Can Bernanke Force Banks to Lend by Halting Interest on Excess Reserves?

Interest-Rates / Credit Crisis 2012 Jul 13, 2012 - 07:03 AM GMTBy: Mike_Shedlock

Several readers have ask me to comment on a King World interview of Michael Pento.

Several readers have ask me to comment on a King World interview of Michael Pento.

Before I offer my comments on Pento's thoughts, let me say upfront that Eric King is a world-class interviewer. King lets his interviewees have their say, no matter what it is.

It is up to listeners to decide whether the message makes any sense or not. King merely wants the position to be well stated.

Email Request From US

Hello Mish:

Have you listened to Mike Pento's scenario where the FED will cease to pay interest on reserves held at the FED, as a result, forcing banks to loan out the money to seek some return. He believes that they will be encourage to purchase US treasuries:

Is this viable and/or probable?

Thanks for providing us with such a great blog.

All the best,

Dan

Email From Down Under

Dear Mish

I follow your work from Australia with great interest. I was impressed with your argument that the creation of new money will not lead to price increases because it is deposited with the Fed, and does not make it into the real economy.

You will no doubt be aware of recent comments by Michael Pento on King World News that the Fed is about to eliminate the incentives for the banks to deposit excess reserves with the Fed, and that this will force the banks to lend in the economy and cause significant inflation, and presumably a drop in the USD.

I would be greatly interested in your views on this, as a deflationist, because if Pento is right then the reason for deflation over inflation might be eliminated. Furthermore, the worsening in key stats such as auto sales and official unemployment might just be the trigger that forces the Fed to squeeze the money out into the economy.

Best regards

Henry

Primer on Bank Lending

With that background out of the way, my first thought is "Here we go again. How many times does such silliness have to be rebutted before it stops?"

Banks lend if and only if both of the following are true.

- They are not capital impaired

- They have credit-worthy borrowers willing to borrow.

That is not an opinion. Rather, that is a statement of fact. I discussed this at length many times.

Excess Reserves Yet Again

Here is a discussion from BIS Working Papers No 292, Unconventional monetary policies: an appraisal.

Note: The above link is a lengthy and complex read, recommended only for those with a good understanding of monetary issues. It is not light reading.

The article addresses two fallacies

Proposition #1: an expansion of bank reserves endows banks with additional resources to extend loans

Proposition #2: There is something uniquely inflationary about bank reserves financing

From the article....

The underlying premise of the first proposition is that bank reserves are needed for banks to make loans. An extreme version of this view is the text-book notion of a stable money multiplier.

In fact, the level of reserves hardly figures in banks' lending decisions. The amount of credit outstanding is determined by banks' willingness to supply loans, based on perceived risk-return trade-offs, and by the demand for those loans.

The main exogenous constraint on the expansion of credit is minimum capital requirements.

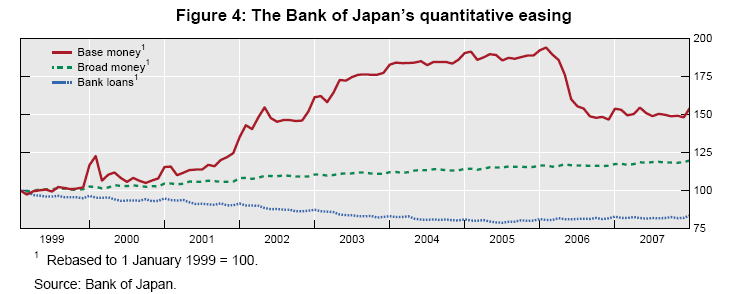

A striking recent illustration of the tenuous link between excess reserves and bank lending is the experience during the Bank of Japan's "quantitative easing" policy in 2001-2006.

Japan's Quantitative Easing Experiment

Despite significant expansions in excess reserve balances, and the associated increase in base money, during the zero-interest rate policy, lending in the Japanese banking system did not increase robustly (Figure 4).

Is financing with bank reserves uniquely inflationary?

If bank reserves do not contribute to additional lending and are close substitutes for short-term government debt, it is hard to see what the origin of the additional inflationary effects could be.

Lending Theory

There is much additional discussion in the article, but it is clear that money lending theory as espoused by many did not happen in Japan, nor is there any evidence of it happening in the US, nor is there a sound theoretical basis for it.

In fiat credit-based economies, lending comes first, reserves come second.

Fed's Next Move

Pento was preaching the same thing on IB Times FX in The Fed's Next Move

As I predicted as far back as June of 2010, the Fed will soon follow the strategy of ceasing to pay interest on excess reserves.

Since October 2008, the Fed has been paying interest (25 bps) on commercial bank deposits held with the central bank. But because of Bernanke's fears of deflation, he will eventually opt to do whatever it takes to get the money supply to increase. With rates already at zero percent and the Fed's balance sheet already at an unprecedented and intractable level, the next logical step in Bernanke's mind is to remove the impetus on the part of banks to keep their excess reserves laying fallow at the Fed. Heck, he may even charge interest on these deposits in order to guarantee that banks will find a way to get that money out the door.

Commercial banks currently hold $1.42 trillion worth of excess reserves with the central bank. If that money were to be suddenly released, it could through the fractional reserve system, have the potential to increase the money supply by north of $15 trillion! As silly as that sounds, I still hear prominent economists like Jeremy Siegel call for just such action. If they get their wish, watch for the gold market to explode higher in price, as the U.S. dollar sinks into the abyss.

Emphasis his.

Facts of the Matter

- Money supply has already soared by any number of measures.

- Credit expansion has been anemic except for student loans and FHA (both with government guarantees)

- The Fed did not cease paying interest on excess reserves as predicted in 2010.

- It would not matter from a lending perspective if the Fed did.

- The idea that excess reserves will come pouring into the economy, multiplied 10 times over is widely believed nonsense. In practice, lending comes first, reserves second. (see "The Roving Cavaliers of Credit" by Steve Keen for further excellent discussion).

Inflationary Nonsense

The simple fact of the matter is Pento has no idea how bank lending works in the real world.

There is no other way to state it. If banks thought they had good credit risks, they would lend (provided of course they were not capital impaired).

Moreover, by paying interest on reserves, Bernanke is slowly recapitalizing banks over time. Would Bernanke easily give that up? Well he hasn't so far. Nor has he even dropped a hint of it.

Even if Bernanke did cease paying interest on excess reserves, it would not impact bank lending for reasons stated.

What If?

For the sake of argument let's play "What If"?

What if the Fed were to reduce interest rates on excess reserves to -3%. Would that do it? Well, it sure would get banks to do something, but that something might not necessarily be lending!

For example, banks might bet against the US dollar, bet on gold, plow into the stock market, etc., etc., etc., but there is no reason to assume banks would extend credit to unworthy borrowers.

Moreover, Bernanke (as foolish as he is), is at least bright enough to figure that out.

Thus, the idea that Bernanke can get banks to lend by reducing interest rates on excess reserves is 100% without a doubt, fatally flawed nonsense from both theoretical and practical standpoints.

ECB Cuts Reserve Rate to Zero

As a practical matter, the ECB just cut interest on reserves to zero. The result is reduced liquidity as banks shut down money market funds rather than lose money.

Please consider How Money Market Funds Were Wounded by European Interest-Rate Cuts

The cut in the interest rate was meant to convince banks to stop parking money, to lend more, to get more money into the system and make it more stable - in Wall Street parlance, to add "liquidity."

But the backlash from banks shows that they're willing to close money market funds rather than lose profits. The effect, ironically, is to reduce liquidity in the financial system.

JP Morgan alone pulled $29 billion in assets.

It's supposed to be different here?

Why?

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2012 Mike Shedlock, All Rights Reserved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.