ECB Expected to Unleash QE Money Printing after Launching of Euro-Bonds

Interest-Rates / Quantitative Easing Nov 29, 2011 - 01:10 PM GMTBy: Gary_Dorsch

Hardly a week goes by, without a major summit between German Chancellor Angela Merkel and French President Nicolas Sarkozy, trying to devise another clever scheme to save the Euro. Yet after 1-½ years of trying to contain the wildfire, - the Euro-zone's debt crisis is more dangerous than ever. The collapse of Greece's €360-billion bond market, now trading at 26% of face value, has triggered contagion sales from periphery of the Euro-zone - Greece, Ireland and Portugal, and into the next upper tier of the Euro-zone, namely, the bond markets of Spain and Italy, which together owe €3-trillion of debt.

Hardly a week goes by, without a major summit between German Chancellor Angela Merkel and French President Nicolas Sarkozy, trying to devise another clever scheme to save the Euro. Yet after 1-½ years of trying to contain the wildfire, - the Euro-zone's debt crisis is more dangerous than ever. The collapse of Greece's €360-billion bond market, now trading at 26% of face value, has triggered contagion sales from periphery of the Euro-zone - Greece, Ireland and Portugal, and into the next upper tier of the Euro-zone, namely, the bond markets of Spain and Italy, which together owe €3-trillion of debt.

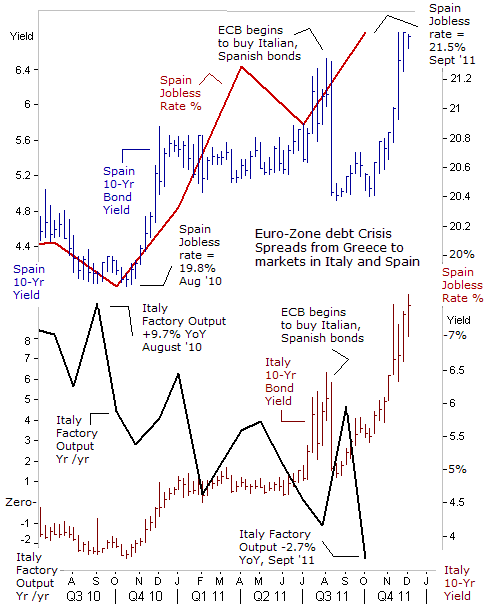

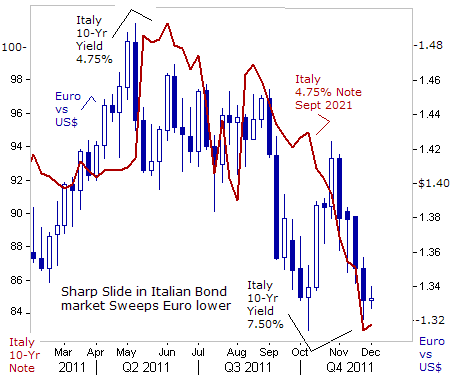

Even after Spain's right-wing Popular Party routed the social democrats in a national election and assumed power, pledging even more severe austerity measures, - Spain's borrowing costs continued to ratchet higher. The yield on Spain's ten-year bonds approached 7% last week, a level considered prohibitively high enough to topple the Euro-zone's fourth largest economy into a depression in 2012. Despite assurances from Italy's new Prime Minister Mario Monti of new austerity measures, Italy's 10-year yield hit 7.50% last week, a 15-year high.

The newly installed governments of Greece, Italy and Spain are promising to imposed deeper spending cuts, further layoffs of public workers, and raising taxes, - all measures that can push their economies into a deep recession. However, as the Wall Street Journal noted on Nov 21st, "Whether the ECB decides to boost its bond-buying or not, investors seem to be coming to the conclusion that any true solution to the European debt crisis will be a years-long process in which governments will be asking electorates to accept enormous sacrifices, in the form of entitlement cuts and tax increases, as well as weak growth and high unemployment."

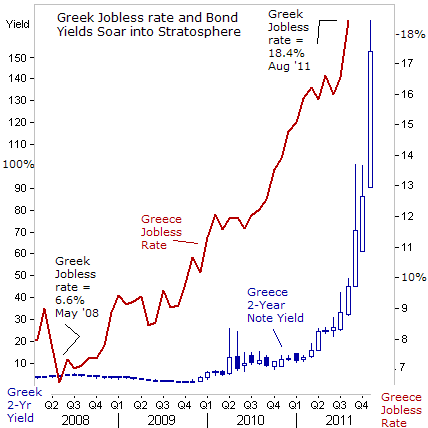

The origins of the Euro-zone debt crisis began in the Greek bond market. Traders began to realize that Greece's small workforce of 6-million wage earners couldn't possibly payback €360-billion ($478-billion) of debt that was accumulated by the crooked politicians in Athens. Last year, Greece's total debt increased to 142% of gross domestic product (GDP). This year, it's expected to reach 160-percent. Yet it's nearly impossible for a government to run a budget surplus when its economy is shrinking, and tax revenues are falling.

In 2010, Greece's economic output fell by -4.5% and roughly 65,000 private companies declared bankruptcy. More than 200,000 people lost their jobs. The situation has gotten much worse this year. Greece's jobless rate hit a record high of 18.4% in August. The country is suffering from painful austerity measures demanded by foreign lenders. The jobless rate for workers in the 15-24-year category reached 43.5%, twice its level three years ago, and is a tinderbox that could explode at any moment. Greece's economy is now seen shrinking for a fourth consecutive year in 2011, at an annual pace of -5.5-percent.

At the same time, foreign lenders refuse to lend money to Greece. The rating agencies have downgraded the country so low that Athens must pay 152% for two-year bonds.If the EU and IMF hadn't agreed to cover Greece's €110-billion borrowing needs thru 2013, Athens would've already declared state bankruptcy. This would've resulted in massive losses for the European banking Oligarchs and Euro-zone governments that hold the toxic debt.

Under the guidance of Berlin and Paris, a large portion of Greece's toxic debt has already been clandestinely shifted from the portfolios of the banking Oligarchs, and dumped into the hands of the Euro-zone taxpayers. In 2009, private banks held 100% of Greek public debt. However, through backdoor bailouts arranged by the IMF, the Euro-zone's Financial Stability fund and the ECB, much of the toxic debt is being transferred from the books of the banking Oligarchs to public hands. Bankers will probably still hold about €180-billion of Greek debt by the end of 2013, compared to just under €300-billion in 2009.

It's highly doubtful that Greece's downtrodden workers would agree to remain slaves to Europe's Oligarchic bankers for long. Athens is now demanding that its lenders write-off three-quarters of the debt owed, in a new restructuring deal. The alternative is for Greece to abandon the European monetary system and reintroduce the drachma as its national currency. That would bankrupt the Greek banks and pension funds that have loaned the Greek state €75-billion. The export sector would see little benefit from devaluation, as exports contribute only 7% of GDP. Most likely, the introduction of the drachma would result in hyper inflation, and decimate the living conditions of broad layers of the population. For Greece, there are no good choices to choose from in Dante's Inferno.

Up until now, the Franco-German strategy for dealing with the sharp decline in the Euro-zone bond markets has been the same prescription employed by the IMF when lending to foreign governments. The EU has demanded brutal austerity measures that make the working class pay the heavy price for bailout money, that goes into the coffers of the banking Oligarchs, and not into the local economies of the impoverished workers. The result is higher unemployment among broad layers of the population amid a deepening economic slump, a sharp fall in tax revenues, and a worsening of the debt crisis.Berlin and Paris now aim to force Athens into selling off the country's crown jewels at fire-sale prices, in return for the bailout loans.

Italy and Spain are trying to pare down their running debt balances through painful austerity measures, but the results are record high unemployment of 21.5% in Spain, and a sharp plunge in Italy's industrial output. Yet the banking Oligarchs are still driving the borrowing costs of Italy and Spain sharply higher, - to their highest levels in 15-years. In turn, the Euro-zone's third and fourth largest economies are at great risk of slipping into a deepening recession. This in part reflects the intention of the Oligarchic banks to ratchet up the pressure on the new governments to follow their dictates. Bank traders are jacking- up bond yields in order to create the impression of a full blown crisis that will scare the European Central Bank (ECB) and Berlin into dropping their opposition to full scale "quantitative easing," (QE), - the ECB's unlimited purchasing of the toxic debt on the secondary markets.

To prepare the groundwork for full scale QE, - the monetization of toxic debts, - the political cronies in Berlin and Paris are maneuvering towards a new arrangement that would blackmail member states of the Euro, into surrendering their sovereignty over fiscal policy. Meeting with French president Nicolas Sarkozy and the new Italian Prime Minister Mario Monti on Nov 24th, Germany's Merkel presented proposals for changes in the EU treaties within a few days. The aim is to give Brussels the means to enforce even harsher austerity measures, - such as deeper spending cuts and higher taxes, without giving a political voice to the working class that must endure the austerity measures. Those who violate the Stability and Growth Pact "must be called to account," and sanctioned, Merkel insisted.

According to recent reports, Merkel and Sarkozy have apparently agreed that if member states want to remain in the Euro monetary system, they must surrender their national sovereignty over spending and tax policies. Republican presidential candidate and former House Speaker Newt Gingrich commented on Nov 4th, "The European system is designed to block the people from having power. The elites in Europe work very hard at controlling the European people by indirect means. And it's only when you get to referendums that you see how decisively the people of Europe are unhappy with the current governments," he said. Having already surrendered their national currencies and decisions about interest rates to the ECB, it would be a fateful step to surrender fiscal policy.

In return for surrendering fiscal policy to Brussels, - Berlin and Paris, the key paymasters of the Euro-zone, would agree to the creation of a common Eurobond that would pool the credit ratings and collateral of all participating Euro-zone countries into a single fixed income instrument. Chancellor Merkel says that German borrowing costs will jump higher because of the creation of a Eurobond, though she is prepared to consider Eurobonds, if the legal framework is in place to ensure all countries in the zone observe the rules.

What Merkel wants to see at the December 9th EU summit is greater harmony of fiscal policies in the Euro-Zone, backed by legally enforceable rules of financial discipline. These would include automatic sanctions on countries that violate the existing rules, - such as annual budget deficits of member states cannot exceed 3% of GDP and that total public debt should be no more than 60% of the GDP. Every Euro-zone country has breached these rules.

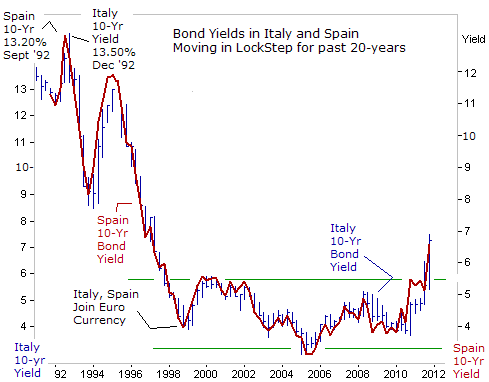

However, if big debtor nations such as Greece, Ireland, Portugal, Spain and Italy refuse to surrender their sovereignty over fiscal policy to Brussels, - the alternative could be the situation that Greece now finds itself - purgatory. About 19-years ago, the governments of Italy and Spain had to pay more than 13% for borrowing funds for ten years. Since joining the Euro currency however, 10-year bond yields for Italy and Spain averaged around 4.50%, until contagion sales from Greece reached their borders in the summer of 2011.

Once fiscal integration is agreed upon, Berlin is expected to agree to the creation of Eurobonds issued by member states that could be purchased in massive quantities (monetized) by the ECB. Countries would be liable for each others' debts, but the ECB could make much of their debt disappear with its electronic printing press. Eurobondswould either be financed with higher taxes on the working class, through austerity measures, or through the inflationary effects of the ECB's money printing machine. With French banks alone holding more of their debts than the entire €440-billion European Financial Stabilization Fund, a default by these countries would likely bankrupt the French financial system. Thus, Paris has been pushing hard for the ECB to monetize debt on a massive scale.

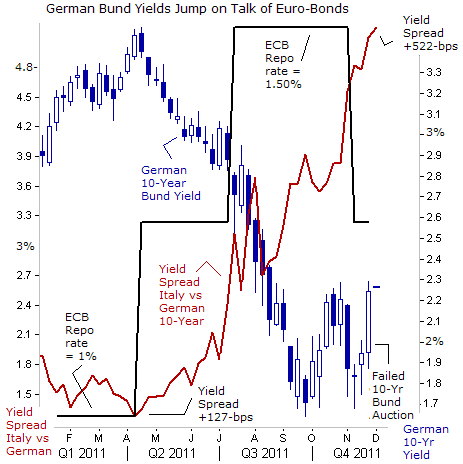

Once the ECB has the assurance that the Eurobonds are backed by a fiscal union, it could be ready to go all out, and easily buy 2-3-trillion Euros worth at anytime. Still, borrowing costs for existing German bunds would probably climb higher while interest rates for existing Italian debt might fall. Currently, Italy's 10-year note yields +524-basis points more than German yields, but that spread could narrow, if Italy surrenders its fiscal sovereignty, as a way for the ECB to guarantee Italy's debts. The ECB could promise to buy unlimited amounts of existing Italian bonds, should yields should rise to a certain identified level. Knowing that the ECB is ready to enforce a safety net under the Italian bond market, through massive intervention, could calm the situation and restore stability to the Milan stock exchange.

One of the alternative schemes that is under discussion is for the ECB and central banks in China, Japan, and elsewhere to lend to the International Monetary Fund, which in turn, could use the money to lend to Euro zone countries under market stress.This would help the ECB side-step the legal problem of financing governments and also help impose IMF-type austerity on the recipients of the aid -- something the ECB cannot do now. One should never underestimate the scheming ability of Euro-zone politicians, which why the Euro currency itself has not fallen apart, as many analysts had predicted.

Rumors in the media suggest that the IMF is secretly drawing up plans for a €600-billion loan package for Italy. Spain may be offered access to an IMF line of credit, to avoid it being "picked off" by the markets in the coming months. Any IMF involvement in European rescue packages would be partly underwritten by US-taxpayers. In other words, 17% of the IMF's $800-billion bailout is being drawn from the US Treasury, equaling $135-billion of the bailout for Europe's banks. Britain would provide 4.5% of the IMF's funding. Some reports say the Fed might print $135-billion, and secretly lend the dollars to the IMF.

Many experts no longer believe that the Euro can survive in its current form. The weaker debtor nations with less than stellar AAA credit ratings might be booted out of the joint currency regime in the year ahead, unless they agree to surrender their fiscal sovereignty over to Brussels. Extraordinary measures might take place by early next year, including the issuance of "Elite-Six" bonds, backed by six of the Euro-zone's 17 countries that have the top AAA credit rating -- Germany, France, Austria, the Netherlands, Luxembourg and Finland.

The sharply higher bond yields in Greece, Portugal, Ireland, Spain, and Italy, reflects the risk that these countries might be split-off from the Euro currency next year, if they refuse to surrender fiscal sovereignty. Furthermore, their governments might confront an explosive backlash from a desperate working class that won't be able to survive under tougher austerity. Still, the possible split-up of the Euro-zone hasn't hurt the Euro currency in a significant way. At today's level of $1.33, the Euro is still far above last year's low of $1.200. A Euro currency made-up of the Elite-Six, plus a few other subordinates, might prove to be more viable, than a currency plagued by a few bankrupt nations that are on the road to default.

The upward spiral in Italian and Spanish interest rates has all but stopped economic growth in the Euro-zone and in England. The stall comes just when Italy, Spain, and Greece and other nations need growth to help them wriggle out of the chokehold of debt. The Euro zone economy grew just +0.2% in the third quarter as solid +0.5% growth in Germany and France was offset by countries at the epicenter of the debt crisis. Matters are likely to get much worse in the months to come, when Italy, Greece, Ireland, Portugal, and Spain begin implementing austerity measures to stop the bond market from melting down.

The European Commission expects the Euro-zone economy to shrink -0.1% in the last three months of the year and to stagnate in the first quarter of 2012. An outright recession -- two quarters of shrinking output -- is now quite likely. That would be bad news for China, which sells 35% percent of its exports to Europe, and for US Multi-Nationals that earn 20% of their revenues from affiliates that are stationed in the Euro-zone. Even a mild contraction in Europe's economy, which equals 25% of global GDP, can slow growth around the world.

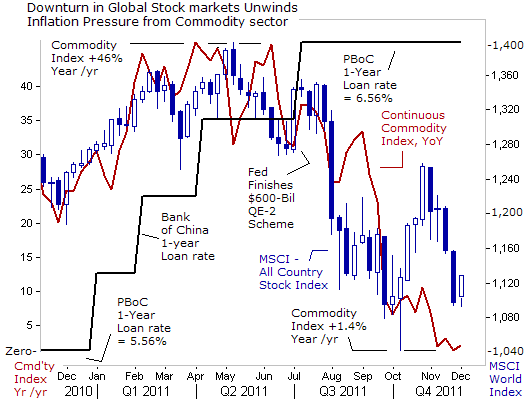

The People's Bank of China tightened its monetary policy in the first half of 2011, lifting its key 1-year loan rate by a total of +100-bps to 6.56%. Combined with weaker exports to Europe, Chinese factory activity fell to its lowest level in 32-months in November, according to a preliminary purchasing managers' survey, reviving worries that China's economy might be skidding towards a "hard landing" and compounding global recession fears. The sub-index for new Chinese factory orders suffered its biggest drop in 1-½-years to sink well below the 50-point mark, suggesting factories received fewer orders on the whole in November.

With the Chinese central bank doing much of the heavy lifting in fighting global inflation, the Continuous Commodity Index (CCI), a basket of 17-equally weighted commodities, tumbled -16% from its record high set on May 1st. Weighed down by a similar -16% slide in the MSCI''s All Country Index, measuring blue-chips companies from 43-stock markets worldwide, the year over year change in commodities has plunged to near zero percent. That's down sharply from as high as +46% in the first half of the year, when inflationary pressures in emerging countries such as Brazil, China, India, and Russia were highly elevated.

In recent years, whenever the annualized rate of inflation in the commodities markets has threatened to go negative, the Bernanke Fed responded with a massive round of money printing, dubbed QE-1 and QE-2. The biggest bond dealers that deal directly with the Fed now say the central bank is poised to start QE-3, injecting even more high powered money into the coffers of the Wall Street Oligarchs by purchasing about $545-billion in mortgage securities. It's an election year, and the Fed aims to help President Obama to win re-election by artificially inflating the value of the stock market with printed money.

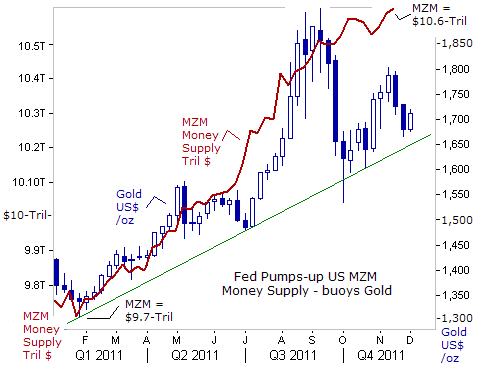

That's also good news for investors in the Gold market. Fed chief Bernanke has pumped-up the high octane MZM money supply to a record $10.6-trillion this month, thus helping to buoy Gold above $1,600 /oz. Dealers expect the Fed to launch QE-3 in the first quarter of 2012. And once Germany and France have established the United States of Europe, and are ready to launch Eurobonds, - the ECB would be expected to launch its own version of QE-1. Commodity and precious metals markets could gyrate wildly, until it becomes crystal clear to the majority of traders, that additional rounds of QE are forthcoming in Europe and the US. Once the money printing schemes are announced, other central banks would probably join the fray with their own version of competitive currency debasement.

China's central bank is expected to start easing its money policy in the first quarter of 2012, which could inject added adrenalin into the Shanghai Gold market, while lifting a broad array of commodities, including crude oil, base metals, and agricultural goods.

This article is just the Tip of the Iceberg of what’s available in the Global Money Trends newsletter. Subscribe to the Global Money Trends newsletter, for insightful analysis and predictions of (1) top stock markets around the world, (2) Commodities such as crude oil, copper, gold, silver, and grains, (3) Foreign currencies (4) Libor interest rates and global bond markets (5) Central banker "Jawboning" and Intervention techniques that move markets.

By Gary Dorsch,

Editor, Global Money Trends newsletter

http://www.sirchartsalot.com

GMT filters important news and information into (1) bullet-point, easy to understand analysis, (2) featuring "Inter-Market Technical Analysis" that visually displays the dynamic inter-relationships between foreign currencies, commodities, interest rates and the stock markets from a dozen key countries around the world. Also included are (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, with the latest news on global markets, and view our updated model portfolio 2008. To order a subscription to Global Money Trends, click on the hyperlink below, http://www.sirchartsalot.com/newsletters.php or call toll free to order, Sunday thru Thursday, 8 am to 9 pm EST, and on Friday 8 am to 5 pm, at 866-553-1007. Outside the call 561-367-1007.

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab's Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR's and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, "Foreign Currency Trends" for Charles Schwab's Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

Copyright © 2005-2011 SirChartsAlot, Inc. All rights reserved.

Disclaimer: SirChartsAlot.com's analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources.

Gary Dorsch Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.