Gold Recap 2012 and Outlook for 2013

Commodities / Gold and Silver 2013 Jan 02, 2013 - 08:01 AM GMTBy: GoldCore

• Introduction – Gold’s Gains In All Fiat Currencies in 2012

• Introduction – Gold’s Gains In All Fiat Currencies in 2012

• Much of Gold’s Gains in 2012 On 11% Price Gain in January 2012

• Japanese Yen Shows How Gold Protects From FX Devaluations

• Food Inflation Risk As Wheat and Soybeans Surge in Price

• Currency Wars and Competitive Currency Devaluations

• Gold Remains Historically and Academically Proven Safe Haven

• Conclusion – Gold in 2013

Happy New Year

Introduction – Gold’s Gains In All Fiat Currencies in 2012

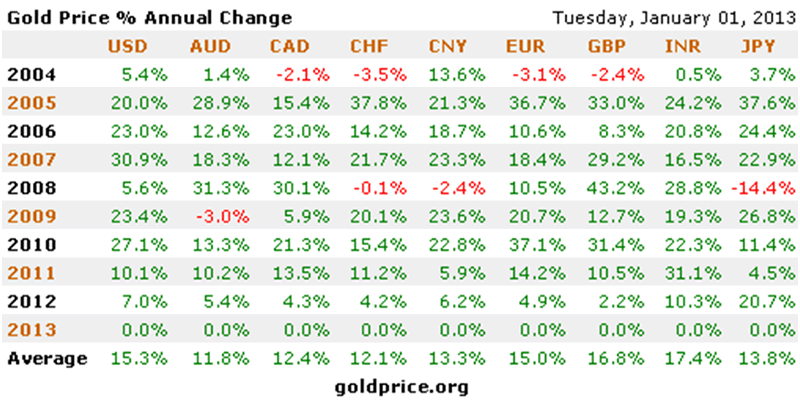

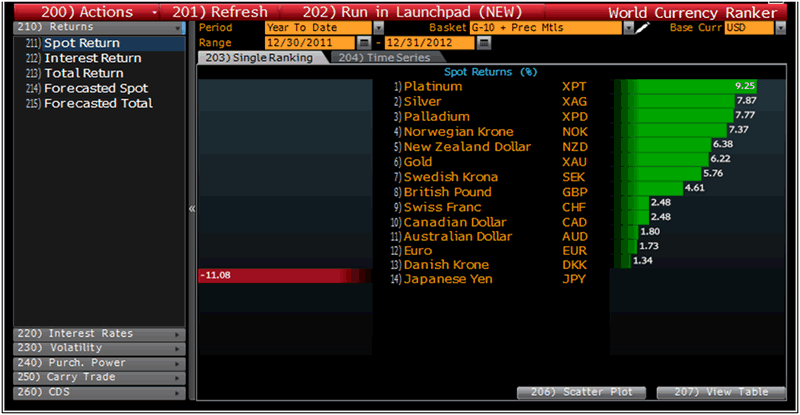

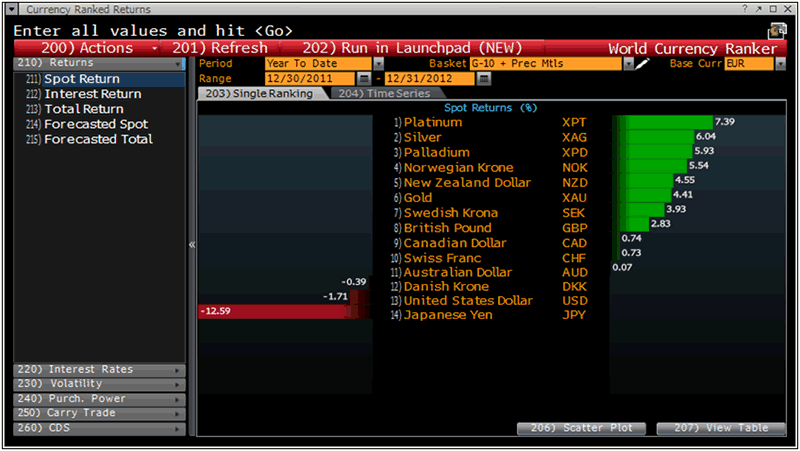

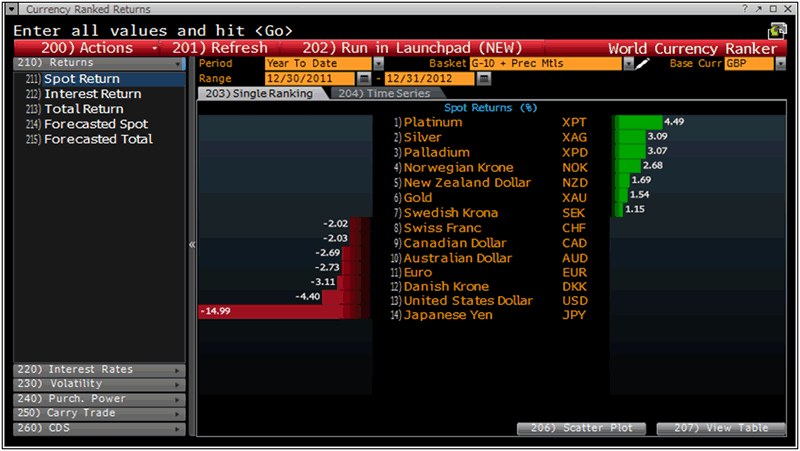

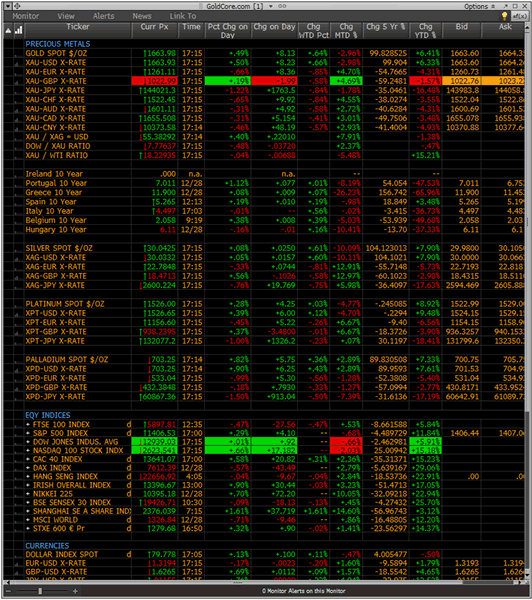

Gold saw gains against all fiat currencies again in 2012 (see charts and tables).

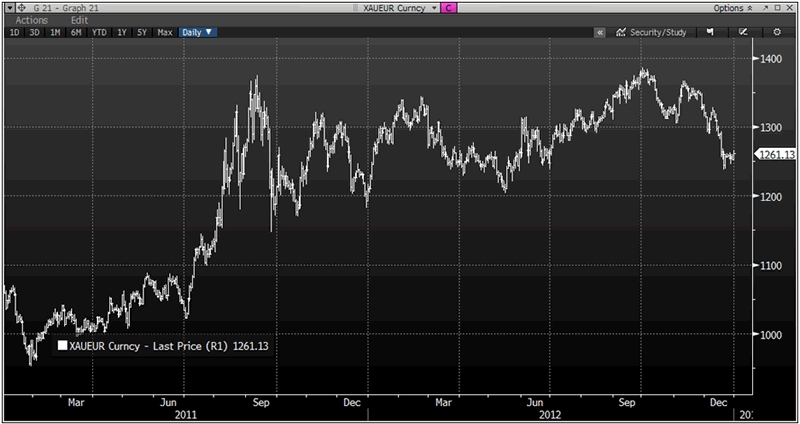

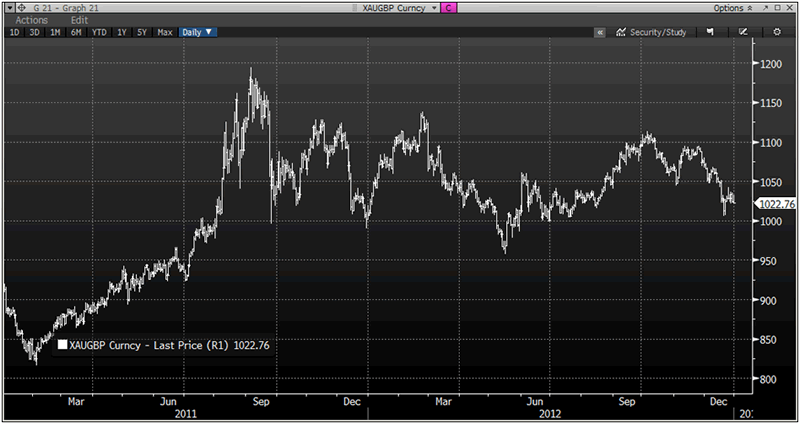

Gold rose 7% in US dollars and was 4.9% higher in euro terms and 2.2% higher in sterling terms or to put it more correctly the major fiat currencies fell these amounts in 2012 against immutable gold.

The gains were the smallest annual gains since 2008 but built on the steady gains of the last 12 years.

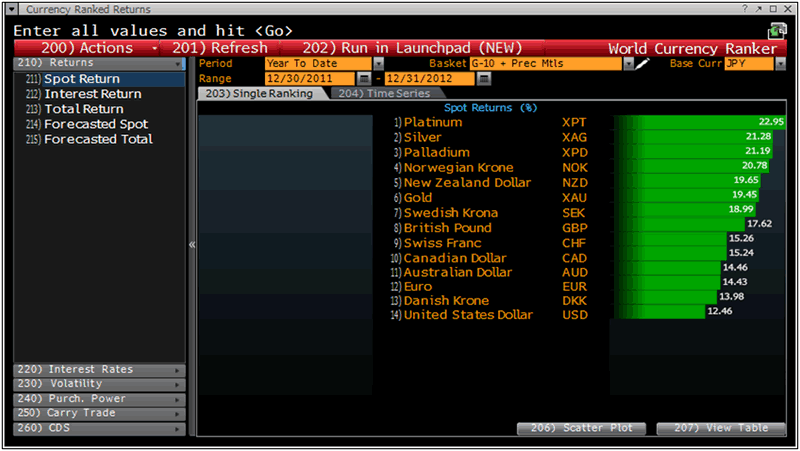

Silver also had a stellar year with all fiat currencies falling against silver in 2012. Silver was 8% higher in US dollar terms and 6.6% in euro terms, 3.9% in sterling pound terms and by 22.6% in Japanese yen terms.

Platinum and palladium also saw gains and returned 9% and 7.5% respectively.

Global shares rallied in 2012 with the help of central banks flooding the world with money and a tentative global economic recovery.

The MSCI All-Country World Index of equities increased 16.9%.

23 out of 24 benchmark indexes in advanced countries rose, with Greece, Germany and Denmark in the lead. Spain was the loser.

The UK's FTSE 100 rose 5.8%; Germany's Dax jumped 29.2%; France's CAC 40 added 15.2%; Italy's FTSE MIB gained 7.8% while Spain's IBEX 35 dipped 4.7%.

Much of Gold’s Gains in 2012 On 11% Price Gain in January 2012

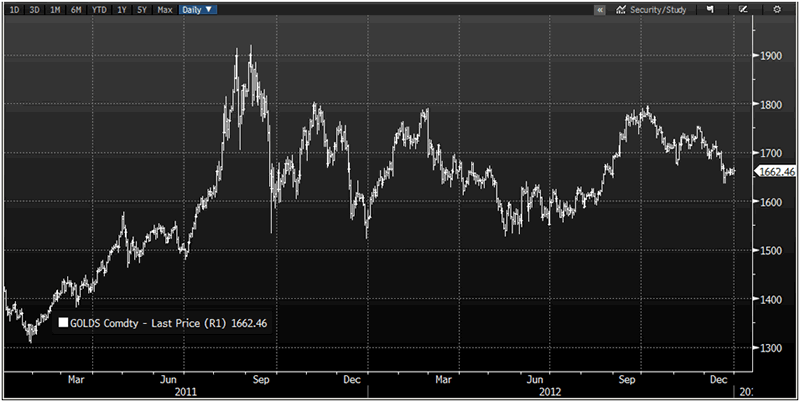

Gold fell in seven months of the year and rose in five (January and June to Sept). Interestingly, gold’s biggest monthly rise was in January when gold returned 11.1%.

Thus, speculative buyers not allocated to gold at the start of the year and attempting to time the market may have not enjoyed the gains of 2012.

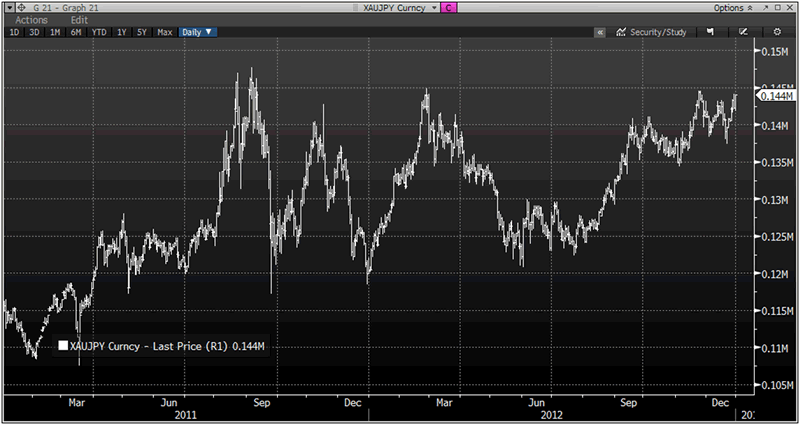

Japanese Yen Shows How Gold Protects From FX Devaluations

Gold’s importance as a safe haven asset and currency that protects against currency devaluations was again seen – especially in Japan.

Japanese investors and savers who owned gold had a return of 20.7% as the Japanese yen fell sharply on international markets. The ‘safe haven’ yen had already fallen 8.8% in 2011.

Sterling was one of the strongest fiat currencies in the world in 2012 – along with the Norwegian Krone and New Zealand Dollar – but it too fell against gold.

The appalling fiscal situation in the UK means that sterling could in 2013 see falls on a par with that seen in the yen in 2012.

The UK is one of the most indebted countries in the industrialised world - the national debt now stands at more than £1.1 trillion pounds (more than $1.7 trillion) and total debt to GDP in the UK remains over 500%.

The Japanese yen, as we saw, experienced marked weakness and was the weakest currency in the world in 2012 – as Japan speeds towards the 1 Quadrillion yen national debt mark early in 2013.

Food Inflation Risk As Wheat and Soybeans Surge in Price

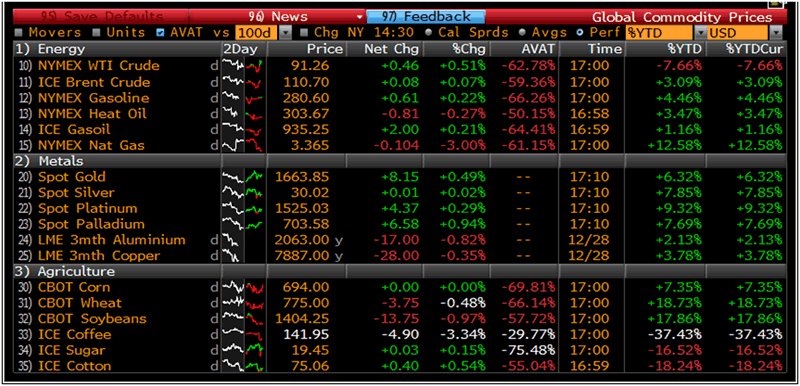

The Standard & Poor’s GSCI Total Return Index of 24 commodities rose 0.1% last year however the benchmark disguises some important trends that are important to keep an eye on.

Growing food inflation can clearly be seen in the 2012 food commodity returns.

A theme we have long written about is inflation in what is rare and in necessities such as food and energy, and deflation in non-essential discretionary items and luxury goods .

Essential foodstuffs used to feed the growing global population such as wheat, soybeans and corn rose quiet sharply in price – corn by 7.3%, soybeans by 18% and wheat by 19%.

While non essential food stuffs with little or no nutritional value and commodities more associated with our modern affluent societies such as coffee and sugar fell in price.

Oil was mixed with NYMEX crude down 7.6% while Brent rose 3%.

An indicator showing the very fragile nature of the recent global economic recovery is the Baltic dry index which was down nearly 60%. The gauge of dry-bulk shipping costs, averaged the lowest since 1986 last year, according to the Baltic Exchange, which publishes rates on 61 maritime routes.

Currency Wars and Competitive Currency Devaluations

While the risk in periphery European nations of reversion to their national currencies and currency devaluations have diminished – the risk remains.

The risk is not that the individual national governments will elect to take this route rather it could happen through contagion or a systemic event that leads to a domino effect jettisoning a member state, such as Greece, out of the monetary union.

t could also come about should German politicians decide that the European monetary project is not worth saving or they decide that it cannot be saved and elect to return to the Deutsche mark.

All significantly indebted nations, so called PIIGS and non PIIGS such as Japan, the UK and the U.S. are at risk of currency devaluations.

Competitive currency devaluations or the debasement of currencies for competitive advantage and currency wars poses real risks to the long term stability and prosperity of all democracies in the world and to the finances and savings of people in all countries.

Gold Remains An Historically and Academically Proven Safe Haven

It remains very important that investors and savers understand gold’s importance as a safe haven asset and form of financial insurance.

There remains a significant lack of understanding regarding gold and gold’s role as a diversification, a store of wealth and a wealth preservation asset.

Some continue to focus solely on gold’s price and not its value as a diversification for investors and savers. Many have been suggesting that gold is a bubble for a number of years and few have ever admitted how wrong they were with regard to predictions that gold prices would fall sharply.

The facts, the data and the charts that we present on a daily basis show that gold is not a bubble.

Whether gold is a bubble or not is not the fundamental question. What is far more important is that there is now a large body of academic and independent research showing gold is a safe haven asset.

Numerous academic studies have proved gold’s importance in investment and pension portfolios – for both enhancing returns but more importantly reducing risk.

Conclusion – Gold in 2013

Some market participants and non gold experts tend to focus on the daily fluctuations and “noise” of the market and not see the “big picture” major change in the fundamental supply and demand situation in the gold markets.

This is particularly due to investment demand from high net worth individuals, from hedge funds, from China, the rest of an increasingly wealthy Asia and of course creditor nation central banks.

Macroeconomic, systemic, geopolitical and monetary risks have abated somewhat but remain and could intensify rapidly in 2013.

The eurozone debt crisis is far from over and will become an issue again in the coming months as will debt crisis’ in Japan, the UK and the U.S.

Support for the price of gold should also come from the rising global money supply coupled with increasing investor and central bank purchases which have been driven by falling real interest rates and concerns about the euro, the dollar and other fiat currencies as stores of value.

Tighter monetary policies, as seen in the late 1970s, would likely help alleviate fears of further currency debasement but it is extremely unlikely that this will be seen in 2013.

Indeed, ultra loose monetary policies, negative real interest rates, debt monetization, competitive currency devaluations and global currency wars look set to continue – if not intensify.

Geopolitical risk remains very underestimated. Geopolitical tensions are particularly evident in the Middle East between Iran and Israel and many western powers.

There are also tensions between western powers and Russia and indeed China and these could intensify in 2013.

These macroeconomic, systemic, geopolitical and monetary risks are leading to increasing investment and store of value demand from the smart money such as Bill Gross, Jim Rogers, George Soros, Marc Faber and hedge fund managers such as David Einhorn and Kyle Bass.

Prudent pension funds and central banks will continue to diversify into gold.

Less informed people continue to call gold a bubble and not understand gold's importance as a safe haven asset and essential diversification.

The precious metals of gold and silver will again be essential diversifications for anyone wishing to protect and grow wealth in what will be a volatile 2013 and in the coming uncertain years.

Owning physical bullion will likely reward in 2013 and in the coming years as it has done in recent years.

For the latest news and commentary on financial markets and gold please follow us on Twitter.

GOLDNOMICS - CASH OR GOLD BULLION?

'GoldNomics' can be viewed by clicking on the image above or on our YouTube channel:

www.youtube.com/goldcorelimited

This update can be found on the GoldCore blog here.

Yours sincerely,

Mark O'Byrne

Exective Director

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information contained in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.