Gold $900 - Fed Failing to Beat Inflation

Commodities / Gold & Silver Jan 13, 2008 - 08:01 AM GMTBy: Joe_Nicholson

“Any perception of the Fed's stinginess might play into a consolidation period for metals and could also start a rally in the dollar that has so far not appeared at the top of the year as some expected. That we've seen any weakness in metals at all lately might simply be the technicals asserting themselves, flattening out the ascent a bit before another run. Consider that oil is trading at all-time inflation adjusted highs, whereas gold's inflation adjusted record is above $2000 per ounce! Breaking through and holding last week's highs will be the first objective of any bullish activity.” ~ Precious Points: Wave 1 Done? January 06, 2008

“Any perception of the Fed's stinginess might play into a consolidation period for metals and could also start a rally in the dollar that has so far not appeared at the top of the year as some expected. That we've seen any weakness in metals at all lately might simply be the technicals asserting themselves, flattening out the ascent a bit before another run. Consider that oil is trading at all-time inflation adjusted highs, whereas gold's inflation adjusted record is above $2000 per ounce! Breaking through and holding last week's highs will be the first objective of any bullish activity.” ~ Precious Points: Wave 1 Done? January 06, 2008

It became too difficult to resist as the chairman opened his speech on Thursday with an overview of the credit crisis and its causes, this sense that Bernanke is not the power behind the Federal Reserve. He's the historian, the bard of the board, a sharp mind knowledgeable enough to elucidate heretofore arcane economic principles. But the power in the financial sphere once wielded by a very few men now seems invested more broadly in the market as a whole. Perhaps it's progress, perhaps depravity, but it's becoming increasingly clear that, in terms of interest rates at least, what the market wants the market gets, if not immediately, then eventually.

We maybe should have read it into the current Fed chief's earlier rhetoric on the importance of anchoring inflation expectations, but after a speech on Thursday aggressive at least in its attempt to shift the language about the Fed's recent performance if not in its specificity on policy, it's clear not only will the Fed cut by 50 basis points in January and probably further at future meetings, it will justify these decisions by its economic forecasts of anemic growth and more importantly by a view of inflation that overlooks short term measures like next week's PPI and CPI and commodities prices in favor of long bond yields and TIPS spreads.

To a candid world the circularity of the argument is evident. Bond yields are low because of economic uncertainty and because of rate cut expectations and, of course, because they are what the market says they will be. Though the Fed has been rather reactive and accommodating by its own historical standards, its evasions, its half measures, its focus on inflation risks have not satisfied a financial sector that has too long struggled and is now failing from the burden of an, until relatively recently, inverted yield curve. Bernanke's latest speech admits the TAF is not so much an emergency injection of liquidity as much as an attempt by the Fed to retain some measure of control over short term rates. But still the market clamors for lower rates and, with steady assurances from the Fed that all will be given in time, has managed on its own to steepen the yield curve while keeping 30-year bond yields just above the target overnight rate. Who but a banker trying to coerce the Fed thinks that's a smart investment?

Of course, all the while, apologists for the Fed have backed away from commodities prices, particularly gold, as an accurate measure of inflation expectations. But what better news could there be for owners of precious metals? Recalling that upwards of 8000 tons of gold are listed as assets of the Federal Reserve, not counting that held under earmark for international accounts, perhaps the bankers will settle for an appreciation of their metal holdings while they attempt to sort out the lessons of their failure to properly collateralize mortgage debt?

So, against the backdrop of not Fed stinginess as one might have expected even a week ago, but pledges of decisive and preemptive action, even of insurance against a potential recession despite all rational and objective measures of real inflation, precious metals had a record week with gold touching $900 and silver moving through $16. Wave 1, if it can still be considered such, was far from over!

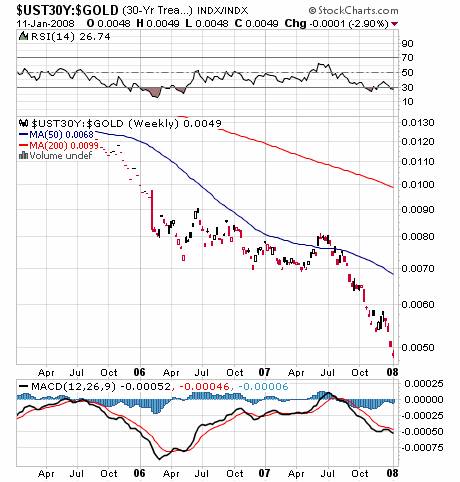

And as the chart above shows, the stock market's difficulties did not begin this past summer, but that in fact has deteriorated for years as gold has seen a protracted run. Even as the markets were hitting record highs nominally, they were exhibiting vastly deteriorated value in terms of the buying power of gold, oil, housing and other tangible commodities. Now that gold is reaching record highs, the S&P 500 to gold ratio threatens to sink below 1.0, where the nominal price of an ounce of gold and a share of the S&P are equal! The chart below shows that 30-year bond yields, too, have faired abysmally as an investment in comparison to gold.

But now that gold has hit $900, the question becomes whether this magnetic price that played on the yellow metal for weeks, calling it ever upward, will act like $100 has for oil, or will gold can break through. Two factors that tend to indicate gold getting through that resistance level in a matter of weeks if not days, are the difference in the inflation adjusted highs for gold and oil, and the bullishness of the Fed's current rate cutting disposition.

Oil is already trading at or near all-time inflation-adjusted highs, but for gold that level would be over $2000. Gold doesn't have the same immediate type of demand oil has, but this difference along changes the dynamic between gold and its current resistance level. And, of course, as explained the Fed has come out, at least rhetorically, in a big way for cuts this week. Even if the inflation talk at the end of the Bernanke's speech that probably contributed to stocks' losing the knee-jerk rally that began as news of the speech was leaked in advance, Bernanke was speaking of long term inflation expectations and Fed funds futures nevertheless remain priced for 100% odds of a 50 basis point cut in January. Bernanke does not appear willing to disappoint again.

Clearly last week's article anticipated a wave 2 retracement in gold we have not yet seen. It's possible we may see something more akin to the December triangle than an all out collapse. Still, as this move begins to be more and more extended, it begins to look like so many other parabolic commodities rallies that ended in sharp selloffs, and that should be a concern. Trying to short the top tick in gold, however, can be disastrous.

Furthermore, even a swift move back to 800 wouldn't even begin to dent this strong bull market. What happens after the January rate cut, or whenever it's no longer perceived the Fed has to cut rates further? How fast can the Fed can really take back their rate cuts, even if the bulk of nonperforming mortgages are identified this year? Because even if financials can stage a second half turn around this year, that doesn't necessarily mean consumers are relieved of their debts, that the subprime borrowers or first time buyers can any more afford to own a home, or that the economy will follow as robustly as a banking sector reinvigorated by low short term interest rates and a steep yield curve. And if rates do get back up to about 5% a year or so from now, that's still low historically and might be enough to slow gold down, but it's going to be darn near impossible to get the genie back in the bottle.

Finally, a reminder that TTC will be raising its monthly membership fee to $129 on February 1, 2008 . If you join now you can take advantage of the current $89 fee and be grandfathered in when we close our doors to retail investors sometime next year depending on sentiment amongst the membership. Over the past several months TTC has become a haven for institutional investors and in 2008 we're going to make a concerted effort to make the institutional side our primary focus. Only existing retail members will continue to be admitted after the cutoff, so if you've been holding out, the time to join is now

by Joe Nicholson (oroborean)

This update is provided as general information and is not an investment recommendation. TTC accepts no liability whatsoever for any losses resulting from action taken based on the contents of its charts,, commentaries, or price data. Securities and commodities markets involve inherent risk and not all positions are suitable for each individual. Check with your licensed financial advisor or broker prior to taking any action.

Joe Nicholson Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.