Could Gold Be Tripped Up by Coming Deflation?

Commodities / Gold and Silver 2012 Aug 08, 2012 - 10:04 AM GMTBy: Jeff_Clark

Interview with Jim Puplava, by Jeff Clark, Casey Research

Interview with Jim Puplava, by Jeff Clark, Casey Research

Jim Puplava has robust convictions….

The CEO of Financial Sense News Hour, Jim is a man you should listen to carefully if gold factors in your portfolio or if you are thinking about adding gold anytime soon.

In this interview, Jim talks about how the dollar affects gold prices.

In this interview, Jim talks about how the dollar affects gold prices.

He discusses whether we are moving into a phase of deflation or inflation and gives his views on what exactly that will mean to gold investors.

He discusses the likely impact of inflationary or deflationary forces, which one he believes will win out, and the effect it will have on our economy.

Finally, he makes a very interesting prediction.

Of course, any investor will tell you that deflationists and inflationists have been arguing for years.

Each side has data to back up its claims, so investors end up none the wiser and non the wealthier. All the arguing simply causes confusion, and that invariably that leads to inaction.

One thing they can't argue about though: A defining moment in the deflation versus inflation argument will present itself when our current overburden of debt finally blows up.

On the one side, deflationists will point to periods in history where deflation resulted from that overburden.

But as always, there's more to the argument.

Jim emphatically states:

"The outcome depends on whether or not the economy is operating under a fiat currency system, because there's never been a deflationary depression when one's been in place."

Interesting.

When I saw this claim, I wanted to hear more, because deflationary forces seem strong at the moment.

I asked Jim for a chat about his viewpoint.

I wanted to get as clear as possible as I could about Jim's thoughts on deflationary pressures, because it has direct and significant implications for investments, including gold, something all my readers care deeply about.

Here's my candid interview with Jim.

Jeff Clark: For those who don't know you, Jim, tell us what you do.

Jim Puplava: Basically I head up three companies. We have our own independent broker-dealer; we have a money management firm and we have a media company which produces the Financial Sense News Hour online. I head up those three companies and am the CEO.

Jeff: It's been four years since the financial crisis, and we're still debating inflation vs. deflation. I found your claim quite compelling, so tell us what you found in your research.

Jim: Well, why don't we begin with the financial crisis that transpired between 2007 and 2009? It's something every investor remembers.

The deflationists would argue that in a crisis as big as that, the resulting downturn in the economy is always deflationary.

But if we look at that period, the money supply continued to expand. In my opinion, inflation is associated with monetary policy.

Jeff: We should probably define the terms we're using.

Jim: This is one of the problems we have when talking about deflation.

You will often hear, for example, that "housing prices fell by 30%" or the "stock market fell by 40%," supposedly meaning it was deflationary.

But that is a specious argument at best, because if we call the crash in real estate and the stock market deflation, then what would the deflationists argue now that housing is starting to turn around?

What would they call the S&P going from 666 to 1,373? It's up over 100%... is that deflation?

Let's take the popular definition of inflation – rising prices, which is really a symptom of inflation.

During the financial crisis, there were only three months where the CPI was negative.

Prior to 2008, the last time you saw a negative CPI was in 1954, when Eisenhower was president!

So despite all the claims about deflation, all you would have to do is look at a graph of M1 and M2 and see that the money supply actually expanded during this period.

Investors may not recall that in the middle of the 2007-2009 crisis, Bloomberg sued through the Freedom of Information Act and got access to the Fed’s records of exactly what they did.

We found out that they either guaranteed, expanded, or backstopped somewhere around $8 to $9 trillion. That can only be done in a fiat money system – something you can't do with a gold-backed system.

Jeff: Like during the Great Depression?

Jim: Even before that. Step back to 1920-1921… If you look at the statistics during that period of time when we were on an actual gold standard, you saw a huge contraction of GDP and in the price of goods.

Here are the actual numbers: between the summer of 1920 and 1921, nominal GDP fell by 23.9%; wholesale prices as measured by the PPI dropped by 40.8%; and the CPI fell by 8.3%. It lasted for roughly two years.

I have yet to see anything like this in Japan. I have yet to see anything like this in the United States – despite the credit crisis and all the fallout we've had.

Furthermore, even in the gold standard we had during the '20s and '30s, we had inflation.

President Roosevelt devalued the dollar by 60% in March of 1933, and when he repriced gold from $20 to $35, he stopped deflation dead in its tracks.

By the end of the month we were experiencing inflation.

We were running single-digit inflation rates the very month he did that in 1933, all the way up to 1937, when FDR and the Federal Reserve reversed course.

So as a result of the devaluation we got large doses of inflation.

Jeff: So your point is that even though we had a gold standard during the Great Depression, the government found a way to cause currency dilution, AKA inflation.

Jim: That's right.

Jeff: You brought up Japan; I assume you're using it as an example instead of the smaller countries because it's a major economy?

Jim: Yes, exactly. Even though the US dollar is the world's reserve currency, we have three major currencies where most trade is conducted – the dollar, euro, and Japanese yen.

Argentina's economy is insignificant in terms of global GDP, for example, and they're constantly printing money, so a lot of people don't like to refer to small countries like these.

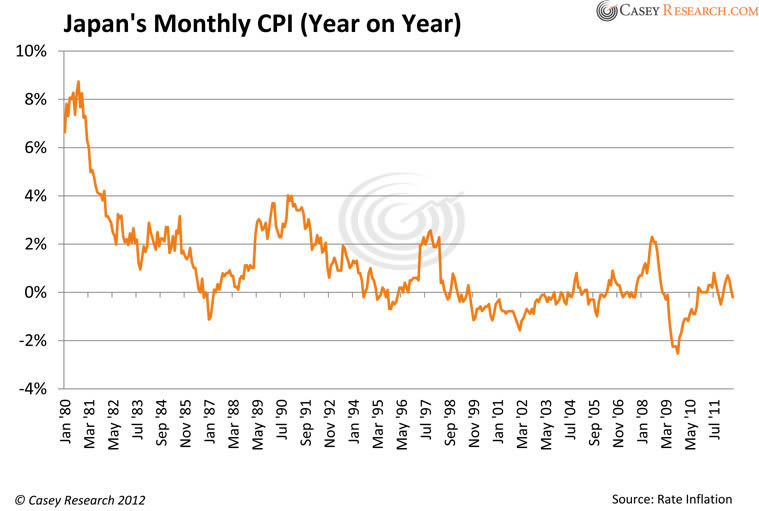

I'd like to address Japan, though, because of its unique situation. And I think a graph will best make the point. The following is Japan's CPI, year over year, going back to 1982.

There were brief periods of deflation, about 1% or 2%, and you can see that most of this occurred between 2000 and 2004 and in the credit crisis following 2009 to 2010.

In that period of falling prices, the CPI was only down 1-2%.

If we take a look at Japan's monetary base, however, there was only one period where it actually contracted, and that was between 2005 and 2010.

But the period that the deflationists like to talk about – 1989 going forward – Japan's monetary base expanded every year. Government spending expanded viscerally.

Jeff: And now their debt is among the highest in the world.

Jim: Japanese debt today is roughly 208% of GDP, one of the highest debt ratios in the developed world. But there's something else that makes Japan unique…

If a government expands its spending in order to rectify weakness in the economy, there are a couple ways governments can finance that. They can print money – which is what the Fed has been doing – or they can finance it through the bond market with existing savings. One of the very measures that allows Japan to escape a rather severe deflation compared to what we experienced in the early 1920s following World War I or in the '30s during the Great Depression was the Japanese savings rate. Going back to when the crisis began in Japan, the savings rate was 18%.

In other words, Japan has been able to finance its deficits internally. Ninety percent of their debt has been financed and held by domestic savings.

If the Fed or US politicians financed government spending with existing savings – in other words, took the savings of Americans and financed the deficit – that would not be inflationary.

Inflation comes when we get debt monetization, and fortunately for Japan, they were able to finance 90% of their debt expansion internally through domestic savings.

The second factor that contributes to what happened to Japan was the carry trade.

As a leading export nation, Japan exported a lot of its money to the rest of the world, and it gave rise to the carry trade, in which we were able to borrow in Japan at some of the lowest interest rates in the world.

So if Japan instituted capital controls, where the excess reserves of the monetary base were not allowed to leave the country, that money would have been confined within Japan itself, and then you would have had more money chasing fewer goods and services.

Jeff: What about Japan's demographics?

Jim: Yes, this is going to play very heavily on Japan.

As their population has aged, the savings rate has declined from 18% to roughly 2%.

If we look at total Japanese debt, 67% of that debt is rolling over in the next five years. More alarming is the fact that they have 900 trillion yen in sovereign debt outstanding, and the bulk of that is set to mature in the next two and a half years.

More importantly, the majority of this debt is now starting to be sold.

Japan's own citizens, as I've pointed out, own a large percentage of this sovereign debt.

For the first time in nine years, Japan's Government Pension Investment Fund, which is the world's largest pension fund, sold 443.2-billion of Japanese government bonds in its fiscal 2009-2010 year.

That was a result of rising benefit payouts to pension reserves requiring a liquidation of debt.

This is a major concern in our opinion for Japan, because as the Japan Investment Fund owns 12% of the country's outstanding domestic bonds, they are going to be selling an additional couple of hundred billion over the next two years.

So as Japan goes forward, there are only two things they can do to finance that debt.

One, they could go into the world bond market, though they could be subject to bond vigilantes where the interest rate spread could be high;

Or two, monetize it.

Because their debt to GDP ratio is 208% and still rising, the only way they're going to be able to keep interest rates down in that country is to monetize that debt in the same way our Fed is doing it through its monetary base and Operation Twist.

My point here, Jeff, is that the same demographics that will force inflation on Japan are the same demographics that are going to force inflation in the United States.

Jeff: Especially when you look at our unfunded liabilities…

Jim: Precisely. Lawrence Kotlikoff, author of The Clash of Generations and former senior economist on President Bush's Council of Economic Advisors, has a new book out, and he says US government liabilities are growing close to $11 trillion a year.

At the end of last year, it stood at $222 trillion. And by the way, these numbers come from the Treasury and CBO [Congressional Budget Office]. These aren't numbers I'm making up, so I rest my case with the deflationists. History has shown deflation can end overnight.

Jeff: So you're saying history shows that when debt blows up in a fiat currency system, inflation has always been the result.

Jim: Exactly. That's the case even in severe downturns. Look at what occurred in Japan between 1989 and 1991… their stock market lost 70% of its value and real estate prices fell 40-50%. Yet you would be hard pressed to find deflation of more than 1% or 2% for brief periods of time.

Jeff: Let me challenge you on a couple points. Some will point to the "lost decade" in Japan as deflationary and say that the government's stimulus efforts didn't work.

Jim: During the Lost Decade of 1990-1999, inflation rates in Japan were 3% to 4%. One of the few times where they allowed the monetary base to shrink significantly was the period between 2005 and 2009, and the result was 1% to 2% deflation.

Jeff: I can hear some deflationists say, "Gee, if the CPI only goes up 3% when debt blows up, I'll take that."

Jim: They'll take that, but if you look at the dire warnings deflationists give, we have seen nothing of that sort in any major economy.

Even in our economy, if we look at the credit crisis of 2007-2009, which had its origination here in the US, the monetary base didn't contract – it expanded.

What people have to understand is that when money is created, central banks can't control it. And what happens with that money is that it finds an outlet.

It has to go somewhere – it can go into housing, it can go into commodities, it can go into stocks.

The big warning the deflationists will give is that the world is going to collapse and that we're going to see a repeat of the Great Depression. I would challenge them to prove that, because if we're on a fiat currency, inflation has always been the result.

Jeff: Another challenge: we're in deflation now because the economy is going nowhere, stocks are going nowhere, even commodities are going nowhere…

Jim: This is one chapter in a long book that has to play out. What we've got right now is the private sector deleveraging and the public sector leveraging up, and these two forces are fighting against each other and the result right now is stagflation.

Jeff: How long does this stagflation continue?

Jim: I think this stagflationary economy continues for the next couple years.

Martin Armstrong, former head of Princeton Economics, also believes that will be the critical period when the fertilizer hits the fan.

Of course a lot can change and accelerate that – the outcome of the November elections, for example.

I've taken a look at the president's budget... According to the CBO, he will expand spending by $700 billion over the next four years, assuming he is reelected, and that's assuming his economic assumptions are correct.

In other words, we can raise taxes by half a trillion dollars and it doesn't impact the economy, even though the CBO and the Fed acknowledge this would subtract 4% from GDP.

So there are some wild cards out there that are unpredictable.

The results of the November election could favor a postponement, or we could get an acceleration of that time frame.

And let me make a prediction: Right now the world is focused on Europe, and we're seeing all the fallout from that.

I think the next crisis jumps from Europe to Japan, and then eventually from Japan to the United States.

Right now the US has the "best-looking house in a bad neighborhood."

A lot of gold investors have been disappointed with the price of gold or gold stocks, but they have no further to look than what's happened to the dollar.

The US has been a big beneficiary of the flight of capital escaping Europe, so we've seen commodity prices go down.

This fall in commodity prices has led to a lower CPI, and as a result we're also experiencing lower import prices, so the United States continues to be the beneficiary of the crisis.

We will continue to be a beneficiary of this, however, only as long as we maintain some form of credibility in the bond market, the idea being that the US will eventually get its own financial house in order and will bring its deficits under manageable conditions.

Jeff: Are you saying we won't have a negative CPI again?

Jim: I'm saying that if we did, it won't stay there long because we're operating under a fiat currency, giving the government essentially free rein to print as much money as it wants.

Jeff: If you're right, then when the crisis moves to Japan, commodities and the gold market, investments my readers particularly care about, could remain weak because investors would still go to Treasuries.

Jim: We're in a period of a rising dollar, and that dollar is competing directly against gold.

I also think it will depend on whether or not the US gets hit with the fiscal cliff in January and the economy weakens.

If that happens, I think the Fed could embark on another massive round of quantitative easing, which would change the picture for the gold market.

Right now, though, the Fed doesn't have to do anything.

One of the reasons I think gold investors got disappointed last fall is that the Fed didn't embark on quantitative easing.

Instead it announced Operation Twist, which was really not expanding the monetary base, and the result was interest rates came down from 2.5% to 1.5%. So it wasn't necessary for the Fed to do QE.

The market was doing the Fed's job for it.

Jeff: Is it your premise that this money finds its way into the economy and leads to inflation, meaning higher prices?

Jim: Absolutely. Our unfunded liabilities are simply too big.

I had to laugh when the president gave a speech last week talking about this tax on the wealthy, which was going to generate, according to the CBO, $65 billion in tax revenue. The government is spending $10.4 billion per day, so that revenue would basically run the government for a little over a week.

Jeff: The extent of our unfunded liabilities would imply much higher price inflation, which in turn would lead to much higher gold prices.

Jim: Absolutely. I'm very bullish on gold. I think we're just going through a long consolidation period. Right now gold is competing with falling commodity prices and a rising dollar.

Jeff: What's your view on silver in this context? In spite of it being a monetary metal, silver could stay flat in this stagflation since it has a lot of industrial uses.

Jim: I think silver can remain weak, but once again, that could change abruptly.

Let's say politicians don't resolve this fiscal cliff we're approaching and we get a fiasco like we did in August of 2011, where the Fed could change its policy and resort to another round of QE.

If you listen to the Bernanke's recent testimony on Capitol Hill, Senator Schumer from New York basically said:

"Look, Congress is in an election year, we're unlikely to resolve this. So get to work, Mr. Bernanke. You're the only game in town."

If Bernanke listened to him, then the Fed would have to take action, especially if we saw economic activity sharply decelerate or unemployment begin to spike.

Jeff: Another question I want to ask you. You've interviewed a lot of people over the years…

Jim: Probably in the thousands.

Jeff: Readers of BIG GOLD would be particularly interested to know, of all the people you've interviewed over, say, the past year, what have you heard that strikes you as particularly insightful or crucial that investors should be aware of?

Jim: I think if there's anything that I have learned in this market from the people I've interviewed and from our experience managing a gold portfolio, Jeff, is that you have to look at your portfolio in several tiers.

I have personally, as well as for clients, set up a core position in gold. That is never going to change.

It's there because I believe it's a store of value, as insurance against the unexpected.

Then we have what we call a trading portion of gold and silver.

Last year around late April early May, we trimmed our silver position in half and instituted a put on silver and gold, including our gold equities.

Because so much of the market today evolves around momentum trading and leveraged hedge funds, money moves in and out of a sector. It's like a hive of bees looking for a place to land. When they land on that sector – boom! –prices skyrocket like you've never seen.

And then all of a sudden that trade plays out, something changes, and the money moves out of the sector. The point is, we no longer live in a "buy and hold" world.

So the thing I would share with your readers is to keep your core position and know why you own it – it's there because it's a store of value, for insurance.

And if you want to increase that position over what you feel you're comfortable with, we recommend trading it.

Jeff: So I guess the question is, how long do we have to wait until the bees come back to the gold beehive?

Jim: Well, it could be this fall, or it could be another year.

A lot of your readers will remember this, but the gold price spent two years consolidating in the mid-1970s, falling from $200 to $100. So when I see the price of gold go up from $1,000 to $1,900, it's not unrealistic to expect there to be a period of consolidation as money goes elsewhere.

What I would suggest gold investors do if they're getting impatient is look at dividend yields.

There are many high-quality mining stocks today that you can buy at seven, eight, ten times earnings, something we never have seen in this bull market, and you can receive a dividend yield that is higher than a 30-year Treasury bond.

So while they're waiting patiently for this to unfold, they're getting compensated.

Jeff: It seems incongruous to bring this up in a weak market, of course, but do you see a likely future mania in the gold sector?

Jim: Oh, very much so. And let me throw out another couple predictions.

There are three phases to a bull market:

- The first phase is where the market starts to take off, and that's the smart money. They come in and drive it.

- The second phase of the bull market is where institutional money starts to come in and participate. I think that's where we were over the past couple years – just look at the plethora of new gold funds and resource funds. Then you get a corrective period, which is what we're going through now.

- Then the third phase is when the public comes in.

If we look at the stock market boom that began in August of 1982, the public did not invest in that stock market until 1995.

Ninety percent of the money that came into the stock market entered between 1995 and 2000.

So that final phase will occur when it finally catches on universally, when Larry Lawnmower and John Q Public are watching Maria Bartiromo talk about the next gold IPO. That is still ahead of us.

Furthermore, at that point I don't think you're going to be able to get the physical stuff.

There likely won't be enough production to meet worldwide demand, and at that point I think it's going to be easier to open your laptop and type in the ticker symbol for a gold stock than it is to go out and try to find bullion.

Jeff: Which implies higher prices for both gold and gold stocks.

Jim: Yes, higher prices in my opinion.

So what I would tell your readers right now is to maintain their core positions and know why they hold them.

Take a look at some of the larger or mid-tier producers that are not only paying dividends but increasing them.

Look at a company like Newmont; they've increased the dividend by over 100%. So at least your money is not just sitting idle – you're earning income while you're waiting for this process to unfold.

Jeff: Good advice, Jim. Thanks for sharing your insights.

Jim: You're welcome, Jeff. Thanks for having me.

Jeff Clark is the senior editor of BIG GOLD, a monthly newsletter that follows the world's best precious metals production and near-production companies. Jeff has recently completed a rather interesting special report, The Four Stocks I'm Buying My Mother, with details on precious metals stocks that are so undervalued he has recently begun buying them for his mother's retirement account. Readers can receive the special report for no charge with a 90-day, risk-free trial subscription to BIG GOLD.

© 2012 Copyright Casey Research - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.