Don't End the Fed, Mend the Fed

Politics / Central Banks Apr 30, 2012 - 11:17 AM GMTBy: Paul_L_Kasriel

Congressman Ron Paul has written a book entitled End the Fed. I have to admit that I have not read his book. But I have read many of Congressman Paul's excellent (in my opinion) essays on monetary theory and policy. Based on the essays I have read, Congressman Paul likely argues in End the Fed that the Fed and other central banks have created monetary "mischief" in the past and are likely to continue to do so in the future. Because of this monetary mischief, I assume that Congressman Paul would like to replace the Fed and other central banks with some form of a gold standard.

Congressman Ron Paul has written a book entitled End the Fed. I have to admit that I have not read his book. But I have read many of Congressman Paul's excellent (in my opinion) essays on monetary theory and policy. Based on the essays I have read, Congressman Paul likely argues in End the Fed that the Fed and other central banks have created monetary "mischief" in the past and are likely to continue to do so in the future. Because of this monetary mischief, I assume that Congressman Paul would like to replace the Fed and other central banks with some form of a gold standard.

I share Congressman Paul's sentiments. But I am no Don Quixote. Although the return to a gold standard for our monetary system has much appeal, it is unlikely to occur. So, let's not let the perfect be the enemy of the good. Perhaps there is second-best monetary policy approach to the gold standard that might achieve most of the desirable outcomes of a gold standard but might have a greater probability of actually being adopted. Such an approach is what I am proposing in my final Northern Trust "Econtrarian" (but perhaps not my final Econtrarian). My suggested approach is very similar to one advocated by Milton Friedman at least 60 years ago. The more things change, the more they stay the same, I guess. I am proposing that the Federal Reserve target and control growth in the sum of credit created by private monetary financial institutions (commercial banks, S&Ls and credit unions) and the credit created by the Fed itself. I believe that this approach to monetary policy would reduce the amplitude of business cycles, would prevent sustained rapid increases in the prices of goods/services and would prevent asset-price bubbles of the magnitude of the recent NASDAQ and housing experiences.

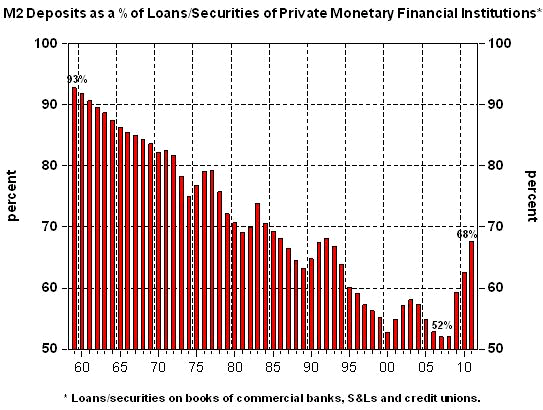

Milton Friedman, the father of modern monetarism, advocated that the Federal Reserve should abandon its obsession with control of the price of credit, i.e., the interest rate, but rather should concentrate on controlling the quantity of money. Friedman's definition of money was currency held by the public and the liabilities of depository institutions (e.g., commercial banks, S&Ls and credit unions) that were redeemable at par and were redeemable on demand, or with a relatively short waiting period. Friedman's definition of money is closely related to what today is defined as the M2 money supply. Fifty years ago, Friedman's proposal and mine were very similar inasmuch as M2-type deposits represented over 90% of the loans and securities on the books of private monetary financial institutions. As shown in Chart 1, by 2007, however, this percentage had dropped to 52, rising back to only 68 in 2011 in the aftermath of the financial crisis. Since 1959, private monetary financial institutions have steadily changed the composition of their funding away from M2-type deposits.

Chart 1

Although my proposal for how the Fed should conduct monetary policy is similar to Friedman's in that the Fed should concentrate on quantities rather than the price of credit, the genesis of my proposal is more aligned with the Austrian school of monetary theory than the monetarist. (I personally, do not believe that there is that much difference between the Austrians and the monetarists when it comes to monetary theory, but if you disagree in a disagreeable manner, send your flaming emails to plk1@ntrs.com.) The Austrians separated credit into two categories, created credit and transfer credit. Created credit is credit that figuratively is created out of "thin air." When credit is created out of thin air, the recipient of this credit can increase his/her spending while no other entity in the economy needs to cut back on its current spending. Thus, under most circumstances, when there is an increase in thin air or created credit, there will generally be a net increase in nominal aggregate spending in the economy. In contrast, transfer credit arises from the ultimate grantor of credit curtailing his/her current spending relative to his/her current income and transferring purchasing power to another entity that has a greater urgency to spend currently than does the grantor. Thus, when there is an increase in transfer credit there is not a net increase in nominal aggregate spending in the economy, but rather a change in the composition of spending. The grantor of transfer credit curtails his/her current spending; the recipient of transfer credit increases his/her current spending. The credit issued by the Fed and private monetary financial institutions is of the created variety, i.e., created figuratively out of thin air.

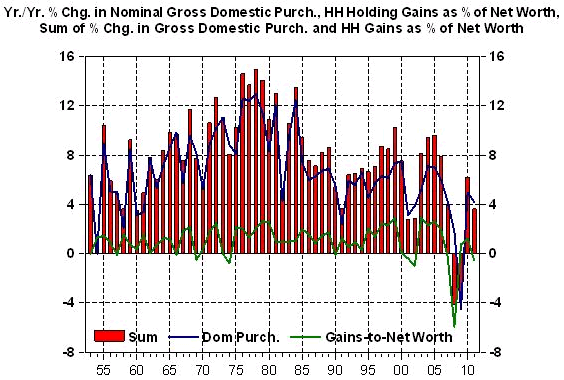

As mentioned above, an increase in "thin air" credit will generally result in a net increase in nominal aggregate spending - nominal spending on currently-produced goods/services and/or existing assets, be they physical assets or financial instruments. Depending on supply conditions, this increased spending resulting from the increased thin air credit can lead to an increase in the current production of goods/services, an increase in the prices of currently-produced goods/services, an increase in the prices of existing assets or some combination of these outcomes. Nominal gross domestic purchases measures the nominal expenditures on currently-produced goods and services by domestic households, businesses and governments. Some of these goods/services are produced domestically; some are imported. A change in nominal gross domestic purchases represents a change in the prices of and/or real quantities purchased of currently-produced goods and services.

An increase in thin air credit might result in an increase in nominal expenditures on existing assets. An increase in expenditures on something existing and, therefore, something whose supply is fixed, must, by definition, imply an increase in the price of that something. One way to measure these price increases on existing assets is to calculate households' holding gains on assets.

In order to capture the effects of changes in thin air credit, I have created a series that is the sum of the year-over-year percent change in nominal gross domestic purchases and households' holding gains on assets as a percent of household net worth. Shown in Chart 2 is this sum along with its components from 1953 through 2011.

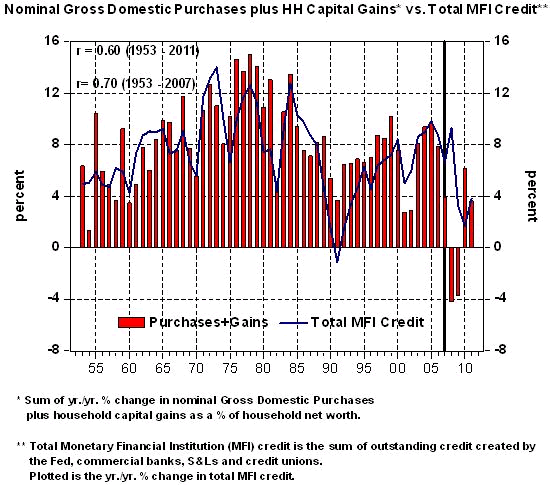

Chart 3 shows the relationship between growth in total monetary financial institution credit (Fed credit plus private monetary financial institution credit) and the sum of growth in gross domestic purchases and households' holding gains on assets as a percent of household net worth. The correlation between the two series from 1953 through 2007, before the onset of the recent financial crisis, is 0.70 out of maximum possible 1.00. Thus, during this period, changes in total MFI credit appear to "explain" a large proportion of the behavior of changes in nominal domestic expenditures on currently-produced goods/services and the behavior of changes in the prices of existing assets. The correlation coefficient declines to 0.60 when the period is extended to include that of the recent financial crisis.

My hypothesis as to why the correlation between changes in total MFI credit and growth in nominal domestic expenditures plus capital gains declines after 2007 is that recipients of Federal Reserve credit that was created in 2008 and 2009 chose to hold a large amount of the funds obtained from the Fed as deposits rather than relending them to some other entity or spending them. As shown in Chart 4, growth in total deposits at private monetary financial institutions did not fall commensurate with the slower growth/contraction in private MFI credit in 2008 and 2009. In those years, had it not been for large increases in the Fed's balance sheet, growth in total MFI credit would have been weaker, resembling that of the growth/contraction in private MFI credit. For example, if the Fed purchases securities in the open market from the nonbank public, all else the same, there will be a net increase in total deposits in the economy - the deposits of the seller of securities to the Fed. Under normal circumstances, the seller of these securities to the Fed would then lend these deposits to some other entity that desired to increase its current spending. But in times of increased economic and financial stress, as what occurred in 2009, the seller of securities to the Fed might choose to simply hold on to the deposits rather than lending them or spending them. In this case, there could be an increase in total MFI credit emanating from the Fed, but no commensurate increase in nominal aggregate spending in the economy.

So, we have learned that there is a high correlation between behavior of total MFI credit and nominal aggregate domestic spending, including holding gains on household assets. Thus, it appears that the behavior of total MFI credit plays a critical role in determining the cyclical behavior of the economy and in determining the asset-price inflation. If the Fed were to stabilize the growth in total MFI credit at some relatively low rate, there is high probability that the amplitude of business cycles would be damped, that the rapid increases in the prices of goods/service as experienced in the 1970s could be avoided in the future and that the magnitude of the asset-price bubbles as experienced during the Greenspan-Fed era also could be avoided in the future. If severe asset-price bubbles could be avoided, then there is a high probability that financial crises such as we recently experienced could be avoided.

What would be the appropriate annual rate of growth in total MFI credit? The answer to this is above my pay grade. Austrians might argue that the proper rate of growth in total MFI credit is zero, or perhaps, the rate of growth in the population. Others might argue that the proper rate of growth in total MFI credit is the potential real rate of growth in the economy, whatever that is. Over the past 59 years, the median annual rate of growth in total MFI credit was 7.3%. I would argue that this is too high if goods/service-price and asset-price inflation is to be avoided. But again, achieving a steady rate of growth in total MFI credit is as important as determining the correct rate of growth.

I would suggest to Congressman Paul that he stop wasting his time trying to end the Fed. Rather, he should sponsor legislation that would specify a single mandate for Federal Reserve policy - achieving a steady and low rate of growth in total MFI credit. If the Fed were to successfully execute this policy, it might not produce economic outcomes as good as a gold standard would, but I believe it would produce economic outcomes considerably better than what has occurred since the early 1970s.

In closing, I want to thank the stockholders and senior management of the Northern Trust Company for allowing me to write these commentaries over the past 25 years. I hope that the readers learned a fraction of the macroeconomics that I learned in writing them.

That's all folks.

Post-April 30 email: Econtrarian@gmail.com

Paul Kasriel is the recipient of the 2006 Lawrence R. Klein Award for Blue Chip Forecasting Accuracy

by Paul Kasriel

The Northern Trust Company

Economic Research Department - Daily Global Commentary

Copyright © 2011 Paul Kasriel

Paul joined the economic research unit of The Northern Trust Company in 1986 as Vice President and Economist, being named Senior Vice President and Director of Economic Research in 2000. His economic and interest rate forecasts are used both internally and by clients. The accuracy of the Economic Research Department's forecasts has consistently been highly-ranked in the Blue Chip survey of about 50 forecasters over the years. To that point, Paul received the prestigious 2006 Lawrence R. Klein Award for having the most accurate economic forecast among the Blue Chip survey participants for the years 2002 through 2005.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

Paul L. Kasriel Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.