013 with a traditional refusal and rejection of the real world - the financial markets need to drag in more hopefuls, more stupids and more greedies right up to the wire. That is their role and mission and has nothing to do with the economy, it is only a midsize but permanent Ponzi scheme. The BCG report describes what has become, in less than 30 years, a giant Ponzi scheme: the entire economic system of the developed world. It now has literally no choice but change. Real change has to come, not Ponzi-style loose change.

The BCG report details why the biggest threat of all has nothing to do with the world's balance sheet, but its income statement. It is now crushingly evident that we, in the debtor countries of the formerly wealthy world, do not have enough cash flow to cover either the principal or the interest. Our only hope is that the asset used to try paying down the ever-growing debt bubble - this "asset" is the entire economic system - can grow and will grow faster than the total debt financing cost.

THE RACE FOR GROWTH

This makes for only a few options, discussed in the BCG report but which we can summarize very easily. One basic option, if it was possible, is to rewind the economy to the 1960s when, the BCG report says, $1 invested in the US economy produced 59 cents in new GDP; at the start of the 2000s, still declining today, the 10-year average is about 18 cents. This can be called the productivity of investment and capital. Where the rest went is simple: to the Ponzi scheme of false wealth and totally certain losers "down the line", meaning all succeeding generations, saddled with unpayable debt.

The 1920-era Italian immigrant to the US named Carlo Ponzi created the scheme the world remembers, like the bigger and better scheme of Bernie Madoff which foundered in 2008. In both cases these criminals were engaged in a race for growth from Day 1 of their operating schemes. In neither case were the "underlying assets" of any real weight or cosequence, although the Madoff scam had a much more elaborate advertising prospectus and back up communication system. Basically of course, no productive investments were made by either of these renowned criminals: the final result was total loss. The incoming revenue paid off previous debt and financed short-run consumption, nothing else.

Economists use the term "Ponzi scheme" to describe a disastrous mechanism in which a financial operator assigns debt and pays off old debt by constantly taking on new debt. The repayment of the debt -- more recent loans plus interest -- is constantly pushed into the always increasingly distant future, fueling an endless process of debt refinancing. To be sure, if productive investments were made with the debt, these investments growing at least at the same rate as the increase of debt, the process could continue; if not, it can't.

The Ponzi-Madoff fake wealth scam has however, and dramatically, been switched from private citizens to the majority of governments - not only or especially OECD governments, but most starkly in the developed nation group. The financial operators running the scheme are the private banks. Banks in Europe, on the basis of broadly convergent data including analyses by the BIS entered 2012 with about 725 billion euros in combined debt. Altogether they received, in different ways, a total of about 280 billion from governments and the ECB in year 2012, but today at the start of 2013 have about 1000 billion euros of combined debt. How was this possible? In other words how did they "lose" around 280 bn euros in 2012?

In fact and showing how near the end of the Ponzi scheme we are, private banks in Europe are estimated to have received close to 280 bn euros only in the first 3 months of 2012. Whenever the private market is off-limits to them, they rely on the ECB to bail them out. The ECB is now lending them fresh money -- as much as they want -- at minimal interest rates. Otherwise, as their CEOs have repeatedly and unashamedly said to government leaders, they will close their doors and governments can sort out the chaos and panic.

The likelihood that the banks are able, let alone willing to repay recent loans, certainly those since 2008, at some unspecified date in the future often placed at "about 2030", is absurdly low. This in no way is the end of the story because Ponzi finance-Ponzi wealth is not only cancerous for banks - transforming them into organized crime syndicates - but parasitic and destructive of the real economy. Understanding why this is the case needs us only to backtrack to the subject of "productivity". Completely the opposite of anything that Ben Bernanke, Mario Draghi and their lookalikes feel obliged to say, economic system wide productivity is rapidly turning from bad to worse, year-in and year-out.

SORRY, THE FUTURE IS CANCELLED

Real productivity of investment capital, labour and land or natural resources is declining. Estimating the transition level for hedge financing and speculative financing morphing to outright and impossible to honor Ponzi financing at a rate of debt-to-income of 60%, the BCG report says this has happened to an increasing number of OECD governments: from 2000 and only concerning the EU27 and USA, the total of "Ponzi debt" relative to "payable debt" has spiraled to attain about $11 trillion for the US and $7.5 trillion for Europe at end 2012. Another way of looking at this estimate is to take those amounts as debt that can never, ever be repaid and should be "forgotten".

Ponzi schemes, when they founder as they always will, often throw up worse-than-anticipated numbers for the losses, and have longer-term negative spillover on investor sentiment and the optimism of economic deciders. For the government-and-bank Ponzi scheme of the developed nations, today, the BCG report states that actual and real, continually accruing but well-hidden debts of governments are increasing. Only "deleveraged" by a few governments and some private corporations (countries currently deleveraging include the US, Japan and Italy), the real level of government debt may be the double of the above figures. For the US and Europe therefore, the total of Ponzi debt could easily be $35 trillion, but we will never know.

The number of unknowns are as the BCG report says, large and increasing. One stark example concerns old age retirement pension funding. This future economic, social and political crisis is programmed and set in stone, and, when mixed with the poison of Ponzi finance as "the new normal" for financing practices, as much part of the New Economy as an iPad, sets heroic or perhaps impossible challenges for society. The report rightly says that "the welfare and pension crisis" in all developed countries, is deadly for the economy as we know it. Basically people live longer but retire earlier - and younger generations will have to work longer at lower net income, to pay off the debt taken on to pay current retirees. This sounds like it could or might be feasible - until we look at what has happened to younger employeds, we mean unemployed persons in the "mature democracies": they are among the first who are junked into the gutter of massive unemployment, with most OECD countries having at least 20% unemployment for their 16-25 year olds. In many countries the rate of youth unemployment is well above 33%. As a stark proof of total disinterest in the future, this one is hard to beat.

Significantly, of 8 developed countries analysed by the Bank for International Settlements (BIS), only three - Japan, Germany and Italy - did not show an almost certain strong, even massive growth of public debt to 2040, for the simplest of reasons: their population size is falling.

The problem of course is that today in 2013 it is "politically impossible" to further increase public debt. For private employers, starting with the largest employer companies in sectors such as the car industry, the simplest readout is to limit recruitment to the maximum, on a continuing basis, and encourage employees to quit work, if or when deals can be struck with labour unions, on one side, and government on the other to limit the costs of "voluntary" labour shedding and no new net job creation. Disguised unemployment and early retirement however only shift the debt burden back to the state, and guarantee that future economic growth will be weak or zero.

BACK TO BASICS

As well known and proven despite feeble rearguard action by some "Keynesian inspired" economists, increasing government debt beyond about 80%-85% of GDP always results in lower trend rates of economic growth. Debt strangles growth. This subject is usually and wilfully confused with what percentage of GDP passes through state or state-related entities, called Public Spending, and what amount stays private from start to finish. As shown by the wide variations (from 25% to 60% of GDP) of this spending in different countries, and their debt crises, this subject is not so important as the major problem - in fact crisis - of declining economic productivity and rising debt whether it is public or private, noting again that they 'morph' or 'transition' from one to the other.

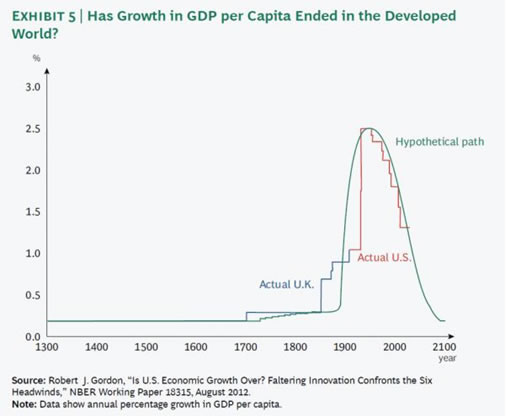

The BCG report is constrained to examine "what went wrong", and cites the work of economist Robert Gordon (Northwestern University, USA) who has repeatedly argued that starting as early as the 1950-1960 period, real economic growth and real wealth have trended downwards, for a large number of convergent reasons. As he puts it: the invention of indoor plumbing had an orders of magnitude more important and longer lasting positive economic impact than iPads, Twitter and Facebook. More easily measured and running diametrically opposite to the claims of Ben Bernanke, Mario Draghi and ther lookaliles the real economic productivity of capital, labour and resources has declined, especially since the 1980s.

The Ponzi answer is what we live, or survive every day: the inflation of selected asset classes or groups starting with housing. For private households in the straight majority of developed countries, today, the continued "appreciation" of their housing is taken as basic and certain. Inflating housing prices enables more private household debt to be taken on, perpetuating the scam. The perverse impacts as the BCG report points out, are economy-wide and include falling rates of interest and increasing resort to high risk and fragile Ponzi-style "investing", either operated directly by households, their banks and investment advisers or by the state.

The system-wide impacts are, to be sure, much larger and extend far beyond the proven and known decline in economic growth and economic productivity as debt continually rises, whether private or public, and always finally public. The end result is "sovereign default", which is known but is often treated as "only known in the history books".

Avoiding sovereign default is lengthily treated by the BCG report, which lays down 10 needed steps starting with an immediate reduction of the debt overhang by a mixture of writeoffs, restructuring, austerity, higher taxes, inflation, and raising employment. Most of these are political no-no items, which as the report says will almost certainly result in the continuation of what we have now: paralyzing uncertainty and refusal to act. Addressed by a political class or generation that prefers War and Circuses to Bread and Circuses, the sheer size of the economic breakdown threat is forcing them to act less irresponsibly.

The Boston Consulting Group report warns that now is the time to inform the public, and to act because social breakdown always follows economic breakdown. As former IMF chief economist Raghuram Rajan cited by the report puts it: "Ultimately a capitalist system that loses its public support loses any vestige of either democracy or free enterprise"

By Andrew McKillop

Contact: xtran9@gmail.com

Former chief policy analyst, Division A Policy, DG XVII Energy, European Commission. Andrew McKillop Biographic Highlights

Co-author 'The Doomsday Machine', Palgrave Macmillan USA, 2012

Andrew McKillop has more than 30 years experience in the energy, economic and finance domains. Trained at London UK’s University College, he has had specially long experience of energy policy, project administration and the development and financing of alternate energy. This included his role of in-house Expert on Policy and Programming at the DG XVII-Energy of the European Commission, Director of Information of the OAPEC technology transfer subsidiary, AREC and researcher for UN agencies including the ILO.

© 2012 Copyright Andrew McKillop - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisor.

Andrew McKillop Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.