The Euro-zone Solution Illusion

Interest-Rates / Eurozone Debt Crisis Jun 05, 2012 - 08:01 AM GMTBy: John_Mauldin

Nobody, in my book, slices and dices data more thoroughly or convincingly than Greg Weldon. In this week's Outside the Box, he first dispels the illusion that either of the two most-expected outcomes of the growing eurozone crisis is really any kind of a solution – neither expelling Greece nor keeping Greece in the club is going to work, he argues – and then, in a feat of legerdemain, he conjures up an alternative that just might work – and backs up his idea as only Greg can. But is this a rabbit he's pulled out of his hat, or is it ... a Black Eagle?

Nobody, in my book, slices and dices data more thoroughly or convincingly than Greg Weldon. In this week's Outside the Box, he first dispels the illusion that either of the two most-expected outcomes of the growing eurozone crisis is really any kind of a solution – neither expelling Greece nor keeping Greece in the club is going to work, he argues – and then, in a feat of legerdemain, he conjures up an alternative that just might work – and backs up his idea as only Greg can. But is this a rabbit he's pulled out of his hat, or is it ... a Black Eagle?

This letter will print a little longer but, as is usual with Greg, it's chock full of great charts. You can learn more about his work at www.weldononline.com. For institutions and hedge funds, it should be required reading. (It is a little more than your average service, but as you can see, he really gets into the data very deeply!)

I am in Philadelphia tonight to speak for Steve Blumenthal's Advisor Forum. We did an evening at the National Constitution Center museum, where they had a Bruce Springsteen exhibit on the first floor and rather fascinating historical display of the history of the US and the Constitution. At the end is a room where there are 39 bronze life-sized statues of the men who were at the Constitutional Convention, displayed as they might have been arrayed at the signing. It got me to thinking about the times. Indeed, there was a quote from Washington about how bad things had become in 1789, sounding much like so many who now see the US as a hopeless culture, careening down a path of socialism and entropy. And certainly, the US and much of the world face some very hard choices in the next year or so; but somehow I think we will do just fine, even if we make a few bad choices and have to correct our course more than we would like.

Of course, it helps to have a Washington, Hamilton, Franklin, Adams, Madison, and Jefferson to help guide the ship on its course, but we will have to make do with what we have. Every country needs leaders with a clear vision and a love of posterity. Maybe later generations will recognize leadership where we do not. Here's hoping.

On Wednesday I get to spend much of the day with David Rosenberg, and I am sure we will go over our own poor vision of what will happen. And Thursday I get to have lunch with George and Meredith Friedman of Stratfor, in Austin, where I will listen as he gives me his latest take on the world. I always come away from my time with them with a whole lot more insight. Then it's a few afternoon meetings and on to the University of Texas for a seminar with Rosie and Rich Yamarone (with whom I had lunch yesterday in New York). It will be fun.

Your trying to get a whole lot done in a short amount of time analyst,

Your watching my own kids grow up analyst,

John Mauldin, Editor Outside the Box JohnMauldin@2000wave.com

Macro-EU: The Solution Illusion

Weldon's Money Monitor

May 23, 2012

Dating all the way back to the day the Greek Drachma was accepted into the EU's ERM (Exchange Rate Mechanism), thus retiring Greece's currency, and replacing it with the Eurocurrency ... we have always believed that a two-tier Eurocurrency 'regime' would ultimately 'reign', once the EUR experiment failed.

We envisioned that the northern 'core' countries such as Germany, France, the Netherlands, Belgium and Austria would represent the 'first tier' EUR countries, while the southern, more indebted non-core nations, including Greece, Spain, Portugal, and Italy, would represent the 'second tier'.

Within the last two years we have abandoned that thought-process, as the 'core' itself has disintegrated, amid a deepening debt-deficit crisis in France, Belgium, Austria and the Netherlands (more of a macro-political crisis in the latter, than a sovereign debt issue).

Indeed, as we have repeatedly stated since 2009 ... 25 of the 27 EU member nations, including both France and Germany, are in violation of the Union Treaty defined (allegedly) 'hard caps' for debt, or deficits, or both.

For sure, the tectonic political shift in France puts their top-credit-rating status at greater risk ... and with it, their position as a 'core' nation.

We have already exposed Belgium and Austria for the egregious level of their sovereign debt, relative to their respective populations ... levels that are, on a relative basis, larger than the debt of Italy.

As for the countries in the south ...

... Spain is already in crisis, on ALL fronts, the sovereign debt front, the political front, the banking sector front, the housing-labor-deflation front, and the macro-economic front as it applies to domestic final demand ...

... while Italy is becoming increasingly desperate in their effort to stave off a bond market crisis.

Portugal is not as indebted as the other second-tier countries, but their banking system is less secure, and their bonds have gotten crushed.

And then there is Greece.

In April of 2010 we 'penned' the first of a trilogy of Money Monitors focused on Greece, using the "Titanic" theme.

As the ship (Greece, and their participation in the EUR) continues to sink, the options as it pertains to actions that might represent a "solution" to the Greek situation, can be whittled down to a simple choice between two courses of action:

--- Greece leaves the EU, and brings the Drachma out of retirement

--- EU officialdom does whatever it takes to keep Greece in the EU, to avoid setting a precedent that could 'spread' to Portugal and Spain, sparking a debate about a return to the Escudo and Peseta.

Seemingly, either solution is merely an illusion, as neither is likely to 'work'.

But what if everyone is looking at this from the wrong 'angle' ???

What if there is an optical illusion dynamic here that is keeping officialdom from 'seeing' an alternative 'solution' ???

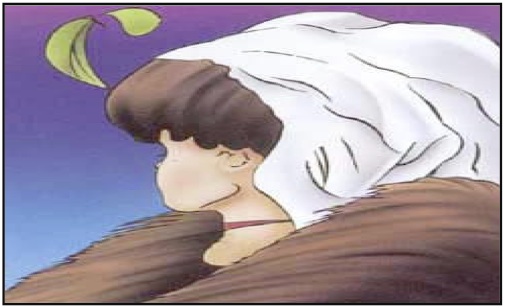

Indeed, we cannot help but think of the old 'optical trickery' offered by the 'image' on display below, picturing one of two possible 'visions'.

From the most often observed perspective, the picture is an older woman facing to the left, with a witch-like profile, and wearing a shawl.

Indeed, the vision of the old woman represents Greece.

In terms of the EU crisis, the vision of the old woman represents Greece leaving the EUR and going 'old-school', by bringing back the Drachma.

But there is an alternative 'vision' to be gleaned from within the picture shown above ... that of a young woman, with dark hair and a perky little nose, facing left and away from the front and wearing a choker (which also serves as the thin lips of the old woman).

The young woman represents an alternative 'vision'.

In terms of the European crisis, the young woman represents an alternative 'solution', one that does NOT include reviving the Drachma.

Indeed, if the Drachma were revived ... eventually, there would be a similar need to bring the Spanish Peseta and the Portuguese Escudo out of retirement too ...

... followed by the Italian Lira, and perhaps even the French Franc.

In such a circumstance ...

... ALL of these currencies would be immediately 'devalued'.

So what if we REVERSED the perspective.

What if we took the OPPOSITE 'view' ???

What if we suggest that a better solution than pushing Greece back into the Drachma ... would be to let Germany resurrect the Deutsche Mark !!!

This would allow for some level of 'rebalancing' in the underlying macro-dynamic, particularly as it applies to trade.

Moreover, this would also allow for some 'depreciation' in the EUR linked to Spain, Italy, Portugal, Greece, France, et al ... as one unit, relative to the German D-Mark.

Rather than 'seeing' the old Greek Drachma woman ...

... we 'see' the younger German Deutsche Mark woman.

Fixed-income markets use the German Bund as the benchmark against which all other sovereign bond yields are measured, as the primary 'credit spread', so why not add the foreign exchange dynamic in the same way, using the D-Mark as a benchmark.

Indeed, the two tiered system is NOT 'dead' ... but rather, the first tier would include ONLY ONE currency, the German currency.

It is Germany's understandable obsession with hard-currency 'driven' monetary and fiscal policies, that ISOLATES THEM from the rest of the EU.

So, let them have their hard currency ... the D-Mark.

And let the rest of the debt-offenders have the softer EUR.

Within the scope of enacting such a seemingly-outrageous idea, perhaps the legal framework can be 'manipulated' to enable the ECB to utilize freshly minted EUR, as a means to monetize, and thus 'eradicate', a portion of the region's sovereign debt ... in a move that would NOT need to be 'approved' by Germany.

Of course, EU officialdom is not likely to be at all enamored by this thought, but perhaps, maybe, potentially ... plenty of support for such an idea could materialize.

For sure, there would be 'problems' and potential roadblocks that we have not yet contemplated. In fact, we generated this idea out of the blue, shooting from the hip on Thursday afternoon while doing an 'interview' with our buddy and colleague Jim Puplava, on his internet radio show "Financial Sense Newshour"( financialsense.com).

But I am, myself, personally ... intrigued by the thought.

It seems to be worthy of debate, at least, given the 'keystone-cop-routine' (slapstick inefficiency) currently being performed by EU officialdom, as the crisis deepens, and broadens ... daily.

And we mean ... daily.

With nearly every data release, from any EU member nation, particularly those that are currently under the market's microscope ... the macro-economic crisis deepens, as does the push into outright deflation.

We need but evidence a mountain of data released in the EU within the last twenty-four hours, reports that include Spanish Retail Sales, Italian Unemployment, the comprehensive EU Commission Consumer and Business Sentiment Surveys, German CPI inflation, and the ECB's money supply and bank credit figures, to quickly conclude that our thesis is VALID ...

... the macro-deflation is deepening, and broadening in its scope.

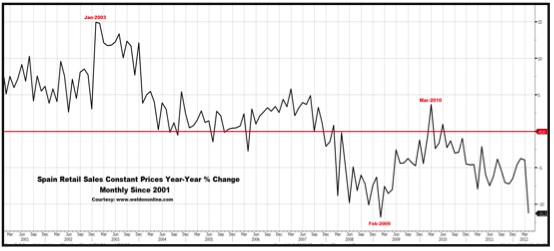

Observe the chart below revealing the complete COLLAPSE in Spanish Retail Sales, as measured by the year-over-year rate-of-change, which plunged in April to a (-) 11.3% yr-yr pace of contraction (constant prices), a massive 'deepening' relative to March's already negative (-) 4.0% rate of decline. Moreover, April's rate of contraction is the second WORST EVER, behind only the Feb-2009 decline of (-) 11.8% yr-yr.

Also of interest within the chart, is the sequentially lower highs reached at each successive macro-cycle peak. The 2006 peak as below the 2003 peak, and the most recent cycle peak set in March of 2010 was lower than both of the previous peaks.

On a 'Current Prices' basis, Spanish Retail Sales fell by (-) 8.8% yr-yr, the worst performance in the last two decades.

And, we shine the spotlight on the two downside leaders, in terms of the sectors suffering the greatest degree of deflation in final retail demand ---

--- Personal Goods, which fell (-) 19.8% yr-yr

--- Household Goods, which fell by (-) 14.3% yr-yr in April.

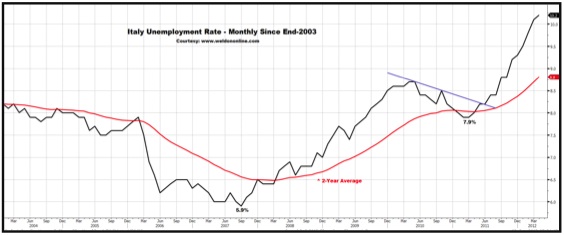

We also note this morning's release of Italian Employment figures, revealing a decline of (-) 28,000 in the Number of Employed during April, marking the third monthly contraction in a row.

In fact, since the latest mini-crisis began in August of last year, the Number of People Employed in Italy has fallen in 7 out of 9 months, with 60% of the total job loss occurring in the last two months.

Indeed, in the last two months alone (Mar-April, May is MOST assuredly to be even worse) ... Italy has lost the 'US-equivalent' of (-) 325,000 non-farm payroll employment, on a population-adjusted basis.

Subsequently, the Unemployment Rate rose to 10.2%, a greater than expected rise from the 9.8% rate originally reported for March, a figure that was revised to 10.1% with today's report.

Telling is the increase from the swing-low reached in March of last year, at 7.9%, with the Unemployment Rate having soared by 2.3 percentage points, or by +30.0% nominally.

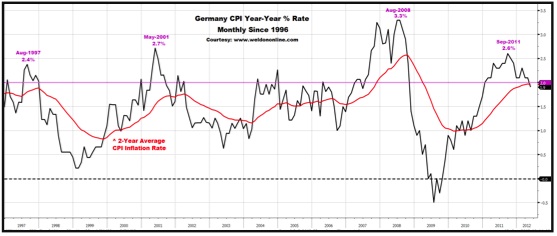

Supportive to our top-down macro-thematic thought-process is the intensifying pace of disinflation in EU Consumer Prices, particularly as it applies to Germany. Observing the chart on display below plotting the year-over-year rate of German CPI inflation. We focus on the decline to 1.9% in May, from 2.1% in April, thus bringing German inflation back below the ECB's (allegedly) hard-cap (2%), and extending the retreat from the Sept-2011 high of 2.6% yr-yr. Moreover, Germany's CPI inflation rate is now back below its 2-Year Moving Average.

More pointedly, we highlight past experiences since the nineties, during which German CPI inflation is receding, following a major-cycle peak above the ECB's 'upside band'. These time frames have been associated with intensified macro-market turbulence ... on EVERY SINGLE OCCASION !!!!

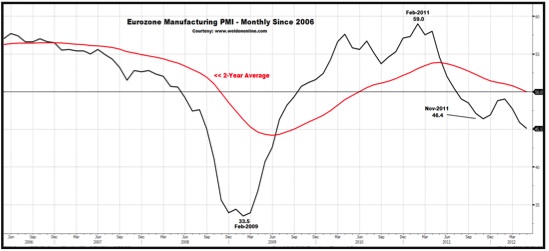

From within this morning's deluge of global macro-economic data, we extract the figures for the EU Manufacturing Purchasing Managers Index (PMIP), to spotlight the continued downside extension to a NEW MOVE LOW, as evidenced in the chart below.

Pegged at 45.1 for May, the Eurozone PMI has now been below the 2011 low for two consecutive months ... and ... has been below the boom-bust 50 level for TEN straight months.

Moreover, we note that the current level is the LOWEST since 2009 ...

... and ... we highlight the move by the secular-trend defining 2-Year Moving Average back BELOW FIFTY !!!

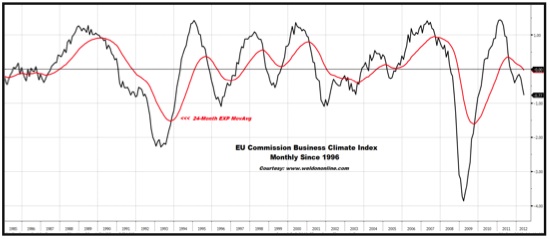

Always a monthly favorite is the EU Commission's of extensively detailed Consumer and Business Sentiment Surveys. We start with the headline EU Business Climate Index, which, as seen in the chart below, plummeted during May to reach a new move low at (-) 0.77 ... a level that in the past has been associated with 'aggravated' macro-market conditions.

Of particular interest is the decline in the secular-trend-defining 2-Year Moving Average, which has been trending lower since the middle of last year, and has now fallen below zero, again, a circumstance linked to expanded volatility in the markets, amid heightened deflation risk.

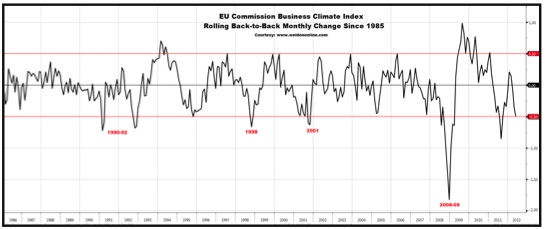

More 'telling', and thus troubling, is the macro-message to be extracted from an examination of the chart on display below in which we plot the 'rolling' back-to-back monthly change in the EU Business Climate Index.

The Index was down by (-) 0.26 in May, a deep single-month decline that came hard-on-the-heels of April's monthly decline of (-) 0.24, for a back-to-back, 'monthly', cumulative decline of (-) 0.50 ...

... which, puts the April-May 2012 period into the 'danger-zone', as defined within the chart, as the (-) 0.50 level. Indeed, previous periods where the headline EU Business Climate Index has fallen by this degree, are linked DIRECTLY to periods of 'recession', and heightened 'crisis' risk ---

--- in 1990-92, 1998, 2001, 2008-09 ... and, now.

Another perspective is offered by the EU Commission, and their own, smoothed, "Twelve-Month Average Business Climate Index". We note the non-stop, sequential-and-near-symmetrical collapse into negative territory, since last September:

May-12 ... (-) 0.12

Apr-12 ... + 0.03

Mar-12 ... + 0.17

Feb-12 ... + 0.31

Jan-12 ... + 0.45

Dec-11 ... + 0.58

Nov-11 ... + 0.71

Oct-11 ... + 0.82

Sep-11 ... + 0.91

The EU Commission Surveys include detailed data for each EU-27 member nation, across the Service Sector, the Retail Sector, and the Construction Sector ... with May readings being heavily skewed towards the negative, in every category, in nearly every country.

Having dissected all fifty-two pages, we come out with a common theme as it relates to the 'country-performance'. To wit:

--- Spain, Portugal and Italy are severely damaged, and sinking fast.

--- the Netherlands, France, Belgium, Finland and Sweden are hurt, and the pain is worsening.

--- Hungary is a potential wild-card.

--- and, there is now sequential erosion in Germany.

Data scalpel in hand, we begin carving into the Service Sector readings, noting that the headline EU Confidence Index (services) fell to (-) 6.0 in May, down from (-) 3.7 in April ... with the Future Demand Index falling to a barely positive + 0.4 in May, down from + 3.7 in April ... and ... the Recent Employment Index fell into negative territory for the second month in a row, pegged at (-) 1.9 in May, versus (-) 0.8 in April, and + 1.5 in March.

Of GREAT interest, particularly given the HIGH and RISING rates of Unemployment across the Continent ... is the PLUNGE in the Service Sector Future Unemployment Index (expected). We evidence the chart on display below with focus on the recent mini-collapse back into negative ground.

The reading for May was pegged at (-) 3.1 ... down from April's (-) 0.4, and sharply lower relative to March's positive reading of + 3.0. We also spotlight the previous violation of, and most recent downside reversal by, the long-term trend-defining 2-Year Moving Average.

We make several more detailed observations on the Service Sector data (all figures, for all sectors, are relative to April except where noted):

Spain, Recent Employment ... (-) 21.1 ... down from (-) 17.4

Spain, Future Employment ... (-) 10.3 ... sliding from (-) 1.7

France, Recent Demand ... (-) 3.3 ... down from + 2.5 (March)

Italy, Future Demand ... (-) 9.2 ... deepening from (-) 5.7 (March)

Italy, Confidence ... (-) 19.5 ... versus (-) 11.3 (March)

Netherlands, Confidence ... (-) 10.3 ... down from (-) 9.4

Belgium, Recent Demand ... (-) 5.0 ... down from + 4.3

Looking next at the Construction Sector, we observe that the headline EU Confidence Index dropped to a NEW MOVE LOW, at (-) 32.4, down from (-) 30.4 in April ... with a particularly steep decline in the Construction Activity Trend Index, which plummeted to (-) 20.5 in May, from (-) 13.5 in April.

Breaking it down, we find the following data nuggets to be of interest:

Spain, New Orders ... (-) 49.7 ... 'crashing' from (-) 34.1

Spain, Confidence ... (-) 56.6 ... deeper still, from (-) 50.9

Portugal, Confidence ... (-) 75.1 ... down from (-) 66.1

Portugal, Employment ... (-) 63.6 ... down from (-) 51.1

Italy, Activity Trend ... (-) 42.9 ... down from (-) 39.0

Italy, Employment ... (-) 18.6 ... down from (-) 14.2

France, Confidence ... (-) 16.4 ... down from (-) 14.9

Hungary, Confidence ... (-) 44.6 ... down from (-) 43.0

Hungary, New Orders ... (-) 64.7 ... down from (-) 63.1

Netherlands, Employment ... (-) 34.6 ... plunging from (-) 26.1

And, of specific interest, is weakness in the 'Nordics', Sweden and Finland (Construction Sector indexes):

Finland, Confidence ... (-) 19.3 ... down from (-) 7.7 in April

Finland, Employment ... (-) 20.3 ... down from (-) 10.5 in April

Finland, New Orders ... (-) 18.3 ... down from (-) 5.0 in April

Sweden, Confidence ... (-) 18.3 ... down from (-) 2.9 in April

Sweden, New Orders ... (-) 30.4 ... down from (-) 14.9 in April

Sweden, Activity Trend ... (-) 11.9 ... down from + 6.4 in April

And of GREAT interest as it pertains to top-down confidence in the EU, from within, is the data on the Retail Sector. The headline EU Retail Sector Confidence Index slid to a NEW MOVE LOW, at (-) 14.6, falling from (-) 8.5 in April. Moreover, EVERY index fell, except, unfortunately, Inventories, which increased on the back of diminished demand.

We specifically spotlight the decline in the Business Index, which fell to (-) 19.7 in April down from (-) 8.6 in April, along with the slide in Future Orders, which fell to (-) 14.8, from (-) 9.9. And, we note a second straight monthly decline in the EU Retail Employment Index. Carving into the country data, we feature the following points-of-interest, as the EU Retail sector comes under increasingly acute, and broad-based downside pressure:

Spain, Business ... (-) 23.5 ... down from (-) 10.3

France, Future Business ... (-) 12.3 ... down from (-) 2.8

France, Confidence ... (-) 20.3 ... down from (-) 9.4 in April

France, New Orders ... (-) 18.1 ... down from (-) 12.5

Belgium, Confidence ... (-) 16.4 ... down from (-) 12.0

Belgium, Future Business ... (-) 23.2 ... down from (-) 17.9

Italy, Business ... (-) 51.6 ... down from (-) 38.0

Italy, New Orders ... (-) 35.4 ... down from (-) 30.9

Portugal, Business ... (-) 48.7 ... down from (-) 46.2

Hungary, Business ... (-) 10.4 ... down from (-) 1.9

Hungary, New Orders ... (-) 15.5 ... down from (-) 9.5

Austria, Confidence ... (-) 11.0 ... down from (-) 2.0

Lithuania, Confidence ... (-) 12.3 ... down from + 4.8

And, even in Germany, there is more than just 'erosion-in-growth' going on, with an outright CONTRACTION unfolding in the German Retail sector, in synch, timing wise, with the first rise in the Number of Unemployed since 2009, posted last month.

Note the darkening skies over Germany's retailers:

Germany, Confidence ... (-) 13.6 ... down from (-) 3.9

Germany, Business ... (-) 1.9 ... down from + 16.7

Germany, New Orders ... (-) 8.7 ... down from (-) 0.8

Germany, Employment ... (-) 2.7 ... down from + 0.3

The broadening and deepening COLLAPSE in 'confidence' among both business leaders, and consumers ... only serves to exacerbate the bigger-picture risk defined by the potential for a region-wide run on bank deposits. We examined the data in last week's "Smell and Tell" Monitor, and we got updated figures on Wednesday (for the month of April) from the European Central Bank detailing money supply and bank balance sheet figures.

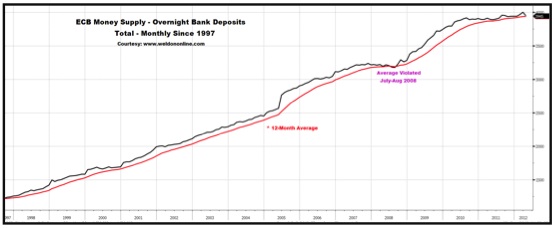

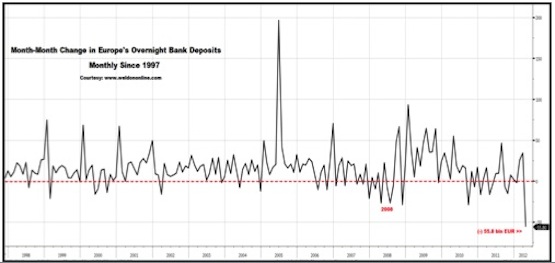

Disturbing for sure, is the fact that the largest component of EU Bank Deposits, Overnight Deposits, deflated in April, and is perilously close to a rare downside violation of the 12-Month Average. See the chart below.

GLARING is the message gleaned from the chart below, in which we plot the month-to-month change in Overnight Bank Deposits ... revealing that April's 'run' (ooops, I mean decline) of (-) 55.8 billion EUR, is the largest single-month contraction in at least the fifteen years.

We cannot help but wonder, in the context of today's top-down theme (a return of the German Mark, instead of the Greek Drachma), might such a move offer some sense of 'confidence' in cementing the belief that the Drachma is NOT coming back, and thus the Peseta, Lira and Franc are not likely to return either ??? ... particularly if removing the German political roadblock allowed the ECB to load up with debt monetization firepower !!!

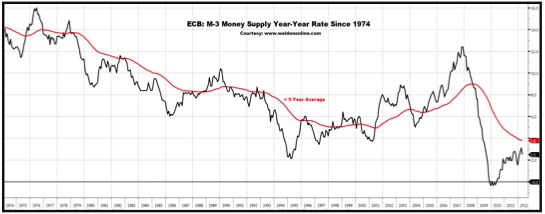

Maybe, and maybe not. Perhaps there would just be a rush out of the watered-down EUR, and into DEM, sparking yet another type of 'crisis'. Unfortunately for all involved, non-action is a KILLER, and this dynamic, as it specifically applies to the ECB, is evidenced by the fact that, thanks largely, though not solely to the historic decline in Overnight Deposits, the three key money supply aggregates, narrow M-1, M-2, and broad M-3 ... ALL ... posted outright contractions in April.

Indeed, broad money M-3 contracted by (-) 51 billion EUR during the month, which drove the year-over-year rate-of-change sharply lower, to +2.5% in April, down from +3.1% in March. Evidence the chart below revealing that the April reversal may mark a post-crisis peak in money growth, particularly if Bank Deposits continue to decline (which they most certainly did, in May).

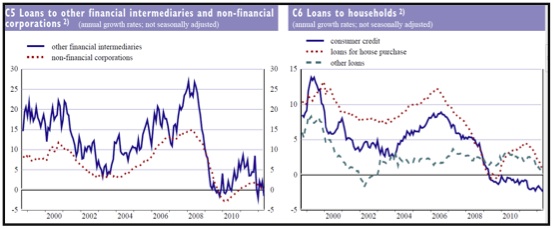

We also focus on the continued push towards intensified deflation in bank lending, with a MASSIVE (-) 49 billion EUR single-month contraction in Loans to Other (private sector) Euro-Area Residents ... with broad based declines in a variety of loan 'types', including Consumer Credit. Consumer Credit fell by (-) 2.0 billion EUR in April, and the year-year rate dumped deeper into overtly negative territory, at (-) 2.4%, down from (-) 2.1% yr-yr in March, and down from (-) 1.9% yr-yr in February. We note the charts below (ECB).

The most important signal offered today by the markets ...

... was that flashed by the German stock market, as per the massive decline in, and technical breakdown by, the DAX.

Evidence the daily chart on display below plotting the nearby continuous DEX futures contract since the 1Q of 2010. We focus on the most recent downside violation of the uptrend line in place since last fall's low ... a move that came in synch with the plunge into outright bearish territory by our med-term Oscillator.

Moreover, we also focus on the negative evolution in the moving average alignment, as the short-term 50-Day EXP-MA crosses below the med-term 100-Day EXP-MA ... and all three, including the long-term 200-Day EXP-MA have completed their own downside reversals, directionally speaking.

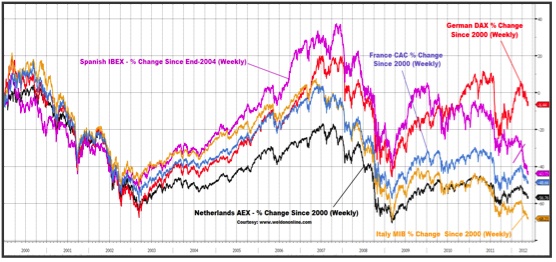

The DAX is ... 'exposed' ... as evidenced in the long-term weekly overlay chart below in which we compare the percentage returns generated by various key EU stock indexes, since the end of 2004. We note that Germany is MOST CLOSELY linked to Spain, and thus the breakdown in Spain is likely more than the DAX can withstand, without cracking wide open itself.

Lest we forget the cold hard fact ... Germany is itself, in VIOLATION of the Union Treaty rules as it applies to their sovereign-debt-to-GDP ratio.

Amid today's violent breakdown in the German DAX, we flash the spotlight on the chart below plotting the 5-Year Sovereign Credit Default Swap linked to Germany's government debt, which totals more than 1.1 trillion EUR.

Simply, Germany's CDS is breaking out to the 'upside', indicating that investor anxiety about a possible DEFAULT on Bunds, BOBLs, and Schatze, is on the rise, as defined by the violation of the downtrend line, and the move back above 100 basis points.

Of course we must take note of this week's move in, and today's close by, the Spanish 5-Year Sovereign Credit Default Swap, which, again, did NOT benefit from chatter related to ECB restarting their asset purchase program, and buying Spanish government debt outright (as Spain would like).

Clearly, the breakout to a NEW ALL-TIME HIGH in the Spanish CDS is NOT a positive sign, and exemplifies the intensified risk of having EU officialdom debating, rather than doing.

The Spanish 5-Year Sovereign Bond yield is probing its crisis high close of 6.29%, and has held above our danger-trigger of 5.50%.

Evidence the chart below, with focus not only on the most recent renewed upside explosion in yield, but also the bearish (higher yield) realignment by the two key med-long-term moving averages, as the med-term 100-Day EXP-MA rises above the long-term 200-Day EXP-MA, while both averages are accelerating to the upside, velocity wise.

Clearly, a move above 6.30% would set off alarm bells.

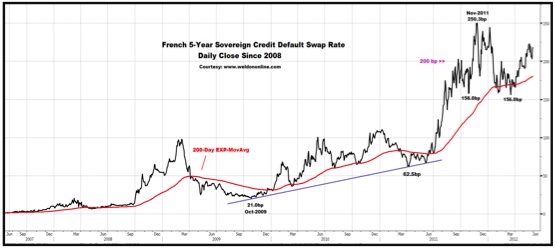

In the next couple of weeks we will be closely monitoring the German DAX, the Spanish 5-Year Bond yield ... among many things ... and, we will be specifically focusing on two instruments in particular, the Credit Default Swaps linked to Italian and French government debt.

First, we look at the 5-Year Italian CDS, seen in the chart below. We note the most recent upside spike, and the renewed directional uptrend in the long-term trend-defining 200-Day EXP-MA.

Clearly, a move above 600 basis points would set off alarm bells.

Similarly, a move above 250 basis points in the French 5-Year Sovereign Credit Default Swap, would set off alarm bells. See the chart below.

Given the recent verbal assault on German leaders, by French, Spanish, and Italian leaders ... might we being to discuss a 'coup' ???

Could it be, that Europe decides to kick Germany out, instead of Greece ???

Okay, maybe it is not that 'dramatic', maybe Germany 'opts out' of the Eurocurrency, like the UK, or Sweden, and brings back the Deutsche Mark, as a way to maintain their own hard-currency policies, while 'freeing-up' the rest of Europe, to pursue debt monetization, and debasement of the new, softer, EUR (ex-Germany). At the very least it would give Germany a choice ... remove your objection to a softer EUR ... or go your own way.

Food for thought.

In the meantime, we remain bearish on European stock indexes, along with the US S+P 500 and German DAX. We continue to focus on the Spanish IBEX, the Euro STOXX-50, the 'Dutch' AEX, the UK FTSE, and the Italian MIB.

We also remain bullish on the US Dollar, with concurrent bearish focus on the Eurocurrency, the Swedish Krona, the British Pound, the Indian Rupee, the Korean Won, the Brazilian Real, the Chilean Peso, the Mexican Peso, the African Rand, and the New Zealand-Australian-and-Canadian Dollars.

We remain bullish on the US and Australian 10-Year Bonds ... and bearish on the Italian 10-Year BTP Bonds.

As for Gold and Silver, recall that we stated on Wednesday ...

"We remain bearish on Gold and Silver, though we are cognizant of the potential for a major low to be 'established' at any time, on the basis of an intensifying debt crisis in the EU, and the possibility of an overt debasement of the EUR.

For sure, we note the triple-bottom pattern in both Gold and Silver, a pattern which has turned into a quadruple-bottom with today's upside reversal from $1532 in August Gold futures ... and ... a pattern defined by the higher low set in Silver. We are tightening our stops."

We are out, and now neutral on Gold and Silver, as things played out today, EXACTLY as we suggested they might.

We remain bearish on Industrial Metals, with focus on Copper, Aluminum, Nickel, Tin, Platinum and Palladium.

And, we remain bearish on select commodities, with focus on Sugar, Cocoa, Cotton, Corn, and Orange Juice.

Gregory T. Weldon

By John F. Mauldin

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2012 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.