U.S. Mint Gold Coin Sales Return to Fundamental Driven Demand

Commodities / Gold and Silver 2012 Feb 03, 2012 - 06:32 AM GMTBy: GoldCore

Gold’s London AM fix this morning was USD 1759.50, EUR 1,335.48, and GBP 1,110.66 per ounce.

Gold’s London AM fix this morning was USD 1759.50, EUR 1,335.48, and GBP 1,110.66 per ounce.

Yesterday's AM fix was USD 1,747.50, EUR 1,326.68, and GBP 1,102.80 per ounce.

Gold prices hit their highest since mid-November this morning as signals that U.S. monetary policy will remain ultra loose increased investor appetite for bullion.

Gold bullion has gained over 12% so far in 2012, and the ascent was rejuvenated last week with Bernanke’s commitment to keep interest rates low and money loose through 2014.

Spot gold hit a high of $1,762.90 before falling a few dollars to $1,757/oz by midday in Europe.

Concerns about the jobs number later today is also supporting bullion. Investors will be watching the US nonfarm payrolls report at 1300 GMT, after yesterday's data showed a surprise drop in jobless claims for last week which led to a pop in gold as did Bernanke’s testimony.

Spot palladium hit a 4 1/2 month high of $713.50. The metal used primarily for producing autocatalyses for gas powered engines, is supported by US auto sales which rose 11% this January, its best sales data in 2 1/2 years.

Gold Bullion Coin and Bar Demand Remains Robust – Tiny Vis-à-vis Other Investments

Data internationally shows that demand for gold bullion bars and coins remained robust in 2011 and into January 2012.

Demand is strong amongst the gold buying public but remains a fringe activity of store of value buyers rather than a mainstream phenomenon. At this stage very few retail investors have any allocation to gold whatsoever and very few have even owned a gold coin or bar in their life.

This is slowly beginning to change with a small minority of retail investors beginning to diversify into gold in order to protect against systemic risk in the banking and financial sector (MF Global) and from the monetary risk of currency debasement.

In Australia, the Perth Mint has reported very strong demand for gold and silver coins in recent weeks. The mint is a major supplier of coins to the UK and Europe.

Perth Mint’s sales director, Ron Currie told the Wall Street Journal that gold coin sales during December and January are up around 80% compared with the same months a year earlier, while silver coin sales have doubled. The mint’s largest markets for coin demand include Germany and the U.S.

However, demand for gold bullion coins and bars remains tiny vis-à-vis capital invested in stocks and bonds and vis-à-vis cash on deposit.

This suggests that the recent uptick in demand for gold coins and bars is very sustainable – especially against the backdrop of the challenging macroeconomic, systemic, monetary and geopolitical risk in the world today in 2012. A backdrop that is likely to be with us for the foreseeable future.

Sales of gold American Eagle coins this month total 114,500 troy ounces, the highest volume in a year and the most since 133,500 in January 2011. This, in turn, was the highest month since sales topped 150,000 ounces in May, June and July of 2010.

Figures from the U.S. Mint show an 18% decline in gold American Eagle sales in 2011 from the previous year, although sales of the silver Eagles still rose 15%.

Silver remains more affordable than gold and many bullion investors see greater value in silver bullion. Some expect the gold silver ratio to continue to fall with many believing, like GoldCore, that the gold silver ratio will fall to 15:1 in the coming years.

American Eagles—the world's most popular minted bullion coins—are generally viewed as a good indicator of retail investment demand for bullion – particularly in the U.S.

Research: US Mint Gold Coin Sales for January - Signal Return to Fundamental Driven Demand?

Dr. Constantin Gurdgiev, a non Executive member of the GoldCore Investment Committee, has analysed the data of US Mint coin sales in January and has looked at them in their important historical context going back to 1987.

January data from the US Mint on sales of gold coins presents an interesting picture, both in terms of seasonality and overall demand for the asset class.

Some background to start with. Gold prices have been moving sideways with some relatively moderate volatility in recent months. Between August 2011 - the monthly peak in US Dollar-quoted price and January 2012, price has fallen 4.55%, but in the last month, monthly move was 10.82% and year on year prices are up 30.4%.

Crisis-period average price is now at USD1,154/oz and the standard deviation in prices is around 337 against the historical (1987-present) standard deviation of 330. In 2011 standard deviation for monthly prices stood at 144(small sample-adjusted), well below historical volatility, due to a relatively established trend through August 2011. However, prices returned to elevated volatility in August 2011-January 2012.

These price dynamics would normally suggest rising caution and buyer demand reductions over time. And to some extent, this sub-trend was traceable in the data for US Mint sales in some recent months too.

For example, unadjusted for seasonal variation, August 2011 sales of Mint coins peaked at 112,000 oz with relatively moderate 0.67 oz/coin sold gold content. By November 2011, sales slowed down to a relative trickle of 41,000 oz at 0.71 oz/coin sold. December sales came in at 65,000 oz with gold content on average of 1 oz per coin sold.

Much media hullabaloo ensued with calls for catastrophic fall off in demand. There were renewed claims that a gold bubble is now in action and the decline in coinage sales is evidence of that.

In reality, there was very little surprising in the sales trends overall.

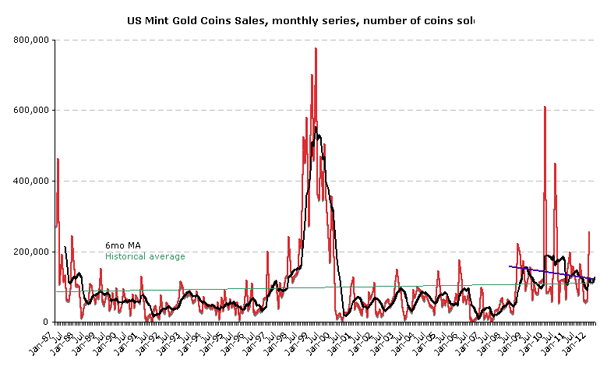

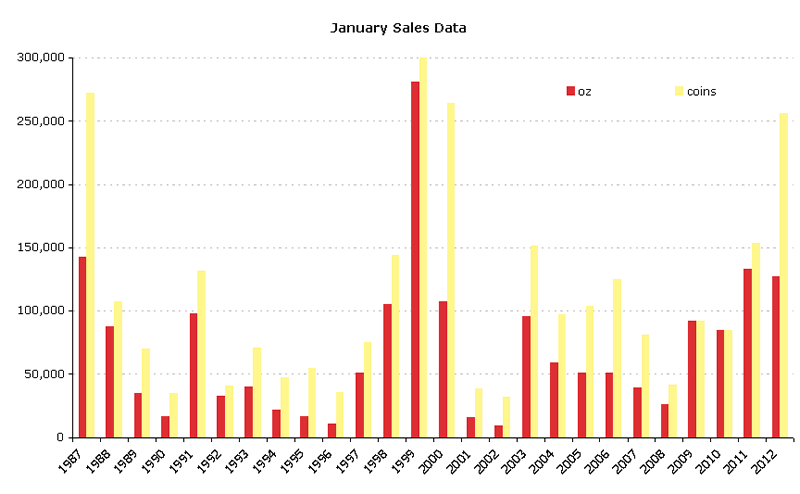

Chart 1 below shows US Mint sales in terms of the number of coins sold. Care to spot any dramatic bubble-formation or bubble-deflation here? Not really. There is a gentle historical upward trend since January 1987. There is volatility around that trend in 2010 and far less of it in 2011. There is seasonality around the trend with Q1 sales uplifts in January, some Christmas season buying supports in early Q4 etc. There is also a slightly elevated sub-trend starting from early 2009 and continuing through today. More interestingly, the sub-trend is mean-reverting (heading down) which is - dynamically-speaking stabilizing, rather than 'bubble-expanding' or 'bubble-deflating'.

Chart 1

Source: US Mint and author own analysis

Now, January sales are strong in the historical context and within the sub-trend since 2009. January 2012 sales of US Mint coins came in at 127,000 oz with relatively low 0.50 oz/coin sales. So coinage sales in terms of oz weight are 95.4% up on December, but 4.9% down on January 2011. For comparison, 2011 average monthly sales were 83,292 and crisis-period average monthly sales were 94,745 all at least 0.5 standard deviations below January 2012 sales. As chart above clearly shows, sales are now well ahead of historical averages and above 6 months moving average.

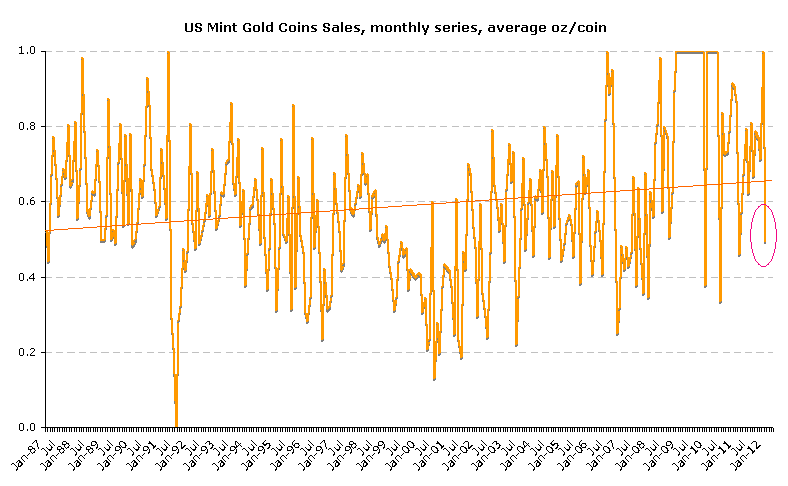

However, as chart below shows, sales in January were well below the trend line for average coin weight for sold coins: oz per coin sold is down 50.5% mom and down 43.1% year on year. Significantly, smaller coins were sold in January this year than in 2011. 2011 average oz/coin sold was 1.0 and the latest sales are closer to 0.59 oz/coin historical average.

Chart 2

Source: Author own data and analysis based on underlying data from the US Mint

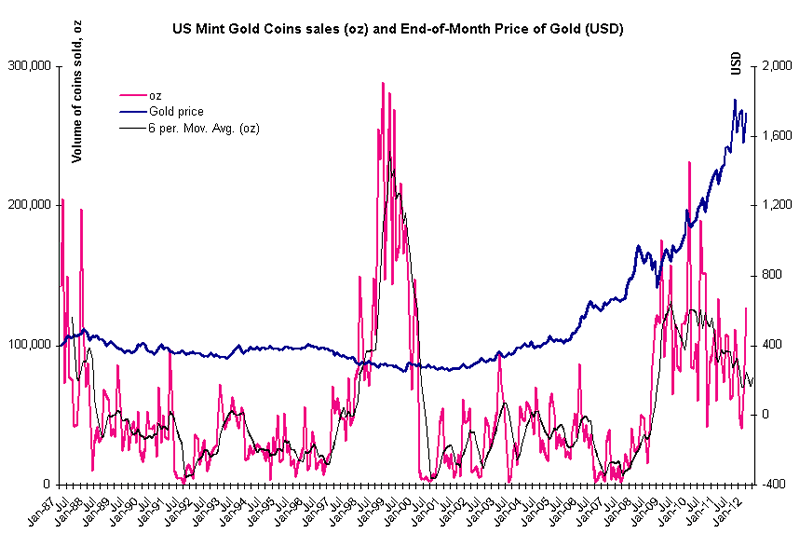

There is no panic in the overall trends in demand for coins when set against the price changes, with negative general trend in correlations between demand and gold price established in mid-2009 continuing unabated, as shown in Chart 3

CHART 3

Source: US Mint, World Gold Council and author own analysis

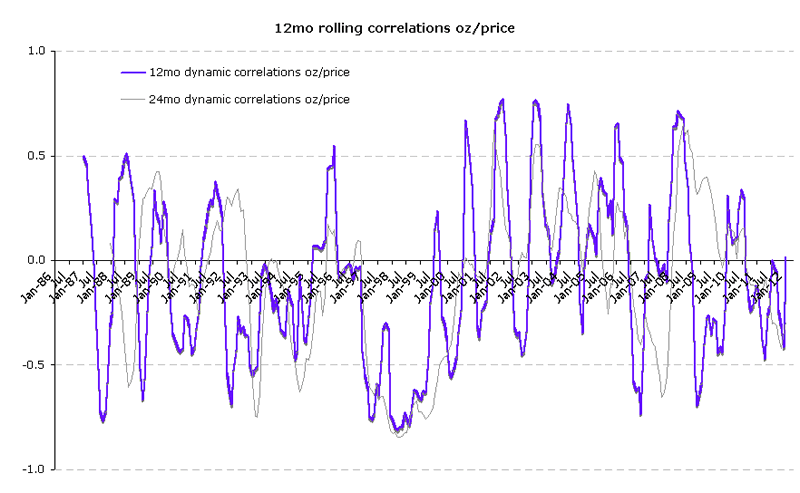

However, when we look closer at the 12 months rolling correlations and 24 months rolling correlations, the picture that emerges for January is consistent with gentle negative correlation that has been present since the beginning of 2011. See Chart 4 below. January 2012 12mo rolling correlation between gold price and volume of gold sold via US Mint coins is +0.02, having reverted to the positive from -0.42 in December 2011. This is the first positive (albeit extremely low) monthly 12mo rolling correlation reading since July 2010. 24 mo rolling correlation in January 2012 stood at benign -0.30, slightly up on -0.34 in December 2012. Again, resilience if present in the longer term series and at shorter horizon there are no huge surprises either. Of course, in general, one can make a case, based on the recent data, that investors are simply turning back to the specific instrument after gold price corrected sufficiently enough. In this light, latest US Mint data would be consistent with fundamentals-supported firming of demand. But crucially, there is no evidence of either panic buying or selling.

CHART 4

Source: Author own analysis based on the data from US Mint

Lastly, let's take a look at seasonally-neutral like-for-like January sales. Chart below shows data for January sales, suppressing the huge spike at 1999. Clearly, sales are booming in terms of coins numbers sold. But recall that coins sold in January 2012 are smaller in gold content, so overall gold sold via US Mint coinage is marginally down on January 2011, making January 2012 sales the fourth highest on record.

CHART 5

Source: Author own analysis based on the data from US Mint

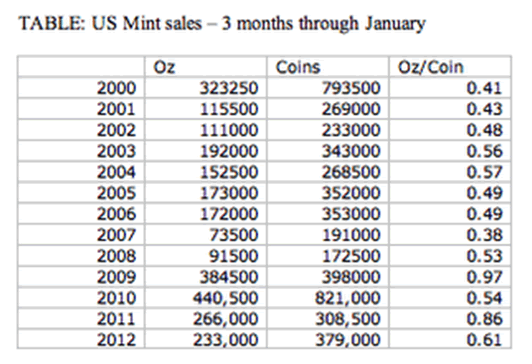

The Table below shows summary of US Mint coins sales for 3 months November-January covering holidays periods sales, including the Chinese New Year sales. While January 2012 period shows healthy sales across all three parameters, there is still no sign of any panic buying by small retail investors anywhere in sight here. Sales are ticking nicely, in 2011 and 2012, well ahead of 2001-2008 levels (confirming lack of perception in retail environment that general sustained price appreciation is a signal to dampen demand), but behind 2009-2010 spikes (further confirming the view that 2011-2012 dynamics are those of moderation in the precautionary and flight-to-safety motives for demand, and more buying on long-term gold fundamentals).

Source: Author own analysis based on the data from US Mint

Welcome back to ‘normalcy’ in US Mint sales.

Once again, the evidence above does not imply any definitive conclusions as to whether gold is or is not a “bubble”. Instead, it points to one particular aspect of demand for gold -- the behaviourally anchored, longer-term demand for gold coins as wealth preservation tool for smaller retail investors.

It does suggest that there is little in the way of ‘animal spirits’ in the gold market with no signs of a gold mania or ‘gold rush’ whatsoever.

Given the state of the US and other advanced economies around the world since January, 2008, U.S. Mint data does not appear to support the view of a dramatic over-buying of gold by the fabled speculatively crazed retail investors that some media commentators are seeing nowadays.

The man and woman in the street in most western countries (except for Germany, Austria and Switzerland) continues to be a more of a seller of gold (jewellery into scrap) than a buyer of gold as seen in the western world phenomenon that is ‘cash for gold’.

The excellent research on US Mint gold coin sales in January 2012 and going back to 1987 by Dr Constantin Gurdgiev can be read here.

SILVER

Silver is trading at $33.85/oz, €25.72/oz and £21.40/oz.

PLATINUM GROUP METALS

Platinum is trading at $1,624.50/oz, palladium at $700/oz and rhodium at $1,400/oz.

For the latest news and commentary on financial markets and gold please follow us on Twitter.

GOLDNOMICS - CASH OR GOLD BULLION?

'GoldNomics' can be viewed by clicking on the image above or on our YouTube channel:

www.youtube.com/goldcorelimited

This update can be found on the GoldCore blog here.

Yours sincerely,

Mark O'Byrne

Exective Director

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information contained in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.