Themes for 2013 - Fiscal Cliff Follies, Gold Momentum, Economic Muddling Through

Stock-Markets / Financial Markets 2013 Dec 31, 2012 - 06:06 AM GMTBy: Andy_Sutton

With the hoax of the Mayan ‘End of the World’ fantasy and the week of extreme materialistic consumerism behind us, we can now return our focus to the events of the day and what might come to pass as we enter 2013. Certainly, there are several issues at the forefront right now, but many of the biggest issues are being buried. As we transition from 2012 to 2013, let’s take a look at what are likely to be the main themes of 2013.

With the hoax of the Mayan ‘End of the World’ fantasy and the week of extreme materialistic consumerism behind us, we can now return our focus to the events of the day and what might come to pass as we enter 2013. Certainly, there are several issues at the forefront right now, but many of the biggest issues are being buried. As we transition from 2012 to 2013, let’s take a look at what are likely to be the main themes of 2013.

1) The Fiscal Cliff Follies Show

Let’s get something straight right from the beginning; the whole idea of a fiscal cliff is a joke. It is a two-bit made-for-TV movie straight out of Hollywood. This country went over the real fiscal cliff decades ago when we blew our strategic advantages after World War II on ‘great society’ largesse. We capitulated totally in favor of greed and put into motion a sequence of events that sealed our doom before this writer was even born. For all intents and purposes the real cliff was breached when the US was taken off the gold standard because of excessive and continuous imbalances with regards to trade and the current account. The debt cycle began.

What we have today is a creation of considerable deliberation (which is intended to appear as ineptitude) designed to further erode our economic base, freedoms, and perpetuate the crisis into the next stage rather than end it. Bernanke and the rest of the MIT econ PhDs, Geithner and the rest of the globalist banking syndicate’s puppets, and most of the lynchpin leadership in Congress all understand that a solution is not possible given the rules they’ve imposed on themselves for the purposes of the debt ceiling / cliff negotiations.

Like it or not, America is following the precise trajectory of Europe, which is still in massive turmoil by the way. Just because the alphabet news networks stop covering a story doesn’t mean it has gone away. I realize that we are conditioned to place emphasis on whatever the media tells us to, but really, Europe is still in extremis. America is right on her heels. Sure, the acronyms of the programs and ‘fixes’ change, but the song remains the same: more debt to solve the problem of too much debt. The problem is that now it is easy to justify more debt to the masses saying that the economy will collapse if the government stops playing the part of the world’s biggest consumer. And sadly, that is quite true at this point. However, does that mean we should just continue blindly into the abyss? Many seem to think so, including quite a few states that see increases in estate taxes as a possible means to either expand their spending or at least stem the tide of red ink.

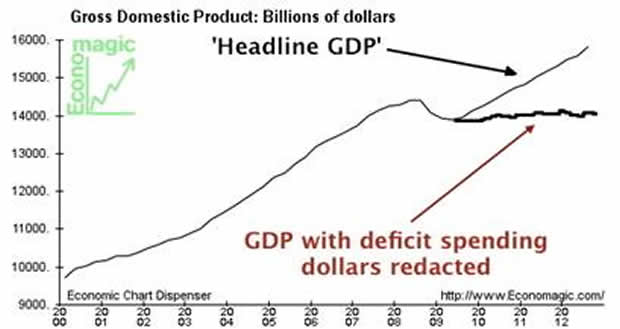

The bottom line is probably obvious to most; whatever comes of this round of the Fiscal Cliff Follies Show, it is by no means the end. There will be a sequel, and another, and another. Why? Because it is politically expedient. The ‘gimme gang’ has spoken much more loudly than the ‘don’t take it from me gang’. Another reason is the old adage that there is nothing more permanent than a temporary government program. The recent FOMC decision to peg interest rates to the headline unemployment rate is also interesting to say the least. It gives the Fed justification to further throttle the economy if another 2 million or so workers leave the workforce or if another million temporary, below subsistence level jobs are created, or some combination of the two. Look at it this way, the USEconomy is barely keeping its head above water now, despite massive deficit spending, ZIRP, and unprecedented monetization. What will happen when interest rates go up? Yes, there is a light at the end of the tunnel; and in this case it is a freight train.

2) Gold Gains Momentum as the Money of Choice

I will not posit that 2013 will be the year that the dollar loses its supremacy; that has already happened. Sure, it is still used in most global transactions, but that doesn’t confer supremacy status. Gold is the money of choice; it always has been and always will be. The syndicate certainly would love to have all the gold for itself, but despite a 12-year record of crushing traditional assets, precious few Americans have even bothered to pay attention. While it is difficult to ascertain the exact proportions of individuals who participate in the gold market, it is safe to state that it is likely less than 10%. Consider the anecdotal support for this statement. First, Americans have precious little savings as a group. Second, most of that savings is in pension plans and 401(k) type arrangements, which typically don’t allow the investor to have exposure to metals. A good case in point is the Thrift Savings Program that federal employees participate in. There are several fund options, none of which give the employee a chance to purchase precious metals, even in proxy form. Thirdly, virtually every individual, reader of this column, or client I have talked to that does buy precious metals reports that there are generally only sellers in the local coin shops around America. Buyers are few and far between, at least at the retail level. It is ridiculously easy to sell your family jewels and precious metals for cash and many Americans have chosen to avail themselves of this option to buy food, pay the mortgage or cover other expenses.

Keep in mind that the media will continue to bash gold (and silver) and JP/HSBC will continue to run up massive short positions to keep prices contained. Investors who understand these dynamics will continue to do what they’ve been doing and that is to take the metal away from the syndicate by taking possession instead of playing around with futures contracts and ETFs such as GLD and SLV, which are merely vehicles used by the syndicate for the purposes of price suppression.

Whether or not 2013 is the year we see $2,000 gold (or higher) is hard to say. I have never been big on providing timelines because most of the time they end up being inaccurate, as many analysts have already learned. There are too many variables and hidden agendas at work. There was a rather popular analyst who predicted the dollar would lose its reverse currency status last year. That didn’t happen – at least not in the manner this fellow described in countless videos, and now he’s lost quite a bit of credibility. But the idea itself that the dollar is toast is very valid. Stay away from specific timelines; in the grand scheme of things it really doesn’t matter if these things happen now or three years from now. The point is they WILL happen.

Many other countries are anticipating this eventuality as well. China, for instance, is re-casting many of its exchange-sized bars into smaller, 1kg bars, with the obvious benefit of creating fungibility for at least a partially gold-backed monetary system. This recasting also has the side benefit of allowing the Chinese to QC all of their gold holdings; don’t forget that one of the biggest stories never to appear on the evening news is the fact that there are a significant amount of counterfeit gold bars in existence. These bars are ‘salted’ with tungsten, so they measure out in terms of size and weight. Add to this that the Chinese and Russians have already hammered out the details of several trade deals whereby their respective currencies would be used for settlement as opposed to the USDollar. There are many other instances of this, however, with the Russians and the Chinese being the world’s two largest consumer groups, this agreement carries with it quite a bit of weight.

3) 2013: Another Year of Muddling Along

2013 is very likely to be another year of muddling along, from an economic perspective. Don’t expect a massive spurt of jobs creation; at least not the kind of jobs we need. GDP growth in ‘officialspeak’ will probably be around 2% to maybe 2.5% unless they really start cooking the books. Obviously this assumes that there is a deal to avert the sequestration aspect of federal spending that is due to be ordered come 1/2/2013 unless a backroom deal is concocted beforehand. Sequestration would require the furloughing of many federal employees considered to be non-essential. I wonder if the Congress falls into that group?

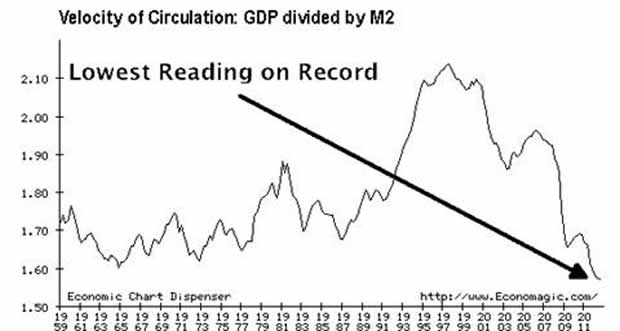

I’ve written many times before regarding the attack on aggregate demand that has been ongoing for the last half dozen years. It is not just apparent in the United States either, but appears to be a global reality. The policies that have created this environment will be continued in 2013. A bigger proportion of consumer spending will originate from new debt, and if our government wants to continue the spending binge, it is going to need to raise taxes or risk going into an overt monetization that would spell impending doom for the USDollar. Ironically, a bevy of new taxes are set to hit on 1/1/13 regardless of what happens with the Fiscal Cliff Follies Show, including an investment tax and a variety of obligations for employers in order to comply with the new (but not improved) socialized healthcare mandates. All of these things will be a drag on the real economy. Anything Congress comes up with in terms of new taxes (or expiration of current reduced tax rates) as a ‘solution’ to the current fiscal crisis will only exacerbate the drag on legitimate economic activity. This drag on the economy is evidenced by the velocity of circulation metric, which measures how fast money moves through the economy. Money is moving slower and slower and in fact M2 velocity of circulation has never been lower than it is currently; and the data series dates back to 1959.

However, despite all the negatives, there are many positives, the first being that there has never been a time, at least in recent history, when more people were seeking to become aware of what is going on. This is particularly true among the younger folks. I guess at least a few of them got the memo that they are on the hook for all of this and are taking it seriously. Awareness is bad news for the establishment and its plans, especially when people begin to realize that they in fact do have some say in what happens next economically. Since most folks are big on New Year’s resolutions, let’s resolve together to make a full frontal assault on the red ink on our personal and family balance sheets in 2013 and beyond. Right now it is cool to be in debt as long as we have all the right status symbols. Let’s make it cool not to be slaves to debt, but rather servants of liberty.

By Andy Sutton

http://www.my2centsonline.com

Andy Sutton holds a MBA with Honors in Economics from Moravian College and is a member of Omicron Delta Epsilon International Honor Society in Economics. His firm, Sutton & Associates, LLC currently provides financial planning services to a growing book of clients using a conservative approach aimed at accumulating high quality, income producing assets while providing protection against a falling dollar. For more information visit www.suttonfinance.net

Andy Sutton Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.