U.S. Dollar Centric Derivatives Complex Progenitor of Parasitic Ponzi Price-Fixing

Stock-Markets / Derivatives Jan 13, 2012 - 12:23 PM GMTBy: Rob_Kirby

The term “derivative” has become a dirty, if not evil word. So much of what ails our global financial system has been laid-at-the-feet of this misunderstood, mischaracterized term – derivatives. The purpose of this paper is to outline the origin, growth and ultimately the corruption of the derivatives market – and explain how something originally designed to provide economic utility has morphed into a tool of abusive, manipulative economic tyranny.

The term “derivative” has become a dirty, if not evil word. So much of what ails our global financial system has been laid-at-the-feet of this misunderstood, mischaracterized term – derivatives. The purpose of this paper is to outline the origin, growth and ultimately the corruption of the derivatives market – and explain how something originally designed to provide economic utility has morphed into a tool of abusive, manipulative economic tyranny.

Definition of Derivatives

Derivatives are financial instruments whose values depend on the value of other underlying financial instruments or objects. The main types of derivatives are futures, forwards, options and swaps.

The original intended use of derivatives was to manage risk [hedge]; however, now they are often traded as investments whether hedged, un-hedged or as component of a spread trading strategy. The diverse range of potential underlying assets and pay-off alternatives leads to a wide range of derivatives contracts available to be traded in the market. Derivatives can be based on different types of assets such as commodities, equities (stocks), residential mortgages, commercial real estate loans, bonds, interest rates, exchange rates, or indices (such as a stock market index, consumer price index (CPI) — see inflation derivatives — or even an index of weather conditions, or other derivatives). In recent years, much has been written about credit derivatives - which have become an increasingly visible part of the derivatives complex. However, the largest component of the derivatives complex remains interest rate products which the U.S. Office of the Comptroller of the Currency tells us constitute more than 82 % of all outstanding bank held notionals. Interest rate derivatives have a great effect on interest rates as will be discussed later.

Origin of Derivatives

Derivatives have their roots in the agri-complex. From an historical context, it was agricultural commodities futures [mainly grain] that first gained traction as viable financial instruments. The genesis of these products dates back to the founding of the Chicago Board of Trade [CBT] in the mid-eighteen hundreds.

Back in the eighteen hundreds large scale farming enterprises were difficult [risky] to “bank”. The risk was embodied by the known costs associated with planting seed, fertilizing and subsequent growth and harvest – versus the often volatile, unpredictable final selling price of a perishable commodity. Futures removed this this “unknown” from the banking/farming relationship and transferred it to speculators for a nominal fee or cost.

From 1850 - 59, American agricultural exports were $189 million/year [81% of total exports]. With agriculture occupying such a huge percentage of exports and GDP it was only natural that business of this scale [potential fees and profits] would and did attract the attention of the money changers. The advent of futures and forward contracts in the agri-complex was productive: giving a higher degree of predictability to farm income making the business of farming more bankable. Making farm income more predictable enabled the growth of corporate agri-businesses which brought with it economies of scale, the freeing-up of human capital which enabled / translated into mass migration [urbanization] of farmers into cities in part assisting with the rise of the human capital pool essential for the industrialization of America.

Early Growth – the Commodity Futures

In the beginning, as with users in the agri-complex – there were IDENTIFIABLE END USERS [farmers] for these products. Over time, futures and forwards were developed to meet demand in other predominantly natural resource based commodities like coal, crude oil, lumber, cattle and others. Similar commodity futures markets for these products and trade volumes were driven primarily by end users and it’s important to distinguish that for the entire 1800s and virtually all of the 1900s – the growth in derivatives was primarily tied to the commodity trade.

Commodities Law Dictates that Futures Only Aid In Price Discovery

Definition of Price Discovery:

A method of determining the price for a specific commodity or security through basic supply and demand factors related to the market.

According to William J. Rainer, former Chairman of the Commodities Futures Trading Commission [CFTC] back in 1999, Section 3 of the Commodities Exchange Act espouses three basic purposes for the regulatory structure currently administered by the CFTC: (1) to protect the price discovery function; (2) to prevent the manipulation of commodities through corners, squeezes and similar schemes; and (3) to assure an effective vehicle for risk transference. Implicit throughout is the need to provide suitable customer protection from abusive trade practices and fraud.

The Rise of Financial Engineering: The Genesis of OTC Interest Rate Derivatives

President Nixon took America and the world off the gold standard in August, 1971. What ensued was a dramatic increase in the price of crude oil which led to burgeoning balances of petro dollars [Euro-dollars] as deposits in the treasuries of banks involved in international trade and a subsequent bolstering of their treasury operations to deal with the influx of ‘inflated dollars’.

Interest Rate Derivatives were developed around 1980. Their basis was the four 3-month IMM [International Money Market] Eurodollar Futures Contracts [Dec, Mar, Jun, Sept] on the Chicago Mercantile Exchange [CME]. These futures contracts are derivatives of 3 month Libor [London Interbank Offered Rate] for Eurodollar Time Deposits. The 3 month Libor rate is ‘set’ daily by a group of banks selected by the British Bankers Association and represents where these ‘reference banks’ are willing to ‘loan’ their mostly recycled Euro Dollars [petro-dollar] to their most credit-worthy customers.

These derivatives/futures gave banks the ability to ‘hedge’ or book profits on sizable amounts of predictable future cash flows. Up until 1980, this bank treasury trading business remained largely a cash trade.

The Toronto - Chicago Nexus

In 1980, Canada revised its Bank Act. In the ensuing few months, Canada had an influx of foreign banks - dubbed schedule “B” banks. Canada went from having 5 domestic banks to having roughly 65 banks in a matter of months. To protect their home turf, the existing domestic banking industry successfully lobbied Canadian politicos to limit the amount of capital new ‘schedule B’ banks could have [initially to 5, or in a couple of instances,10 million CAD].

This placed growth restrictions on foreign banks, new entrants, beginning operations in Canada; capital ceilings implied severe balance sheet restrictions. 60 new banks had just opened their doors – but they were substantially limited in participating in main stream bank treasury operations like lending long and borrowing short - in the inter-bank market because these activities bloated balance sheets.

These new treasury operations needed to find a profitable raison d’etre or their parent banks would shut them down.

Competition Breeds Innovation

To differentiate themselves from the rest of the crowd back in the early 1980’s, particular institutions like Citibank, Toronto and Chemical Bank, Toronto and Chase, Toronto went on a hiring binge of Ph. D mathematician types and immersed themselves in ‘financial engineering’ utilizing then emerging exchange traded futures [cited above]. These financial engineers conjured into existence two Over-the-Counter [OTC] products – Future Rate Agreements [FRAs] and Interest Rate Swaps [IRS]. Trade in these products did not entail the exchange of principal sums between counterparties – only interest-rate differentials on principal amounts [referred to as notional underlying amounts]. The beauty of this “new trade” was a] it was fee based, b] that, for accounting purposes, it was “off balance sheet” and c] it circumvented capital ceiling restrictions.

From a customer standpoint – these products were marketed to corporate customers as a means to achieve cheaper, more flexible funding or alternatives for funding in terms [yrs.] they otherwise would not be able to access.

From an historical perspective - it was during the 1980s when Citibank, Toronto or Chemical Bank, Toronto traded the very first Inter-bank U.S. Dollar Interest Rate Derivative – known as an FRA [Future Rate Agreement] which, at its core – was nothing more than a glorified ‘bet’ on what 3, 6 or 12 month Libor will be at a future date.

It was Citibank Toronto who first engineered a financial model to successfully book accounting profits from FRAs and interest rate swaps.

In the beginning – these trades were ENORMOUSLY profitable – so much so that Citibank Toronto very quickly became the world’s biggest OTC interest rate derivatives house and was, in fact, the clearing house for OTC interest rate derivatives for Citibank worldwide.

This business absolutely mushroomed!

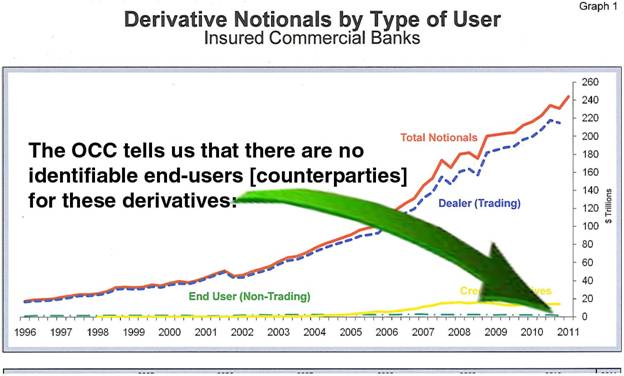

Source: U.S. Comptroller of the Currency

Tracking the evolution of the aggregate derivatives held by U.S. banks, it is apparent that trade in end-user products has been ABSOLUTELY OVERWHELMED by volumes in dealer trades – all in a “supposed market” which is 96% constituted by 5 players [the magnificent 5; J.P. Morgan, BofA, Citi, Goldman, Morgan Stanley] – as the U.S. Comptroller of the Currency tells us in the executive summary of their Quarterly Derivatives Report,

“Five large commercial banks represent 96% of the total banking industry notional amounts.”

At this rate of concentration, the derivatives complex appears a lot more like an “old boys club” than it does “a market”. Therefore, the derivative market rapidly evolved during the late 1990’s to the early 2000’s from a previously end-user-based to a dominantly dealer-based or trading market. The parabolic rise of these dealer traded volumes parallels the rise of market rigging or the movement toward a centrally planned economy.

From Humble Beginnings, How and Why We Got Here

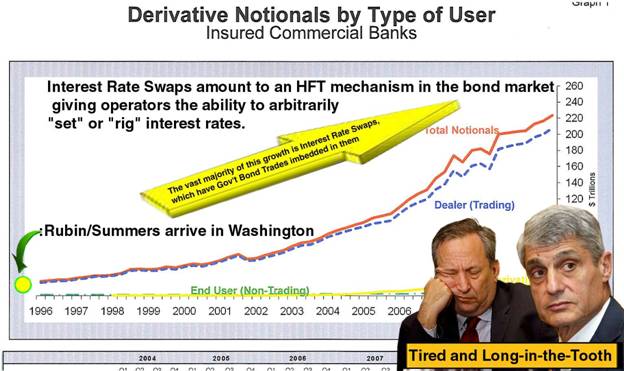

The graph of outstanding notional amounts above depicts a serious growth curve. To explain why, let’s take a look at the same graph with some added highlights explaining “what” is growing so quickly:

Source: U.S. Comptroller of the Currency

Through the late 1980’s and early 1990’s – folks at the Fed and U.S. Treasury – with a little bit of help from academia - realized that interest rate swaps could be utilized to CONTROL fixed income [bond] markets and hence – controllers could arbitrarily determine the cost of capital. As such, it’s no coincidence that institutions like Citibank Toronto had their ‘U.S. Dollar derivatives books’ repatriated back to New York in this time frame.

The Neutering of Usury or “Neusury”

Historically, the Federal Reserve/U.S. Treasury ONLY had control of the VERY short end of the interest rate curve – specifically the Fed Funds rate [the rate at which banks and investment dealers borrow and lend to each other on an overnight basis]. With the advent and proliferation of interest rate derivatives – specifically Interest Rate Swaps [IRS], the Fed/Treasury gained effective control of the “long end” of the interest rate curve. Thus the Fed / Treasury has been practicing an undeclared form of financial repression for a very long time.

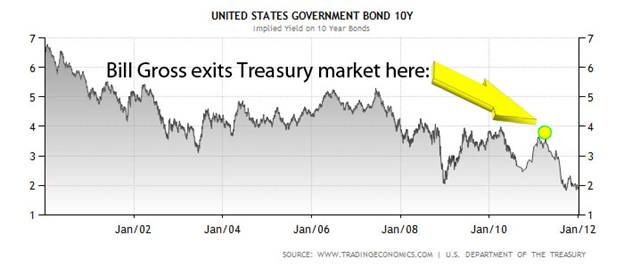

In free market economies the laws of usury dictate that the interest rate mechanism serves as the arbiter as to where scarce [finite] capital is allocated. Historically, it was a group of industry professionals known as the bond vigilantes who enforced this discipline – primarily on spend-thrift governments – by making them pay more, through elevated interest rates, when they demonstrated poor stewardship of national finances. Pre “neusury” – when we had truly free markets – when the bond vigilantes “sold” – interest rates WENT UP. To illustrate this point look no further than Bill Gross – the closest thing there is to a bond vigilante today - who heads the world’s largest bond fund PIMCO. It was CNBC who reported back on March 9, 2011 that,

“Pimco has dumped all of its US Treasury bond exposure in its flagship Total Return Fund. The move makes sense given Pimco chief Bill Gross's public statements that Treasurys are over-valued.”

Pre “neusury” – such a pronouncement would have caused a MAJOR SELL OFF in bonds [higher rates]. Nowadays, the Fed / U.S. Treasury and their ‘captive’ investment banking vassals high-frequency-trade pre-determined outcomes through the Interest Rate Swap complex to show folks like Bill Gross who’s really in charge. The cascade in 10 year yields depicted above just happens to coincide with the first half of 2011 – when, according to the Office of the Comptroller of the Currency, Morgan Stanley just happened to grow their swap book from 27.2 Trillion to 35.2 Trillion in notional – for a cool increase of 8 Trillion in six months at one investment bank.

The sheer volume physical U.S. government bond trade created by the interest rate swap derivative complex has resulted in “neusury” and OVERWHELMED the bond vigilantes – rendering them either impotent, extinct or perhaps just plain-old confused and afraid [take your pick?].

The incapacitation or extinction of the bond vigilantes has enabled the U.S. government to spend like drunken sailors, prosecute wars and misallocate resources on a grand scale – all the while lowering and / or keeping interest rates at or near ZERO. This arbitrary, gross mispricing of capital helped to spawn further abuses like the real estate and equity bubbles – the development of which produced new sub-sets of equity derivatives and cdo’s which also enabled the macro-management of these markets. Economics 101 tells us that capital is scarce and finite. By arbitrarily rigging interest rates too low – capital markets created the false impression of abundance – and loose lending practices resulted.

Control over the long end of the interest rate curve works as follows: The U.S. Treasury’s Exchange Stabilization Fund [ESF], a secretive arm of the U.S. Treasury unaccountable to Congress, began entering the “FREE MARKET” – deals brokered by the N.Y. Fed - as a receiver of “all in” fixed rates - in terms from 3 to 10 years in duration. Interest rate swaps [IRS] trade at a spread – expressed in basis points – over the yield of the 3, 5, 7 and 10 year government bond yield. Banks are virtually all spread players. When trades occur between spread players – one side of the trade sells the other side of the trade the proscribed amount of U.S. Government bonds. This creates superfluous settlement demand for bonds. When the U.S. Treasury’s Exchange Stabilization Fund [ESF] intervenes in this market – they are not spread players.

When the ESF trades with “spread players”[Morgan, Citi, BofA, Goldman, Morgan Stanley] – the banks are forced to purchase cash, physical U.S. Government bonds in the proscribed terms [3-10 years], almost dollar-for-notional-dollar – as hedges for each trade they do with the ESF [because the ESF does not supply them]. This is why – instead of the hollow, contrived, official excuses offered by the Fed – despite record, off-the-charts, government bond issuance – a remarkably large percentage of U.S. Government bond trades fail to settle.

++The ESF participates in these trades taking “NAKED INTEREST RATE RISK” – meaning they do not provide their counterparties with the requisite amount of bonds to hedge their trades – thus forcing them into the “free market” to purchase them. This generates UNBELIEVABLE “stealth” settlement demand for U.S. Government securities. This is how/why U.S. Government bonds and hence the Dollar can be made to appear “bid-unlimited” - even when economic fundamentals are SCREAMING otherwise. The amount of demand for cash government bonds that can be conjured out-of-thin-air in the derivative interest rate swap complex, which might be best described as “high-frequency-trade” on steroids - measured in hundreds of Trillions in notional - literally OVERWHEMS the cash bond settlement process. This means bond yields are set arbitrarily – in accordance with Fed / Treasury policy - NOT IN FREE MARKETS. This also explains why there are no identifiable end-users for the dizzying growth in interest rate derivatives [swaps] – the trade is all attributable to the Treasury’s ‘invisible’ ESF – an institution that is not publicly accountable to ANYONE or ANYTHING. This is why other nations can and do have, from time to time, failed bond auctions while America never has and NEVER WILL BE ALLOWED TO. This is all done in stealth to facilitate and give an air of legitimacy to the U.S. Treasury’s ZIRP [zero interest rate policy].

With gratitude, the detailed, documented, inner workings of the Treasury’s Exchange Stabilization Fund and their unique relationship with the N.Y. Fed trading desk is best explained by forensic financial researcher Eric deCarbonnel, here.

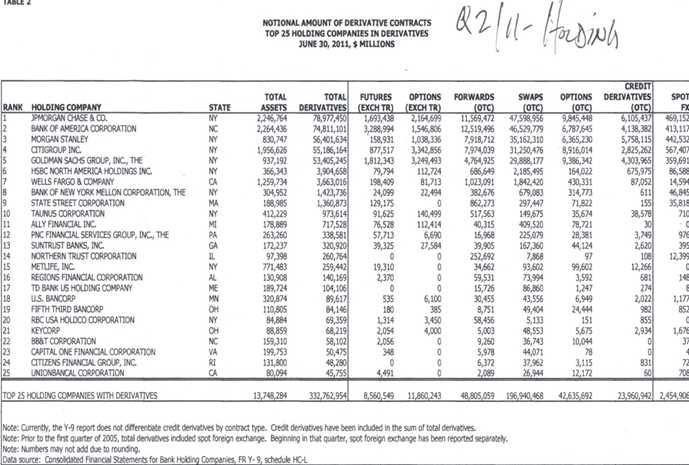

This is the real reason why J.P. Morgan Chase and the rest of the magnificent 5 now sport OTC derivatives books of 50 - 80 TRILLION in notional.

Here’s a peak of outstanding derivatives for U.S. Bank Holding Cos. as of June 30, 2011:

Source: U.S. Office of the Comptroller of the Currency

How We Know the ESF is the Other Side of These Trades

Morgan Stanley [MS] supplies us with the “smoking gun”. MS grew their derivatives book by 14 TRILLION in notional in the first 6 months of 2011 – virtually all in product [swaps] that requires 2-way / mutual credit lines. MS is a company with about 30 billion in market cap. who could not find a “dance partner” [anyone to buy them for a ‘pittance’] back in 2008 during the financial crisis. The GLOBAL BANKING SYSTEM – in aggregate - does not have sufficient credit lines to allow Morgan Stanley to conduct this level of trading activity in these credit dependent products as reported with legitimate banking counterparties. The notion that this obscene amount of trade represents legitimate business with banking counterparties that was bilaterally “netted” is preposterous and a non-starter. Ergo, the other side of the bulk [if not ALL] of this trade is necessarily the ESF – being done in the name of “national security” and / or the perpetuation of ZIRP and global U.S. Dollar hegemony. This obsequious, crony, insider trade has effectively served as an attempt to re-capitalize an insolvent MS via the public teat.

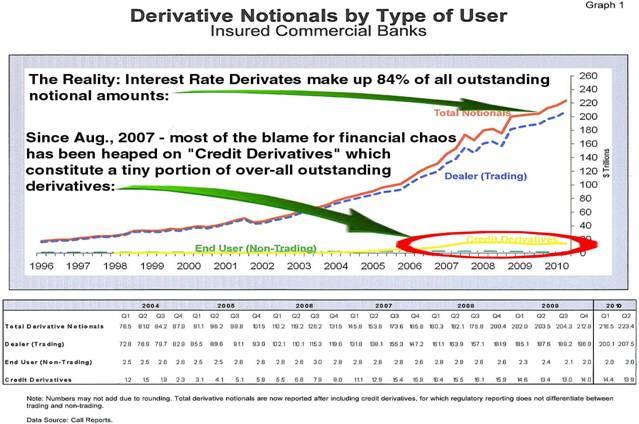

The [Mistaken] Promoted and Populist View of Derivatives

When the sub-prime crisis came to light in August 2007, much of the “blame” for our financial system melt-down was placed on the proliferation and reckless use of Credit Derivatives. Our bought-and-paid-for mainstream financial press was complicit in perpetuating this myth. This was a conscious effort to deflect attention away from what was being done the value of capital itself. Take note of the small proportion that Credit Derivatives [in yellow] contribute to the total outstanding notionals. Also take note of there being virtually ZERO identifiable end-users [slotted green line hugging the “x” axis]:

source: U.S. Comptroller of the Currency

The rise in the use of credit derivatives paralleled the rise in securitization of mortgages. Credit derivatives were used to “guarantee” the falsified values of toxic mortgaged-backed securities [MBS].

The growth of the housing bubble, Credit Derivatives and Credit Default Swaps [CDS] is more a symptom of systemic debasement of the value of capital – through ZIRP – than a cause.

Complete Capture of the Derivatives Complex and Defiling of Fiat Capital

That irredeemable fiat money is designed to fail – by its very nature – is laid out very well in Chris Martenson’s, Crash Course – a staple which everyone is encouraged to take the time to watch. But rather than let the “fiat” U.S. Dollar fail, as all irredeemable fiat currencies are designed to do – the sociopathic miscreants in charge of the Anglo/American banking edifice have BOUGHT TIME through the capture of the DERIVATIVES PRICE CONTROL GRID – by blatantly commandeering the unlimited resources of the U.S. Treasury’s ESF along with the printing presses of the Federal Reserve. This is done to make historic alternative currencies, like precious metal, appear unworthy. This has further endangered the financial wellbeing of all who have acted prudently and financially responsible.

Physical Precious Metal: The Achilles Heel of Fraud

As the interest rate swap mechanism is used to corral interest rates – so are gold futures contracts on exchanges like COMEX and the London Bullion Market Association [LBMA] used to suppress the price of the U.S. Dollar’s number one competing currency alternative - gold.

The reality is that metals exchanges, like those identified above, have sold as much as 100 times, or in some case much more, paper ounces or promises of gold in the form of receipts than they have physical bullion available for delivery in their vaults.

There is plenty of documented proof available [even in the conflicted, dinosaur financial press] that conduits for procurement of physical precious metal like national mints have been choked or suspended for prolonged periods of time over the past few years for investment grade physical gold and silver bullion coins. These shortages have always been characterized by, or in, the dinosaur financial press as being the result of issues specific to the retail trade – like not enough gold or silver “blanks” available – from which bullion coins are stamped.

These reported bottlenecks fly in the face of anecdotal reports by the likes of major industry players such as Sprott Asset Management principal, Eric Sprott, who has attempted to bring an air of transparency to these opaque markets. In reporting on difficulties and delays his firm has encountered, procuring institutional amounts of physical silver bullion – Eric Sprott has reported that institutional amounts of silver bullion RECEIVED – was virtually all smelted AFTER it was bought and paid for.

The delays and difficulties receiving bought-and-paid-for physical silver bullion relayed by Eric Sprott over the past year are INCONSISTENT with the waterfall declines [sewering] of paper-silver-prices on highly conflicted and suspect exchanges like COMEX and also inconsistent with the notion that physical silver bullion shortages are strictly a retail phenomenon. The derivatives that trade on exchanges, supposed to reflect or aide in price discovery, are increasingly being used as tools of price manipulation.

Regaining control and the reinstatement of integrity to our capital markets requires market participants to continue saying “NO” to paper promises and yes to physical bullion.

Focus on M.F. Global

The conflicted nature of the paper derivatives exchanges like COMEX / CME and their regulators has recently been brought into disrepute through the collapse of commodity broker M.F. Global and subsequent revelations by the likes of commodity industry mavens Gerald Celente and Ann Barnhardt.

Celente, as a client of M.F. Global who wanted to exercise his COMEX gold futures contracts to take delivery of physical gold bullion – was denied his contractual rights when M.F. Global declared bankruptcy. He was screwed out of - not only his money in a supposedly secure segregated brokerage account – but his contractual rights to procure physical gold bullion at an agreed price.

Ann Barnhardt had a different experience. She was the principal of a brokerage firm which specialized in trading cattle futures – whose expressed purpose was to aide cattle farmers in hedging their on-the-hoof live cattle exposure. Recognizing the M.F. Global bankruptcy for what it really is – Barnhardt chose to close her own brokerage and return her client monies for fear that that the risk of confiscation of funds was an inherent and unacceptable risk for her to expose her clients to.

Ms. Barnhardt has become a hero of mine – correctly identifying the major exchange participants like Jon Corzine – former head of M.F. Global, former Democrat Senator and Governor of New Jersey and former Goldman Chairman, along with J.P. Morgan chief Jamie Dimon and regulators at the C.F.T.C. like Gary Gensler – another former Goldman lieutenant under Corzine, as being criminally responsible for breach of trust to investors and irresponsible actions threatening to destroy the integrity and confidence in our financial markets.

Barnhardt makes special note of how Jon Corzine was complicit in seeing to it that M.F. Global’s bankruptcy was filed as that of a securities dealer – with 4 thousand securities clients – versus that of a commodities dealer – with 40 thousand commodities clients – ALL so creditors like J.P. Morgan would have first call on the residual value of liquidated M.F. Global assets – leaving segregated commodity account holders of M.F. Global – screwed!!!

Ms. Barnhardt emphatically believes that Corzine’s and J.P. Morgan’s actions were pre-emptive, provocative and implemented with intentional malice toward commodities clients.

Subsequent to M.F. Global’s bankruptcy filing, it is a fact that the aggregate of all of the physical precious metal due to be delivered by M.F. Global to their clients – almost to the ounce - appeared as a “book entry” into the registered holdings of none other than J.P. Morgan.

This would appear to strongly support the notion that the M.F. Global debacle was physical, precious metals related or centric.

Ms. Barnhardt states on her blog,

“It is absolutely amazing to me, and frankly awful, that these interviews I do are so popular. Most interviews or radio programs I do wind up being the most popular (or top-three) for their respective program or host. And we talked about my "Going Galt" letter being #6 for ZeroHedge yesterday. Don't think for a second that I relish in any of this. The truth is, I find it very, very disturbing, as should all of you, that I, relatively insignificant me, am apparently one of the only people in Western Civilization who has the stones to simply state the OBVIOUS OBJECTIVE TRUTH. I am a minor cultural phenomenon because I basically say that one plus one equals two, and I can say it clearly and directly without a bunch of "uhs" and "ums" and "you knows".

Really? So all a person need do in this culture to be some sort of a hero is be able to string three articulate sentences together which state the obvious? God help us.

I have many detractors who say, "Who the hell is this chick and why the hell do we care what she says?" Yep. I'm right there with you. Where are the billion-dollar fund managers (excepting perhaps Kyle Bass)? Where are the captains and titans of industry? Where are the so-called "leaders"? WHERE IS THE CLERGY??? I'm cynical, but SURELY there must be SOMEONE ELSE who has a brain in their head and a pair in the bag who can speak proper English above a mumble besides me. Anyone? Anyone? My 15 minutes are surely winding down. Someone else is going to have to step up here.”

All I can say is, “Ms. Barnhardt, welcome to our ‘systemically polluted’ capital markets. As a staunch supporter of GATA I’ve been writing about it for at least 8 years. The folks at GATA are very familiar with and have been documenting the systemic abuse of our capital markets since 1998 - LONG before ANYONE ever heard of Kyle Bass and years before the world ever heard of ZeroHedge.”

Maintenance of the Dollar Standard at Any Cost

If anyone still doubts whether or not the Fed and U.S. Treasury have been active in managing outcomes in strategically important markets or outright suppressing the price of gold and rigging the bond market - they might want to take a read of former Federal Reserve Governor, Kevin Warsh’s op-ed of Dec. 6, 2011 in the Wall Street Journal, snippets appended below:

The 'Financial Repression' Trap

“In Capitals Worldwide, Policy Makers Deliberately Obscure Market Prices and Prevent Informed Judgments”

“…Markets are not always efficient, but the market-clearing prices for stocks, bonds, currencies and other assets (like housing) are critical to informing judgments, in good times and bad. Market-determined asset prices often reveal inconvenient truths. But the sooner the truth is revealed, the sooner judgments can be rendered and action taken.

By contrast, government-induced prices send false signals to users and providers of capital. This upsets economic activity and harms market functioning. Markets that rely on governmental participation will turn out to be less enduring indicators of value….”

“….ratings agencies have been rightfully criticized for assigning higher ratings to various financial products than were justified by their fundamentals, yet now we see a dangerous irony: Governments are trying to persuade ratings agencies to assign higher ratings to sovereigns than deserved or justified by market prices. Blaming the ratings agencies for the dysfunction in funding markets will not lower funding costs.”

Warsh’s op-ed reads like a bloody confession! Anyone who reads it should be OUTRAGED!!!! Kevin Warsh is admitting that the finger prints of Government [read: the U.S. Treasury] are ALL OVER our dysfunctional, systemically failing financial markets. Furthermore, it appears that he is attempting to absolve the Fed and the part it has played in the subversion of our capital markets – laying the whole pile of disgusting, corrupt stench at the feet of government. Perhaps this is why Mr. Warsh announced his resignation from the Board of Governors of the Federal Reserve back on Feb. 11, 2011 – with his post not due to expire until January 2018. Who knows, maybe the man grew a conscience?

In any case, make no mistake – the Federal Reserve has acted, lock-step, in cahoots with the sociopaths and sycophants “playing god” at the U.S. Treasury - aiding and abetting the ESF’s nefarious, ruinous interventions in our capital markets. Heck, the former President of the New York Fed, Timothy Geithner, is the sitting U.S. Treasury Secretary.

Manufacturing Is Alive and Well in America

All is not well in America – not by a long shot. America has been taken over through subterfuge in a financial, fascist coup and the perpetrators have installed a police state. America is no longer a nation of laws. Any additional regulation of the financial services industry would be fruitless. There already exists “laws on the books” – to prevent the blatant, criminal price rigging / abuse that has already occurred. The abuse has been allowed to occur by derelict regulators who have vacated [or been bought] their fiduciary duties.

While America’s industrial potential has been largely “off-shored” – their Constitution and Bill of Rights are in tatters but their propensity to manufacture is there – it just manifests itself in different ways:

- Manufactured financial data

- Manufactured cost of capital [int. rates]

- Manufactured gold and precious metals prices

- Manufactured cost of energy

It’s all about control. Derivatives products – well intentioned when they were conceived – have been utilized to prop-up a failing fiat currency / undermine capital through the establishment of a phony, crony, price control grid. As such, derivatives have become very dangerous tools in the hands of a gaggle of miscreant sociopaths – who think, speak and act as if they are doing god’s work - that now occupy the U.S. Treasury / Fed and rule Wall Street.

Got physical gold yet?

By Rob Kirby

http://www.kirbyanalytics.com/

Rob Kirby is proprietor of Kirbyanalytics.com and sales agent for Bullion Custodial Services. Subscribers to the Kirbyanalytics newsletter can look forward to a weekend publication analyzing many recent global geo-political events and more. Subscribe to Kirbyanalytics news letter here. Buy physical gold, silver or platinum bullion here.

Copyright © 2012 Rob Kirby - All rights reserved.

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors before engaging in any trading activities.

Rob Kirby Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.