Bernanke's Waterloo; Deflationary Collapse or Inflationary Disaster?

Economics / Deflation Sep 07, 2011 - 06:47 AM GMTBy: Mike_Shedlock

The September Contrary Investor It's A Long Hard Road is an exceptional marriage of debt-deflation concepts, long-wave K-Cycles, credit cycles, and Austrian economic thinking. Here is a lengthy snip of several key points with permission.

The September Contrary Investor It's A Long Hard Road is an exceptional marriage of debt-deflation concepts, long-wave K-Cycles, credit cycles, and Austrian economic thinking. Here is a lengthy snip of several key points with permission.

If there has been one consistent theme since day one at CI, it has been our perhaps near myopic focus and focal point highlight of importance that is the macro credit cycle. Does this play into long wave and perhaps Kondratieff cycle or Austrian economics type of thinking? Call it what you will, but elements of all of these schools of thought very much overlap. Right to the point, we believe THE key thematic construct to keep in mind as a macro cycle decision making overlay and character point dead ahead is the now more than apparent collision of the generational long wave credit cycle with the current short term business cycle of the moment. Without trying to reach for melodrama, this is the first time a multi-decade long wave credit cycle has collided with the short-term business cycle since the late 1920’s/early 1930’s.

Most decision makers and Street seers of the moment have absolutely no experience with this type of a generational collision. Moreover, our illustrious academician Fed Chairman has never even considered long wave or credit cycle based Austrian economics thinking in his and the broader Fed’s policy making – absolutely key and crucial mistake. Although it’s just our perception, this will be Bernanke’s legacy Waterloo. It also tells us directly that his only policy tool ahead will be more money printing.

We suggest to you that macro credit cycle issues did not end in 2009. Certainly Europe is a poster child example of this thinking, but it absolutely also applies to what lies ahead for the domestic US economy. We’ve only had a reprieve from long cycle reconciliation over the last few years due to historically unprecedented Government and Federal Reserve balance sheet levering, which itself is unsustainable longer term. Has the election cycle played havoc with needed deleveraging reconciliation and simple identification of the underlying causes of current circumstances? Without question. Although it’s clearly a personal comment, we’ve been disgusted with the short-term focus and actions of politicians at the expense of longer cycle strategic domestic economic thinking and needed financial reconciliation. These actions simply guarantee the deleveraging process will play out over a longer period than may otherwise have been the case. A very important construct with direct implications for the tone and rhythm of the domestic economy over time.

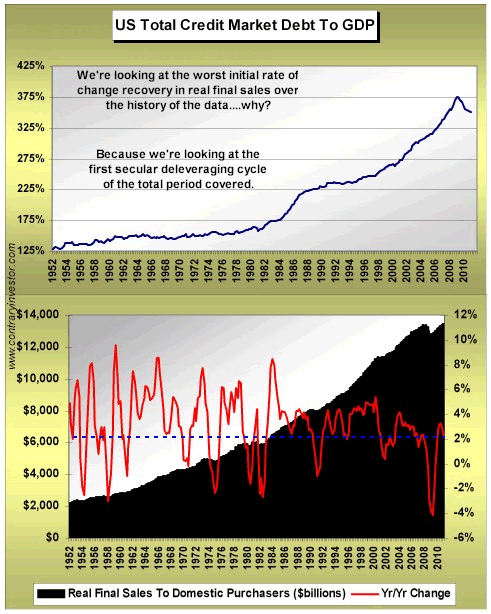

The top clip of the following chart is probably the one graphic we’ve published the most times over our short existence. Total US credit market debt relative to GDP. As is more than clear, the process of total credit cycle reconciliation has barely begun.

The bottom clip of the chart is one you’ve seen a number of times from us and we believe quite important to what lies ahead. To the point, real final sales to domestic purchasers is GDP stripped of the influence of inventories and exports. What we’re left with is as good look at domestic only GDP and as you can see, the year over year change in terms of growth in the current cycle is the weakest of any initial economic recovery cycle over the time in which official numbers have been kept. Message being? We are seeing very weak aggregate demand, exactly as one would expect in a generational credit cycle reconciliation process.

We also need to remember that THE primary goal of the Fed and politicians has been to thwart the generational credit cycle deleveraging process to the best of their abilities while it is occurring, all in the interests of being reelected. So as you look at the bottom clip of the chart above, remember that this is the growth in domestic economic activity in the current cycle that has occurred while the Government has borrowed $5 trillion and used the proceeds for increased transfer payments, cash for clunkers, help for those with mortgage problems, deals for appliances, etc. And yet still we’ve experienced incredibly subdued domestic economic activity. Just what would this have looked like in the absence of historic Government balance sheet leveraging?

Monetary Policy Useless in Deleveraging Cycles

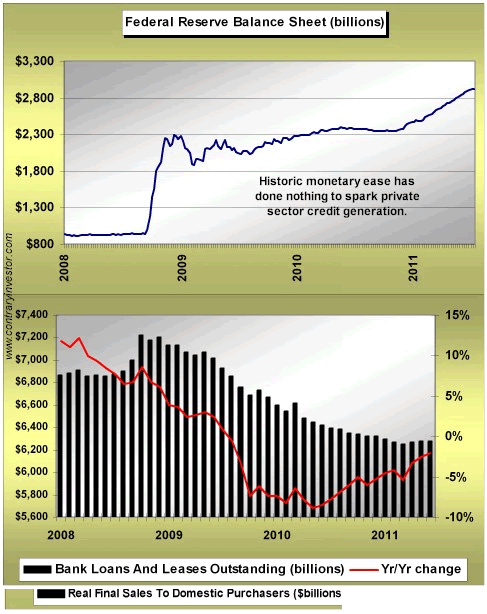

Although it appears obvious conceptually, we're not so sure the markets yet fully appreciate the fact that in true generational deleveraging cycles, monetary policy is powerless to influence credit expansion. Again, our near myopic focus on credit is driven by the fact that credit is the cornerstone of modern economic development and balance, and certainly not just in the US. The character, availability and price of credit regulate the ongoing tone of aggregate demand, so monitoring credit is simply crucial. If credit cannot expand, then neither can aggregate demand. A simple yet key truism, especially in our current circumstances. As you can see below, we've seen literally unprecedented monetary expansion so far in the current cycle, yet private sector credit creation (as is exemplified by the bank loans and leases outstanding) remains wildly subdued at best. The whole pushing on a string thesis? Exactly.

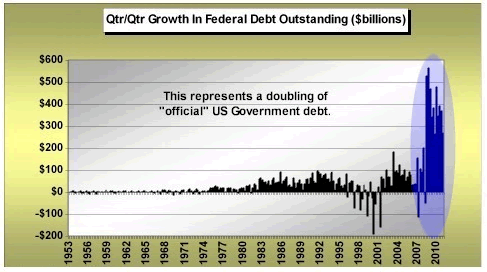

The bottom clip of the chart above has been adjusted for the $450 billion of off balance sheet bank loans that were mandated to arrive back on bank balance sheets as per FASB dictates in April of last year. As is clear, bank loans and leases out since early 2009 have declined significantly. The bulls have trumpeted the growth over the last three months. You can decide for yourself whether this minor uptick is deserving of trumpeting, if you will. To ourselves the message appears absolutely crystal clear. In generational deleveraging cycles, Fed monetary policy is simply a non-event. Rather monetary extravagence finds its way into inflation hedge assets and can be used simply to speculate. Remember, as per Fed monetary largesse, the banks are sitting on $1.5 trillion of excess reserves as we speak. Excess reserves can be used as collateral for derivative and futures trading. You already know trading profits have been a crucial piece of bank earnings since 2009. As of now, monetary policy has been completely ineffective in the current cycle in creating credit - the lifeblood of economic activity and growth - except in one instance. And that instance lies below. Of course we are referring to Government debt.

In typical recessionary periods past, the Fed has been able to lower interest rates and stimulate demand for credit. Demand for credit ultimately stimulates broad economic activity via an increase in aggregate demand. But in deleveraging cycles as opposed to typical business cycles, interest rates can fall to zero and still not positively influence demand for credit. This is exactly what has occurred in the current cycle. You may remember from our discussions over the years we asked one question again and again, "is this a business cycle or a credit cycle?" The only borrower of substance in the current cycle has been the Federal Government, yet we are currently reaching the limits of Government balance sheet expansion tolerance, as clearly witnessed by the debt ceiling melodrama. This has only served to weaken the US as a credit. Again, the inability to generate demand for credit by almost any means (and in our present circumstance historic means) is simply a classic fingerprint of a generational deleveraging cycle.

Bernanke No Student of History

Never in modern history have we faced the type of domestic labor market circumstances we face today. As we've tried to describe, monetary policy is powerless to change this. If Mr. Bernanke was the true student of history he would fully realize exactly the circumstances we've described. It's not that we don't have precedent. The US in the 1930's and Japan over the last two decades are the model. Looking at the Depression years and claiming the issue was that the Fed was not loose enough misses the key fingerprint character points of a generational deleveraging cycle completely. Again, the refusal of Bernanke and friends to even acknowledge Austrian or Kondratieff economic constructs has been and will continue to be their policy making downfall. Who knows, maybe all of this will find its way into the economics textbooks of tomorrow. Let's hope so anyway for future generations. But as the old market saying goes, people don't repeat the mistakes of their parents, they repeat the mistakes of their grandparents.

Government and Fed policy has been aimed at fostering credit creation up to this point. Fed money printing and Government borrowing has been undertaken in an attempt to stimulate credit creation and likewise spark broad reacceleration in consumption. Certainly Government and Fed actions have also been an offset to the contraction in private sector (think financial sector) credit so far in the current cycle. As of now, unprecedented Fed actions have acted to both devalue the dollar and suppress interest rates. But in a generational deleveraging cycle, the Fed is ultimately impotent in terms of being able to successfully spark private sector credit creation that would lead to expansion in aggregate demand and macro GDP growth.

But what has occurred as a result of Fed and Government "solutions" again is a classic macro deleveraging cycle response - a devalued currency and negative real interest rates has driven investors into inflation hedge assets such as gold, oil, ag assets, etc. at the margin. As opposed to having achieved the stated goal of fostering employment growth, credit creation and raising aggregate demand, etc., Fed QE has essentially succeeded in raising the cost of living in a cycle characterized by generational labor market and direct wage pressure among the middle and lower class wealth demographic. From a broad perspective, has Fed and Government policy actually done more harm than good? It simply depends where one sits amidst the wealth demographic pyramid of life. Policy has been fabulous for Wall Street and the banks, but not so fabulous for the average household. The average household has faced vanishing interest income and negative real wage growth amidst an environment of a meaningfully rising cost of every day living (food and energy prices).

Policy has been counterproductive because policy makers continue to focus on short term outcomes as opposed to longer term structural remedies. Remember, people repeat the mistakes of their grandparents, not their parents. Mr. Bernanke is apparently an "expert" on the actions of "grandparents", yet he is very much repeating their same mistakes by his implicit refusal to even consider Austrian/Kondratieff like economic ideas. You already know, THE key character point of successful investors over time is flexibility in outlook and behavior. It's just a shame we can't clone that character point inside the Fed and Administration at present. But of course that would be counterproductive to the interests of Wall Street and the big banks.

There is much more in the Contrary Investor article. I excepted the ideas pertaining to credit.

It is very refreshing to see someone else writing about debt deflation and how powerless the Fed is to stop it. Instead, we see article after article by people touting high inflation, even hyperinflation.

Hyperinflation is complete silliness at this point. Were it to come, it would be an act of Congress that would create it, not an act of the Fed, and the Fed would probably have to play along. I doubt the Fed would. For all its many faults, the Fed does not want to destroy banks. Hyperinflation would do just that.

The Republican dominated House wants little or nothing to do with more stimulus. Certainly US government debt is going to mount, but it is going to mount in Japan, the Eurozone, and the UK as well.

Moreover, Eurozone structural issues matter now, while US government debt will matter more in the years to come.

Midst of Deflationary Collapse or Brink of Inflationary Disaster?

Although the Keynesian and Monetarist economists have missed the boat on what is happening and why, Austrian minded folks who fail to understand the importance of credit and how little the Fed can do to revive it have blown the call as well.

It pains me to see articles like On the Brink of Inflationary Disaster by Austrian economist Robert Murphy.

We are clearly we are in the midst of a deflationary collapse as noted in Yes Virginia, U.S. Back in Deflation; Inflation Scare Ends; Hyperinflationists Wrong Twice Over

Focus on Money Supply Alone is Fatally Flawed

Deflation is about credit, it is also about attitudes that govern the demand for credit.

As I have stated many times over the years, and as stated above in the Contrary Investor, there is nothing the Fed can do to force businesses to expand or banks to lend.

That point explains why Austrian economists who focus on money supply alone have failed and will continue to fail.

Until consumer demand returns, businesses would be foolish to expand. Unfortunately, the Fed's misguided easing policies have stimulated commodity speculation thereby increasing manufacturing costs, while simultaneously clobbering those on fixed income and reducing final consumer demand.

I wrote about the plight of those on fixed income in Hello Ben Bernanke, Meet "Stephanie" back in January. Please give it a read if you have not yet done so.

The Deflationary Hurricane of Deteriorating Social Mood

One of the best posts recently on social mood and deflation is by Minyanville professor Peter Atwater.

Please consider The Deflationary Hurricane of Deteriorating Social Mood

This morning, in the aftermath of Fed Chairman Ben Bernanke’s speech on Friday, the editorial page of the Wall Street Journal noted, “Mr. Bernanke also lectured that ‘U.S. fiscal policy must be placed on a sustainable path,’ though not by cutting spending in the short-term. So the Fed chief joins the Keynesian queue of spending St. Augustines – Lord, make us fiscally chaste, but not yet.”Price Deflation on the Way?

Everything we need to do for long-term economic, if not societal success and stability comes with very severe short-term consequences. And so the response of most policymakers (and not just those responsible for fiscal policy but also regulatory policemen like Mr. Bernanke himself) has been to advocate for short-term expansionary programs and rules, while postponing the real teeth of necessary change until some later date in the future. Basel III, for example, has a phased-in capital-strengthening requirement for the banking system that does not finish until 2019 – again, "chaste, but not yet."

I am sure that what is behind the thinking of policymakers is the notion that if we can just get through this tough “transitory” period, the economy will turn up; and at that point, whether it is fiscal or regulatory policy, our ability to handle constraints will be much, much easier to bear.

After 11 years of declining social mood, the notion that further monetary stimulus has limited use is hardly a surprise. As I have cautioned so many times, when it comes to the consumer it is not the depth of a recession that matters, but rather its length. And while for policymakers and financiers this may feel like a three-year-old recession (and for some even just a three-week-old recession!), for the American consumer this is a decade-old recession that has deteriorated well into a depression. The average American is now financially and emotionally exhausted. And given the news reports out of Washington over the past month, they are also now afraid that they are at risk of losing some or all of their government safety net, too. Like the children of fighting, divorcing parents, they are now fearful of what an increasingly uncertain future holds.

While further fiscal stimulus – particularly job-related initiatives – may slow the pace of deterioration, I am increasingly afraid that further fiscal and monetary policy actions are now impotent agents against our current social mood. Where in 2000, the future was so bright that we’d need shades, in 2011, the future for many Americans is so dark that they can’t see their way forward.

The consequence will be price deflation -- and not just further price deflation across those debt-dependent purchases like homes and automobiles, but across all categories of consumer goods. And for the first time since the 1930s, American businesses will see that lower prices are not always met with greater demand.

My definition of deflation is "a decrease of money supply and credit with credit marked-to-market". Judging by symptoms of deflation and Fed's efforts at fighting it, the US is back in deflation now by my measure. In my model, falling prices are not a requirement for deflation.

The important point is not definition, but rather the expected conditions. Yet, the conditions I expect and indeed the conditions in the US right now (in aggregate) match deflationary scenarios, not inflationary ones.

Murphy calls for an "inflationary disaster" while Atwater calls for "price deflation across all categories of consumer goods".

I do not know if we see across the board price deflation Atwater calls for given peak oil constraints and an inept US energy policy that also affects food prices.

However, I do expect to see falling education costs and falling medical costs as well as falling prices in a broad array of consumer goods and services, especially if Republicans can get a few sensible deficit measures passed.

Whether that scenario happens or not, the idea "brink of inflationary disaster" is complete silliness unless and until the Fed can revive credit, yet the Fed is powerless to do so.

So, unless Congress goes really haywire, attitudes will change and deleveraging will play out before the US experiences serious inflation. Unfortunately, Fed and Congressional policies have only served to lengthen the deleveraging timeline.

Those looking for hyperinflation or even strong inflation have missed the boat again, and again, and again, and will continue to do so, interrupted by periodic inflation scares until debt-deflation plays out.

Understanding the Deflationary Cycle

To understand what is happening, why businesses are not hiring, why housing is stagnant, and where the economy is headed, one needs a model that takes into consideration five key factors ...

- Mark-to-Market Measures of Bank Credit and Capitalization Ratios

- Credit Cycle Theory

- Attitudes of Banks, Businesses, and Consumers

- Futility and Limits of Keynesian Stimulus

- Futility of Monetary Stimulus

1 -Mark-to-Market Measures of Bank Credit and Capitalization Ratios

Banks cannot and will not lend unless they are not capital impaired and unless they have credit-worthy customers. Atwater noted Basel III was delayed until 2019. I noted on many occasions banks are still hiding investments off the balance sheets in SIVs and mark-to-market rules have been suspended several times.

As happened in Europe, delay tactics can only work for so long before the market questions if loans on the balance sheets of banks will ever be repaid. That time is now, not 2019. Thus banks are too capital impaired to take excessive risks, even if they wanted to. Moreover, too few credit-worthy businesses want to expand in the first place.

2 - Credit Cycle Theory

In accordance with long-wave, Kondratieff Cycle (K-Cycle) theory credit expansion and contraction cycles play out over decades. At least 75% of the time, continuously (not on and off), the economy grows in an inflationary manner. When deflation hits, few expect it because all many have known for their entire lives is inflation.

As long as consumers have ability and willingness to add debt an leverage, the Fed seems to have power to revive the economy via various stimulus efforts. Once a consumer deleveraging cycle starts, the Fed's power ends.

3 - Attitudes of Banks, Businesses, and Consumers

The willingness and ability of banks to lend and consumers to borrow and increase leverage is shot. Banks don't want to lend (or are to capital impaired to lend), and boomers are heading into retirement overleveraged in housing, without enough savings.

Consumers first thought tech stocks would be their retirement, then housing. Both dreams have been shattered. Consumers are now determined to pay down debt (saving), even if by outright default or walking away. Default and walking-away impacts banks willingness and ability to lend.

Think of attitudes like a pendulum. Attitudes can only go so far before they reverse. Housing reversed in 2007 as did the Nasdaq in 2000. Both reversed when the pool of greater fools ran out.

The Nasdaq is still nowhere close to old highs. These cycles last longer than most think. I expect housing will be weak for a decade once it bottoms, and it has not yet bottomed.

Finally, it's not just boomer attitudes that affect credit. Kids see their parents and grandparents arguing over debt, worried about bills, worried about jobs and vow not to repeat their mistakes. This point ties in with K-Cycle theory above.

4 - Futility and Limits of Keynesian Stimulus

Keynesian economists always want more, then more, then still more stimulus until the economy heals. Japan with debt-to-GDP ratio over 200% has proven such policies cannot ever work.

Keynesian economists always refuse to discuss the endgame, how the debt can be paid back, and what happens when stimulus stops.

The US has virtually nothing to show for all the make-shift, ready-to-go projects that temporarily put people back to work in 2009 and 2010. Not only did we repave roads that did not need paving, those hired still have debt-overhang and are still underwater on their houses.

All that happened was a delay in the day-of-reckoning. More Keynesian stimulus will only further delay the day-of-reckoning while adding to the national debt and interest on the national debt.

Priming-the-pump Keynesian theory will fail every time in a debt-deleveraging cycle. Indeed, it never works, it only appears to work until debt leverage is maxed out.

5 - Futility of Monetary Stimulus

As discussed above, monetary stimulus negatively affects the real economy for the temporary benefit of the financial economy and Wall Street. The tradeoff was not worth it except through the perverted-eyes of Wall Street.

Telling action in bank stocks says the limits of helping Wall Street may have even run out.

Many point to excess reserves as a sign of future inflation. I point to excess reserves as a sign of failed Fed policy. Commentary from Austrian economists shows they fail to understand how credit even works.

The idea those excess reserves are going to pour into the economy in a 10-1 leveraged fashion is simply wrong. Banks do not lend when they have excess reserves. Banks lend when they have credit-worthy borrowers, provided they are not capital impaired.

It is time Austrian economists finally wake up to this simple economic truth.

Academic Theory vs. Reality

Economists of all sorts stick to failed models.

- The Monetarist currency cranks want more monetary stimulus even though it is counterproductive

- The Keynesian clowns simply will not admit end-game constraints

- The Austrians for the most part either ignore credit or incorporate failed models of credit expansion into their theories.

That said, I side with the Austrians about what to do (essentially let things play out, while implementing much needed structural reforms).

Twelve Specific Recommendations

- Banks and bondholders should take a hit. Banks are not going to lend anyway so bailing them out at the expense of taxpayers is both morally and economically stupid. End the bailouts, all of them, and prosecute fraud, the higher up the better.

- Implement serious bank reform now, not 9 years from now. Banks should be banks, not hedge funds. This proposal will necessitate breaking up banks. So be it.

- Scrap Davis-Bacon and all prevailing wage laws. Such laws drive up costs and have wreaked havoc on many cities and municipalities, now bankrupt or on the verge of bankruptcy.

- Pass national right-to-work laws. Once again, we need to reduce costs on businesses and local governments to spur more hiring and reduce costs.

- End collective bargaining rights of all public unions. The goal of unions is to provide the least service for the most money. The goal of government should be to provide the most services for the least money.

- Scrap ethanol policy and end all tariffs.

- Legalize hemp and tax it. Prison costs will go down, tax revenue will grow, and biofuel and fiber research will expand as hemp produces very soft fibers.

- Corporate income tax rates should be lower in the US than abroad. Current policy encourages capital flight and jobs flight via lower tax rates on profits overseas than in the united states. This penalizes businesses that work only in the US, especially small businesses that do not have an army of lawyers and lobbyists.

- Stop the wars and set a plan to bring home all US troops from Iraq, Iran, and 140 or so other countries.The US can no longer afford to be the world's policeman.

- Implement Paul Ryan's Medicare voucher proposal. It is the only way so far that anyone has proposed that puts much needed consumer "skin-in-the-game" that will reduce medical costs.

- Legalize drug imports from Canada

- End the Fed and fractional reserve lending. Both have led to boom-bust cycles of ever-increasing amplitude.

Notice how counterproductive Fed policy is and how counterproductive Obama's policies are.

The Fed wants positive inflation but businesses have not been able to pass the costs on. Instead, companies outsource to China. Those on fixed income get hammered.

Fool's Mission

Obama wants to create jobs via stimulus measures. It's a fool's mission.

Prevailing wages drive up the costs, few are hired, and the cost-per-job (created or saved) is staggering. Money never goes very far because the US overpays every step of the way.

Stimulus plans that do not fix the structural problems are as productive as pissing in the wind. Then when the stimulus dies, which it is guaranteed to do, a mountain of debt remains.

Instead, my 12-point recommendation list will fix numerous structural problems, create lasting jobs, and reduce the deficit. What more can you ask?

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2011 Mike Shedlock, All Rights Reserved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.