Gold Stocks Where Is The Bottom?

Commodities / Gold & Silver Stocks Apr 25, 2012 - 04:38 AM GMTBy: Ron_Hera

Gold and silver mining stocks have sold off by roughly 30% from their 52-week highs based on the PHLX Gold/Silver Sector Index (XAU) and by roughly 32% based on the Amex Gold Bugs Index (HUI). In comparison, gold is down approximately 14% from its nominal all time high in 2011 while silver is down approximately 37%.

Gold and silver mining stocks have sold off by roughly 30% from their 52-week highs based on the PHLX Gold/Silver Sector Index (XAU) and by roughly 32% based on the Amex Gold Bugs Index (HUI). In comparison, gold is down approximately 14% from its nominal all time high in 2011 while silver is down approximately 37%.

The XAU / Gold ratio suggests that gold and silver miners are oversold. In fact, the shares of some companies are trading below their net asset values.

Metal Price Trends

Despite having come down from their 2011 highs, gold and silver prices have shown stubborn resistance below $1650 for gold and below $30 for silver. When prices have broken through these levels, the metals have rebounded. Unlike the breakdown in gold and silver prices after the 1980 mania, gold and silver prices are currently stabilizing at lower levels.

Although prices remain volatile from day to day, current prices appear to reflect a trading range that suggests a consolidation.

Adjusting the Price of Gold

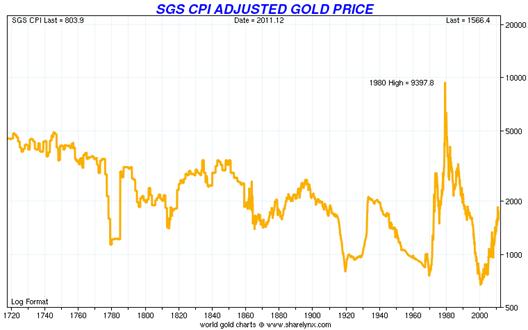

Adjusted using the current U.S. Bureau of Labor Statistics (BLS) Consumer Price Index (CPI), the 2011 highs in gold and silver prices appear similar to the bubble of 1980, but the BLS has changed the way that the CPI is calculated since 1980.

Based on the 1980 formulation of the CPI, which is still calculated by economist John Williams of Shadow Government Statistics, gold and silver prices do not appear to have been in a bubble in 2011.

In addition to changes in the calculation of CPI since 1980, the Federal Reserve’s funds rate is currently close to 0% rather than the 1980 average of 13.36% and the Federal Reserve cannot realistically raise rates in the face of weak economic fundamentals, overleveraged banks and excessive debt levels. Unlike the 1980s, the world reserve currency status of the U.S. dollar is slowly deteriorating and the future of the Euro, which was introduced in 1999, is unclear.

Prices Measured in What?

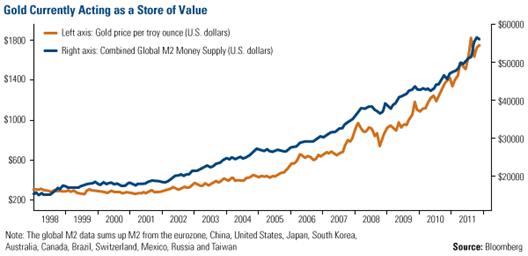

Artificially low interest rates, government deficit spending and quantitative easing by central banks, e.g., the Federal Reserve’s central bank liquidity swap lines and the European Central Bank’s (ECB) Long Term Refinancing Operation (LTRO), expand the money supply independent of sustainable economic activity and population growth. When the money supply expands in a disproportionate way, the value of money falls and prices rise as a result, i.e., because of currency debasement.

Currency debasement will continue in the foreseeable future. Current monetary and fiscal policies in the U.S., the United Kingdom, the European Union and Japan, prevent large, overleveraged banks from failing and allow high levels of government borrowing to continue despite higher debt levels and lower tax revenues resulting from weak or deteriorating economic fundamentals.

Given the economic and financial condition of Western countries, as well as Japan, it is not practicable for monetary expansion to abruptly cease or for money supplies to be quickly brought back in line with sustainable economic activity and population growth. In other words, there is no practical way for central banks to stop currency debasement without bank failures and sovereign defaults.

Value Versus Psychology

With gold and silver prices at or above current levels, some gold and silver mining stocks are severely undervalued. However, exploration companies without substantial defined resources and producers that have relatively high production costs or relatively low grade deposits are less likely to rebound when mining stocks begin to recover.

Metals prices stuck in a trading range and higher oil prices, thus, higher energy costs, are crushing the prices of exploration stocks and impairing the share prices of producers with higher production costs or lower grade deposits. In contrast, the share prices of gold and silver mining companies achieving consistent growth in resources and reserves, production, revenues and cash margins can be expected to rebound vigorously when confidence in metals prices firms. Cash flow will separate the wheat from the chaff.

The question on the minds of many investors is “Where is the bottom?” Many fund managers have pulled out of gold stocks after making little progress in the past year or more, and there is a growing sense of despair in the marketplace. At the same time, investors who pulled out are afraid to get back in. What is important about the pervasive negative sentiment is that it is a key indicator of a market bottom. At the top of the market, there are a hundred reasons to buy and, at the bottom of the market, there are a hundred reasons to sell. If psychology is any guide, gold stocks have hit bottom.

About Hera Research

Hera Research, LLC, provides deeply researched analysis to help investors profit from changing economic and market conditions. Hera Research focuses on relationships between macroeconomics, government, banking, and financial markets in order to identify and analyze investment opportunities with extraordinary upside potential. Hera Research is currently researching mining and metals including precious metals, oil and energy including green energy, agriculture, and other natural resources. The Hera Research Newsletter covers key economic data, trends and analysis including reviews of companies with extraordinary value and upside potential.

###

Articles by Ron Hera, the Hera Research web site and the Hera Research Newsletter ("Hera Research publications") are published by Hera Research, LLC. Information contained in Hera Research publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in Hera Research publications is not intended to constitute individual investment advice and is not designed to meet individual financial situations. The opinions expressed in Hera Research publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and Hera Research, LLC has no obligation to update any such information.

Ron Hera, Hera Research, LLC, and other entities in which Ron Hera has an interest, along with employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. The policies of Hera Research, LLC attempt to avoid potential conflicts of interest and to resolve conflicts of interest should any arise in a timely fashion.

Unless otherwise specified, Hera Research publications including the Hera Research web site and its content and images, as well as all copyright, trademark and other rights therein, are owned by Hera Research, LLC. No portion of Hera Research publications or web site may be extracted or reproduced without permission of Hera Research, LLC. Nothing contained herein shall be construed as conferring any license or right under any copyright, trademark or other right of Hera Research, LLC. Unauthorized use, reproduction or rebroadcast of any content of Hera Research publications or web site, including communicating investment recommendations in such publication or web site to non-subscribers in any manner, is prohibited and shall be considered an infringement and/or misappropriation of the proprietary rights of Hera Research, LLC.

Hera Research, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of Hera Research publications or website, any infringement or misappropriation of Hera Research, LLC's proprietary rights, or any other reason determined in the sole discretion of Hera Research, LLC. ©2011 Hera Research, LLC.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.