Sorting Out the Euro-zone Mess

Economics / Euro-Zone Dec 13, 2011 - 06:31 AM GMTBy: John_Mauldin

I had the pleasure of spending the morning and part of the afternoon today with Louis Gave and Anatole Kaletsky at a seminar here in Dallas; and we shared a long lunch, where Europe and China were the topics of conversation. So, with their permission, here is their latest "Five Corners," in which Charles Gave and Anatole Kaletsky discuss last week's summit, and then engage in an internal debate about whether Italy really has a significant trade deficit with Germany. As I expect from GaveKal, it's not your typical analysis. And since I have to run to dinner – and glean more insights from their team (there will be homework when I get back!), this introduction to Outside the Box is short, and we can jump right into today's piece. Have a great week.

I had the pleasure of spending the morning and part of the afternoon today with Louis Gave and Anatole Kaletsky at a seminar here in Dallas; and we shared a long lunch, where Europe and China were the topics of conversation. So, with their permission, here is their latest "Five Corners," in which Charles Gave and Anatole Kaletsky discuss last week's summit, and then engage in an internal debate about whether Italy really has a significant trade deficit with Germany. As I expect from GaveKal, it's not your typical analysis. And since I have to run to dinner – and glean more insights from their team (there will be homework when I get back!), this introduction to Outside the Box is short, and we can jump right into today's piece. Have a great week.

Your feasting on information analyst,

John Mauldin, Editor

Outside the Box

JohnMauldin@2000wave.com

Sorting Out the Euro Mess

By Anatole Kaletsky, Charles Gave, Francois Chauchat – GaveKal

Starting With the Bad News...

Although the usual post-summit rally should not be too hard to orchestrate in the thin markets around Christmas, there was more bad news than good for the dwindling band of bureaucrats and politicians who are determined to save the Euro, regardless of the costs to the democracies and economies of Europe. We will begin with the "bad" news–partly because our bias is to treat bad news for the Euro as good news for the world and Europe, but mainly because this so-called comprehensive and final "fiscal compact" was no more comprehensive and final than any of the previous failed deals. As in all the previous summits, the only truly definitive decision on Friday was to have another meeting in three months' time, when a new agreement would supposedly be cooked up to resolve all the controversial issues left undecided on Friday. Once the holiday season is over and investors start to think seriously about this "fiscal compact," the economic and political uncertainties are bound to intensify, building to another crisis ahead of the next summit in March.

The summit failed to satisfy the first (and maybe not the second?) of even the minimum necessary conditions to give the Euro a chance of medium-term survival. These are (i) creation of a fiscal union, which will take at least one to two years to set up, and (ii) unlimited ECB lending to bridge the gap between this multi-year political timetable and a market timescale measured in weeks or months. While the ECB may still end up being more pro-active than Mario Draghi suggested last week (see next page), the summit's most obvious failure was on the fiscal front. Despite the self-

congratulation among EU politicians about their "fiscal compact," the fact is that Germany vetoed the most important characteristic of a true fiscal union, which is some degree of joint responsibility for sovereign debts. Since Germany refused even to discus Eurobonds or a vastly expanded jointly-guaranteed European Stability Mechanism, the summit did nothing to reassure the savers and investors in Club Med countries that their money will be protected from either devaluation or default.

Secondly, the summit raises huge political uncertainties. With the UK failing to climb on board, an intra-governmental deal will need to be arranged outside the EU legal framework. Will all 17 countries in the EMU ratify the new treaty and how long will this take? Will Ireland be able to avoid a referendum in a period when Europe is viewed by the public as a hostile colonial power? Will all 17 members insert German-style debt-brakes into their constitutions to the satisfaction of the German courts? If a country fails to legislate or implement an adequate debt-reduction programme, will it be expelled from the Euro? If so, can the Euro be described as "irrevocable" any longer and does it really differ from any previous fixed currency peg? Worst of all, perhaps, how will this deal affect French politics? If Marine Le Pen and Francois Hollande denounce Merkozy's "fiscal compact" as a betrayal of French sovereignty and democracy, then this agreement will be worthless until after the French presidential election on May 6.

Thirdly, and most decisive in the long run, is the economic and political incoherence of what Merkozy are trying to do. Even if the fiscal compact could be immediately put into practice, even if it contained provisions for joint-liability debts and even if the ECB backed it with unlimited monetary support, it would aggravate the Club Med's economic nightmare of unemployment and economic stagnation. Small open economies such as Ireland and Sweden may be able to deflate their way out of a debt crisis, but for large continental economies in the Eurozone this is arithmetically impossible. In this respect at least, Keynes's key insight of the 1930s—that workers and taxpayers are also customers—remains as relevant today as it was then. By imposing permanent austerity, the fiscal compact guarantees permanent depression—and that in turn guarantees that the citizens of Europe will eventually turn against Merkozy and the Eurocrat elites.

...And Now for the Good News

Now let us turn to the good news, at least for the Eurocrats and perhaps, in the short-term, for the European markets. The potential support from the ECB is the one part of the summit deal that could turn out to be much stronger than it seemed at first sight. While Mario Draghi's public statements were less than helpful, they were presumably directed at a German audience, as was Bundesbank president Jens Weidman's astonishing decision on Thursday to vote against even a -25bp rate cut. This seemed to confirm our longstanding view that, whatever the preferences of Angela Merkel and other politicians, the Bundesbank would like to sabotage the Euro if it can. Behind this macho posturing, however, the ECB may be moving towards a programme of sovereign debt monetisation and quantitative easing on a scale that even Ben Bernanke and Mervyn King would never contemplate.

The three-year unlimited liquidity operations announced last Thursday could provide infinite monetary support for European banks and through them, their sovereign debt markets. Once these three-year repos get started, banks in the Club Med countries will be able to borrow as much as they want from the ECB at 1% and use this money to buy government bonds now yielding 6% or more. Because of the unprecedented maturity of these repo-operations, banks will now be able to theoretically acquire unlimited government bond portfolios without exposing themselves to rollover or maturity risks. Banks will therefore be able to pick up 500bp of carry, with zero risk-weightings, by hoovering up all the debt their governments can throw at the markets. Of course there would be risks—we cannot say banks will want to jump on this deal, but in theory they can.

This Ponzi scheme could potentially result in an even bigger money-printing operation than anything the US, British and Swiss central banks have done on their own accounts. It would allow the banks to rebuild their equity with no dilution to shareholders. And if the banks in Italy or Greece became too "profitable" by using cheap ECB funding to buy up their entire sovereign debt markets, then the Italian or Greek governments could always recover the "excess" profits with special taxes. The governments could thus effectively reduce their own cost of funds to the 1% rate offered to banks by the ECB. Of course if the Italian government defaulted on its debts, Italian banks would go spectacularly bust. But these banks would go bust anyway if the Italian government ever defaulted. All the incentives for Italian bank management will therefore be to go for broke in their sovereign debt markets, making maximum use of the new ECB credit lines.

That said, however, the European Banking Authority's recent stress tests forced banks to assume mark-to-market losses in the stressed scenarios. These demands from the EBA may inhibit banks from adding more sovereign risk—unless the EBA uses the "fiscal compact" as an excuse to ease up on the stress tests.

And it is crucial to remember that banks are likely to use the ECB credit lines only to buy the bonds of their own national governments, partly in response to political pressures but also for prudential reasons. If the Euro were ever to break up, Unicredit would not want to own any Greek or Spanish debt, since this would entail unpredictable currency risks. An Italian bond, by contrast, would be redenominated into the new Lira and would be matched perfectly against Unicredit's borrowings from the Bank of Italy, which would also be redenominated into Lira.

Thus, the result of the ECB's covert QE via the banks will be gradually to re-nationalise the banking systems and the sovereign debt structures in Europe. This process will help Club Med countries avoid sovereign debt defaults, but it will make eventual breakup of the euro much less painful– and therefore more likely.

The Long March of the Euro Communist Economies

As we look forward to the coming year, we can bet our bottom drachmas that French and Italian trade deficits are going to continue to crater. Industrial production in most European countries will continue falling (who will invest given the uncertainty and the constant changing rules?). Unemployment is going to go ballistic.

This is because Europe's problem is fundamentally not one of excess debt (look at how Japan, the UK or the US are dealing with debt). The true problem is that half of Europe is uncompetitive and falling into debt traps (see page 5). As a result, budget deficits are going to explode. Remember that Greece after the first fix was supposed to grow in 2011?With hindsight, this looks like quite a joke. Though not a very funny one.

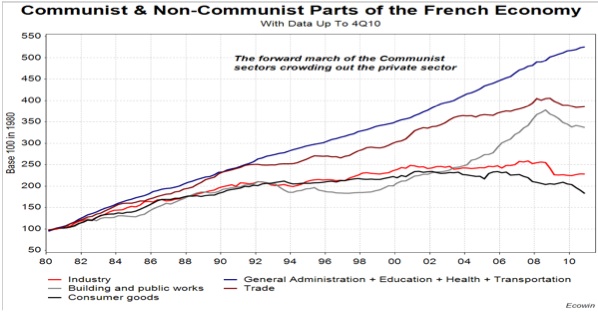

Nearly a decade ago, in the ad hoc Communist France vs Capitalist France (or in French the book Des Lions menes par des Anes), I wrote about the growing weight of government sectors (and employment) in the economy of France. It seems to me that everything that happened in the latest EU summit was about saving the "communist economy" (by guaranteeing its financing at a low rate); even if that meant sacrificing the "capitalist economy".

It is also hard for me to imagine that much in the way of reform will actually take place—why should one reform if money is readily available from one's domestic banks? Because we have signed on to a tougher, tighter fiscal treaty? We did not even manage to respect the previous, easier, treaty. Why assume that it will be any different this time? Fool me once, shame on you; fool me twice...

The media all over the world, but especially in France, are presenting the crisis as a financial one, as if the governments and the politicians have no responsibility. This crisis is in fact very typical of a communist system arriving at the end of its ability to borrow and make the productive system service the debt it has accumulated, simply because the productive sector is going bust.

And nowhere is it more visible than in France. The "communist sectors"—which I define as the sectors in which there are no market prices and lifetime employment—have grown remorselessly since 1980. The market sectors are falling by the wayside one after the other as everybody can see:

This is not a banking crisis but a political crisis, and as Toynbee wrote, political crises always occur when the elites have betrayed. For reasons that I have never really understood, such crises tend to end either with reforms (in countries where people drink beer) or in revolutions (where people drink wine). As far as France is concerned, it seems to me that we drink both, but with a marked preference for wine.

Have Southern Europeans Bought Too Many BMWs?

We are often being told that the first decade of the Euro led to artificially low rates in the South, which provoked a credit-led consumption boom that allowed the poor guys in Valencia or Lecce to buy a BMW. This story is supposed to provide a colorful illustration of the intra-Eurozone imbalances accumulated over the last decade. Yet, as we show below, the deterioration of the Southern European trade balances with Germany has accounted for a relatively modest part of the rise of their trade deficits. More importantly, the story misses the essential point about the main cause of these deficits.

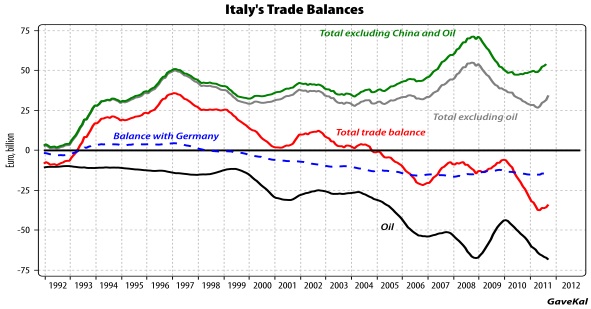

Take the example of Italy. Italy had a €25bn trade surplus when the Euro was introduced in January 1999, and has a €35bn trade deficit now—that is a €60bn swing. Germany has accounted for €13bn, or 22% of the total deterioration, and this was in part caused by declining German imports during the first half of the last decade. But as the chart below illustrates, the bulk of the deterioration of Italy's trade deficit came from oil first (€60bn since 1999), and China second (€20bn). Excluding China and oil, Italy today runs a comfortable trade surplus that is almost twice as high as it was in 1999 in nominal terms, and that has remained roughly stable as % of GDP (3% to 4%).

Thus, the idea that the rise of Southern European trade deficits was essentially due to (or reflected in) intra-Eurozone trade imbalances is largely a myth. The additional consumption of Italian and Spanish households benefitted oil-producing countries, China and other Asian countries first and foremost. And viewed from the German side of the equation, only 13% of the rise of German exports of the last decade went to Southern Europe.

Most observers and analysts now tend to interpret everything that has happened in the Euro area during the last decade as a consequence of the Euro experiment. But they hugely underestimate the fact that the rise of China during this same decade, and the accompanying explosion of commodity prices, has had even more impact on the Eurozone economies than the monetary union. This is especially true of trade development in Southern Europe.

Looking at the trade deficits in Italy and Spain, we can see that their main challenge is not to regain competiveness against German producers, but to reduce their dependency on oil imports (through the development of solar energy, for example). This will obviously take its time, and in the meantime the deleveraging Southern European countries will begin (Italy) or continue (Spain, Portugal, Greece) to improve their current account balance through lower import volumes. This would have to take place even if they left the Euro and devalued. We doubt, however, that BMW will prove to be the main victim of this inevitable development.

The Triumph of Southern Italy over Northern Italy

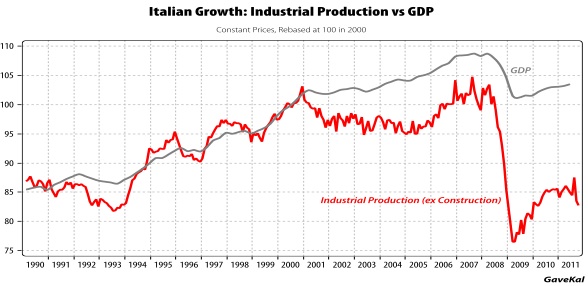

On the previous page, my colleague argues that Italy's balance of payments problem is not caused by the Euro, but instead by the China factor and rising commodities prices. Besides the fact that Italy would have better adjusted to the pressures of a rising China and higher commodities prices were it not for its artificially high foreign exchange rate under the Euro, this theory fails to explain Italy's disappearing industrial sector.

As the chart below shows, up to 2000 Italy's industrial production and GDP grew roughly at the same rate. Then the Euro was invented, and Italian GDP growth has basically flat-lined. But the situation was far worse for the country's industrialists as these days IP is some -15% lower than 2000 levels:

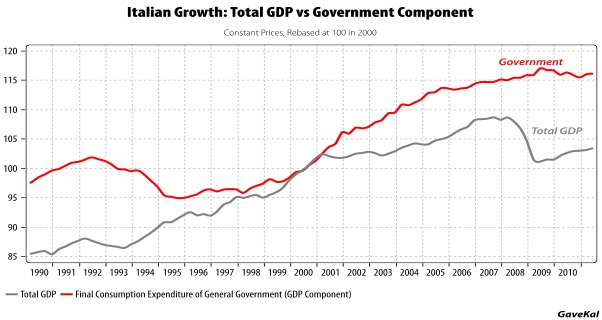

This dichotomy reveals a very sad reality—that the relative stability of GDP in Italy is thanks only to the relentless growth of the public sector:

The industrial production index gives thus a perfectly good representation of the state of the private sector in Italy—it is going out of business. Meanwhile, the free loaders' economy of southern Italy has won the day. Unfortunately, the bill will have to fall on Northern Italy. And needless to say, if you tax Northern Italy a little more every year for the primary surplus to remain a surplus, Northern Italy grows even less, which means that the following year, you need to tax Northern Italy a little more...eventually Rocco and his brothers in the South will also find themselves in trouble.

So the Euro has in fact led to the triumph of Rome and Southern Italy over Northern Italy and of course of the rentier over the entrepreneur. Is it sustainable? No more than the Soviet Union was...

By John F. Mauldin

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-rial sector.

As the chart below shows, up to 2000 Italy's industrial production and GDP grew roughly at the same rate. Then the Euro was invented, and Italian GDP growth has basically flat-lined. But the situation was far worse for the country's industrialists as these days IP is some -15% lower than 2000 levels:

This dichotomy reveals a very sad reality—that the relative stability of GDP in Italy is thanks only to the relentless growth of the public sector:

The industrial production index gives thus a perfectly good representation of the state of the private sector in Italy—it is going out of business. Meanwhile, the free loaders' economy of southern Italy has won the day. Unfortunately, the bill will have to fall on Northern Italy. And needless to say, if you tax Northern Italy a little more every year for the primary surplus to remain a surplus, Northern Italy grows even less, which means that the following year, you need to tax Northern Italy a little more...eventually Rocco and his brothers in the South will also find themselves in trouble.

So the Euro has in fact led to the triumph of Rome and Southern Italy over Northern Italy and of course of the rentier over the entrepreneur. Is it sustainable? No more than the Soviet Union was...

By John F. Mauldin

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-rial sector.

As the chart below shows, up to 2000 Italy's industrial production and GDP grew roughly at the same rate. Then the Euro was invented, and Italian GDP growth has basically flat-lined. But the situation was far worse for the country's industrialists as these days IP is some -15% lower than 2000 levels:

This dichotomy reveals a very sad reality—that the relative stability of GDP in Italy is thanks only to the relentless growth of the public sector:

The industrial production index gives thus a perfectly good representation of the state of the private sector in Italy—it is going out of business. Meanwhile, the free loaders' economy of southern Italy has won the day. Unfortunately, the bill will have to fall on Northern Italy. And needless to say, if you tax Northern Italy a little more every year for the primary surplus to remain a surplus, Northern Italy grows even less, which means that the following year, you need to tax Northern Italy a little more...eventually Rocco and his brothers in the South will also find themselves in trouble.

So the Euro has in fact led to the triumph of Rome and Southern Italy over Northern Italy and of course of the rentier over the entrepreneur. Is it sustainable? No more than the Soviet Union was...

By John F. Mauldin

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-rial sector.

As the chart below shows, up to 2000 Italy's industrial production and GDP grew roughly at the same rate. Then the Euro was invented, and Italian GDP growth has basically flat-lined. But the situation was far worse for the country's industrialists as these days IP is some -15% lower than 2000 levels:

This dichotomy reveals a very sad reality—that the relative stability of GDP in Italy is thanks only to the relentless growth of the public sector:

The industrial production index gives thus a perfectly good representation of the state of the private sector in Italy—it is going out of business. Meanwhile, the free loaders' economy of southern Italy has won the day. Unfortunately, the bill will have to fall on Northern Italy. And needless to say, if you tax Northern Italy a little more every year for the primary surplus to remain a surplus, Northern Italy grows even less, which means that the following year, you need to tax Northern Italy a little more...eventually Rocco and his brothers in the South will also find themselves in trouble.

So the Euro has in fact led to the triumph of Rome and Southern Italy over Northern Italy and of course of the rentier over the entrepreneur. Is it sustainable? No more than the Soviet Union was...

By John F. Mauldin

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-rial sector.

As the chart below shows, up to 2000 Italy's industrial production and GDP grew roughly at the same rate. Then the Euro was invented, and Italian GDP growth has basically flat-lined. But the situation was far worse for the country's industrialists as these days IP is some -15% lower than 2000 levels:

This dichotomy reveals a very sad reality—that the relative stability of GDP in Italy is thanks only to the relentless growth of the public sector:

The industrial production index gives thus a perfectly good representation of the state of the private sector in Italy—it is going out of business. Meanwhile, the free loaders' economy of southern Italy has won the day. Unfortunately, the bill will have to fall on Northern Italy. And needless to say, if you tax Northern Italy a little more every year for the primary surplus to remain a surplus, Northern Italy grows even less, which means that the following year, you need to tax Northern Italy a little more...eventually Rocco and his brothers in the South will also find themselves in trouble.

So the Euro has in fact led to the triumph of Rome and Southern Italy over Northern Italy and of course of the rentier over the entrepreneur. Is it sustainable? No more than the Soviet Union was...

By John F. Mauldin

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-rial sector.

As the chart below shows, up to 2000 Italy's industrial production and GDP grew roughly at the same rate. Then the Euro was invented, and Italian GDP growth has basically flat-lined. But the situation was far worse for the country's industrialists as these days IP is some -15% lower than 2000 levels:

This dichotomy reveals a very sad reality—that the relative stability of GDP in Italy is thanks only to the relentless growth of the public sector:

The industrial production index gives thus a perfectly good representation of the state of the private sector in Italy—it is going out of business. Meanwhile, the free loaders' economy of southern Italy has won the day. Unfortunately, the bill will have to fall on Northern Italy. And needless to say, if you tax Northern Italy a little more every year for the primary surplus to remain a surplus, Northern Italy grows even less, which means that the following year, you need to tax Northern Italy a little more...eventually Rocco and his brothers in the South will also find themselves in trouble.

So the Euro has in fact led to the triumph of Rome and Southern Italy over Northern Italy and of course of the rentier over the entrepreneur. Is it sustainable? No more than the Soviet Union was...

By John F. Mauldin

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.