Why did Central Banks Stop Selling Gold?

Commodities / Gold and Silver 2012 Dec 06, 2012 - 01:59 PM GMT

In 2009 the signatories of the Central Bank gold Agreement effectively stopped selling gold. This was just after signing the third Central Bank Gold Agreement which lasts until September 26th 2014. Why?

In 2009 the signatories of the Central Bank gold Agreement effectively stopped selling gold. This was just after signing the third Central Bank Gold Agreement which lasts until September 26th 2014. Why?

In 1999, the first of such agreements was signed by the U.K. and was called the Washington Agreement. It received the tacit blessing of the U.S.A. and Japan. This was followed by the signing of the Central Bank Gold Agreement, which ran from 27th September 2004 to the 26th September 2009. Ostensibly to accommodate the I.M.F.'s sale of 403 tonnes of gold on their own books, a third Central Bank Gold Agreement was signed to run from the 27th September 2009 to the 26th September 2014. Apart from the up-to 7 tonnes year of gold sales by Germany's central bank for the minting of gold coins, there have been virtually no sales of gold from the original signatories of their gold. In fact the previously announced sales (going back to the turn of the century) have not been fulfilled completely, even now. Once the I.M.F. completed their sales of gold, the absence of the developed world's central banks from the sale side of gold spoke volumes! How?

Their absence from the gold market is not a non-event. It makes as strong a statement on policy decisions as either buying or selling gold. If I, as an investor, sold or bought gold, it would express my opinion on the future of the gold price. The same applies to my continuing to hold gold. The same is true of central banks. We look at the reasons why the fear of an overhang of central bank gold sales pushed the gold price down until 1999 and why the fear of developed world central bank gold sales has dissipated and added to by the emerging world's central banks buying gold. Generally now, few expect the developed world to sell any more gold from their reserves. Perhaps a look at the percentage content that gold takes in their reserves over the years will give us one aspect of the answer?

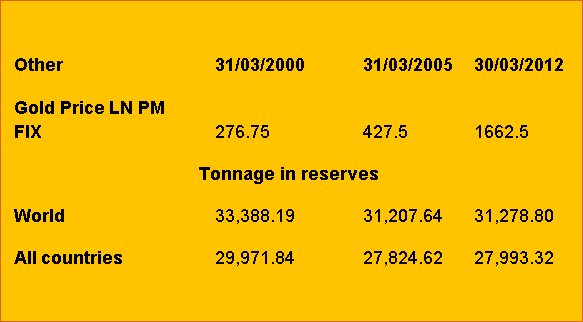

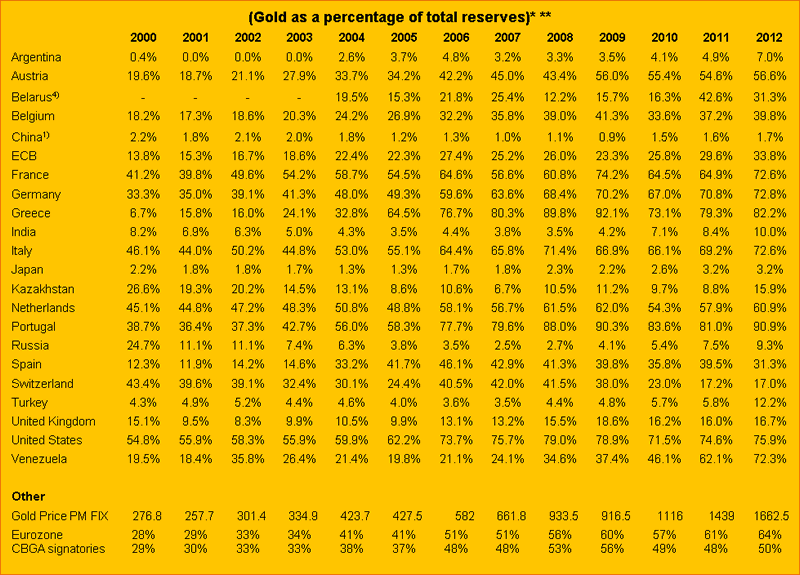

Table of % of reserves of central banks in 2000, 2005, 2012

This first Table highlights the amount of gold held by the world's leading central banks throughout the world then the amounts held by the nations. More importantly it gives the gold price in 2000, 2005 and 2012. In the year 2000 when the gold price was $275.75 the next table shows the percentage gold formed of total reserves. As you can see the amount of gold held officially has dropped since then by around 2,000 tonnes, but the percentage it forms of total gold reserves has soared to 75.9% in the case of the United States as you can see in the table above.

The very fact that the world's leading central banks have retained their gold (even though the leading ones sold some of their gold) confirms their statement embodied in the Central Bank Gold Agreement statements that, Gold remains an important reserve asset.

The leading central banks who sold up to 50% of their gold reserves are being reminded of it frequently. Those who sold 20% under these agreements regret it, but those who signed the agreement but never reduced their reserves by sales into the open market, such as Germany, are smiling on both sides of their faces. But even the more reckless sellers of gold such as the U.K. and Switzerland have watched what's left of their gold reserves multiply by six times as defined by the U.S. dollar.

We certainly believe that the well qualified gentlemen who populate central banks know full well that the value of gold goes far beyond its dollar price.

We are fully aware that despite not buying more the simple fact that the threat of selling gold, which was the overall case with central banks before this century began, has been replaced by the visible fact that developed world central banks are no longer willing to sell gold but want to keep a firm grip on it, while emerging world banks are buying as much as they can as it becomes available.

The conclusion of this position is that central banks have moved away from rejecting gold as part of the monetary system and now see it as a reserve asset that is needed in the present monetary system. If the monetary system continues on its current decaying path, then that need will grow. It is a short step from there to wanting more.

Gold as a Counter to Currencies

When asked why Germany did not take up its option to sell 600 tonnes of gold, under second Central Bank Gold Agreement, Axel Weber, the, then President of the Bundesbank said that "Gold is a useful counter to the swings of the Dollar." No other statement explained so precisely why gold must be held by central banks. He went on to say. "Gold is an important factor for the confidence in the stability of the €."

The future is full of change just as the past has been, so a pure currency experiment, even if it lasts for forty years without disaster, cannot be expected to replace gold long-term. The inaction of the signatories of the Central Bank Gold Agreement were fully aware of this when they persisted in including in the Agreements as Clause 1, the statement that: "Gold will remain an important element of global monetary reserves."

Europe has seen far too much devastating change in the last century to place absolute faith in a currency system that history has shown, all too often, fails under pressure. The U.S. has not had the same experience and has absolute faith in its power and the dominance of dollar hegemony. History shows that this is vulnerable and is headed for a fall. One only has to look at the threats to the U.S. dominance over O.P.E.C. and the oil price alongside the impending arrival of the Chinese Yuan on the global scene to see the dangers from outside. Inside, the state of U.S. debt and the battle over reducing the deficit shows that the dollar's days both as a measure of value and the sole global reserve currency are numbered.

The behavior of the developed world's central bankers, in retaining the gold they now have, amply demonstrates the realization that gold is the only asset in history that facilitates the passing though from one monetary system to the next. It does this through economic failure, wars and the like. What it boils down to is that trust, in nations and their systems, always fades away. Gold is inhuman and as a result is trusted to survive any such passing.

There's no need for the signatories to buy gold at the moment as the rising gold price is having the same impact as more purchases would have done if the price had remained static as the above tables amply demonstrate.

Controls versus Realities

Leaders throughout history have been impelled to impose controls on their people, "for their benefit". But at the same time they have to accept the harsh realities of their nation's existence. When the euro and the European Central Bank came into existence, the E.C.B. stated that it wanted to hold 15% of its reserves in gold. If they had held to that it would have required them to sell a great deal of the gold donated to them by member countries because the rising price of gold has defeated that objective as gold is now 33.8% of its reserves. For central banks to manage the financial security of their nations prudently, they have to take into account changing risks and realities. We believe that the signatories of the three agreements of the European Central Banks accept that the E.C.B. will not sell gold and change the present percentage. The rising gold price is most certainly acting as a "counter" to the decaying nature of the developed world's monetary system. That's why the signatories have such a tight grip on it.

One of the traps financial analysts and investors can fall into is to believe that arithmetical formulae dominate the relationships of the movements of markets, including the prices of precious metals. What makes any relationship between, say oil and gold, or silver and gold, or even the multiples shares and stocks trade at, is what investors see the future holds. Items like confidence and trust and investor perception set a pattern that in turn gives rise to these formulae. Formulae follow and don't lead markets. Consequently they are changing all the time. Take the multiples on the share in U.S. equity markets; they are still very high, telling us that investors have a high degree of trust in a U.S. growing in the future. If that belief in the future turns to a bleak one, then these multiples will fall and reflect that future. So what does the future hold?

Future Central Bank Actions in Gold

With emerging market central banks across the entire emerging world buying gold as it becomes available on top of other buyers in the market, the supply of gold at 4,000 tonnes or so (around 1,600 in scrap and the balance in newly-mined gold) is barely sufficient to give central banks what they want. It's likely that from January 1st 2013, we may see commercial bank demand enter the market gold market. Due to the implementation of Basel III happening from then through the next two years, the demand may come first from banks outside the U.S. before it comes directly from U.S. banks. They're all aware of this timetable and certainly won't want to be in the rush on the date it is active. So expect to see commercial banks enter the gold market in the near future. We imagine that they will buy in the same way as central banks do -waiting for the offer. But with such a heavy potential demand the supply will prove insufficient. The only way forward in such a market is to chase other demand away with higher prices, which we certainly expect.

But as we have seen since 2007, the main concern of governments is the health of the banking sector. This is placed much higher up the priority list than the citizen's interests. With the monetary system decaying steadily, there comes a point where action is needed to restore confidence in it both home and abroad. As we can see from the above, it's the central and commercial banker's confidence that's to be protected first so they can continue to operate like the main arteries and veins in the body.

To restore that confidence, expect to see gold become the domain of the central and commercial banks at some point in the future. When this happens, depends on pre-empting a collapse of confidence and is as such, is impossible to predict.

With banker's concerns foremost, the return of gold to a pivotal position in a world, that will move away from globalization soon, is certain. It's somewhere around that point that one after another, nations will call in their citizen's gold whether held at home or abroad through a Confiscation Order. While it will have a similar impact to the one in 1933, it will be for entirely different reasons. The only common denominator will be the clear confidence in gold at the time among bankers.

We know of only one twin structure that can prevent your gold from being so confiscated and it is Stockbridge Management alliance Ltd. Under the guardianship of the Ultimate Gold Trust S.A. based in Switzerland [www.stockbridgemgmt.com & www.ultimategoldtrust.com ] and the author does have an interest in SMA.

Apart from that it is most likely that citizen's gold will be confiscated both at home and abroad under pressure at home from your central bank. In 1933 these pressures came as potential massive fines from them.

Apart from that it is most likely that citizen's gold will be confiscated both at home and abroad under pressure at home from your central bank. In 1933 these pressures came as potential massive fines from them.

Gold Forecaster regularly covers all fundamental and Technical aspects of the gold price in the weekly newsletter. To subscribe, please visit www.GoldForecaster.com

![]()

By Julian D. W. Phillips

Gold-Authentic Money

Copyright 2012 Authentic Money. All Rights Reserved.

Julian Phillips - was receiving his qualifications to join the London Stock Exchange. He was already deeply immersed in the currency turmoil engulfing world in 1970 and the Institutional Gold Markets, and writing for magazines such as "Accountancy" and the "International Currency Review" He still writes for the ICR.

What is Gold-Authentic Money all about ? Our business is GOLD! Whether it be trends, charts, reports or other factors that have bearing on the price of gold, our aim is to enable you to understand and profit from the Gold Market.

Disclaimer - This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Gold-Authentic Money / Julian D. W. Phillips, have based this document on information obtained from sources it believes to be reliable but which it has not independently verified; Gold-Authentic Money / Julian D. W. Phillips make no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Gold-Authentic Money / Julian D. W. Phillips only and are subject to change without notice.

Julian DW Phillips Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.