Blue-Chip Dividend Growth Stocks Are Today’s Strong Option For Retirement Portfolios

Companies / Dividends May 18, 2012 - 02:05 AM GMT

There is a confluence of factors that are painting a very odd picture of current investor behavior. Common sense and a careful analysis of the market dynamics between equities and bonds today would indicate that investors should be acting in the exact opposite manner than they are. Interest rates are hovering at a 100-year low, which creates two problems for investors. First, there is not enough return from bonds to fund a retiree’s income needs or to fight inflation. Second, investing in bonds with interest rates so low makes it riskier to own bonds today than it has been in over a century.

There is a confluence of factors that are painting a very odd picture of current investor behavior. Common sense and a careful analysis of the market dynamics between equities and bonds today would indicate that investors should be acting in the exact opposite manner than they are. Interest rates are hovering at a 100-year low, which creates two problems for investors. First, there is not enough return from bonds to fund a retiree’s income needs or to fight inflation. Second, investing in bonds with interest rates so low makes it riskier to own bonds today than it has been in over a century.

Conversely, many US equities, especially blue-chip dividend paying equities with long histories of paying and increasing their dividends are at historically low valuations, and therefore, offering historically above-average current yields. Furthermore, high-quality blue-chip US corporations are perhaps in better financial health than we’ve seen in decades. Consequently, low valuation and healthy corporate financials would indicate that quality equities offer lower real levels of risk and higher long-term returns than they have in decades.

Nevertheless, investors are not only making a classic mistake, I believe they are making a very obvious and thus quite avoidable mistake. It is an undeniable fact that bond prices go down when interest rates go up. Since interest rates cannot go to zero or below, it logically follows that interest rates have nowhere to go over the long term but up. Perhaps, as many believe, federal intervention may keep rates low for another year or so. But in the longer run, the powerful forces of the market can only be contained for so long.

Yet given what I’ve already said, we continue to see that bond mutual fund inflows remain at a record high, while simultaneously equity fund outflows are some of the largest on record. In other words, investors are selling stocks, the undervalued out-of-favor asset class and investing into the most overvalued asset class - U.S. Treasury bonds. I believe that people are forgetting that bond prices can fluctuate just like stocks. And with interest rates at such an extreme low level, bond price fluctuations could be more severe than equities have been even during their worst days.

The Evident Risk Profile of Bonds

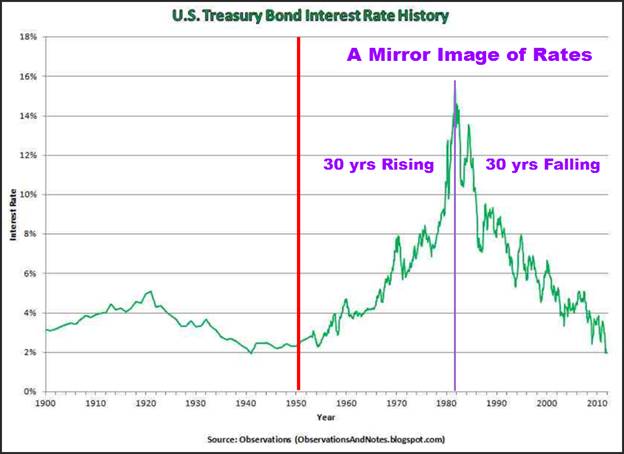

In searching the Internet for a long-term graphic on 10-year U.S. Treasury notes I came across the following 110-year chart courtesy of the financial blog Observations. Although the chart from 1950 through 2010 illustrates a clear mirror image of interest-rate behavior, the portion going back to 1900 is even more illuminating. This is not statistical mumbo-jumbo showing correlation without causation, this is a factual depiction of interest rates spanning over 110 years. This casts a bright light on the risk of bonds to anyone that understands the interest rate and bond price relationship. Rates clearly have nowhere to go but up long term, and when they do, prices of existing bonds will collapse. To be clear, I didn’t say drop, I said collapse. Bond buyers beware.

To summarize, the only rational reason that people are eschewing stocks in favor of bonds is fear. The precipitous drop in stock prices during the great recession has yet to be forgotten. On the other hand, what is forgotten is the fact that the same thing can happen to bonds as well. Therefore, I believe the irrationally exuberant confidence in bonds is ill-gotten. The only reason bond prices haven’t fallen in 30 years is because interest rates have been falling since the early 1980s. When interest rates fall, bond prices go up and therefore an even greater aura of safety surrounds bonds. Keep in mind; although prices on pre-issued bonds will go to a premium as interest rates are falling, the premium vanishes at maturity.

Furthermore, at maturity, investors are forced to reinvest in new bonds at lower rates than they had on the existing bonds that matured. Regardless, stability with bond values makes people feel good. This was not true from 1950 to the early 1980s. When interest rates are rising, holders of existing bonds will see their principal devastated. Consequently, they will have less capital available to invest in the new and higher interest rates when they occur. As a result, even though rates go higher, investors will fail to take advantage of it because they will have less money to invest.

The Case for Blue-chip Dividend Paying Stocks

One of the biggest misconceptions that I believe people erroneously hold regarding equities is the notion that all equities are the same. In truth, equities come in many different flavors, some good and some not so good, therefore, to paint all equities with the same brush stroke is both misleading and unfair. This is why I so vehemently argue against evaluating and even making investment decisions based on generalities like “the stock market is high or the stock market is low.” Instead, I believe in evaluating each specific holding that I might consider thus making my decisions on a case-by-case and I feel more rational basis.

Additionally, there are several facts regarding the long-term ownership of quality dividend paying equities that many people either overlook or forget. But perhaps the most important fact is that any of the damage that the great recession caused was only temporary in nature for the prudent and intelligently patient investor. The prudent investor is defined as one who in the first place, was careful to only invest in blue-chip equities when valuations made sense. This is especially true for the best-of-breed blue chips that continued to generate strong earnings during the recession and consequently raised their dividends. Inevitably, the stock prices on quality companies whose earnings held up eventually return to fair value.

It’s true that generally speaking, their stock prices did drop along with most other stocks, but because their businesses remained strong and healthy their stock prices did recover, and as I already stated, the income that they generated never faltered. In other words, as long as the stocks were not panic sold out into price weakness, existing shareholders soon recovered their temporary losses while continuing to enjoy a steadily growing dividend income stream along the way. As I also stated before, it’s not the volatility itself that represents risk, but rather the emotional reaction to volatility which is where the real risk sits.

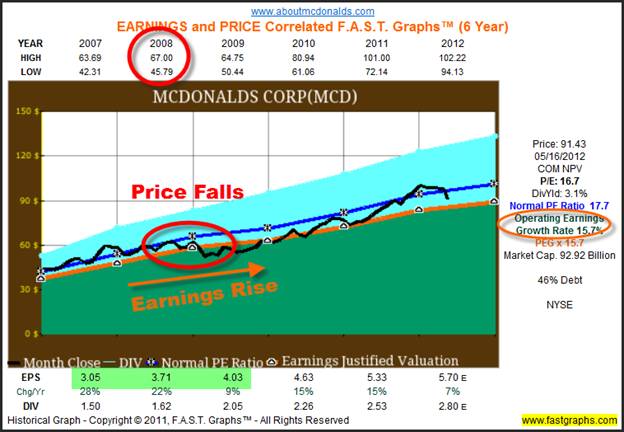

Two classic examples of what I’m describing thus far can be found by examining the businesses behind McDonald’s Corp. (MCD) and Kimberly-Clark Corp (KMB) in conjunction with how the marketplace treated their stock prices during the great recession. I will utilize the F.A.S.T. Graphs™ (fundamentals analyzer software tool) to vividly illustrate my points. To focus the reader, my points are that even a catastrophic event such as the great recession of 2008, did not have a permanent long-term effect on best-of-breed companies that were able to maintain their businesses in spite of the economic challenges.

McDonald’s Corp. During the Recessionary Years

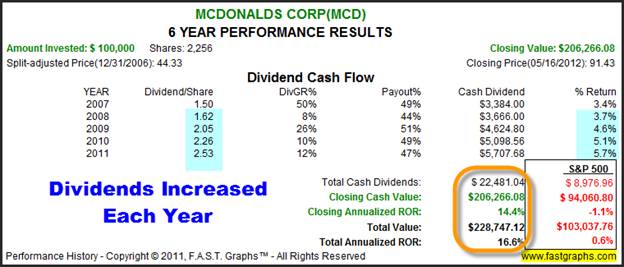

My first example, McDonald’s Corp., represents a Dividend Champion and Dividend Aristocrat blue-chip with a consistent, above average and clearly recession-resistant track record of earnings and dividend growth. Nevertheless, the stock price of McDonald’s shares did fall from a high of 67 to a low of $45.79 in calendar year 2008, but quickly recovered back to $64.75 by year-end 2009, and continued on to its current price in excess of $91 per share.

Even more interestingly, McDonald’s was very generous to their shareholders during and coming out of the great recession with large dividend increases. My point being, that as long as McDonald’s shareholders didn’t panic because of the pessimistic stock market behavior, they ended up being richly rewarded for their confidence and rational behavior.

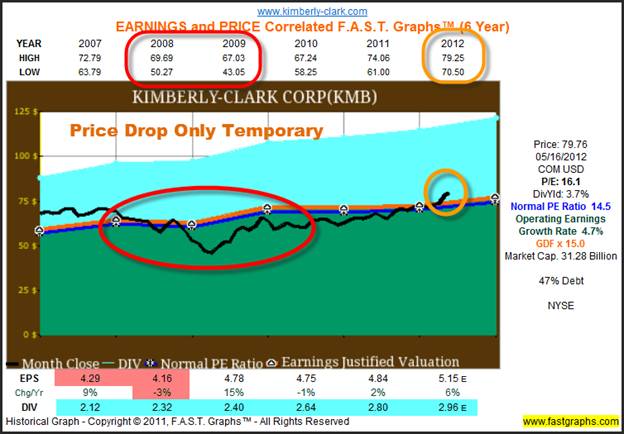

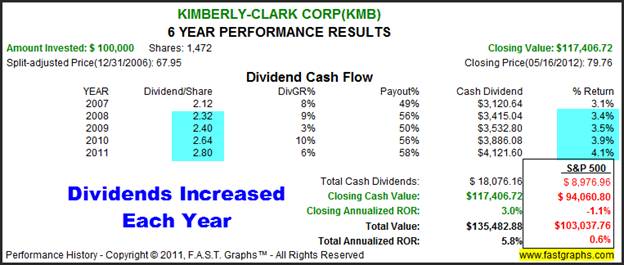

Kimberly-Clark During The Recessionary Years

With my second example, I chose a high-quality blue-chip that also had a consistent record of earnings and dividend growth, however, at not nearly the same rate as McDonald’s achieved. Furthermore, Kimberly-Clark did experience a very minor drop in earnings during the recession which led to a more precipitous, but temporary drop in their stock price. Once again, we see that the stock price recovered in short order with little long-term damage to shareholders, especially those that only purchased Kimberly-Clark when the price was aligned with its earnings justified valuation.

Just as we saw with McDonald’s, Kimberly-Clark shareholders enjoyed a rising dividend income stream right through the great recession. Although Kimberly-Clark does not grow as fast as McDonald’s, it is clearly a quality blue-chip holding that is also a Dividend Champion and Dividend Aristocrat (for those that are not aware this means that the company has increased its dividend for at least 25 straight years in a row).

A Fascinating and Unexpected Lesson Learned From The Great Recession

Up to this point, I’ve been building a case that there are many quality Dividend Champions and Dividend Aristocrats that from a business perspective weathered the great recession in fine fashion. Nevertheless, this did not protect their shareholders from a precipitous, albeit temporary, drop in stock price. Consequently, I have personally intended to covet companies that were able to maintain a high level of earnings strength even during challenging economic circumstances, like recessions.

As I have contended in this article, and others, as long as solid operating results remain intact, then I believe that shareholders have little to worry about except fear itself. Stock price volatility is often more a function of the emotional response than it is the rational response in the short run. However, in the longer run, I have long believed that dialectic thinking will prevail and rational behavior will follow. In other words, I was confident that stock prices will inevitably return to their fundamentally justified valuations. But interestingly, the recent recession may have taught this old dog a few new tricks.

As I was reviewing the performance of quality dividend paying companies post recession, I came across a startling fact that is, partially at least, counterintuitive to what I have long believed. I discovered that quality companies that experienced a sharp drop in earnings during the recession that soon returned to normal profitability actually outperformed the steady eddies like McDonald’s and Kimberly-Clark, etc. However, I still believe that this outperformance is accomplished within a much higher level of risk. Nevertheless, the principle that stock price will inevitably track earnings justified valuations remains intact.

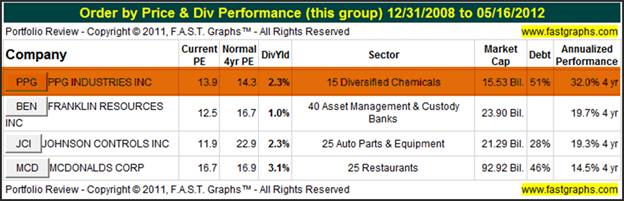

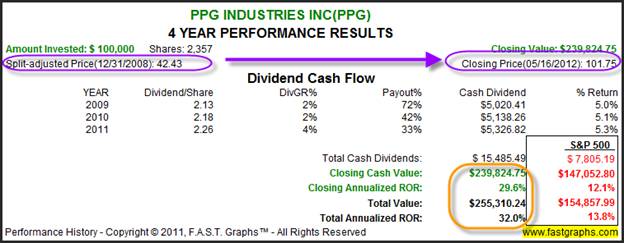

The following table reviews three high-quality blue chips that experienced a temporary, but very sharp drop in earnings during the great recession of 2008. McDonald’s Corp. has been added to the list to provide a benchmark of performance. Note by reviewing the far right column that each of these three examples significantly outperformed the more consistent McDonald’s Corp. over the time frame 12/31/ 2008 to 5/16/2012. In the case of PPG Industries Inc. (PPG), the outperformance is rather startling, and is more than double the annual rate of return of McDonald’s.

PPG Industries Inc. - The Power of an Earnings Recovery

Personally, I believe it is unwise to underestimate the power and protection available from investing in established US Corporation like PPG Industries Inc. The following brief history of the company taken directly from their website validates my thesis:

“Company History – PPG Industries’ vision is to continue to be the world’s leading coatings and specialty products company. Through leadership in innovation, sustainability and color, PPG helps customers in industrial, transportation, consumer products, and construction markets and after market to enhance more surfaces in more ways than does any other company.

Founded in 1883, PPG has global headquarters in Pittsburgh and operates in more than 60 countries around the world. Sales in 2011 were $14.9 billion. Our success is driven by a tradition of well-regarded product and process technology, management and ethical standards. Join us for a look back on more than 125 years of breakthrough ideas and transforming innovations.”

Once again, I will turn to the F.A.S.T. Graphs™ (fundamentals analyzer software tool) to illustrate the opportunity within a temporary interruption in the operating results of a quality established blue-chip US corporation. The point of this exercise is to establish the realization that it’s not a good idea to underestimate the power and value of an established US corporation. As the legendary Warren Buffett so eloquently once put it: “fear is the foe of the faddist, but the friend of the fundamentalist.”

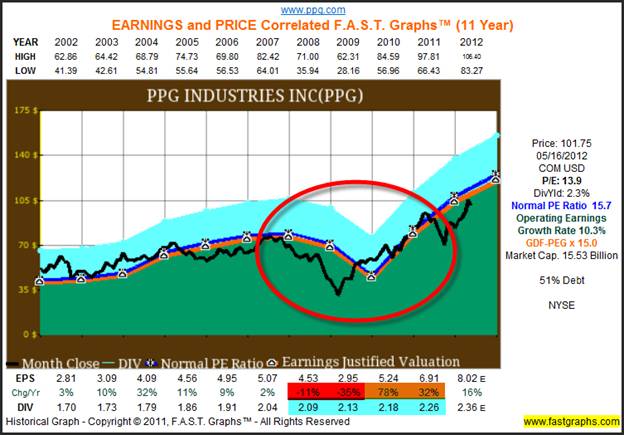

Although PPG Industries remained a profitable company even during the throes of the great recession, as you can see by the graph below the company has experienced two years in a row of falling earnings. Nevertheless, even though their earnings and price both fell, the company did manage to moderately increase its dividend each year. But the real focal point of the following graph is that you can’t keep a good company down. Notice how the company flexed its operating muscle as earnings sharply rebounded (increasing 78% off of a low base – orange shading).

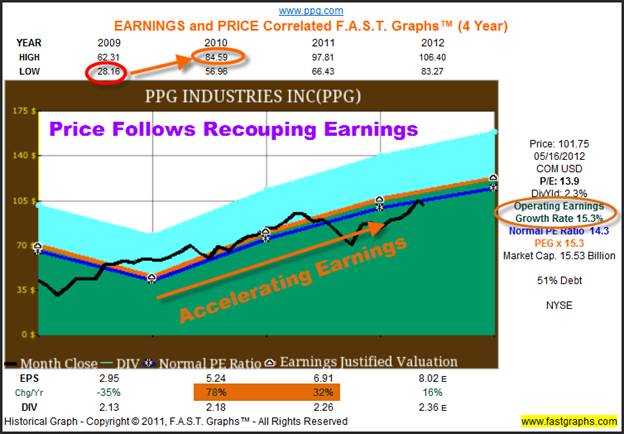

Consequently, the years 2010 and 2011 represented years where the company announced staggering growth rates in their earnings per share. And, as I’ve already pointed out, even though these growth rates were coming off of a low base, the market responded with a rapidly recovering stock value.

The following graph focuses on the low price of $20.16 in 2009 that resulted in a 55% drop from its high of $62.31. Clearly, such a price drop would unnerve many investors, especially those without a strong foundation of understanding the business. Sadly, this would have caused many shareholders to become panic stricken and thus sell at precisely the time when they should have been adding to their position.

The reader should note that the following performance calculation is based on the closing price on 12/31/2008 of $42.43. The price did fall approximately another 30% to $28.16 before it started to recover. Therefore, the annualized compound rate of return of 32% per annum is not measured from its lowest price. In other words, the courageous and perhaps brilliant (lucky) investor would have had an opportunity to generate an even higher return off of all-time lows.

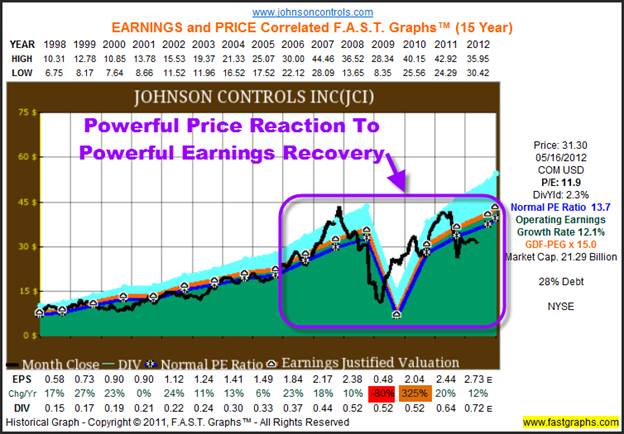

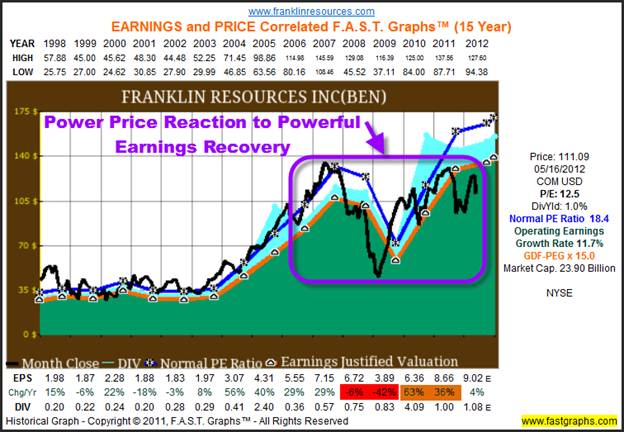

The following two graphs review Johnson Controls (JCI) and Franklin Resources Inc. (BEN) and illustrates the same phenomenon of powerful price advances stimulated by the recovering earnings of blue-chip companies. Once again illustrating that the greatest risk of volatile stock prices from quality US companies, even those with a temporary drop in earnings, lies within the reaction to volatility more than the volatility itself. In other words, fear is riskier than the business cycle.

Summary and Conclusions

There are many pundits and prognosticators that never weary of attempting to convince investors on how risky it is to invest in equities, even high-quality dividend blue-chip paying equities. Invariably, they will always point to volatility as the evidence supporting their thesis that stocks are too risky of an investment for retirees. Personally, I believe this is a great travesty that is prominently promogulated upon an unwary investing public. Hopefully, it is more out of ignorance of the true facts than it is by bad intentions. The inevitable interruptions in the business cycle have conditioned people into believing that stocks are riskier than they really are, at least in my opinion.

Furthermore, I believe that it’s important that investors understand that portfolios cannot be managed for Armageddon. If the world economies are truly coming to an end, as many would like us to believe, then frankly there is absolutely nothing we can do to protect ourselves. If our greatest corporations were to all go bankrupt in one fell swoop, there would be no sanctuary to be found. Bonds would be no good, real estate would be no good, gold would be no good because there would be nothing that we could buy with any of. Under that scenario, the only things of value would be a well-fortified bunker full of food and water, and enough ammunition to fend off the starving hordes that would be trying to take away from us. Not an existence that I would be too interested in.

Therefore, I contend that a much more rational approach is to build portfolios that are based on successful outcomes. Common stocks represent ownership in not only our greatest corporations, but also our very economy itself. Frankly, most of our great corporations will more likely than not be in existence long after most of us are gone. Accordingly, I feel that it is rather foolish to be afraid to invest in them, especially when they can be bought at attractive valuations. This is true even when, and perhaps especially when those attractive valuations are the result of a temporary economic crisis. I don’t believe it’s a sound strategy to sell our country, our economy, or our great corporations short.

In part two of this series I will present and review a list of Dividend Champions that I believe are currently on sale. The second part of this series will represent a follow-up and update to my previous article: Dividend Champions a Rare Undervalued Opportunity

As I have discussed in this article and many previous articles, I believe investors should behave according to the advice of legendary hockey star Wayne Gretzky who taught us “I skate to where the puck is going to be, not where it has been.” In that vein, I believe that tomorrow successful investors will follow Wayne Gretzky’s lead.

For the past several decades bonds have been a great refuge of safety and attractive return, especially for the investor desirous of income. But I believe a careful examination of the 110-year-old 10-year Treasury bond history presented in this article indicates that that is about to change. Conversely, I believe the future for US based dividend paying equities is quite bright. At least that is where I recommend skating in today’s investment environment.

Disclosure: Long MCD, KMB and JCI at the time of writing.By Chuck Carnevale

Charles (Chuck) C. Carnevale is the creator of F.A.S.T. Graphs™. Chuck is also co-founder of an investment management firm. He has been working in the securities industry since 1970: he has been a partner with a private NYSE member firm, the President of a NASD firm, Vice President and Regional Marketing Director for a major AMEX listed company, and an Associate Vice President and Investment Consulting Services Coordinator for a major NYSE member firm.

Prior to forming his own investment firm, he was a partner in a 30-year-old established registered investment advisory in Tampa, Florida. Chuck holds a Bachelor of Science in Economics and Finance from the University of Tampa. Chuck is a sought-after public speaker who is very passionate about spreading the critical message of prudence in money management. Chuck is a Veteran of the Vietnam War and was awarded both the Bronze Star and the Vietnam Honor Medal.

© 2012 Copyright Charles (Chuck) C. Carnevale - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.