There is a Hole in the U.S. Economy, Economic Growth Could be Slashed By 71%

Economics / US Economy Jul 19, 2012 - 02:43 PM GMTBy: Dan_Amerman

Everything from the ability to pay for Social Security, to projected federal deficits, to retirement planning and stock market valuations is based upon assumptions that the United States and other nations will emerge from crisis and return to "normal" long-term growth rates.

Everything from the ability to pay for Social Security, to projected federal deficits, to retirement planning and stock market valuations is based upon assumptions that the United States and other nations will emerge from crisis and return to "normal" long-term growth rates.

What happens if we don't return to those growth rates?

When we step far back from the crisis in Europe, the US fiscal cliff, the Federal Reserve's "twists" and "easings", and other day to day headlines, and we instead go down deep to the very bedrock factors that help determine economic growth - then we can see that some major changes have taken place. Indeed, when we combine three of these deep and fundamental factors, there are strong historical reasons to believe that the United States growth rate could drop from a long-term historical rate of 3.5%, to an annual rate of 1.3% - and a per capita rate of 0.2% - in the coming decades.

If so, then over a period of a little more than 20 years this would compound to a 71% reduction in economic growth. This lack of future growth would result in a 40% smaller overall economy, compared to what it would be with normal growth. Because current government deficit projections, stock market valuations, and retirement planning models are all based upon "normal growth", the results would be catastrophic. There would be a much smaller economy available to support retirement and government promises, almost no growth in the stock market, and a long-term collapse in the value of retirement portfolios and pension plans.

This may sound extreme. Yet, the three factors reducing long-term growth rates are not wild "gloom and doom" projections, but rather are quite fundamental factors that form the bedrock of the economic and financial present and future, albeit little noticed in the exciting daily hubris of the financial news.

Debt Overhangs

The first issue is that the United States government is heavily in debt, with outstanding federal debt in excess of 100% of the size of the national economy. This could lead to many different outcomes, which may or may not include default, and may or may not include hyperinflation or a currency collapse.

What we do know is that many nations have been in this situation in the past, and regardless of the particulars for how it was resolved - there is almost always a powerful, long-term drag on economic growth. Heavy government debts generally create a somewhat toxic environment for economic growth, and the resulting reduction in growth rates isn't speculation, but is in fact global economic history for many nations over the centuries.

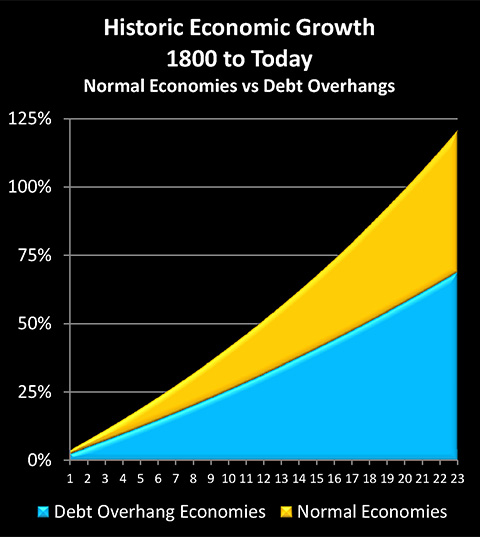

An excellent historical analysis of this issue can be found in the working paper, "Debt Overhangs: Past and Present", which was published by the National Bureau of Economic Research in April, 2012. Authored by Carmen Reinhart, Vincent Reinhart and Kenneth Rogoff, it examines 26 different "debt overhangs" that have occurred around the world since 1800, with "debt overhang" being defined as public debt exceeding 90% of GDP for at least five years. Among the many nations studied were the United States, the United Kingdom, Japan, Canada and Australia.

The analysis determined that while growth averaged 3.5% per year when public debt was less than 90% of GDP, it went down to only 2.3% per year when public debt was more than 90% of GDP. This is a reduction of 1.2%, or a little more than a third of annual economic growth.

A reduction of a little more than 1% per year may not sound like much, but it is critical to keep in mind that economic growth rates are a form of exponential compounding that drive everything from average household incomes to budget deficits to stock market valuations. Over 20 years, an economy growing at 3.5% per year will almost double in size. However, an economy growing at 2.3% per year will increase in size by a little more than 50%. So, almost half of the economic growth is lost, and the total economy is almost a quarter lower in size than it would have been without the massive government debt outstanding (ending GDP equals 158% of starting GDP, instead of 199%).

What Reinhart, Reinhart and Rogoff found was that the average duration of a debt overhang was 23 years, and that the end result was a 24% reduction in the size of national economies, compared to what they would have been if they had grown at their average growth rates when not crippled by large government debts.

That is a startling number.

If household income were to rise and fall with the overall economy (it has been growing at a lower rate in the US), then if the United States had had today's debt overhang during the period from 1985 to 2008:

- Median household income would be about $38,000 a year, instead of $50,000 per year.

- Government spending would be much less, or taxes much higher, or deficits much higher - or some combination of the three.

- Social Security would be running a huge annual deficit, and it would have started years before.

- The day to day standard of living for the entire nation would be appreciably lower, and would be seen in everything from cars driven, to the size of average homes and apartments, to food, to electronics and restaurant sales.

- Half of the growth in corporate profits would not have occurred - and the stock market would be far lower.

The empirical evidence from more than two centuries of world history is that if a debt overhang had existed in the United States starting in 1985 - there is about a 90% chance that it would dominate our current day to day standard of living, government spending, and investment performance (the nations in debt overhangs avoided the reduction in growth rate in only 3 of the 26 episodes analyzed).

For the majority of the people in the middle, life would be at least a little different, and that would be seen in everything from the meals they eat, to the size of their TV and how old their car was.

Those beneath the poverty line would be more numerous, and the safety net would likely be less, because it couldn't be paid for.

For the wealthy and upper middle class - their paper wealth would be considerably less, likely less than half as much, because profits would have been slashed for decades, and lower growth rates would be assumed for what profits there were.

Of course, this didn't happen; there was no debt overhang in 1985. But, it has happened today: outstanding federal debt is more than the 100% of the size of the United States economy, meaning the US is currently well into the debt overhang range.

And history shows that out of the 26 times that nations have found themselves in this position over the last couple of centuries, there were 23 cases where the citizens of the nation became a little poorer every year as a result (compared to normal growth), for decades to come. From where we are today then, it is all too likely that as the annual nicks in economic growth add up, year after year, our standards of living will feel the ever-increasing cumulative damage, with ripple effects that change everything from the viability of Social Security and Medicare to the value of the stock market.

Unfortunately, there is more to future growth rates than "just" debt overhangs. To get a more complete picture, we need to take a look at something else, which is what happens when debt overhangs combine with rapidly aging populations.

An Aging Population

In a major speech in October of 2006, Federal Reserve Chairman Ben Bernanke identified what he believed would be the single most important influence on the economy in the decades to come. He asserted that as the Baby Boom aged, the declining number of workers as a percentage of the population would likely decrease the growth rates for per capita GDP, decrease the growth rate in living standards, and decrease the growth rate in consumption.

Now, one might say that Bernanke missed the mark entirely, as he failed to anticipate the building financial crisis of 2007 that would lead to the near collapse of 2008, with disastrous consequences that still dominate the global economy today - and that would be correct. Bernanke did completely fail to foresee the changes that would shatter the economy under his watch.

Bernanke's blunder does not, however, make the major demographic problem that he spoke of go away, or lessen it. Indeed the problem is that the two are happening side by side, and both are powerful long term trends that may last for decades. The Boomers are aging, while the national debt is sky-high and climbing - and both will be true for many years to come.

The precise impact of an aging Baby Boom is harder to assess than debt overhangs, as this is not something that one can study over the centuries. It is a phenomenon of the early 21st century, being the result of the intersection of fundamental advances in medicine, the post-World War II economic and social environment, and the arrival of highly effective and convenient birth control in the 1960s.

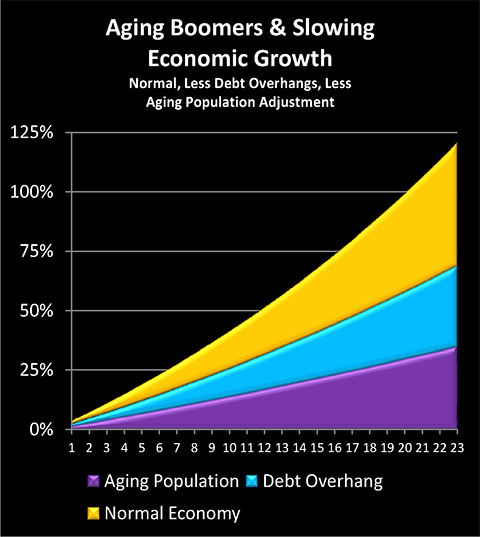

That said, economists have given the assessment a try, and during the same month that Bernanke gave his speech, the Economist magazine published an article titled “The Slow Road Ahead". A number of economists were consulted about the economic impact of this upcoming fundamental demographic change, and the consensus was that there might be a new "speed limit" for economic growth of around 2.5% per year among the aging nations of the West. In other words, an ever-increasing ratio of retirees to younger workers was likely to lead to about a 1% decline from the 3.5% long-term average in the developed world, with this slow down persisting for decades.

So, the debt overhang is likely to lead to a decades-long reduction in economic growth of about 1.2% per year - if this overhang works out to be average. Separately, if economists' estimates are correct, an aging nation with a steadily decreasing percentage of people in their prime working years is likely to experience reduced economic growth over the long-term, with a shortfall of about 1% per year. Combine the two factors, and economic growth falls by 2.2% per year, from 3.5% to 1.3% per year, which is a 63% reduction in the growth rate.

The next question is how long the two growth reducers are likely to work together. The average duration of a debt overhang episode is 23 years. In the United States, the peak of the Baby Boom retirement wave will arrive by the late 2020s and continue into the early 2030s, with the maximum number of Boomers still alive but age 65 and older, and the number of workers aged 64 and younger having fallen to only 2.0 per retirement age person. The two long-term problems cover similar (though not identical) periods, and 23 years is likely as good of a number as any for the calculation.

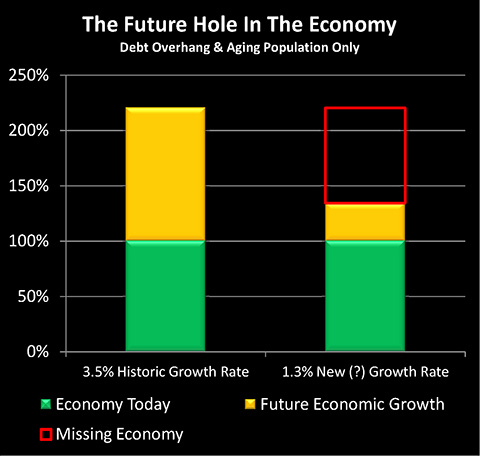

As shown in the graph below, when we take 3.5% growth and compound it for 23 years, then an economy should grow by 121%, meaning it ends up at 221% of it starting size. With a 1.3% growth rate, an economy grows by a mere 35% over 23 years, meaning it ends at only 135% of its starting size.

One way of looking at this is that the economy only enjoys 29% of the growth that it would in normal conditions, meaning 71% of historic average growth is lost to the 1-2 combination of debt overhang and aging population (35/121 = 29%).

A different perspective is that the ending economy after 23 years is only 61% of the size it would be with normal growth, meaning the average person sees a reduction of almost 40% in their income and standard of living, compared to normal economies (135/221 = 61%). To go back to our 1985 to 2008 example, if growth had been reduced by 2.2% per annum, then the median household income today would be about $30,000 per year instead of the current $50,000 per annum.

In other words, about 40% of the current US economy simply wouldn't exist.

Fortunately, this situation of a combined debt overhang and soaring retiree population didn't exist in 1985. Unfortunately, it does exist today, and this is a much worse time to have a national debt that exceeds the size of the national economy. For it isn't just that an aging population is likely to have a lower growth rate, but it costs more to maintain.

The issue is that we have a cost structure for Boomer retirement that is theoretically somewhat fixed with Social Security, Medicare and pension promises. Less money available in the overall economy means that these promises will consume an even larger share of the economy, and there is still less money available for consumption – or for buying investments from retired Baby Boomers.

Falling growth and rising costs is a toxic combination, but there is a third element to consider as well, and it also comes down to basic demographics. When we include this factor, growth may come to a halt altogether, and indeed, may already have done so.

Topics addressed in the second half of the article include: the third major demographic force; the potential near end of growth when all three are combined; and how the combination may change everything we think we know about deficits, Social Security and long-term stock market returns.

Daniel R. Amerman, CFA

Website: http://danielamerman.com/

E-mail: mail@the-great-retirement-experiment.com

Daniel R. Amerman, Chartered Financial Analyst with MBA and BSBA degrees in finance, is a former investment banker who developed sophisticated new financial products for institutional investors (in the 1980s), and was the author of McGraw-Hill's lead reference book on mortgage derivatives in the mid-1990s. An outspoken critic of the conventional wisdom about long-term investing and retirement planning, Mr. Amerman has spent more than a decade creating a radically different set of individual investor solutions designed to prosper in an environment of economic turmoil, broken government promises, repressive government taxation and collapsing conventional retirement portfolios

© 2012 Copyright Dan Amerman - All Rights Reserved

Disclaimer: This article contains the ideas and opinions of the author. It is a conceptual exploration of financial and general economic principles. As with any financial discussion of the future, there cannot be any absolute certainty. What this article does not contain is specific investment, legal, tax or any other form of professional advice. If specific advice is needed, it should be sought from an appropriate professional. Any liability, responsibility or warranty for the results of the application of principles contained in the article, website, readings, videos, DVDs, books and related materials, either directly or indirectly, are expressly disclaimed by the author.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.