Financial Crisis American Gridlock, Why The “Left” And The “Right” Are Both Wrong

Politics / Credit Crisis 2012 Feb 07, 2012 - 04:52 AM GMTBy: John_Mauldin

Today we dive into Part 2 of Woody Brock’s notes from his new book, American Gridlock ( www.amazon.com/gridlock). He looks at what we can do in the future to prevent another crisis like we had in 2008, why we need to change, how we bargain with China (will be very controversial, in China at least!), what capitalism really is, and then he addresses the thorny issue of what it means to distribute wealth fairly. What can be said to those concerned with the top 1% of the population owning a grossly disproportionate share of the nation’s wealth?

Today we dive into Part 2 of Woody Brock’s notes from his new book, American Gridlock ( www.amazon.com/gridlock). He looks at what we can do in the future to prevent another crisis like we had in 2008, why we need to change, how we bargain with China (will be very controversial, in China at least!), what capitalism really is, and then he addresses the thorny issue of what it means to distribute wealth fairly. What can be said to those concerned with the top 1% of the population owning a grossly disproportionate share of the nation’s wealth?

You can learn more about Woody and his economic services at www.SEDinc.com, as well as see some of his previous essays. You can also follow him on Twitter and Facebook (Twitter: @HwoodyBrock; Facebook: American Gridlock [ http://tinyurl.com/7ch7vld]) . (Note: Woody is attempting a social media strategy to help deliver his message, and I am just curious as to how many people will follow him on Twitter.)

I had a long dinner with Woody last week and was on a panel with him the next evening. He is one of the more fascinating minds and interesting people I have met in my travels, and he tells the best historical stories (where else can you learn about who went down on the Titanic and why, and the foundations that were set up in their names that changed the US?).

I am off to South Africa tomorrow night and back Saturday, spending three of the next four nights in airplanes, experiencing the glamour side of travel. Not sure when or where I will write the letter for this week, but it will get done. And thanks to those of you who sent kind words and thoughts regarding my daughter Melissa, who I mentioned in last week’s letter. You are very kind, and it is appreciated. Have a great week!

Your getting 60 hours to read and write offline analyst,

John Mauldin, Editor

Outside the Box

JohnMauldin@2000wave.com

American Gridlock

Why The “Left” And The “Right” Are Both Wrong

Commonsense 101 Solutions to the Economic Crises

Part 2

Dr. Woody Brock

In this sequel to my essay on American Gridlock that appeared last week, I confront four final policy dilemmas confronting the US: (1)How can we prevent future Financial Perfect Storms of the kind that brought the world down in 2008? (2) How can we avoid bargaining with China as we have for several decades, ending up on the losing side of most negotiations despite possessing four times the “net power”of China, as measured correctly within the theory of games? That is, how can we earn an A rather than a D in Bargaining Theory 101? (3) Given today’s widespread discontent with “capitalism,” what kind of resource allocation system might be better? By what criteria can we legitimately rank systems such as communism versus socialism versus capitalism versus whatever? (4) Finally, what exactly do we mean when we speak of “fair shares”of income and wealth? What exactlydoes fair mean? What can be said to those concerned with the top 1% of the population owning a grossly disproportionate share of the nation’s wealth?

These four topics are discussed in my book American Gridlock in Chapters 4 through 6, respectively. As was the case of the policy proposals I introduced last week for redressing today’s Lost Decade and tomorrow’s Entitlements Spending crisis, my goal will be to deduce win-win solutions to these issues, solutions that are neither Left- nor Right-wing in nature. My most ambitious effort along these lines arises in topic 4, the thorny issue of the distribution of wealth. On the surface, this is a 100% partisan issue, with little common ground to unify the Left and the Right. I shall argue that this is not the case, as the issues that arise here are profound, and all I can do in this brief synopsis is to sketch the problems involved. A much more satisfactory discussion can be found in my new book, where detailed policy solutions to all four above questions are deduced.

Chapter 4: Preventing Future Financial “Perfect Storms”

“What is happening in the credit markets today is a huge blow to the Anglo-Saxon model of transactions-oriented financial capitalism. A mixture of crony capitalism and gross incompetence has been on display in the core financial markets of New York and London. From “NINJA” subprime lending, to the placing and favorable rating of assets that turn out to be almost impossible to understand, value, or sell, these activities have been riddled with conflicts of interest and incompetence.

These events have called into question the workability of securitized lending, at least in its current form. The argument for this change—one that I admit I once accepted—was that it would shift the risk of term-transformation (borrowing short to lend long) out of the fragile banking system and onto the shoulders of those best able to bear it. What happened, instead, was the shifting of the risk on to the shoulders of those least able to understand it.”

—Martin Wolf, “Why the Credit Squeeze Is a Turning Point for the World,” Financial Times, December 11, 2007

Widely acknowledged as the dean of world financial commentators, Martin Wolf outdid himself in these prescient comments made during the early days of the global financial crisis of 2007–2010. Going deeper, Gretchen Morgenson’s book Reckless Engagement argued that a self-dealing network of politicians/lobbyists/regulators/bankers enriched themselves at the expense of the broader public. Greed on stilts! While Wolf, Morgenson, and many others are right in what they say, they fail to point out that much deeper forces were at work here—forces that would transform the US housing market collapse into a veritable Perfect Storm. These deeper forces were identified only 15 years ago by means of a completely new concept of market risk developed by Mordecai Kurz at Stanford University. Kurz’s new theory of “endogenous risk” (risk that bubbles up from inside an economic system) teaches us that, while greed, incompetence, and conflict of interest stressed certainly exacerbate Perfect Storms, they are not in fact necessary for the occurrence of such crises. Something bigger is going on.

The primary purpose of Chapter 4 is to explain how such storms arise, and to do so from first principles utilizing the paradigm introduced by Professor Kurz. His theory represents the particular form of “deductive logic” I utilize in this chapter to help resolve an otherwise intractable problem. Because this new theory permits an identification of the true causes of market risk, and does so at a deeper level than ever before, it makes possible two other important advances. First, it can help policy makers identify valid policies for preventing, or, at least, mitigating future financial market storms. That is, the field of risk management receives a boost. Without understanding exactly what causes Perfect Storms to arise, meaningful storm-prevention policies cannot be identified. This point is often overlooked as legislators vent their rage at“the system.”

Second, the field of risk assessmentreceives a boost. There are, of course, many perspectives on market risk, including the popular “fat tail” theories celebrated by Nassim Taleb in his delightful book The Black Swan. But these theories usually describe risk rather than explain it at a fundamental level. Once again, without an understanding of the factors that give rise to risk in the first place, how could risk be properly assessed? For reasons stressed by Taleb and others, it is simply not enough for “quants” to massage historical data in an effort to determine meaningful probabilities of future events. For the probabilities of future events such as market meltdowns that define future risk cannot be assessed without first assessing the probabilities of the underlying causes of such events.

One caveat is in order here at the outset. The global financial crisis of 2007–2010 consisted of two parts. In the first part, the mortgage banking crisis in the United States and the United Kingdom held center stage. In the second part, the crises in these two nations spread across the globe like wildfire immediately after Lehman Brothers was allowed to go under in September 2008. I shall focus on the first stage because this is where the greatest confusion reigns. I ignore the second stage because the causality here is well understood: The collapse of Lehman Brothers and AIG precipitated a panic-driven cessation of interbank lending among all major financial institutions. This in turn caused the crisis to go global, and to impact the Main Streets as well as the Wall Streets of the world.

The Four Origins of the 2008 Financial Crisis: Figure 1 offers a summary of the four principal sources of the Global Financial Crisis. The contents of the boxes should be intuitively clear, with the exception of the first box: Poor Economic Theory. This is at once the least understood, yet arguably, the most important issue, along with Excess Leverage appearing in the fourth box on the right. It turns out that the two are closely interrelated, since poor financial theory provided bogus justification for levels of leverage that proved catastrophic to the entire world.

Financial economics between 1960 and 1990 was dominated by a highly problematic economic theory. This theory is usually referred to as Efficient Market Theory. More technically, economists refer to it as the theory of“Rational Expectations.” A theory (whether in physics or economics) is problematic if it neither explains nor predicts real-world data and if, at a deeper level, its Basic Assumptions are indefensible. In the case of good theories, the reverse is true: the Basic Assumptions from which the theory is deduced are judged“eminently reasonable,” and the resulting theory has the power both to explain and predict real-world data. Additionally, a good theory must be“falsifiable” in Karl Popper’s sense.

In what follows, Kurz’s new theory will be a foil against which the deficiencies of classical financial theory will become crystal clear. For it is a good theory in the precise sense just articulated. In particular, whereas classical theory could only explain about 19% of stock market volatility between 1900 and 1980 when tested by Robert Shiller at Yale in his classic 1981 essay, Kurz’s new theory can explain some 90% of observed risk. This represents remarkable progress. Regrettably, his new theory has been set forth in articles that are very demanding mathematically, and for this reason, his work is not yet widely known. This is SOP in the history of science.

Root Problems With the Efficient Market Theory: In the case of finance, the Efficient Market Theory is a poor theory insofar as: (1) It posits as a basic assumption that participants in markets never make mistakes, properly defined; (2) It assumes that all risks can be hedged, as well as that hedges never melt down—a pair of assumptions which, when combined with the no-mistakes axiom, imply that leverage will rarely cause significant problems; (3) It assumes that everyone in a market knows how to correctly “price” the news once it is announced—there are no disagreements as to how to interpretnews; (4) It predicts a level of volatility that is about one-fifth of what is observed in reality—with no Perfect Storm being possible; (5) It gave rise to the creation of new financial securities that did not perform as they were supposed to, and in fact became weapons of massive financial destruction; and (6) It implies that markets left to themselves will almost always function well, and will not break down.

As the following case study will show, poor financial theories—not just poor policies—can be very deleterious to the public welfare. They affect how we think, and thus how we regulate markets, or deregulate them, for that matter. As years go by, the Global Financial Crisis of 2008 should remind us of the extent to which bad thinking can lead to bad policies, as well as the extent to which bad policies really matter.

Superiority of the New Theory of “Endogenous Risk”: I believe that the new theory of endogenous risk developed at Stanford University is the appropriate antidote to the Efficient Market Theory, and the disaster which its models helped to foster. Like most good theories, the new theory does not reject the predecessor theory—Efficient Market Theory—but rather generalizes it. That is, it includes classical finance as a special case that will only work under idealized conditions that will rarely, if ever, be encountered in the real world. This was the case with Einstein’s general theory of relativity, which incorporated Newton’s theory of gravity as a limiting special case. Specifically, if and when space-time can be approximated as “flat,” not curved, then Newton’s laws work just fine, as they do in everyday life.

My job is now to explain the new theory, and convince you of its power. I shall demonstrate how it can explain the emergence of Perfect Storms—one form of those“fat-tailed” events that are usually described, but rarely explained from First Principles. Moreover, once the new theory is understood, the true deficiencies of classical Efficient Market Theory will become crystal clear. In particular, it will become clear how traditional financial theories have blinded policy makers, bankers, quants, and investors alike to the true magnitude of risk and, hence, the true likelihood of Perfect Storms.

Explaining Financial Perfect Storms Without Assuming Malfeasance: Can a Perfect Storm arise even if there are no greedy bankers, and no regulatory authorities beset by conflicts of interest—the conditions stressed by Martin Wolf in the opening citation above? The new theory of endogenous risk demonstrates that such crises can indeed arise without malfeasance. Of course, malfeasance will always exist, and its ancillary role is to amplifythe story we are about to tell. But malfeasance turns out not to be a necessary condition for Perfect Storms.

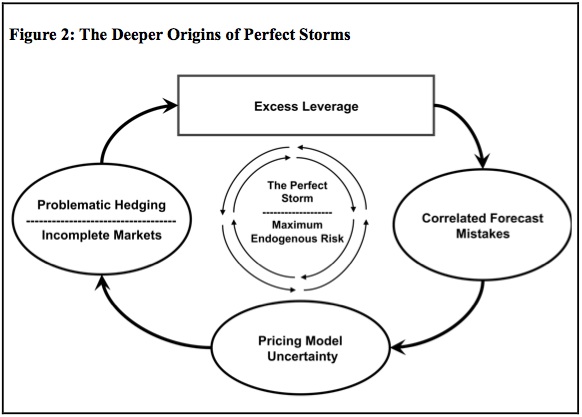

Please consider Figure 2. You see here the conditions that lead to a Perfect Storm, even when greed and self-dealing play no role. The best way to make sense of the four factors in the four outer boxes is to understand how and why each is a violation of the strict (and wholly unrealistic) assumptions of the Efficient Market Theory reviewed above.

Precondition 1: The Right-Hand Oval—Correlated Mistakes:In the world of efficient markets, it is assumed that all agents learn from historical data the true probabilities of all future events and prices. Thus, all agents share the same probability forecast. Moreover, given the assumption that the random process generating historical data cannot change—so the past is a perfect predictor of the future—then all agents’ forecasts will be the correct forecast. Accordingly, the concept of “mistake” does not arise in classical finance, and in no finance textbook will you find this word. A mistake occurs when someone looks back and says: “Gosh, the world has changed (e.g., global warming occurs, OPEC arises, derivatives are invented), and the betting odds I calculated from historical data were wrong.” Given the reality of “structural changes” that often make historical data unreliable, investors end up with a plethora of different forecasts. Since at most one forecast will be correct, most everyone will end up wrong, to one degree or another. What a contrast this is to the calm of an efficient market world in which no one ever says “I was wrong,” or rushes to change his portfolio.

Once mistakes enter the picture, market risk is transformed, a point central to Kurz’s new theory of risk. More specifically, it turns out that what matters to market prices and volatility is not merely that people’s bets are wrong, but additionally how correlatedtheir mistakes are. It is when most investors are wrong in the same direction that the greatest portfolio adjustments occur, and that prices change the most; for most everyone will either sell or buy, and the price swings accordingly. This is not the case when your bet ends up 15% high of reality, whereas mine is 15% low of reality. In this case, our mistakes cancel out, and prices do not move.

A classical example of a “correlated mistake” were bets on US house prices as late as 2006. Almost no one assigned high probability to the inconceivable 35% drop in house prices that transpired. The market response was fast and furious. Correlated beliefs of this kind are an important source of what Kurz calls “endogenous risk.”

Precondition 2: The Left-Hand Oval—Problematic Hedging: Life would be a lot less risky for almost all of us if we could perfectly hedge all the risks in our lives, the “complete hedging markets” assumption of classical financial theory. But as Professor Robert Shiller of Yale and others have shown, many of the most important risks in our lives cannot be hedged at all. These include the probability of unfairly being fired, the probability of having to sell a house when house prices are low rather than high, the probability of a good marriage remaining a good marriage and not ending in divorce, and the probability of stock prices being high versus low during the month we retire and seek to annuitize our wealth for a guaranteed lifetime income. The problem here is known within economic theory as the problem of“missing markets.”

You might suppose that non-hedgability of this kind has become much less of a problem than it used to be as instruments for improved risk-hedging become more available (e.g., many types of “derivative” securities). While there has been great progress along these lines in recent decades, it is well known in the economics community that many of the most important risks will never be able to be hedged due to problems of “moral hazards” and other related issues in economic theory.

In addition to the non-existence of hedges for smoothing out some of the bumpiest moments in our lives, there is the reality that hedges that do exist can melt down and malfunction just when they are most needed. Recall the terrifying U.S. market crash of October 1987, “Black Monday.” Also recall the collapse of the hedge fund Long-Term Capital in 1997. In both cases, distress was compounded and hence “risk” was greater when numerous hedges ceased to function. To conclude, problematic hedging is the second source of Financial Perfect Storms.

Precondition 3: The Lower Oval – Pricing Model Uncertainty: This condition is a bit more technical in nature. Have you ever been in a car with other impatient passengers, vainly trying to locate a destination on a roadmap when you cannot read the map? Confusion and mistakes result. The same idea arises in finance due to investors’ inability to read another kind of map. Do you recall from school the idea of a “function” F? For example, consider Y = F(X), expressing the concept that variable Y is a function F of some other variable X. Suppose X denotes “the news” in some market, and Y denotes market price. Then the function F transforms or “maps” this news X into price Y. In traditional finance and indeed economics as a whole, it was always assumed that, if investors knew the news, then they would know the price, or more correctly, the true probability of price that would result. That is, everyone knows and agrees on the function F. This is called Pricing Model Certainty.

Now let’s consider a different function Z = G(Y) where Z denotes the price of mortgage-backed securities—that class of weird, newfangled assets that melted down during the financial crisis of 2008. Let Y in this case represent the mortgage default rate on single-family houses. So this time, the function G specifies mortgage-backed security prices as a function of mortgage default rates Y.

Suppose, finally, that investors neither understand nor agree on the nature of the function G. More generally, assume that everyone knows that everyone else is uncertain about the true nature of G. Then, evenif everyone knows the truth about the default rate, they will not know the price of the associated securities. In my own research, I have called this Pricing Model Uncertainty. It can be proven mathematically that, the greater thistype of uncertainty is, then the greater the volatility of the market will be. In the case of a bubble, the greater the magnitude and duration of the bubble will be. Likewise, when the bubble bursts, the greater the resulting crash will be. Price “overshoot” thus occurs in both directions.

The intuitive reasons why this is true are explained in American Gridlock. Recall that classical financial theory assumes that such Pricing Model Uncertainty does not exist at all. This is one reason why classical theory has trouble explaining market booms and busts, and why it underestimates risk in general.

The existence of Pricing Model Uncertainty in the recent Perfect Storm was implicitly acknowledged by Federal Reserve Chairman Ben Bernanke in a speech he gave at the Plaza Hotel in New York late in 2007. He apparently asked a large audience:“We know the mortgage default rate news, but can anyone in this room stand up and tell me what this stuff (mortgage-backed securities) is worth?”Martin Wolf expresses a similar view in his above comment when he points out that such assets were “almost impossible to understand, value, or sell.”

So this is our third precondition for a Perfect Financial Storm: maximal Pricing Model Uncertainty. It is important to note that the kind of risk being generated here encompasses short-term volatility as well as longer-term bubbles.

Precondition 4: The Topmost Box—Excess Leverage: The last requirement for a Perfect Storm is that the various parties involved be maximally leveraged, just as both banks and homeowners were in the years preceding the Global Financial Crisis. The intuitive reason for the role of this last precondition is pretty obvious. Just think of yourself having made a significant investment without any leverage. From the start, there is the risk that this investment will either increase your wealth or reduce it over time. Now, suppose that you make the same investment, but you leverage your position 1:1, that is, you borrow half and put the other half down in cash. Next, suppose that you as an individual have leveraged your house 15:1, and that your bank is leveraged 50:1.

When your bet on future price goes badly wrong, and so do the bets of most others (recall that the housing crash represented a correlated mistake of this kind), then all hell breaks out in this case. Excessive leverage amplifies the role of the correlated mistake, of non-hedgability, and of pricing model uncertainty, as depicted clearly in the figure. This amplification is the principal source of the Perfect Storm seen in the center of Figure 2. Combined, these four factors shown in the outer boxes generate “maximal endogenous risk,” or equivalently, the Perfect Storm seen in the center circle.

What Must Be Done to Prevent Future Perfect Storms: The new theory sketched just above implies a great deal about how to reform the financial system, and why. To begin with, let me cite a distinction familiar to any engineer or systems theorist. There are two kinds of variables in the theory of the control of dynamical systems: state variables and control variables.The former refer to “states of the world” over which people have little, if any, control. Think of waves breaking on the shoreline of a coastal community. Control variables, on the other hand, are variables that can be chosen by human beings to improve a situation. For example, the denizens of the shorelines can choose to construct a granite sea wall to prevent the waves from damaging their community.

From this standpoint, note that all of the variables appearing in Figure 2 with the exception of“Excess Leverage” are state variables. Mistakes are going to happen, and cannot be banished. Hedging markets will always be “incomplete,” and hedges will often break down in extreme market conditions. Pricing Model Uncertainty is a fact of life in virtually all asset classes, with the possible exception of government bonds—at least prior to 2011! We can complain about such problems, and wish them away. But they will not go away. The same is true of those “malfeasance”variables not shown in the figure. We may dislike stupidity in regulators, but we are most likely stuck with it. As for “greed,” the idea that you can legally exorcise greed is as absurd to hoping to exorcise horniness among teenagers. People are no more greedy now than they were five thousand years ago. If you do not like this, go live on mars.

But leverage offers a different story. It is a control variable as is designated by being“boxed,” as opposed to “circled” in the figure. Leverage used to be vigilantly controlled, prior to the advent of the Greenspan-Bernanke era with its extreme deregulatory ideology. The principal policy conclusion of Chapter 4 in American Gridlock is that leverage must be reduced in all asset markets, and managed counter-cyclically by a new“leverage Tsar” on an asset market by asset market basis. This responsibility should be separated from the Federal Reserve Board, where as is customary attention should focus on setting interest rates to maintain price stability and growth on Main Street. The notion that the Fed funds rate should—much less can—control prices both in the goods markets and in the asset markets is one of the more preposterous conceits of current monetary theory. If you doubt this statement, just calculate the negative correlation between goods prices and asset prices during recent decades.

Why am I so insistent that excess leverage is the principal culprit in generating Perfect Storms? This is because of the highly non-linear way in which such leverage amplifies market risk in the context of Figure 2, and thus, can give rise to Perfect Storms, even in the absence of malfeasance. Demonstrating this formally is extremely mathematical, and the underlying theory is new. But it is correct, as well as commonsensical. The good news is that leverage is a control variable—not a state variable—and hence can be regulated at will as it once was and should be. Who will be the losers, and will oppose this with all their might? Partners in firms whose incomes will fall from $100 million to a measly $10 million per year. Pity such players, many of whose wives will doubtless sue for divorce. Many other financial markets reforms are proposed in Chapter 4, but these can best be understood by reading the book.

Chapter 5: Bargaining Theory 101, And How Not to Negotiate With China

This chapter has two different missions. In Part I, I argue for a resurrection of the disciplines of political science and political theory—both being“updated” to incorporate the modern logic of game theory. Part II applies this new logic to a real-world case study: the bargaining game being played between the US and China. In the first part of the chapter, I argue that politics is becoming more important than economics, or in Aristotelian terms that Res Politica will trump Res Economica as the future unfolds. For example, what was traditionally a free market in many commodities will become an increasingly politicized system in which nations vie to obtain “resource permits” from China for access to the markets it increasingly controls. In another direction, remember how Putin turned off the supply of natural gas to the Ukraine for not playing ball, politically, with Russia.

Need for “Core Models”: For the moment, economics is the dominant discipline, certainly not political science. Over the past five decades, we have gained a very good understanding of many aspects of economics, largely because of the existence of the core model of supply/demand/price familiar from page 1 of Econ 101. How does political science compare? Miserably. It offers no corresponding core model and is a discipline held in low esteem. When it comes to political philosophy, the discipline that is, at present, most needed since governance everywhere is breaking down, students are referred to the stale work of Dead White Males (Rousseau, Hobbes, Aristotle, Mill, Locke, etc.) who lived ages ago.

Yet how ironic all this is. For the dismal state of political science can easily be remedied, as the “core model” that is so needed already exists, and could play precisely the role in political science that the Law of Supply and Demand plays in economics. This is the model of n-person multilateral bargaining developed jointly by John F. Nash Jr., John Harsanyi, and Reinhard Selten during the period of 1960 to 1975. All three shared the Nobel Memorial Prize in economics in 1994 for their creation of this and related landmarks in game theory. I had the honor of working closely with both Harsanyi and Selten in my formative years, and am thus privileged to know this work intimately.

As I show in American Gridlock, their path-breaking bargaining model can be summarized in a few simple diagrams setting forth the basic logic of who gets how much of the pie in the political process of multilateral bargaining, and why. In a political science textbook of the kind I hope to see written, these graphs would be the political counterpart of those elementary supply/demand/price graphs appearing in Chapter 1 of Microeconomics 101 texts. The only difference is that the subject matter of the political graphs is far more embracing than those of “perfectly competitive markets,” and far more relevant to today’s increasingly politicized world.

Meaning of “Relative Power”: In my book, I describe their model, demonstrate how it works, and show how it gave rise to the first quantitative index of Relative Power, arrived at deductively (with no data) by John Harsanyi in 1962. We learned from Harsanyi’s work that relative power represents the weighted-sum of five different dimensions of relative bargaining power in any n-person cooperative game. More specifically, a player is more powerful than other players to the extent that:

1. Resource Power: He has greater resources than other players (money, military prowess, athletic prowess, intellectual capabilities).

2. Threat Power: He has greater threat power than other players as defined earlier. [John Nash brilliantly solved the problem of measuring “relative threat power” back in 1953. He showed that my relative threat power against you is a function of (i) how much my optimal threat can hurt you, net of the cost to myself of doing so, versus (ii) how much your optimal threat can hurt me, net of the cost to yourself of doing so. He proved formally that, in any two-person game, there will be a unique pair of optimal threat strategies, one for each of us.

3. Worth-to-Coalitions: He contributes more “worth” to the coalitions that he joins (e.g., an MVP has more power than other players because he contributes the most to his team).

4. Coalitional Muscle: He joins coalitions that are more powerful in opposing other coalitions than are the coalitions that other players join—that is, he has greater“coalitional muscle.”

5. Risk Tolerance: He has greater tolerance for risk in pressing his demands during bargaining than other players have, or equivalently, he has less “fear of ruin,” as game theorists put it.

Harsanyi formulated a power index measuring the relative power of different players in a manner that captures all five of these strategic dimensions of power.

The second part of Chapter 5 is quite different from the first. It is a case study analyzing the bargaining behavior of the US versus China during the past thirty years. I show informally that in the case of dimensions 1–4 of relative power just listed, the US was far more powerful than China, even if its relative power is now shrinking along some dimensions. The problem lies with dimension 5, the relative risk aversion of the two superpowers.

Given Harsanyi’s theory, there is only one “rational” explanation for the supine behavior of the US, and for its poor bargaining performance given its superior strength in dimensions 1–4: The US was risk averse in the extreme (the 5th dimension), and was never willing to take the risk of standing up to China. The evidence suggests that this was indeed the case. Along these lines, I reveal the dirty little secret that the yuan/dollar exchange rate today is nearly 50% lowerthan it was in 1991. Economic theory says that this exchange rate should have appreciated by about 300% during the past 22 years—not depreciated by nearly 50%. This is currency manipulation in the extreme. During a comparable period of 1971 and 1991, the Japanese were strongly criticized for currency manipulation, yet their exchange rate more than doubled against the dollar.

How could we have let China join the World Trade Organization without demanding remedies for such egregious currency misalignment, not to mention intellectual property theft of a magnitude never before witnessed? The interests of millions of American workers were sold down the river by successive administrations who seemed to view Nash’s concept of “optimal threats” as politically incorrect in the extreme. Can you imagine Secretary of State Clinton (whom I admire) ever issuing credible threats? This would be a contradiction in terms. But as Nash proved brilliantly, if you are a pacifist who wants peace, not war, then you had better articulate rational, credible, and enforceable threats up front. Or as the ancients said, “If you want peace, be prepared for war.”

If you do not believe that extreme US risk aversion explains risk-averse US bargaining behavior with China, then the only other explanation is that successive administrations were stupid, incompetent, and oblivious to the most elementary realities of bargaining. Bluntly, they were repeatedly and unnecessarily duped. At the end of Chapter 5 in the book, I propose several ways in which the US can regain the upper hand in its negotiations with China.

Chapter 6: Beyond Democratic Capitalism: An Idealized Policital Economy, Including Distributive Justice

The last chapter is the most profound and, I believe, the most interesting in American Gridlock. Due to limitations of length, the most I can do is to sketch the issues addressed, and refer you to the text for a more satisfactory discussion.

I start off explaining why true capitalism properly understood represents one of the great institutional innovations and successes of history. As the eminent New York Times journalist David Leonhardt wrote in his economics column published on July 27, 2011:

Economic truths may not rise to the level of certainty of two plus two equals four, but they are not so different from the knowledge that the earth is round, or that smoking causes cancer. When it comes to economics, we know that a market economy with a significant government role is the only proven model of success. The United States has outgrown Europe because of our greater comfort with market forces. . . . On the other hand, unencumbered market forces often lead to disaster, as 1929 and 2008 made clear.

The Meaning of True Capitalism, and the Concept of the Public Good: But what exactly is Leonhardt claiming here? What are the various economic, institutional, and governmental preconditions for successful capitalism? What are the precise circumstances under which Adam Smith’s concept of the “invisible hand” really does work as advertised? And under what other circumstances will it fail? As we review these circumstances, we will see that true capitalism does not represent some libertarian alternative to a system with a strong government. For strong and good government has been presupposed by capitalist theory from the time of Adam Smith, a point many self-styled conservatives seem to have forgotten. Additionally, the role of “perfect competition” that is central to Adam Smith’s concept of capitalism is all too often overlooked in today’s debates about the status of capitalism. Do the Occupiers of Wall Street understand that, according to “pure” capitalist theory, firms like Goldman Sachs would not be allowed to exist? Do they know that K Street in Washington would be closed? These are theorems, not opinions.

This section of the chapter culminates in a definition of the “public good” as set forth in classical economics. This concept makes clear what the market and the government should each do to maximize the public good, or in economics jargon, to achieve an efficient allocation of private and public resources. This ideal provides a yardstick for measuring how far today’s“bastardized capitalism” falls short of the way things should be.

Beyond Capitalism – Idealized Social Systems: The second section of the chapter builds on the classical results of the first, but delves much deeper. It investigates the concept of idealized social systems. More specifically, we investigate those properties above and beyond economic efficiency that might characterize an ideal economic resource allocation system. For example, do not most of us value the properties of freedom, distributional justice, informational efficiency, system stability, and privacy—along with classical efficiency? Drawing upon the brilliant work of another former teacher of mine, the late Nobel laureate Leonid Hurwicz, I explain how “snow-white capitalism” alone is consistent with all these norms, norms to which any of us would subscribe. [By snow-white capitalism, I mean the perfectly competitive free market backed up by the rule of law.] Hurwicz proved this from First Principles, and he also demonstrated how virtually any other resource allocation system (including communism and central planning) will not be compatible with these appealing norms.

Confronting “Distributive Justice”Head-On: The chapter then shifts to the polarizing issue of justice, and, in particular, the subject of Distributive Justice, which concerns the optimal distribution of wealth and income. My principal goal is to show how the issue of redistribution of wealth is not “outside” of free market economics, as is widely and erroneously believed, but is in fact integral to it. In particular, I demonstrate how a belief in the principles of true capitalism logically requires a belief in redistribution. This remarkable (and little known) result stems from combining the concept of “economic efficiency” on the one hand with an appreciation of the role of luck in wealth creation on the other.

This finding will make many self-styled conservatives and anti-redistributionists do a double-take! More generally, it renders the familiar Left- versus Right-wing divide on redistribution highly problematic. Bluntly, if you believe in market efficiency, then you must believe in a large dose of redistribution from the lucky to the unlucky. This is not an opinion. Rather, it is a theorem proven by Kenneth Arrow, of Stanford University, yet another Nobel laureate and, arguably, the most important economic theorist alive.

Morally-Based Theories of Distributive Justice:Arrow’s theorem just cited established a new link between the economic norm of“efficiency” and Distributive Justice. It does not, however, tread on the turf of political philosophers concerned with moralarguments for redistribution from the rich to the poor. The traditional prejudice here is that, because people possess what economists call“diminishing marginal utility of wealth and income,” then the poor ought to be taxed at a lower rate than the rich. The reasoning here is completely different from (but supportive of) Arrow’s results on redistribution implied by economic efficiency. It is reasoning relying on the concept of the relative “neediness”for income by the poor versus the rich.

The Left/Right Divide Over Redistribution:Moral philosophers have traditionally taken the side of the Left in interpreting Distributive Justice as a case for higher taxes on the rich, due to the greater relative neediness of the poor. In doing so, they have ignored a completely different dimension of the “fair shares” problem, namely “To Each According to his Relative Contribution.” No concept of “To Each According to his Relative Needs” can overcome the reality that, if you are the MVP of a team, then you should walk away with a larger share of the earnings than less valuable players. If this were not the case, then you would quit the team, and your teammates would soon be out of work. Certainly this outcome would not be“fair”!

At Last – Integration of Both Needs Justice and Contribution Justice: The challenge for moral theory, then, is to create a theory which integrates both Needs-Justice and Contribution-Justice, each norm operative in its appropriate domain. I created and published a theory achieving precisely this integration upon completing my doctoral work at Princeton. This theory is described at the end of Chapter 6, and has been deemed the highpoint of the book. What matters for my purpose in this book is how this achievement further narrows the divide between the Right and Left: For whereas the Left has always focused on Relative Neediness, and the Right on Relative Contribution, it turns out that both concepts of fair shares must and can be successfully integrated within a single theory of the state. Once again in this book, we learn how to transcend Left/Right gridlock, even in this mostcontroversial of all topics: Who really owes how much to whom, and why? This reaffirms my optimism that win-win solutions to our most difficult challenges are possible, and I hope it will render you more optimistic too.

When you read the chapter, you will learn how to measure the “relative contribution” and“relative neediness” of different agents in any situation, and you will learn that there is only one acceptable way to do so in both cases. Both measures were discovered by deductions from First Principles. I hope readers will come away from this discussion astonished by the recent progress that has been made in utilizing game theory to clarify age-old ethical concepts long that have long been recognized as important, but that were previously murky and non-quantifiable.

This wraps up the present two-part synopsis of American Gridlock, now available on Amazon or wherever books and ebooks are sold.

ERROR: I apologize for my stupid arithmetic mistake in last week’s essay where I said 7 x $12 = $94, rather than $84. Too much bad wine!

H. Woody Brock, Ph.D. New York City, NY

Woody@sedinc.com www.AmericanGridlock.com www.SEDinc.com

By John F. Mauldin

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2012 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.