Investing in Western Utility Stocks - Do Today’s Valuations Make Sense?

Companies / US Utilities Aug 01, 2012 - 03:43 AM GMT

In part 1 of this series on utilities published on July 26, 2012, we looked at the utility sector with a broad brush. In this part 2, we will focus on utilities located in the western part of the United States. The series was inspired because of the apparent general impression that utility stocks are overvalued.

In part 1 of this series on utilities published on July 26, 2012, we looked at the utility sector with a broad brush. In this part 2, we will focus on utilities located in the western part of the United States. The series was inspired because of the apparent general impression that utility stocks are overvalued.

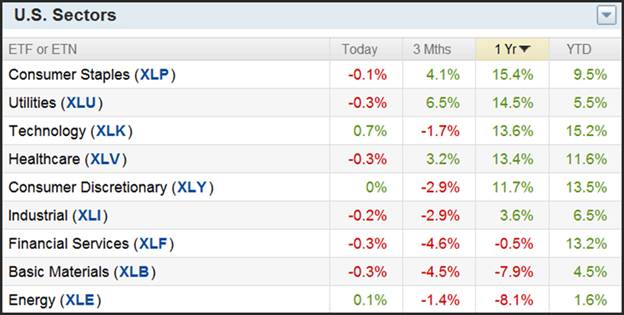

This impression stems from the fact that utilities have been the best performing sector over the past year. Therefore, people automatically assume that because an asset class has risen in price, that it must also be overvalued. However, if they have risen from previously undervaluation levels, this may not be the case. The following comparison of the performance of US ETF’s by sector first reported in part 1 on July 26, 2012, illustrates their recent outperformance.

On the other hand, with all the volatility there is today, it’s amazing the difference just a few days can make. Here is an update of the above graph through July 30, 2012, just five days later. Here we discover that utilities’ performance over the past year has still been exceptional. However, they have now moved into second place behind consumer staples but just ahead of technology, which is making a homestretch charge.

Western Utilities - A Review Of Valuation

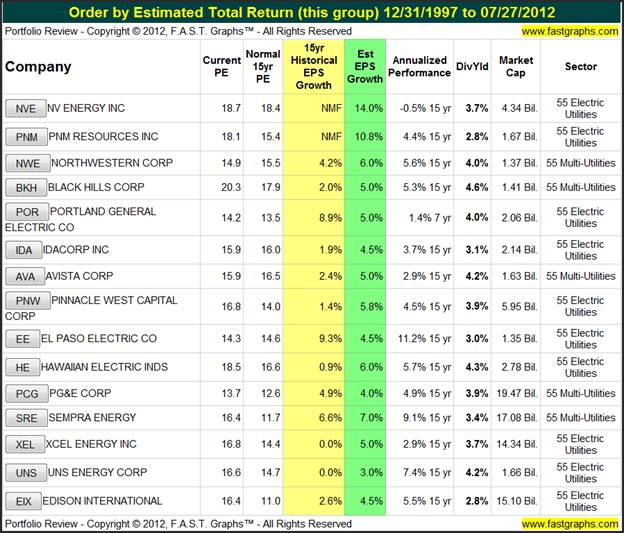

The following table compares the valuations of the major Western utility stocks utilizing the FAST Graphs™ portfolio review tool. The first two columns compare each company’s current PE ratio to the PE ratio that the market has historically applied to each stock. Based on this cursory analysis, the Western utility group appears fully valued, but not necessarily overvalued.

Based on this analysis, 3 of the 15 companies covered could technically be called moderately overvalued. However, we would not call any of them dangerously so. Another 5 of the 15, we would classify as sitting on the upper end of fair value, and the remainder we would call fairly valued. On the other hand, we did not see any that we would be willing to call undervalued companies in this Western region of the utility sector.

There are several issues regarding investing in utilities stocks that are important to consider. As a general rule, the utility industry has been a low growth industry due to the regulated nature of the majority of its business. Many utilities are attempting to diversify their businesses away from the regulated side. The third column of the table below lists the historical past 15 years earnings growth. As a review of the table shows, only El Paso Electric Co. (EE), Portland General (POR) and Sempra Energy (SRE) display any acceptable historical growth.

However, the reviewer might also notice by the estimated EPS column, that estimated growth for most companies is more optimistic. Many of the utilities in the Western region are currently involved in regulatory activity, which is nothing new for utilities in this region. Then there is the issue of capital expenditures requiring cost of capital filings. Consequently, a large part of the future growth prospects of utility stocks are at the mercy of their various regulatory commissions.

In addition to the uncertainties mentioned above, utilities are facing issues in Washington DC. In addition to proposed increases in dividend tax rates, tax credits for certain alternative energy investments are also scheduled to expire. Add it all up and there’s a lot of uncertainty regarding future earnings and dividends for this essential sector.

The typical utility stock attracts investor interest primarily with their yields; Western utility stocks are no different. However, their long-term dividend records are spotty at best. Below when we showcase individual examples, we will elaborate more on the dividend records of several Western utility companies.

Evaluating Western Utilities - A More Specific Approach

As we reviewed the individual earnings and price correlated graphs on Western utilities, we were struck by the lack of consistency in their operating histories. Consequently, our general view of the utility sector as a conservative income generating equity asset class was challenged. Although there are exceptions, the variability of earnings within the Western utility sector is a concern.

What follows is a look at specific examples of Western utilities based on valuation. What we found as we examined utilities from the Western geographic region was a rather vague determination of value. Although many in this group could be considered reasonably or fairly priced, we found none that we would consider compelling. On the other hand, we saw none that we would call ridiculously or dangerously overvalued either.

Overvalued Examples

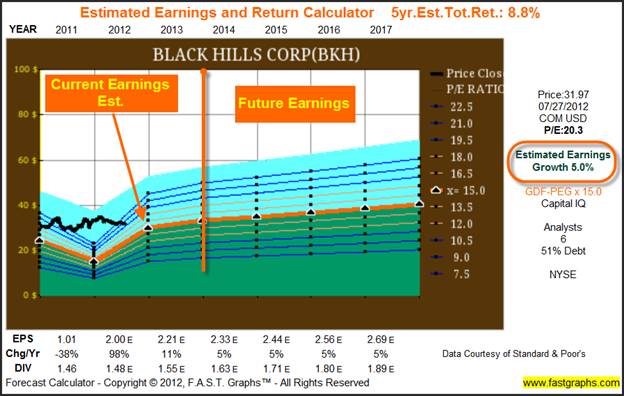

Black Hills Corporation (BKH)

Directly from the company’s website:

“Black Hills Corporation is a strong, diversified energy company with a vision to be the energy partner of choice. Our utility operations include Black Hills Power - an electric utility and our legacy business that provides service to approximately 68,000 customers in the Black Hills region and sells surplus power in wholesale markets - and Cheyenne Light Fuel & Power, serving 39,300 electric customers and 34,500 natural gas customers in the greater Cheyenne, Wyo., area.

Additionally, our recently acquired Black Hills Energy utility operations provide electric services to approximately 94,000 customers in southeastern Colorado and natural gas utility services to approximately 527,000 customers in Colorado, Iowa, Kansas and Nebraska.

Our energy portfolio also includes non-utility businesses; Black Hills Exploration & Production produces oil and natural gas in New Mexico, Wyoming and Colorado. The Wyodak coal mine in Wyoming's Powder River Basin supports the Company's low-cost, mine-mouth power generation. Black Hills also has a fleet of power generation facilities in Colorado, Wyoming and South Dakota that produce more than 1,000 MW of energy annually for our own utility customers as well as others.”

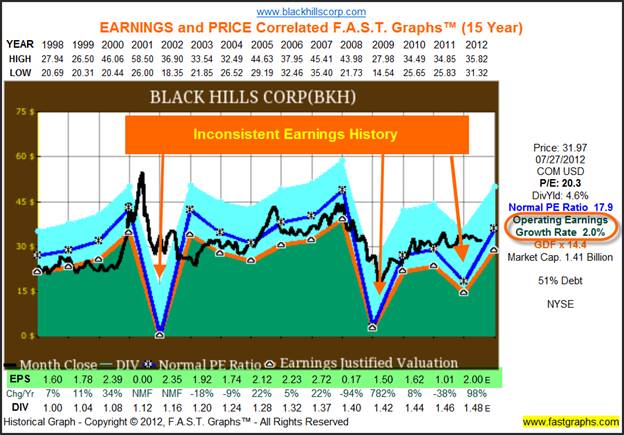

Black Hills Corp. represents a classic example of the Western utility with inconsistent historical operating results. In addition to earnings generally growing very slowly, we discover more than one instance of earnings collapsing and/or even disappearing altogether.

The current higher than average blended PE ratio of 20.3 can be attributed to weak fiscal 2011 earnings. Therefore, overvaluation in this case is more a function of sagging earnings than high stock price.

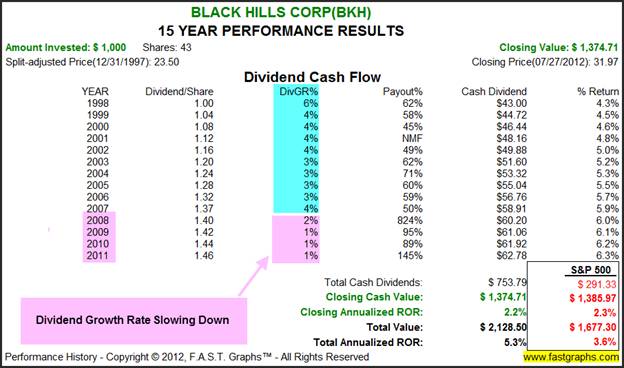

When you analyze Black Hills Corp.’s performance since 1998, you discover a reasonably steady record of consistent dividend payments with moderate growth. Moreover, notice how dividend growth has slowed down in recent years consistent with recent inconsistent earnings performance.

Consensus estimates for future earnings growth for 2012 look for a 5% per annum average growth rate. Given the company’s history, I find it hard to accept a consistent record of future growth. However, if it were to happen, this stock would not really be as overvalued based on future earnings, as it looks now based on current earnings.

Moderate Overvaluation Examples

Hawaiian Electric Industries, Inc. (HE)

Directly from the company’s website:

“Hawaiian Electric Industries, Inc. (HEI) supplies power to 95% of Hawaii's population through its electric utilities, Hawaiian Electric Company, Inc., Hawaii Electric Light Company, Inc. and Maui Electric Company, Limited, and provides a wide range of financial services to individuals and businesses through American Savings Bank, F.S.B., one of Hawaii’s largest financial institutions.”

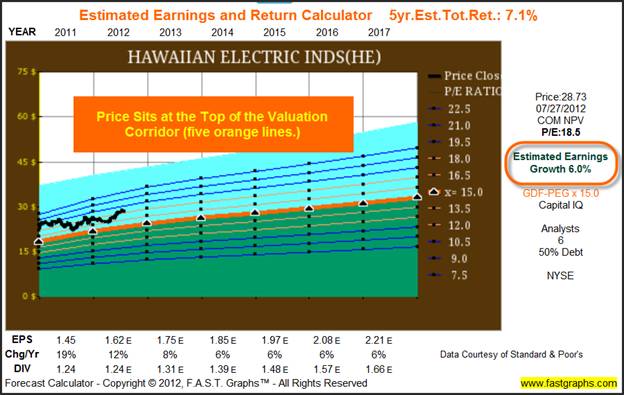

Hawaiian Electric has had a lot of trouble generating any earnings growth due to difficulty in getting regulatory cooperation or relief. However, according to the Value Line Investment Survey, a new regulatory mechanism has been enacted providing for annual rate adjustments for capital spending. However, it is still questionable as to whether this will have any meaningful impact on future returns.

The stock is rated as moderately overvalued based on historic norms. However, overvaluation is not significantly high, especially considering stronger future earnings forecasts, which I will examine later. On the other hand, as I discussed in part 1, and will restate in the summary of this article, overvaluation at any level for a slow growth utility is more troublesome than it would be with a business with greater growth potential.

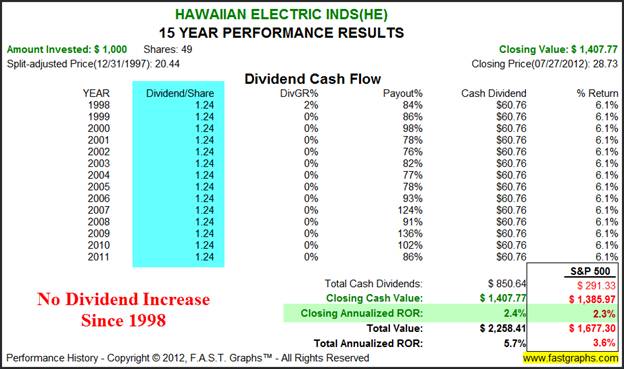

When you review the performance of this utility, you discover that the company has not increased their dividend since 1998. Moreover, capital appreciation, although it has generally mirrored the S&P 500, has not been very attractive either.

When we check current consensus earnings estimates, we discover a more positive outlook than history has justified. Perhaps this is attributed to the new regulatory mechanism. However, if history is any guide, this may still not translate into any meaningful change in dividend policy.

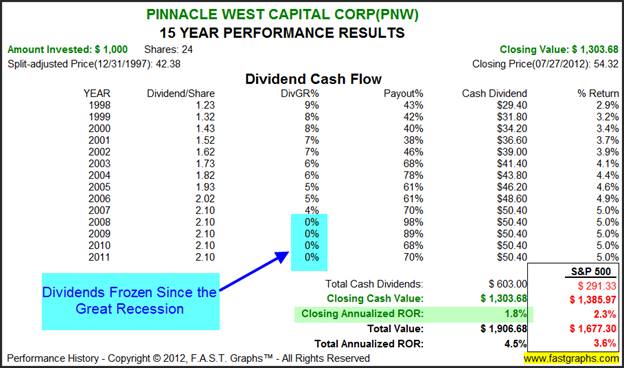

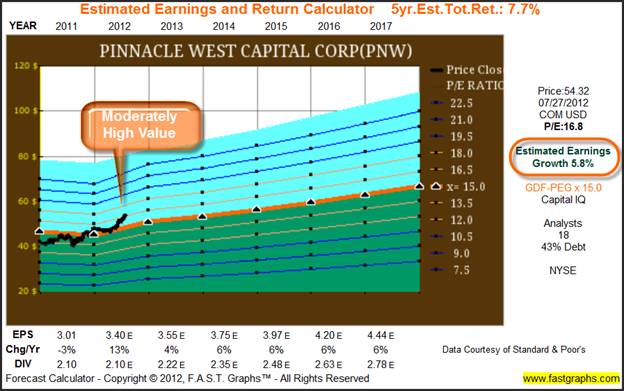

Pinnacle West capital Corp. (PNW)

Directly from the company’s website:

“For 125 years, Pinnacle West and our affiliates have provided energy and energy-related products to people and businesses throughout Arizona. Based in Phoenix, Pinnacle West has consolidated assets of about $11 billion.

Our largest affiliate, Arizona Public Service (APS), generates, sells and delivers electricity and energy-related products and services. APS serves more than a million customers in 11 of Arizona’s 15 counties, and is the operator and co-owner of the Palo Verde Nuclear Generating Station – a primary source of electricity for the Southwest.

Our other affiliate is El Dorado Investment Company, a venture capital and investment firm.”

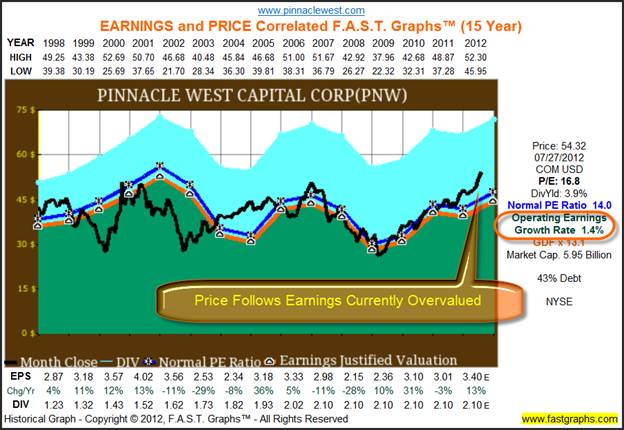

Here we find another example of low and inconsistent earnings growth. Also, based on historical norms, the company’s shares do appear to be overvalued at this time. This is another company that faces significant regulatory hurdles that could severely cripple their ability to consistently grow their business.

When we calculate the historical performance of this Western utility, we discover another example of a spotty dividend growth record, and low capital appreciation that is consistent with its earnings record. Therefore, with returns historically this low, even moderate overvaluation may prove to be a significant long-term problem.

Once again, we see another example where consensus estimates exceed historical earnings growth. However, even these more optimistic earnings estimates can hardly justify the risk of investing at today’s moderate overvaluation.

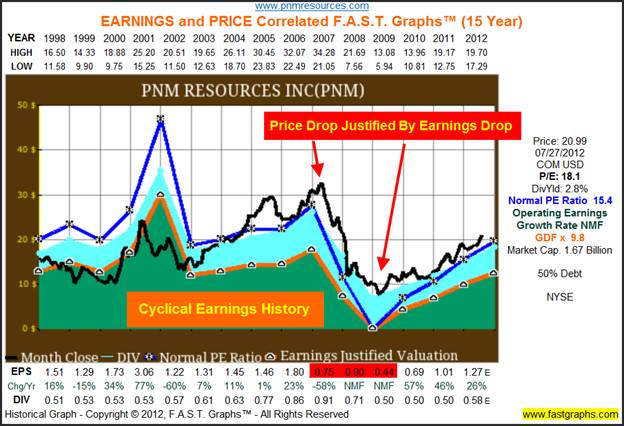

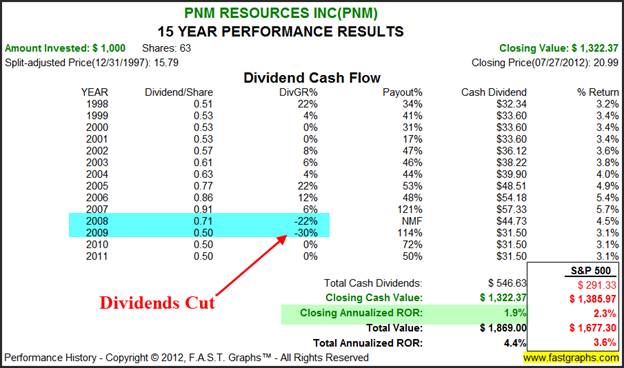

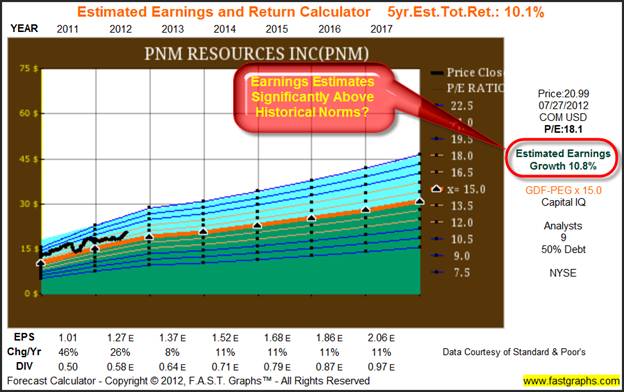

PNM Resources Inc. (PNM)

Directly from the company’s website:

“Based in Albuquerque, N.M., PNM Resources is an energy holding company with 2011 consolidated operating revenues of $1.3 billion. Through its utilities - PNM and TNMP, PNM Resources serves electricity to nearly 730,000 homes and businesses in New Mexico and Texas.

Our generation capacity of more than 2,530 megawatts reflects a balanced mix of coal, natural gas, nuclear, wind and solar generation.”

We included the earnings and price correlated 15 year historical graphs on PNM Resources to illustrate how cyclical utility earnings can be. Moreover, price volatility that is justified by earnings volatility may be more than one might be willing to accept from this typical regulated utility.

When looking at the performance of this utility, there are a couple of significant points that need to be considered. First of all, capital appreciation is very weak, even though the company’s stock price is technically moderately overvalued. Typically, when we see overvaluation, we expect to see excess return as a result. Next, significant dividend cuts in 2008 and 2009 do not instill a lot of confidence.

PNM Resources look to be a company in transition. They recently exited the competitive energy arena which makes them more dependent on the regulated business. Consequently, estimates for future earnings growth are much higher than normal. However, I question the sustainability of the currently expected future growth.

Fairly Valued Examples

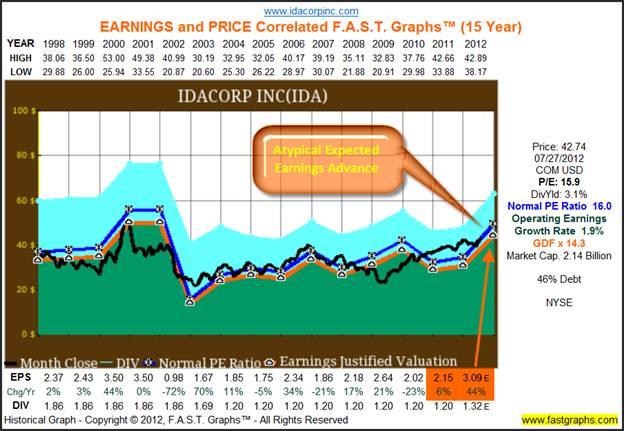

IDACORP, Inc. (IDA)

Directly from the company’s website:

“IDACORP, Inc. (NYSE: IDA) is based in Boise, Idaho and was formed in 1998 as a holding company. IDACORP subsidiaries include: Idaho Power, a regulated electric utility; IDACORP Financial, an investor in affordable housing projects and real estate; and Ida-West Energy, an operator of small hydroelectric projects. IDACORP’s origins lie with Idaho Power and operations beginning in 1916. Today, Idaho Power employs approximately 2,000 people who serve nearly 500,000 customers throughout a 24,000-square-mile area in southern Idaho and eastern Oregon.”

Once again, we see another example of inconsistent earnings results and low growth. Technically, this company would be considered fairly valued today, but only because of an atypical expected earnings advance this fiscal year. This again confirms our belief that ascertaining fair value for utility stocks is more art than science.

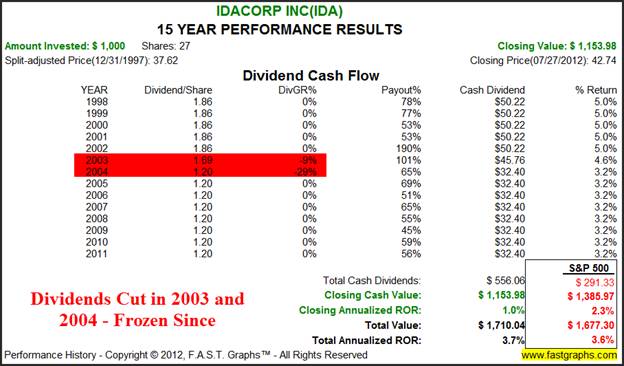

When examining the long-term performance of this company once again we discover low capital appreciation and a spotty dividend record. We had no increases, a couple of dividend cuts and a frozen dividend since the last cut. However, this electric utility has increased its dividend for this fiscal year.

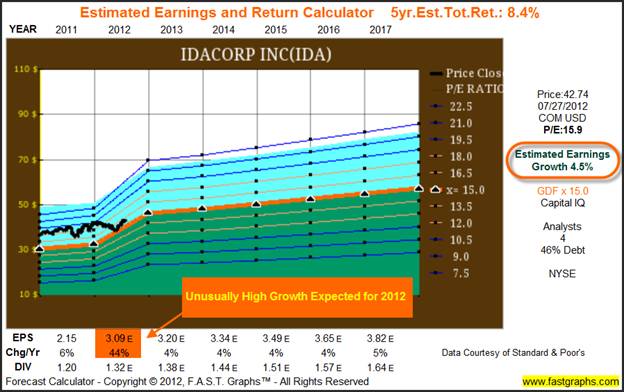

Even though this company appears to be fairly valued, low expectations for future growth past this fiscal year do not paint a compelling picture.

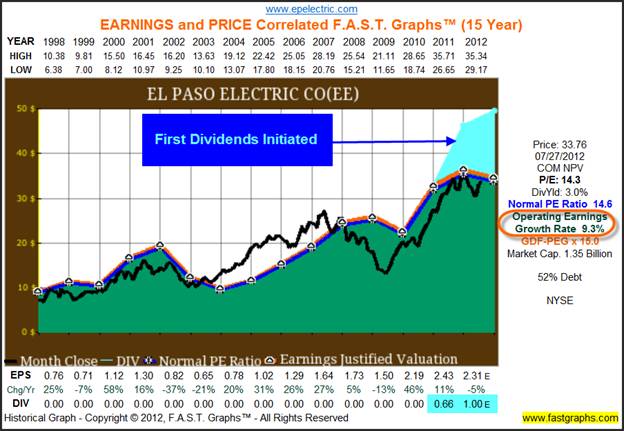

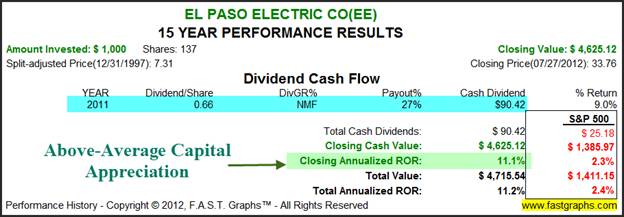

El Paso Electric Co (EE): Not a Typical Utility

Directly from the company’s website:

“Today, El Paso Electric is a regional electric utility providing generation, transmission and distribution service to approximately 380,000 retail and wholesale customers in a 10,000 square mile area of the Rio Grande valley in west Texas and southern New Mexico. Its service territory extends from Hatch, New Mexico to Van Horn, Texas and includes two connections to Juarez, Mexico and the Comisión Federal de Electricidad (CFE), Mexico’s national utility. EPE’s principal industrial and large customers include steel production, copper and oil refining, and United States military installations including the United States Army Air Defense Center at Fort Bliss in Texas and the White Sands Missile Range and Holloman Air Force Base in New Mexico.

EPE has a net dependable generating capability of 1,795 MW. It’s facilities include a 15.8 percent interest in the Palo Verde Nuclear Generating Station in Wintersburg, Arizona, a 7 percent interest in the Four Corners Station in northwestern New Mexico, the Rio Grande Power Station in Sunland Park, New Mexico, the Newman Power Station and the Copper Power Station in El Paso and the Hueco Mountain Wind Ranch in Hudspeth County, Texas.”

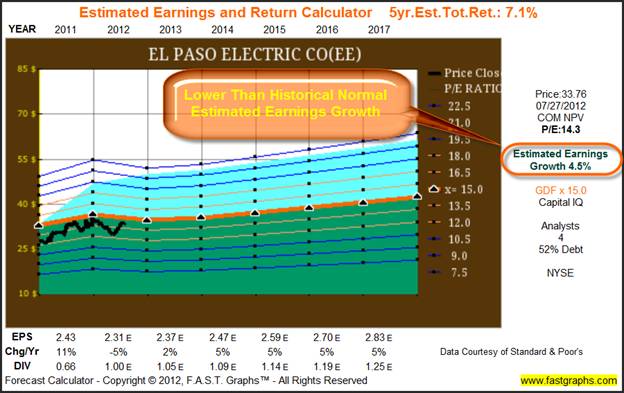

My final example of Western utilities looks at El Paso Electric, a utility stock that does not fit the typical utility mold. First of all, the company’s earnings growth rate is significantly above the average Western utility. On the other hand, the company instituted its first dividend in 2011. However, continuing disputes with their regulatory commission puts future earnings growth at risk.

Thanks to stronger than average historical earnings growth, this Western utility has provided the best performance amongst its peers in spite of the lack of the dividend. However, a lot has changed its regulatory environment, therefore, the past is clearly no indicator of the future in this specific case.

Although this company appears fairly valued both on a historical and a future basis, long-term future returns based on reduced earnings expectations are not very promising.

Summary and Conclusions

After examining the predominant companies in the Western utility group we came away with several impressions. First of all, these utility stocks are not the ultra conservative investments that many people believe that utilities normally are. Furthermore, in our opinion, rather anemic historical and forecast returns do not warrant the required extensive level of due diligence and research that would be required to invest in any one of these companies. The capital structure, sources of revenue, and various regulatory challenges appear foreboding. Especially when you weigh the potential below-average returns that all this effort stands to reward you with.

Furthermore, we want to emphasize that this article has reviewed the Western utility sector solely on the basis of their historical earnings and price correlations, plus consensus forecasts. As we have alluded to in the past, this industry is going through a lot of changes; many of them mandated by the difficulty these companies have had growing their businesses. Therefore, there’s a lot of uncharted territory that will be the driver of tomorrow’s returns. Investors need to ask themselves if the rewards are worth the risks.

Finally, the primary emphasis of this series of articles is intended to determine the relative valuation of utility stocks today. However, this has presented us with a conundrum of sorts. Although we did not find a lot of excessive overvaluation so far, we are not finding any significant undervaluation either. Since utility stocks are typically very low growth enterprises, we believe that the prudent investor is best served and, in our opinion, must insist on very low valuation before they can prudently invest in this equity class, if they should even invest in all. Utility companies provide great and essential services to their customers. Therefore, it may be acceptable for them to be regulated as they are. However, the total package doesn’t add up to a great investment story. There is little growth, however, usually decent dividend yields, all wrapped up in a lot of uncertainty. Caveat emptor.

Disclosure: No positions at the time of writing.By Chuck Carnevale

Charles (Chuck) C. Carnevale is the creator of F.A.S.T. Graphs™. Chuck is also co-founder of an investment management firm. He has been working in the securities industry since 1970: he has been a partner with a private NYSE member firm, the President of a NASD firm, Vice President and Regional Marketing Director for a major AMEX listed company, and an Associate Vice President and Investment Consulting Services Coordinator for a major NYSE member firm.

Prior to forming his own investment firm, he was a partner in a 30-year-old established registered investment advisory in Tampa, Florida. Chuck holds a Bachelor of Science in Economics and Finance from the University of Tampa. Chuck is a sought-after public speaker who is very passionate about spreading the critical message of prudence in money management. Chuck is a Veteran of the Vietnam War and was awarded both the Bronze Star and the Vietnam Honor Medal.

© 2012 Copyright Charles (Chuck) C. Carnevale - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.