The Kondratieff K Wave Strikes Back, a multi-generation long wave debt cycle

Stock-Markets / Financial Markets 2012 Apr 20, 2012 - 06:33 AM GMT

The Kondratieff long wave cycle (aka The K Wave) provides the only good explanation of the current state of the global economy and financial markets. It is clear that a multi-generation long wave debt cycle has driven individual, government and corporate debt to crisis levels that are now in the process of a slow motion implosion. The debt is coming due, but central banks and governments have transferred much of the debt to innocent parties and postponed the due date. These misguided monetary and fiscal policies only bought a little time.

The Kondratieff long wave cycle (aka The K Wave) provides the only good explanation of the current state of the global economy and financial markets. It is clear that a multi-generation long wave debt cycle has driven individual, government and corporate debt to crisis levels that are now in the process of a slow motion implosion. The debt is coming due, but central banks and governments have transferred much of the debt to innocent parties and postponed the due date. These misguided monetary and fiscal policies only bought a little time.

The K Wave is now striking back, undermining the confidence game the central banks and politicians are playing. They are trying to stop the long wave winter season's natural decline, but the evidence is mounting that they are failing. The undertow of the K Wave debt deflation winter has triggered a depression in periphery countries that is picking up steam and heading rapidly toward the developed core countries.

The K Wave is the great cycle of human action in the global economy, both free market and government sponsored coercive human action. The final decline of the K Wave is unfolding globally as the final business cycle of this long wave tops out and turns down. Investors should prepare for a final round of global financial systemic shock that will shake global markets to their foundations.

The ancient Jubilee debt cycle, with a fixed date of debt cancellation in the future, was to prevent the excessive build up of debt in the system. International free market capitalism is the greatest system ever devised by man, but it does not have a Jubilee debt forgiveness target date in the future to prevent the buildup of excessive debt. Instead, international free market capitalism has a global K Wave depression, which purges economically unsustainable debt and cleans the excesses and overproduction from the international system. The creative destruction of a long wave winter always lays the groundwork that triggers a new K wave spring season, a new beginning for the global economy.

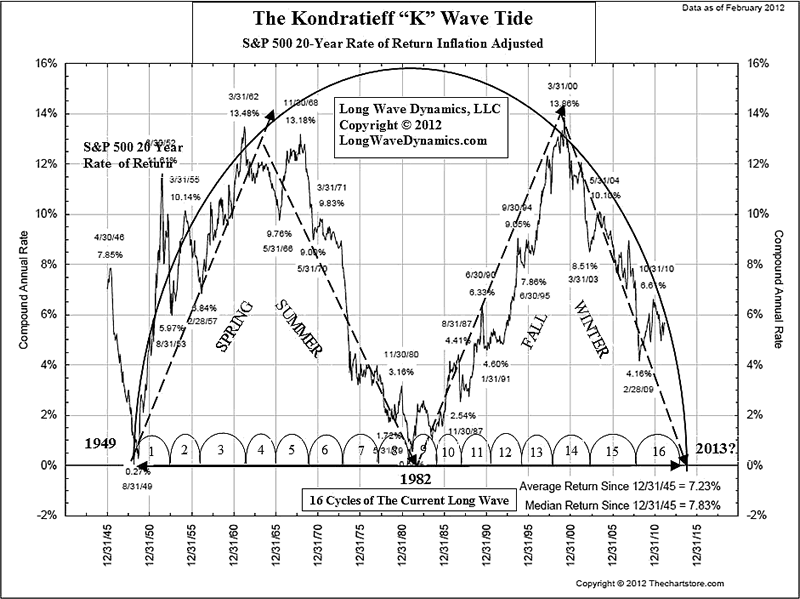

The inflation adjusted 20-year rate of return in the S&P 500 is one of the best charts for revealing where global markets are in the K Wave cycle. This chart knocks out the noise and presents the compound annual rate of return. The spring and fall seasons provide outsized returns, while the summer and winter seasons are drug down by the corporate inefficiency of the long wave forces at work. These K Wave seasonal forces control long-term investment returns. A final global plunge into 2013 in the 20-year rate of return to end the long wave winter season is in the cards. Central bank efforts to fight this natural downturn are counterproductive. They are only protecting special interests and exploiting the working class that ultimately pays the tab.

Central banks and governments have spent other people's money to try to save and return to the glory days of this long wave cycle. They will not accept that the old cycle must end. The passing of the old provides the room for a new global economy through innovation, hard work and capital formation. More debt that is only seeking to save banks and businesses best left to their just rewards is not the answer.

In the current K wave, debt has driven excess capacity in banking, autos, manufacturing, retail, etc. There is not sufficient demand to keep up with the debt-financed overproduction and supply of everything. Only politicians scrambling for their political survival think the debt binge can go on forever. It cannot and it will not. The debt game is coming to its final K wave ending.

In an attempt to save the old order by saving the bad debt funding the excesses, misguided policies are driving the system inexorable toward greater chaos than would otherwise take place in the transition of a K wave from the long wave winter to a new long wave spring. Instead of cycles being the background noise of human action and progress, the government and central bank managers have delivered the world into the eye of a global long wave hurricane ending. The next encounter with the K wave eye wall is rapidly approaching.

Fortunately, it is not all gloom and doom. There remains the chance that the phenomenon of emerging markets will limit the damage of the ending of this long wave. The final systemic shock phase could be short and V shaped. Dozens of new countries are embracing and integrating with international free market capitalism. Even former communist China has joined international free market capitalism. China does not represent a new civilization; it is integrating into western civilization. Spengler was wrong. We are not witnessing the decline of the west, but the westernization of the world that could lead to a new golden age, if the politicians and central bankers get out of the way and let producers and markets get to work.

Large cap global brand and franchise companies that pay great dividends will come roaring out of the coming long wave bottom. The bottom of this long wave winter will produce the greatest buying opportunity of a lifetime. The final plunge of the long wave winter season will offer great yields on great companies.

In terms of the current business cycle, the late market analyst PQ Wall proposed that every long wave contains 16 Kitchin cycles. This cycle model corrected the error of Joseph Schumpeter. The cycle model presented by Schumpeter in his seminal work on cycles titled Business Cycles proposed 18 Kitchin cycles in every long wave. The Kitchin/business cycle evidence indicates that the global economy has now likely topped in the final Kitchin cycle #16 of the long wave cycle. You can actually count out the business cycles in the K Wave in the chart above, or in more detail using swings in stochastics.

The fact that the world is in the final business cycle of a long wave winter season, means the economy and markets could suffer a final reversal of fortunes much faster than most realize. The business cycle was rolling over in December, with the European banking system going over the edge. A trillion euro LTRO program re-liquified the global financial system. That sugar high is now wearing off. The liquidity only served to expand the business cycle; it did not solve the problems of spreading global K wave insolvency. The LTRO is likely just the first step in bank nationalization required to address the K wave decline and the sovereign debt and banking bust that is running its course in Europe.

Any number of events could precipitate the final leg down of the long wave decline. All eyes are on Europe and Spain's terrifying prospects in particular. Spain is experiencing a Great Depression. Spain is demonstrating what is coming to the rest of the world over the next 18 months. The idea that the depression in the periphery of Europe is not going to spread to the core and to the global economy is nonsense.

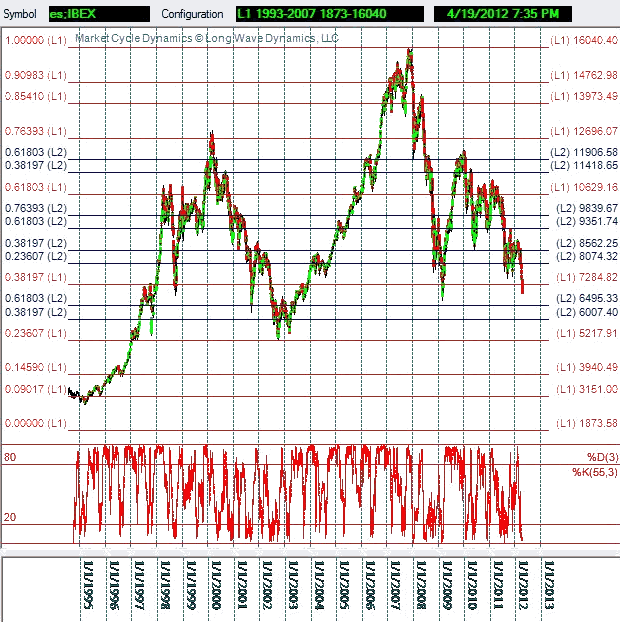

The chart below reveals the Level 1 Fibonacci Grid in Spain using the 1993-2007 bull market. Spain topped in Wall cycle #1, making the Kitchin/business cycle since the low in 2009 an extreme left translated cycle. Spain's IBEX has just crashed through the inverse golden 38.2% target of 7284 in the decline of Wall cycle #6. This is an ominous sign. The crushing K wave winter depression is clear in Spain, and likely has much further to go on the downside.

Spain is important, but in Asia, a hard landing in China could be what sends global markets toward their final lows for this long wave winter season in the years directly ahead. Hong Kong is the gateway to Asia, and China in particular. It is also one of the best barometers sitting between the developed world and the emerging world.

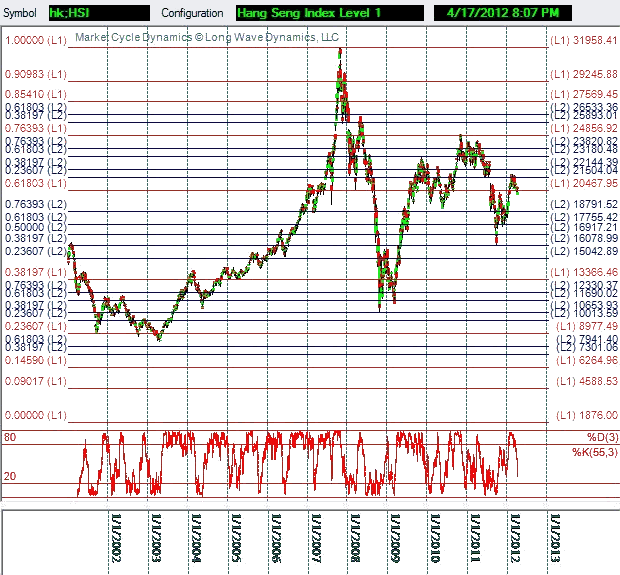

The Fibonacci grid chart below, created with Market Cycle Dynamics software, presents the Level 1 grid of the entire 1987-2007 bull market in the Hang Seng Index. Notice that the Hang Seng is now sitting on the golden ratio of the entire bull market at 20,467.96. It dipped under it a few days ago. This golden ratio is critical. It provides the clue to the direction in Asia, and in turn the developed world. Global markets are a complex system of human action. We are all in this K wave together. Global markets are hanging on this golden ratio wire of psychological support. If it snaps, global confidence will go with it.

Global equity markets will bottom six to nine months ahead of the economy. Of course, the politicians and their central banker funding could still screw things up, and trigger a far more extended and serious ending to this long wave winter season. A weekly close below the golden ratio in Hong Kong may be one of the best signals that the final business cycle of the long wave will soon accelerate its decline. There is a good chance that many markets will test their 2008-2009 lows before this K Wave winter finds a bottom and turns the corner.

Investors and traders are beginning to recognize that there are nine smaller Wall cycles in every Kitchin/business cycle. Investors and traders track the Wall cycle as a formula timing plan to identify buying and selling opportunities. Hong Kong topped in Wall cycle #4 in this business cycle, meaning that the current Kitchin Third cycle is a left translated cycle. The current Wall cycle is Wall #6. When a Wall cycle #6 drops through a golden ratio in an important market it can trigger global technical damage.

The Kondratieff long wave is having a profound impact on the U.S. and global economy. The updated and expanded definitive book on the long wave is now available. Based on popular demand, the book has been returned to the 1995 McGraw-Hill title of The K Wave; Profiting from the Cyclical Booms and Busts in the Global Economy (2012), in eBook format. The book includes dozens of updated K wave charts, and the Level 1 Fibonacci grids and charts for major stock markets around the world.

Aggressive central bank policies have expanded the current business cycle. Even so, a hard landing for the global K wave is directly ahead. The central banks could pump a few more trillion into the global system and buy some more time, but the K Wave forces of debt and excess capacity must run their course. More easy money will just extend the day of reckoning and make it worse than it has to be. The global economy and financial markets remain in a K Wave winter season where trends can change quickly. Tracking all the market cycles is now more critical than ever for investors and traders.

David Knox Barker is a long wave analyst, technical market analyst, world-systems analyst and author of Jubilee on Wall Street; An Optimistic Look at the Global Financial Crash, Updated and Expanded Edition (2009). He is the founder of LongWaveDynamics.com, and the publisher and editor of The Long Wave Dynamics Letter and the LWD Weekly Update Blog. Barker has studied and researched the Kondratieff long wave “Jubilee” cycle for over 25 years. He is one of the world’s foremost experts on the economic long wave. Barker was also founder and CEO for ten years from 1997 to 2007 of a successful life sciences research and marketing services company, serving a majority of the top 20 global life science companies. Barker holds a bachelor’s degree in finance and a master’s degree in political science. He enjoys reading, running and discussing big ideas with family and friends.

© 2012 Copyright David Knox Barker - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.