Blue-chip Dividend Growth Stocks Today’s Strong Option for Retirement Portfolios Part 2

Companies / Dividends May 24, 2012 - 01:38 AM GMT

In part one of this two-part series (Found Here) I laid the groundwork for why I believe that blue-chip dividend paying US equities represent not only a viable, but also a safer investment choice than many give them credit for. I also pointed out why I believe the risk profile on bonds is currently upside down, arguing that for one of the few times in history they may actually be more dangerous an investment than equities.

In part one of this two-part series (Found Here) I laid the groundwork for why I believe that blue-chip dividend paying US equities represent not only a viable, but also a safer investment choice than many give them credit for. I also pointed out why I believe the risk profile on bonds is currently upside down, arguing that for one of the few times in history they may actually be more dangerous an investment than equities.

This is not normal, and therefore, I believe requires looking at investment choices differently than we traditionally have. I once read a comment from the renowned spiritual leader Dr. Wayne Dyer that summarizes my point quite nicely: "when you change the way you look at things the things you look at change." In today's investment environment I think we need to change the way we look at bonds and simultaneously change the way we look at equities. At least temporarily regarding bonds, until interest rates normalize, which I believe they eventually will. But perhaps we should change the way we look at equities more permanently.

I believe a critical part of changing the way we look at equities is by the recognition that there are wide differences in the safety profile of various equity classes. For example, many highflying non-dividend paying growth stocks tend to carry a lot more risk than more established dividend paying stalwarts. There are many reasons for this that goes beyond just the fact that the latter pays a dividend. On the other hand, the dividend itself is a great mitigator of risk. Maybe the best way to understand this is through a quote attributed to Will Rogers: "I'm not as concerned about the return on my money as I am the return of my money." Every time a company pays you a dividend, you are receiving a return of your money as well as on it. Therefore, with each dividend paid you technically have less money at risk.

Additionally, the legendary investor Ben Graham shared his feelings on the safety of dividend paying stocks when he wrote in the value investor's Bible, The Intelligent Investor in Chapter 11, Security Analysis for the Lay Investor as follows:

"4. Dividend Record. One of the most persuasive test of high quality is an uninterrupted record of dividend payments going back over many years. We think that a record of continuous dividend payments for the last 20 years or more is an important plus factor in the company's quality rating. Indeed the defensive investor might be justified in limiting his purchases to those meeting this test."

Of course it should go without saying, those companies on the prestigious Dividend Champions list of companies that have not only paid a dividend for 25 consecutive years (five more than Ben required), but also increased their dividend every year as well, goes beyond Ben Graham's definition of a quality company. And therefore, since a defensive investor is by definition one that is wary of taking risk, it would only seem logical that dividend paying equities, especially Dividend Champions, possess the safety characteristics they desire, at least according to Ben Graham and yours truly (here is a link to David Fish's list of dividend champions).

My Top 20 Dividend Champions

Before I reveal my favorite Dividend Champions, a few more introductory remarks on this specific equity class, and equities in general, are in order. First and foremost, even though every stock in the prestigious Dividend Champions list shares the characteristic of 25 years of consecutive dividend increases, they are not all the same. In truth, the discerning investor will discover many differences among the characteristics between the individual companies (105 in total) and the overall group. But for purposes of this article, I will concentrate on two primary subsets within the group as I screen for my favorite 20. Then, I will create two top 10 lists for each subset based on the different characteristics that each subset possesses.

The reason I am focusing on these two different classes of Dividend Champions is because they each provide characteristics that best serve the unique needs of dividend growth investors with different goals and objectives. One set will serve the dividend growth investor that is perhaps already retired and seeking maximum current income, while set number two might better serve the dividend growth investor that is near retirement but still has some time to accumulate assets before needing to harvest yield. Therefore, subset one will focus on yield with total return secondarily, and subset two will focus on total return with yield secondarily. Nevertheless, yield on cost, or what I prefer to call growth yield, will be an important attribute of both groups.

Dividend Champions That Were Screened Out

Instead of providing a long list of metrics that I used to eliminate Dividend Champions, I thought it might be more efficient to illustrate it with pictures. I've always felt that utilizing statistical representations from which to make investment decisions is fraught with error. Even though the statistics can be accurate, they can mislead you due to their lack of what I consider to be relevant details. For example, as most readers may know, the Dividend Champions list is comprised of 105 companies that share a vital data set. Each company on this prestigious list possesses a consecutive streak of at least 25 years of dividend increases.

Therefore, on the surface, it would be easy to assume, based on this statistic, that each company on the Dividend Champions list has a consistent long-term record of earnings results. This assumption is logical, because dividends are paid out of earnings. In other words, a consistent and long-term consecutive streak of dividend increases implies steadiness. Here is where the phrase a picture is worth 1000 words really becomes apparent. The following three examples utilizing F.A.S.T. Graphs™ are Dividend Champions that were rejected because of a significant lack of evenness with their operating results.

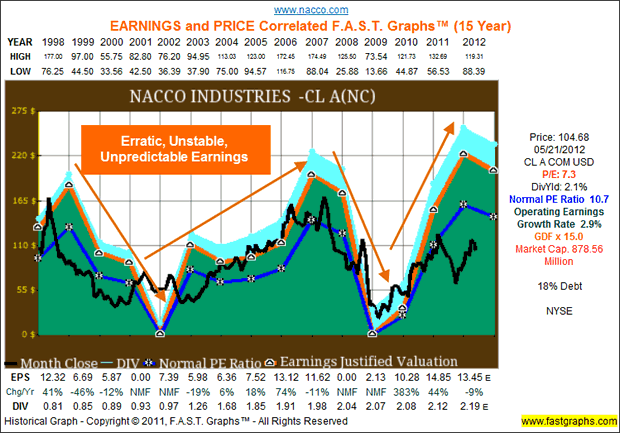

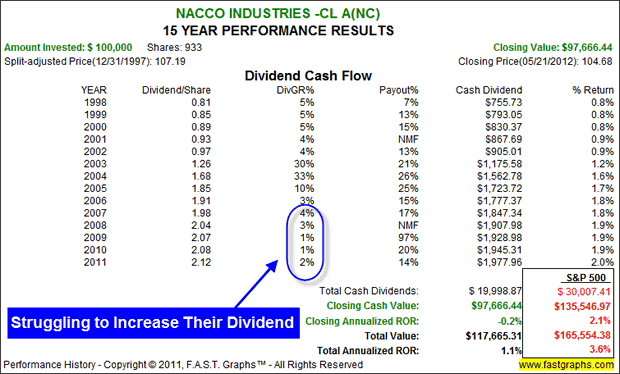

Nacco Industries (NC)

From their website:

"NACCO Industries, Inc. is an operating holding company with subsidiaries in the following principal industries: lift trucks, small appliances, specialty retail and mining."

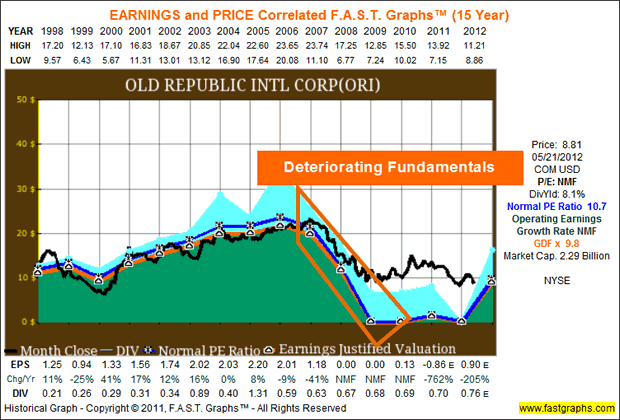

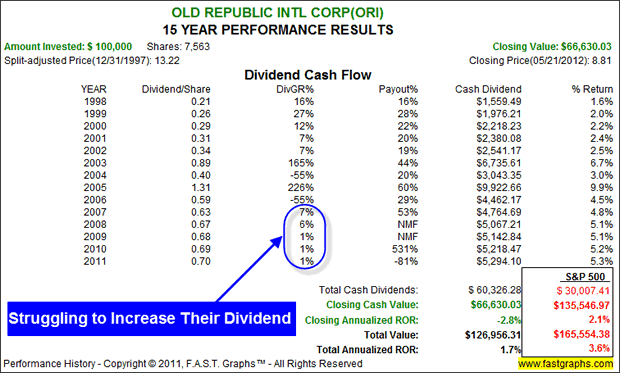

Old Republic International Corp (ORI)

From their website:

"Chicago-based Old Republic International Corporation is one of the nation's 50 largest publicly held insurance organizations. Its most recent financial statements reflect consolidated assets of approximately $16.16 billion and common shareholders' equity of $3.77 billion, or $14.74 per share. Its current stock market valuation is approximately $2.29 billion, or $8.82 per share.

Note: ORI announced a spinoff of subsidiary RFiG along with a leveraged buyout. Therefore, the future prospects of this company may be changing for the better giving it speculative appeal."

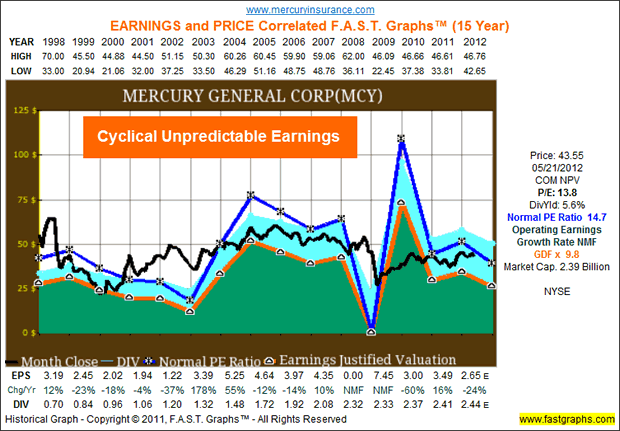

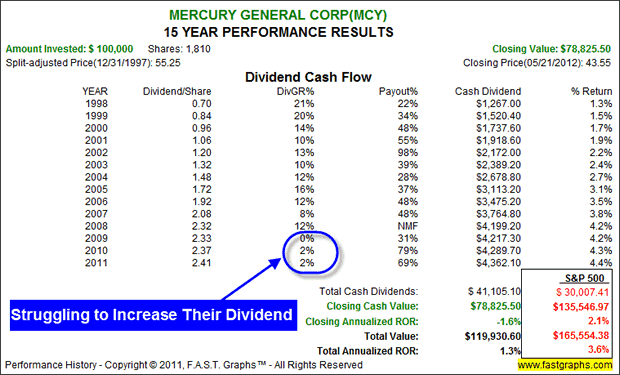

Mercury General Corp (MCY)

From their website:

"Mercury General (NYSE-MCY)is the leading independent broker and agency writer of automobile insurance in California and has been one of the fastest growing automobile insurers in the nation. It is ranked as the third largest private passenger automobile insurer in California, with total assets over $4 billion. Mercury also writes automobile insurance in Arizona, Florida, Georgia, Illinois, Michigan, Nevada, New Jersey, New York, Oklahoma, Pennsylvania, Texas and Virginia. In addition to automobile insurance, Mercury writes other lines of insurance in various states, including mechanical breakdown and homeowners insurance."

Performance and Dividends Impacted By Operating Stress

It should be clear from the above graphs that the earnings records of these three Dividend Champions have been far from steady, consistent or reliable. Therefore, I cannot get comfortable in either recommending them or investing in them because I cannot get comfortable predicting what their future operating results may be. Furthermore, by examining the performance results associated with the above earnings and price correlated graphs illustrates a lot of uncertainty. A focus on the earnings growth rate column illustrates a lot of stress on each company's ability to keep their dividend streaks alive (Blue Circles).

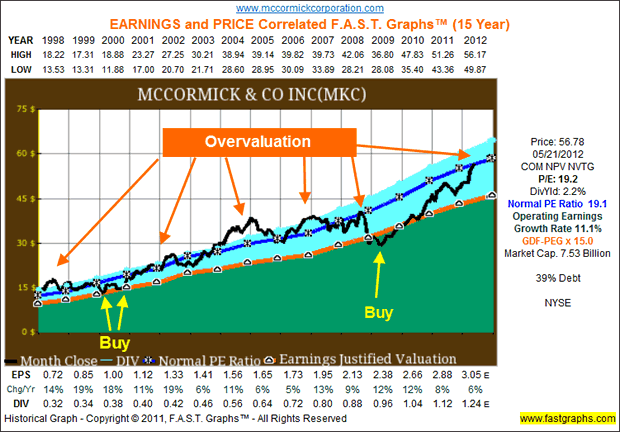

The Overvaluation Rejection

Other reasons besides irregular earnings growth that caused a Dividend Champion to be rejected include one of my all-time favorites, valuation. Or to be more precise - overvaluation. The following example, McCormick & Co. (MKC), represents one of my favorite Dividend Champions based on a very consistent above-average record of earnings growth that produced its impressive dividend streak. The only reason that this Dividend Champion was rejected was because of current overvaluation.

Top 20 Dividend Champions That Made The Cut

Currently, there are 105 Dividend Champions; however, as I've already pointed out, I do not feel that a company should be invested in just because of its dividend streak. There are many other considerations that I think are important. Anyone who's a regular reader of my work will know that current valuation is one of the most important to me. But I also covet an above-average growth rate, both historically, and even more importantly, forecast to continue in the future. The consistency of the company's operating results, regardless of growth rate, is also important. And of course, there is the yield versus total return issue that many dividend growth investors enjoy debating about. There are others, but these are the essential ones to me.

The important point that I am iterating here is that not all equities are the same, and also not all Dividend Champions are the same. But most importantly, the differences between the individual companies can make all the difference in the world regarding whether or not they should be invested in. Sometimes, the differences are temporary, for example, an overvaluation situation that may one day correct itself. In other cases, a permanent deterioration of fundamentals may soon render a current Dividend Champion a dud, and end its streak of dividends.

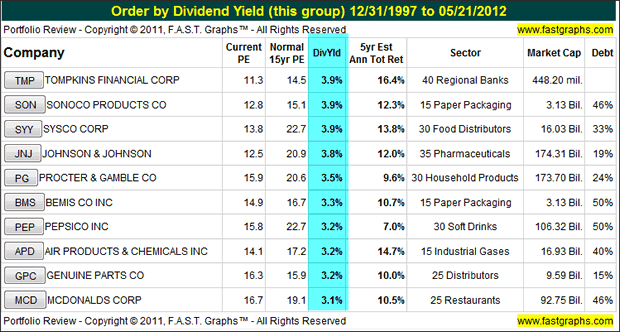

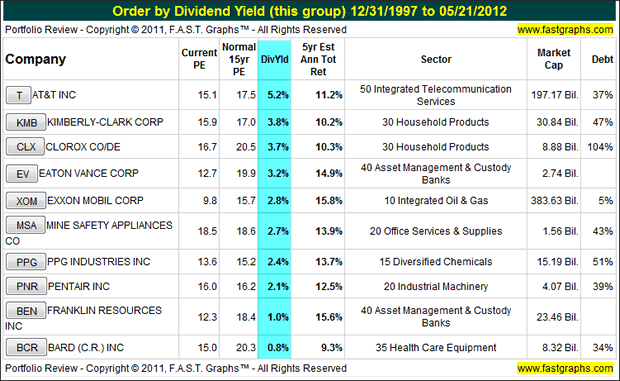

Top 10 Dividend Champions For Yield

This first top 10 list is offered for dividend growth investors that are most focused on current yield. My primary consideration here was a minimum current dividend yield of 3% (greater than the 30-year T-bond). However, I also put a premium on consistency and safety based on the assumption that this investor may already be retired and living off the income of their dividend growth portfolio. Finally, each of these companies had to be fairly valued, and some I would even consider significantly undervalued. Therefore, this list is presented in order of highest dividend yields to lowest.

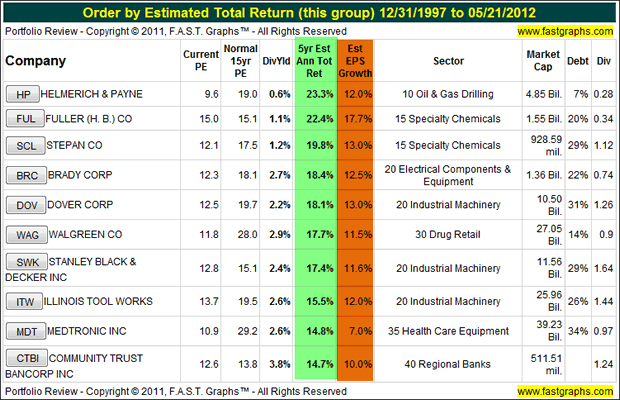

Top 10 Dividend Champions For Total Return

My next top 10 list focuses more on total return than current yield. I offer this list for the dividend growth investor that may still be in the accumulation phase. Although the primary emphasis here is on total return, how it will be accomplished can vary from one company to the next. In some cases, return is a function of above-average expected earnings growth. In other situations very low valuation may be the generator of future return. Or perhaps return will be driven by a combination of both.

Many companies in this group can be identified by the highest estimated five-year earnings growth rates. Others in this group can best be identified by the lowest PE ratios relative to estimated earnings growth. The remainder will be represented by some combination of the above factors.

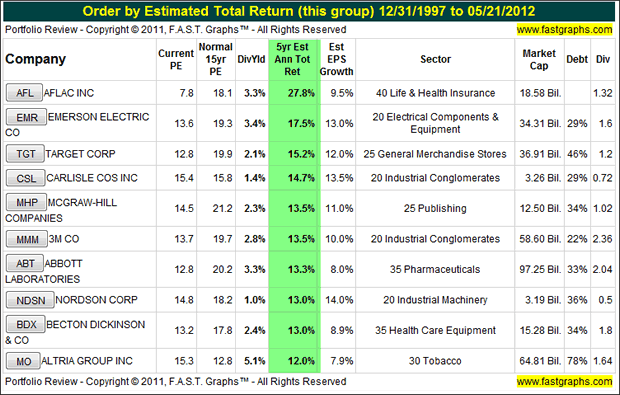

Top 10 Dividend Champions Bonus List

In addition to my top 10 favorite Dividend Champions for total return, and my top 10 Dividend Champions for yield, I will offer two additional lists of 10 each. One I will call my bonus list containing companies that could theoretically make either of the top two favorite lists, total return or yield. My second additional list I will call the honorable mention top 10. This list will contain an additional 10 Dividend Champions that were simply hard to exclude. In other words, although they did not make a favorites list, they each represent solid and attractive candidates that the dividend growth investor might want to consider.

Actually, there are several companies on these lists that qualified for either or both of my favorites lists. For example, Aflac (AFL) and or Emerson Electric (EMR) could easily be on both lists. My point is that I feel the reader should give the same consideration to each of these names as they would the two top 10 lists. To be clear, selecting the top 10 was difficult and therefore to a great extent subjective on my part. My method was to simply run a F.A.S.T. Graphs™ on each Dividend Champion with above-average total return calculations. Then my lists were created by picking and choosing those companies that from my review looked best based on value, earnings and safety.

Top 10 Dividend Champions Honorable Mention

This final list of 10 Dividend Champions I have dubbed as honorable mention candidates. As I suggested with the bonus list, I feel this group also contains attractive candidates for the prudent dividend growth investor to consider.

Summary and Conclusions

When I invest in stocks, I invest in the business not the market. Therefore, I intend to be a shareholder of the business for a very long time. Consequently, I am rarely too concerned about current market volatility because I focus more on the business behind the stock. It's important to remember that in truth you only get real information on the business four times a year, when the company's quarterly announcement is made. Exceptions would be major announcements such as acquisitions, mergers or some other material events that could permanently affect the viability of the business.

As a result, there are only three reasons that would prompt my desire to sell a fine business:

-

If the valuation became too high thereby making the market risk too great to ignore. In this case I would sell and replace with another company offering better value.

-

If I felt that there was a permanent fundamental deterioration in the business prospects of the company.

-

If I came across an exceptional opportunity that was too good to pass over, then I might consider replacing what I perceived to be my current holding with the least potential with the new irresistible opportunity (it should be noted that this opportunity would have to be really extraordinary to cause me to consider such a move).

What I feel I've offered here is a list of 40 Dividend Champions that represent worthy candidates for consideration by the prudent dividend growth investor. Some of the names I offered for their yield, and others I offered for their total return potential. Although I believe that each of the candidates on the various lists represent Dividend Champions that are reasonably priced today, they are not necessarily all cheap. In other words, some are fully valued, some are attractively valued, and some are downright cheap. I leave it to the reader to conduct their own comprehensive due diligence on their own.

However, I do believe that these lists represent an efficient group of prescreened opportunities that are worthy of further consideration. There are other dividend candidates such as Johnson Controls (JCI) and Illinois Tool Works (ITW) that were covered in the previous article Part 1, that do not meet the standard of consecutive dividend increases. Accordingly, I do not consider this a comprehensive or complete list of all possible dividend growth opportunities, but I do consider them a great place to start looking.

Finally, this article is also offered as a follow up to my previous article 43 Dividend Champions On Sale: A Rare Opportunity

Both of these articles and their lists of Dividend Champions are offered as candidates for long-term ownership of the businesses behind the stocks. I have always held that long term is defined as at least a business cycle (3-5 Years Minimum). When I invest in a company, I buy earnings in a company today that I believe will grow into more earnings tomorrow. This is my expected source of greater dividends and capital appreciation from the capitalization of my greater earnings. Not from fickle Mr. Market behavior.

By Chuck Carnevale

Charles (Chuck) C. Carnevale is the creator of F.A.S.T. Graphs™. Chuck is also co-founder of an investment management firm. He has been working in the securities industry since 1970: he has been a partner with a private NYSE member firm, the President of a NASD firm, Vice President and Regional Marketing Director for a major AMEX listed company, and an Associate Vice President and Investment Consulting Services Coordinator for a major NYSE member firm.

Prior to forming his own investment firm, he was a partner in a 30-year-old established registered investment advisory in Tampa, Florida. Chuck holds a Bachelor of Science in Economics and Finance from the University of Tampa. Chuck is a sought-after public speaker who is very passionate about spreading the critical message of prudence in money management. Chuck is a Veteran of the Vietnam War and was awarded both the Bronze Star and the Vietnam Honor Medal.

© 2012 Copyright Charles (Chuck) C. Carnevale - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.