Stock Market Rally Shows Bull Market Still Has Some Kick Left

Stock-Markets / Stock Markets 2011 Jul 05, 2011 - 06:44 AM GMTBy: Money_Morning

Jon D. Markman writes:

U.S. stocks ripped higher every day of the past week following positive news on U.S. manufacturing, Greek sovereign debt and an absolutely epic amount of short-covering.

Jon D. Markman writes:

U.S. stocks ripped higher every day of the past week following positive news on U.S. manufacturing, Greek sovereign debt and an absolutely epic amount of short-covering.

The past week's rally has shown at least that the spirit of the bull market still lives. It rarely pays to be bearish for more than a few weeks at a time, and even then only very selectively. So long-term investors need to keep their eyes on the on the horizon until sellers can prove their moxie.

Right now the set-up is more than likely a stutter-step rally back toward the highs for the major indexes until the second or third week of earning season -- around July 18 -- and then the picture changes.

While second quarter earnings were probably decent for large companies due to overseas sales, low employee expenses and low interest rates, forward guidance is going to be a challenge. Already we're seeing more companies than normal cutting guidance, and now we'll have to see if investors are willing to overlook that -- or whether it will begin to matter.

Last week's baby bull market rally gave the markets a nice little pop. The Dow Jones Industrial Average rose 5.4%, the Standard & Poor's 500 Index rose 5.6%, the Nasdaq rose 6.1% and the Russell 2000 small caps rose 5.3%. Breadth was very good, at 4-to-1 in favor of advancers, as new highs surged to 414 compared to 50 new lows.

It was very curious the market rose in such spectacular fashion just as the second round of quantitative easing, or QE2, ended, because it looked exactly like the start of QE2. I'm not saying that the Federal Reserve helps engineer these rallies to make itself look good, but I will say it's an amazing coincidence. And I don't believe in coincidences.

Another notable element of the rally was that it came on virtually no company news. Got to like that surprise attack by the bulls. About the most interesting corporate action of the week was the revelation of a new stake in specialty truck maker Oshkosh Corporation (NYSE: OSK) by activist Carl Icahn. Since that's actually not particularly exciting, it just goes to show what a slow news week it was.

The only stocks that look fantastic are the defensives such as CignaCorporation (NYSE: CI) and McDonalds Corporation (NYSE: MCD) - or the kinds of stocks that do best in the weakest conditions.

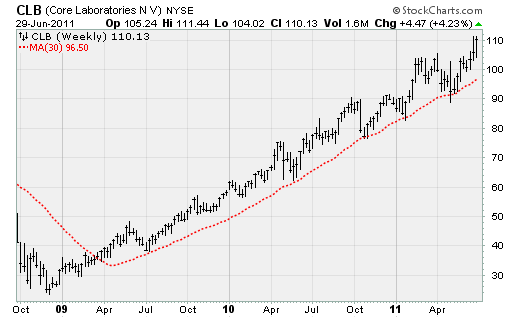

Some financial companies have shown signs of stirring following some good news on the international and domestic regulatory front.American Express Company(NYSE: AXP) is almost back to a new high, and Wells Fargo & Company(NYSE: WFC) is showing a pulse, and some energy services stocks, like Core Laboratories N.V. (NYSE: CLB) are still making new highs.

Murky Picture

Now about those manufacturing numbers: The Institute for Supply Management (ISM) index rose 1.8 points, upending expectations for a 1.8-point decline. If you recall, the past few weeks have been marked by consternation over regional surveys showing declines in manufacturing in Dallas, New York and Philadelphia.

Then on Friday a report from Chicago came that was positive. And now we have a national number that's a bit higher.

Still, what is the big picture? The number is only back to where it was two months ago, but it is the first improvement since February. And all five components rose: new orders, production, employment, inventories and lengthier delays to deliver. All the rises were tiny, but that there was any improvement is what the market liked.

All these economic numbers are backward looking and subject to a lot of revision. My favorite economic forecaster, Lakshman Achuthan of the Economic Cycle Research Institute, says his work shows that industrial production is in a profound, pervasive decline. If that is true, then in any given month there could be a small countertrend move, such as this one, but the bigger move is lower.

Let's also keep in mind that other parts of the economy are not in such great shape, either. Construction spending is still weak, with spending down for the sixth straight month according to data released last week. Public sector cutbacks are evident -- the result of a cutback in fiscal spending. Commercial construction spending was down for the third straight month.

Finally, consumer sentiment is weaker than ever. The latest University of Michigan consumer sentiment index was published Friday and it showed the headline level fell 2.8 points from May -- with expectations still very weak. Expectations correlate to future spending levels, so that is something to bear in mind going forward.

Bottom Line:The economy is not veering off the road into a yawning abyss, but it is not exactly smokin' hot either. The market sank for seven weeks for reasons that were a bit mysterious, and then rose for a week to reverse that decline for reasons that were just as mysterious. In the meantime, a lot of people left the stock market near the bottom and were loathe to jump back in.

Thus this was just another example of how divorced the stock market can be from anything that resembles rationality in short stretches of time, although over longer stretches it does tend to reflect the growth of earnings, the swelling of confidence and the pace of inflation.

Bits and Pieces

A few items I picked up over the weekend:

- With memories of the debt contagion of 2008 still fresh in their minds, investors have started to worry not just about equities and not just about bonds, but also about money market funds. Many are exposed to Greek credit through the commercial paper of European banks. The Investment Company Institute reports that $51 billion was pulled out of money market funds and placed, apparently, in U.S. Treasurys! As a measure of how freaked out people are, consider that three-month T-bills are paying just one hundredth of one percentage point. Add inflation and that's a negative yield. Treasurys are now outperforming stocks in 2011. That's a lot of money that is going to need to come back to stocks if and when the mood turns brighter.

- Bespoke Investment Group estimates that inflation in commodity prices has led to increased costs of $7,000 for a family of four since 2008. The recent drop in commodity prices in the past two months has reversed this trend, a net positive for consumers. Bespoke argues that Americans are spending 96 cents less per person per day now than they were when essential commodities were peaking. That may be in part why retailers are suddenly doing better.

- The past week was the third straight in which we had more positive economic surprises than negative surprises. Perhaps the economy really is stabilizing. Of the twelve data points released last week, six were stronger than expected, four were weaker and two were in line. Bespoke and Citigroup Inc. (NYSE: C) analysts both note that the market responds to the numbers compared to perceptions rather than to the actual numbers. So if expectations have been lowered enough, the negativity finally may be abating -- allowing a surprise turn higher to emerge.

- Earnings season is around the corner. Quick look forward: Bespoke notes that in the last quarter the percentage of stocks that beat estimates was just 60%, the lowest level of the bull cycle. Since then, 259 more companies have reported, and 66% of them have beaten estimates -- more evidence that expectations are lower, which is always a plus. However, guidance has been lousy. In the off-season period, 8.5% of companies have lifted guidance while 9.3% have lowered. If guidance numbers keep dropping, anyone looking for earnings season to provide a boost may be sorely disappointed.

Allocations

By now you should know my recommended allocations. Stick to mid-cap growth for your bet on beta through the iShares S&P Midcap 400 Growth ETF (NYSE: IJK) fund. You get all sectors, and you get the companies that are nimble, audacious and growing without having to place specific bets in close combat.

Through thick and thin this year, IJK has been a leader and it should stay that way. If you need to make one passive index bet -- where the other choices might be the S&P 500, or a sector fund -- then this should be it. And it's liquid enough that you can make it a large position. Right now we've got it at 10% as we wait for a 90% upside-day confirmation that buyers are back. It can go up to 50% or more of an entire portfolio.

As for sectors, health care and staples have been the way to go, with industrials turning higher again as well. I've got them at 10% each.

Groups we are avoiding now are financials and technology. Banks remain under pressure from new regulations and tougher lending standards, and techs are suffering from a lack of business investment and downturn in employment. Both can turn on a dime, though, so don't count them out completely.

Regions to avoid at the moment are Europe, emerging markets and Japan. The continent has had moments of outperformance in the past year, but overall they are going to suffer the most when Greece defaults, as it inevitably will -- and when it's most inconvenient.

The most hated stocks right now are U.S. homebuilders, natural gas producers, European banks and Indian equities, with Japanese equities not far behind. Hard to say with certainty, but usually if you buy some of the most hated groups and put them away in a lockbox for a year or two you will find that they came back to life when no one was looking. That did happen to the refiners earlier this year, as well as to down-and-out drug maker like Pfizer Inc. (NYSE: PFE) and perennial also-ran Verizon Communications Inc. (NYSE: VZ).

The Week Ahead

The holiday shortened week ahead is relatively light but features one monster economic report on Friday: the employment situation report for January.

Monday, July 4: Markets closed for Independence Day Holiday.

Tuesday, July 5: Factory orders for May

Wednesday, July 6: Composite index for the ISM non-manufacturing survey for June

Thursday, July 7: Initial jobless claims

Friday, July 8: Nonfarm payrolls for June; private payrolls; unemployment rate; average workweek; average hourly earnings

[Bio Note: Money Morning Contributing Writer Jon D. Markman has a unique view of both the world economy and the global financial markets. With uncertainty the watchword and volatility the norm in today's markets, low-risk/high-profit investments will be tougher than ever to find.

It will take a seasoned guide to uncover those opportunities.

Markman is that guide.

In the face of what's been the toughest market for investors since the Great Depression, it's time to sweep away the uncertainty and eradicate the worry. That's why investors subscribe to Markman's Strategic Advantage newsletter every week: He can see opportunity when other investors are blinded by worry.

Subscribe to Strategic Advantage and hire Markman to be your guide. For more information, please click here.]

Source :http://moneymorning.com/2011/07/05/week-long-rally-shows-bull-market-still-has-some-kick-left/

Money Morning/The Money Map Report

©2011 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or 72 hours after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Money Morning Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.