Currency Wars and Quantitative Easing

Interest-Rates / Central Banks Aug 06, 2011 - 11:00 AM GMTBy: CentralBankNews

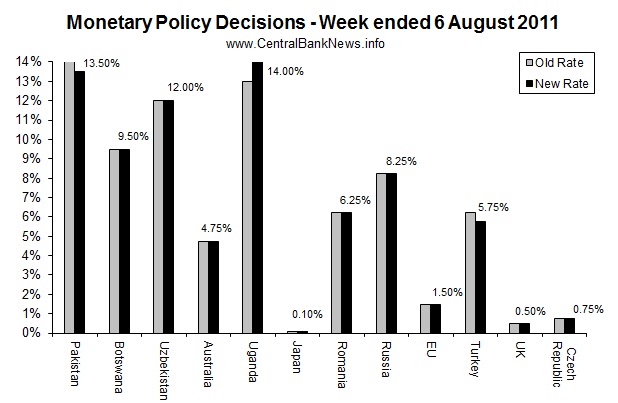

The past week in monetary policy saw 12 central banks reviewing monetary policy settings, with 2 expanding asset buying programs, and just 3 adjusting interest rate levels. Those that adjusted interest rates were: Pakistan -50bps to 13.50%, Uganda +100bps to 14.00%, and Turkey -50bps to 5.75%; Switzerland also adjusted its interest rate target range downward to halt gains in the Swiss franc. Meanwhile those that held rates unchanged were: Botswana 9.50%, Uzbekistan 12.00%, Australia 4.75%, Japan 0.10%, Romania 6.25%, Russia 8.25%, EU 1.50%, UK 0.50%, and the Czech Republic 0.75%.

The past week in monetary policy saw 12 central banks reviewing monetary policy settings, with 2 expanding asset buying programs, and just 3 adjusting interest rate levels. Those that adjusted interest rates were: Pakistan -50bps to 13.50%, Uganda +100bps to 14.00%, and Turkey -50bps to 5.75%; Switzerland also adjusted its interest rate target range downward to halt gains in the Swiss franc. Meanwhile those that held rates unchanged were: Botswana 9.50%, Uzbekistan 12.00%, Australia 4.75%, Japan 0.10%, Romania 6.25%, Russia 8.25%, EU 1.50%, UK 0.50%, and the Czech Republic 0.75%.

Other than interest rates, the Bank of Japan announced a 10 trillion yen expansion of its asset purchase (quantitative easing) program, Japan was also reported as intervening in the foreign exchange market to weaken the Yen. Similarly the European Central Bank recommenced its bond buying program in efforts to stabilize financial markets. Such moves spurred speculation that the US Federal Reserve may also adjust its quantitative easing program when it meets next week. Elsewhere the People's Bank of China announced a ban on foreign Yuan loans for purposes other than import/export.

Perhaps the most interesting or notable theme of the week was the currency factor, with Switzerland and Japan both announcing measures to counter excessive appreciation of their currencies against the US dollar. Last month Brazil's central bank also announced measures to halt the rise of the surging Brazilian real-USD exchange rate. So is this an escalation of the so-called currency wars? The US has been criticized by some for using its quantitative easing program to weaken the US dollar, indeed the US dollar has experienced a period of significant weakness. The trend towards currency interventions, and currency oriented monetary policy decisions marks a course in the opposite direction of the coordinated global monetary policy response during the financial crisis, and time will tell what effects it may bring.

Other than exchange rates, central banks showed over the week that they were thinking about the usual problems of balancing inflation and economic growth. Indeed, the source of inaction for most of the central banks was managing that balance, but one key element that was similar in most bank's monetary policy statements was concerns about tail risks. Indeed, the US debt drama, and the ongoing sovereign debt crisis in the Euro area was explicitly mentioned as causing policy and economic outlook uncertainty; unfortunately signs are that these risks will persist in the medium term.

Following are some of the key quotes from the key central banks, and those announcing adjustments in monetary policy settings:

Reserve Bank of Australia (held rate at 4.75%): "Year-ended CPI inflation has been high, affected by the extreme weather events earlier in the year. As these effects reverse over the next couple of quarters, CPI inflation should decline. But measures that give a better indication of the trend in inflation have begun to rise over the past six months, after declining for the previous two years."

Bank of Japan (held rate at 0.10%, expanded QE): The Bank said it "deemed it necessary to further enhance monetary easing, thereby ensuring a successful transition from the recovery phase following the earthquake disaster to a sustainable growth path with price stability,".

European Central Bank (held rate at 1.50%, resumed bond buying): "an adjustment of the accommodative monetary policy stance was warranted in the light of upside risks to price stability. While the monetary analysis indicates that the underlying pace of monetary expansion is still moderate, monetary liquidity remains ample and may facilitate the accommodation of price pressures. As expected, recent economic data indicate a deceleration in the pace of economic growth in the past few months, following the strong growth rate in the first quarter. Continued moderate expansion is expected in the period ahead. However, uncertainty is particularly high".

Central Bank of Turkey (dropped rate -50bps to 5.75%): "Concerns regarding sovereign debt problems in some European economies and the global growth outlook have continued to intensify, increasing the risks highlighted in the July Committee meeting." On the rate cut the bank said it was intended "to reduce the risk of a domestic recession that may be caused by the heightened problems in the global economy."

Bank of Uganda (increased rate +100bps to 14.00%): the move was "intended to reduce the growth of bank credit in the economy, which expanded very rapidly in the 2010-11 fiscal year, and to provide some support for the nominal exchange rate, which affects domestic prices of imported goods,".

State Bank of Pakistan (cut rate -50bps to 13.50%): "The key parameter in this assessment is the outlook of inflation that indicates that average inflation in FY12 is expected to remain in line with the announced target. No adjustment in the interest rate would have entailed further tightening of monetary policy in real terms, which is not warranted given the decline in private investment."

Central Bank of Russia (held rate at 8.25%): "considering current domestic and external economic conditions and the effect of the monetary policy measures, implemented in recent months, the Bank of Russia judged that the current level of money market interest rates was appropriate to maintain the balance between inflation risks and risks to economic activity in the coming months"

Swiss National Bank (announced a series of measures aimed at the CHF): the Bank noted that it "considers the Swiss franc to be massively overvalued at present. This current strength of the Swiss franc is threatening the development of the economy and increasing the downside risks to price stability in Switzerland".

Looking to the central bank calendar, next week's focus will no doubt be squarely on what the US FOMC does; will Bernanke follow Japan and the EU and expand the Fed's asset buying (quantitative easing) program? Also on the agenda is the Bank of England's inflation report on the 10th of August, also on the 10th is China's inflation data, so keep an eye on that; there are rumors that the People's Bank of China may opt for another interest rate increase.

USD - USA (Federal Reserve) - expected to hold at 0.25% on the 9th of Aug

IDR - Indonesia (Bank Indonesia) - expected to hold at 6.75% on the 9th of Aug

NOK - Norway (Norges Bank) - expected to hold at 2.25% on the 10th of Aug

KRW - South Korea (Bank of Korea) - expected to hold at 3.25% on the 11th of Aug

Source: www.CentralBankNews.info

Article source: http://www.centralbanknews.info/2011/06/monetary-policy-week-in-review-18-june.html

© 2011 Copyright centralbanknews - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.