Euro Crisis and Holland Mortgage Debt, Those Dutch Tulips Ain't Looking All That Rosy

Interest-Rates / Eurozone Debt Crisis Sep 12, 2012 - 12:18 PM GMTBy: Raul_I_Meijer

Well, the German Supreme Court decision is through, and it looks positive at a first superficial glance, so what could go wrong from here?

Well, the German Supreme Court decision is through, and it looks positive at a first superficial glance, so what could go wrong from here?

Sorry to break it to you, but plenty could. It’s amusing to see that decisions like these, the German court one or last week’s Draghi bond buying announcement, are seen as being positive for markets and/or entire economies, while in fact the only reason they have to be taken in the first place is that the situation is getting worse all the time.

If things were fine, Draghi wouldn't have to buy bonds, and the ESM wouldn't have to be propped up with measures that threaten to violate any constitution or sovereignty. Markets these days rise on bad news, because bad news makes politicians and central bankers hand out the people's money and checkbooks.

In the shadow of the ESM decision, European Commission President Manuel Barroso today, in his "State of the Union" speech, introduced a grand plan plan to hand the ECB what is basically total control over European banks, and move towards political union. As per today's Wall Street Journal:

Mr. Barroso said Europe needs a leap forward in the integration of member states to back up the common currency. He outlined the plans—launched Wednesday—for a single supervisor for all euro-zone banks that will allow some banks to gain access soon to emergency bailout funds.

The Commission asked legislators to adopt the proposal by year-end, a move that will face challenges from a European Parliament seeking to strengthen enforcement efforts and form a requirement that all EU states must unanimously agree the proposal. "We want to break the vicious link between sovereigns and their banks," Barroso said Wednesday.

The proposal gives the European Central Bank authority to issue and revoke banking licenses while ensuring banks comply with capital, leverage and liquidity requirements. The ECB would also be able to carry out early intervention measures when a bank breaches those requirements. [..] "We will need to move toward a federation of nation states. This is our political horizon. This is what must guide our work in the years to come..."

Of course the EU is already a federation of nation states. It's in the level of integration, in the details, where the devil resides. As I wrote recently, former Spanish PM Jose Maria Aznar said only last week that the drive for full fiscal and political union is "deeply misguided": "A United States of Europe is an impossible idea. It is a very serious mistake to try to destroy the nation states". Now Barroso may claim that you can still have a nation state after you have given up your fiscal, political and monetary powers, but that seems mere semantics. Granted, Barroso was shrewd enough cover his tracks:

He called for a clean break with how treaty changes have been pushed through in the past, saying they should win direct popular backing and not be pushed through with the "implicit consent" of citizens.

A good example of what this could lead to, and a solid indication of why Barroso's ideas will never ever be accepted by the people of Europe, can be found in the demands the Troika placed on Greece today. They want to fire 150.000 civil servants, raise the retirement age to 67 years immediately, cut "lay-off compensation" by 50%, and, wait for it, introduce a 6-day working week, and stretch the working day to 13 hours. In theory, that could lead to a 78-hour working week.

As my writing partner Nicole Foss remarked in true Monty Pythonesque Four Yorkshiremen spirit: "I wonder when we'll see the 8 day working week at 25 hours per day". Not surprisingly, the Greek government isn't thrilled at the demands; they can already see their heads end up on top of pointed sticks alongside the winding streets of Athens.

Want to take a guess at how many European countries will voluntarily sign up for similar treatment?

Another event in this packed day (besides the iPhone 5 launch) are the parliamentary elections in The Netherlands (a.k.a. Holland, and yes, I still carry the passport). I've been following campaigns in the past two weeks from the corner of my eye, and even there it's not pretty. There is absolutely nothing being said that reflects Dutch reality. There'll be another coalition government that will lead the country into another 2-3-4 years of delusion. Until either the infighting picks up again, or the real economic situation can no longer be denied. Whichever comes first. Hard to call that one.

And when the latter happens, the blow will be devastating: everyone will look to the government for salvation, but the government will face Troika demands like those presently forced upon Greece. For now, however, I bet you can't find a soul in the whole country who would think this is a realistic scenario. But really, just thinking and saying that you're rich doesn't make it so.

To understand how grave the Dutch plight may be, I’ll take a look at the household debt situation in Holland, mainly through a report issued last week by the government's own Central Bureau for Statistics (Centraal Bureau voor de Statistiek).

One thing to remember: in the election campaign, the only true household debt related issue that was discussed was mortgage interest deductibility, a longtime stalwart. Do they cut it entirely, do they keep it, or do they cut it very slowly? They can't agree. And still that is where the essence of the Dutch debt trouble lies: mortgage interest deductibility. Along with a majority of mortgages being interest only, so people pay interest, but no principal, and that interest is tax deductible to boot. In Holland you CAN have your cake and eat it.

Nor does the mess stop there: over 80% of mortgages are guaranteed by the Dutch government through the Nationale Hypotheek Garantie, the National Mortgage Guarantee. Which is where everyone looking to the government to save them will come in, as soon as house prices start falling for real. But at that point, as I said, the same Troika that now visits Athens may have moved to The Hague (in Holland the government does not reside in the capital, Amsterdam). I can already hear the derisive feel-rich Dutch reactions to my raising such options ...

One issue that is hardly ever addressed when it comes to such matters as the ESM is the one of those of the parties involved that are perceived as strong and rich. When the ESM, and bail-outs in general, are discussed, conversation circles around, on the one hand, the PIIGS countries' debts and needs, and on the other, the rich countries' willingness to pay for them. It's rare to see the rich countries' ability to pay questioned, it's all about willingness. Nice smoke screen, but not very convincing once you look behind the curtains.

As an introduction, I’ll start off with some quotes from an article that Ambrose Evans-Pritchard wrote back in April this year - the fact that it comes with a great EPA picture of far right leader Geert Wilders (the only politician to call for Holland to leave the eurozone) is a mere bonus:

Fitch doubts Dutch AAA as property slump reaches 'coma'

Fitch Ratings has issued the clearest warning to date that Holland faces losing its AAA rating if it fails to deliver austerity cuts or lets political conflict intrude on economic management. [..]

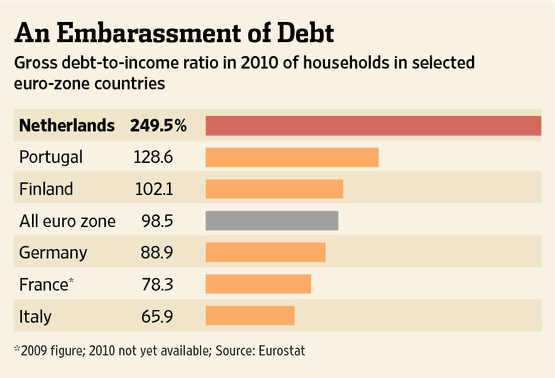

The warning comes as Dutch property tips into deeper slump, with the inventory of unsold homes nearing South European levels. Household debt is the eurozone’s highest at 249% of income, compared with 202% in Ireland, 149% in the UK, 124% in Spain, 90% in Germany, 78% in France and 66% in Italy - according to Eurostat data from 2010.

[..] home prices have fallen 11% from their peak in August 2008 [..]

The stock of unsold properties has doubled to 221,000 since 2008 as "Te Koop" signs proliferate on Dutch streets, almost double the declared level in the US on a per capita basis. [..]

Public debt will climb to 76% of GDP by 2015, according to the official Bureau for Economic Policy Analysis (CPB). [..]

The central bank said in its Financial Stability Report that the country faces a nasty mix of problems. "The outlook for financial stability in the Netherlands is worrying. Dutch households have almost the highest debt in the world. Declining real wages and rising unemployment are putting pressure on incomes. The steady fall in house prices is weakening their position while also increasing the likelihood of debt problems."

The report said credit outgrew the deposit base of lenders during the property bubble, leaving banks dependent on fickle capital markets. "Short-term funding may dry up overnight, as in 2008 when the interbank market stalled and again in the summer of 2011. A drop in house prices will compromise the issue of mortgage-covered bonds, while significant loan losses may lead to margin calls by the owners of such bonds," it said.

The regulator said Dutch pension funds are deeply underwater. They need €90bn in extra funding to meet future obligations, and $200bn to restore buffers.

Critics say Holland’s policy of full tax deductibility on mortgages as well as loan-to-value caps of 112% (with stamp tax) encouraged a debt spree along Anglo-Saxon lines.

To see where this places Holland internationally with regards to household debt, here's a WSJ graph:

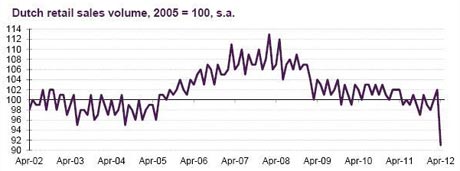

And by the way, there's more going on below the surface, as is evident in this graph from Lombard Street Research from a more recent (June 14) Ambrose article:

As if matters were not bad enough already in Euroland:

Dutch retail sales collapsed by 11pc in April, even worse than the 9.7pc drop in Spain. (Royal holidays cannot explain this).

As you can see from today’s chart by Lombard Street Research, it is a sight to behold.

OK, at last the Dutch Central Bureau for Statistics report that caught my attention last week, which is kind of based around a comparison between developments in Holland and Germany. Still, the bare Dutch numbers steal the show. A few snippets; the translation is mine.

Total long term Dutch household debt rose from 56% of GDP in 1995 to over 125% in 2011. More than 90% of this is mortgage debt. The rise in long term debt was faster than in France, Spain or the UK. In Germany, relative household debt even fell. Hence, while Germany had the same debt quota as Holland in 1995, in 2011, it had half that of Holland.

Along with mortgage debt, home prices in Holland rose at an explosive pace until the [2008] crisis. Around the turn of the century, they rose close to 20% annually.

From 1985-2007 average Dutch home prices went up 228%, while price inflation was 56%. In Belgium, Spain , Ireland , the UK and France they also rose more than threefold. In Germany, however, home prices fell. [..]

The relationship between home prices and mortgage debt is complex. Normally, newly closed mortgages rise along with home prices, but in other countries with rising home prices mortgage debt rose less fast than in Holland. Mortgage interest deductibility seems to have played a decisive role in this. [..] Germany offers far less fiscal advantage for home buyers.

Though mortgage interest deductibility stems from 1893, it was only in the 1990s that its benefits were fully employed through new mortgage constructions, like savings mortgages and investment mortgages, the essence of which is that only the interest is paid until the mortgage reaches maturity. Only then is the principal paid off. Until then households pay into a savings (investment account). Put together, these plans allow for lower monthly costs and higher purchase prices. This pushed home prices upward.

The fiscal attractiveness of high debt caused rising home prices to translate into extremely high mortgage debt levels. In other countries people did pay down the principal, because there was no drive to let debt remain as high as possible for as long as possible. [..]

The report goes on a bit more, but the gist is clear. You may not be overly surprised to learn that my initial reaction when reading it was: Wow wow wow!!. You see, my view is that this constitutes criminal behavior by a government and the banking industry it shares a pillow with. When you make it attractive for people to rack up as much debt as they can, there is only one possible outcome: some form or another of debt slavery.

It's very hard to get any closer to Charles Ponzi and Bernard Madoff than this, but at least those guys were not officially sanctioned by a government. The US subprime boondoggle has absolutely nothing on this; the only difference is that the Dutch real estate market has fallen just some 11% until now, not the 33% and counting in America. But it will, and then some; Charles Ponzi guarantees it on his mother's grave.

To top it off, the Statistics Bureau has the gall to state that total domestic real estate value has increased!. How does that work? Well, you hand everyone who wants it a truckload of free credit, they all buy their neighbor's homes, for which they don't have to pay down any principal, rinse and repeat as often as you can (get away with), and voilà!, everyone's richer. Easy as pie. I'm not joking: that is a pyramid scheme if I ever saw one.

And as I said before, none of this was hardly mentioned at all in the run-up to today's Dutch elections, though the government's very own statistics bureau published the numbers just last week. Truly incredible.

Yeah, I cracked some numbers too, it's probably good to get this into a US perspective.

The US has 314 million inhabitants, 18.8 times as many as Holland, which has 16.7 million (on a plot of land smaller than many if not most US states).

Holland's mortgage debt is €670 billion = $864.3 billion (at today's 1:1.29 rate), times that 18.8 would equal $15,712 trillion, while actual US debt is "only" $10.3 trillion. So Holland's mortgage debt is over 50% worse than America's. Which you thought was bad enough ...

That is €670 billion/16.7 million = €40.119 x 1.29 = $51,753 per capita. But only 54% of Dutch people are homeowners (vs 66% of US in 2011).

So 54% of 16.7 million = 9.1 million, carry the €670 billion = $864.3 billion debt, which comes to €73.626 ($94,977) per capita. For young families with 2 children, average(!) debt is €294.504 ($379,908).

And it gets worse: older people have obviously paid off much more on average, plus they have more savings on average. In other words, young families are sitting on highly explosive situations. Through less income, lay-offs, or other negatives, they can lose it all basically overnight (average income in Holland is €32.500 or $42,925).

Also, about those mortgage related savings and investment accounts: what do you think they are invested in? Not government bonds, at 1.x%, that’s for sure. Try risk. Try the stock market. Which rises only when more taxpayer money (including Dutch) is handed to the markets. Running to keep still doesn't do it justice.

With these levels of household debt it would seem obvious that the Dutch are sleepwalking into disaster, but don’t expect them to wake up anytime soon (or their politicians to warn them, apparently). After all, over 80% of mortgages are "insured", so why worry?

However, as is the primary characteristic of why any Ponzi scheme must and will collapse, this one too will run out of - enough - new entrants. And probably already has.

And this is a country that is supposed to pay tens of billions of euros to save its "poorer" cousins through the ESM, the EFSF and the ECB?! Come on!

As I said before, the "richer" countries in Europe need breathing space in order to save themselves. Because they're not nearly as rich as they like to think, and they like to make you think too. It would be far more realistic to let the weaker eurozone countries go, because not doing so risks imploding the entire edifice. And that in turn can and will lead to very ugly consequences.

Europe is a powderkeg in waiting. But don't tell the Dutch that. They like their delusions too much. Then again, don’t we all?

By Raul Ilargi Meijer

Website: http://theautomaticearth.com (provides unique analysis of economics, finance, politics and social dynamics in the context of Complexity Theory)

© 2012 Copyright Raul I Meijer - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.