Economic Whiplash, Eurozone Debt Crisis Intolerable Choices, U.S. Non-Farm Payrolls Worse Than Headlines

Economics / Global Debt Crisis Jun 04, 2011 - 12:05 PM GMTBy: John_Mauldin

Do you feel as if you are suffering from some sort of economic whiplash? Between focusing on the European crisis (and it is a crisis), then looking at softening data in the US and political turmoil in Japan, not to mention the Middle East, you can be forgiven for feeling like someone just slammed into the back of your "economic recovery car." This week we look at today's US employment numbers, then at a troubling slowing of economic velocity, precisely at a time when it should be rising, and then consider a powerhouse, must-be-read-twice commentary from Martin Wolf on the European situation. Then I will weigh in with some of my own thoughts. Counterintuitively, the holders of certain European debt are being put at further risk by the bailout. (This letter may be a little shorter and take more work than others -which some of you think will improve it - as I am suffering from Caesar's Revenge here in Tuscany, although I am getting better!)

Do you feel as if you are suffering from some sort of economic whiplash? Between focusing on the European crisis (and it is a crisis), then looking at softening data in the US and political turmoil in Japan, not to mention the Middle East, you can be forgiven for feeling like someone just slammed into the back of your "economic recovery car." This week we look at today's US employment numbers, then at a troubling slowing of economic velocity, precisely at a time when it should be rising, and then consider a powerhouse, must-be-read-twice commentary from Martin Wolf on the European situation. Then I will weigh in with some of my own thoughts. Counterintuitively, the holders of certain European debt are being put at further risk by the bailout. (This letter may be a little shorter and take more work than others -which some of you think will improve it - as I am suffering from Caesar's Revenge here in Tuscany, although I am getting better!)

As you know, I am a firm believer that the state of the global economy is such that we as investors have to be especially agile and focused today. Consequently I spend a great deal of time and effort looking into alternative investment strategies and managers. I'm very pleased to announce that I am relaunching my special newsletter for accredited investors, to share the latest opportunities and pitfalls in alternative assets.

The good news is that this Accredited Investor Letter is completely free. The only restriction is that, because of securities regulations, you have to register and be vetted by one of my trusted partners before you can be added to the subscriber roster. They include Altegris Investments in the US, Absolute Return Partners in Europe, Nicola Wealth Management in Canada, and Fynn Capital in Latin America. This is a painless process (I promise!), and just to sweeten the pot, after you register my partner will provide you access to the video of Gary Shilling's speech from my Strategic Investor Conference in La Jolla. I don't need to remind you how insightful Gary is, but if you've never seen him speak, let me just tell you that he's absolutely compelling.

[Click here now to register] and you'll be part of the summer relaunch of my letter exclusively for accredited investors. In the meantime, enjoy Gary's video presentation and benefit from his intelligence as you plot your investment course. Over time, we will make all the conference videos available to the subscribers of the free Accredited Investor E-letter. Those who attended the conference, or have spoken with an Altegris professional, already have access to all the speeches and panels.

I do not like limiting the letter to accredited investors, but those are the rules under which I work. This is not of my choosing, and I have worked in front of and behind the scenes to try to change what I think is a very unfair rule. (See important risk disclosures below. In this regard, I am president and a registered representative of Millennium Wave Securities, LLC, member FINRA.) And now to the letter.

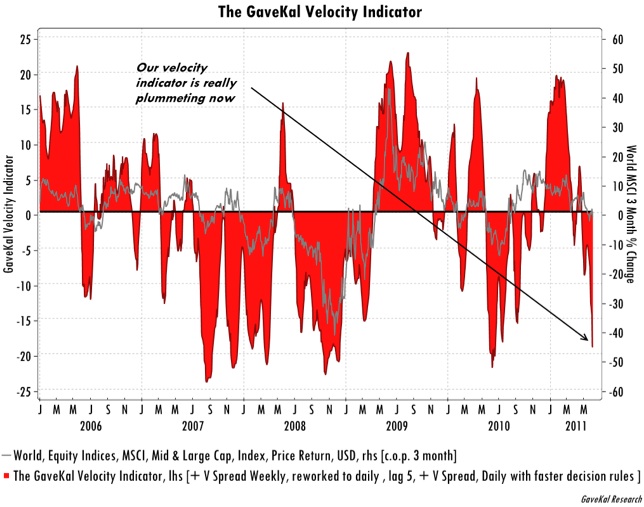

Velocity Rolls Over

Quickly, the following came to my inbox from my friends at GaveKal. They chart their own private calculation of the velocity of money. Notice in the chart below that the velocity of money was screaming "Problem!" during the recent crisis, began to improve with the recovery in 2009, rolled over with the end of QE1, and started to improve again (more or less) with QE2. Now, with QE2 ending, velocity is already down and falling, which is worrisome, as this comment shows. (Understand, the guys at GaveKal are typically looking for reasons to be bullish.)

"As we have highlighted in recent Dailies, our Velocity Indicator has been heading south rather rapidly. At first glance, this might appear surprising as there are few signs of stress in the financial system today: corporate spreads are decently tight, IPOs continue to roll out, and the VIX remains low. Sure, Greek debt has now been downgraded below Montenegro's and stands at the same ratings as Cuba's, but even acknowledging this, the recent depths reached by our Velocity Indicator is still somewhat surprising. Why, in the face of fairly benign markets, is our indicator so weak?

"The answer is very simple and it is linked to the recent underperformance of banks almost everywhere. Indeed, with short rates still low everywhere, and yield curves positively sloped, we are in the phase of the cycle when banks should be outperforming. The fact that they are not has to be seen as a concern. So does the underperformance come from the fact that the market senses that losses have yet to be booked (Europe?)? Is it a reflection of a lack of demand for loans (US?) or that more losses and write-offs are just around the corner (Japan?)? Is the bank underperformance signaling that we are on the verge of a new banking crisis, most likely linked to the possibility of European debt restructurings? Or perhaps it is linked to the coming end of QE2 and consequential tightening in the liquidity environment (see our Quarterl

published earlier today for more on this topic)?

"In our view, any of the above could potentially explain the recent bank underperformance. But whatever the reasons may be, it has to be seen as a worrying sign. One of our 'rules of thumb' is that if banks do not manage to outperform when yield curves are steep, the market must be worried about the financial sectors' balance sheets (given that, with a steep yield curve, there are few reasons to worry about the bank's income statement)."

As I have noted before, Martin Wolf is one of my all-time favorite writers. He alone is worth a subscription to the Financial Times (www.ft.com). I highlight below a column he did earlier this week. It presents the rather stark choices faced by Europe. This sentence from the 5th paragraph is spot on: "Moreover, because national central banks have lent against discounted public debt, they have been financing their governments. Let us call a spade a spade: this is central bank finance of the state." If such a situation is allowed to prevail, it has to undermine the value of the euro. My comments, after you read this slowly and thoughtfully.

"Intolerable Choices for the Eurozone"

By Martin Wolf

"The eurozone, as designed, has failed. It was based on a set of principles that have proved unworkable at the first contact with a financial and fiscal crisis. It has only two options: to go forwards towards a closer union or backwards towards at least partial dissolution. This is what is at stake.

"The eurozone was supposed to be an updated version of the classical gold standard. Countries in external deficit receive private financing from abroad. If such financing dries up, economic activity shrinks. Unemployment then drives down wages and prices, causing an 'internal devaluation'. In the long run, this should deliver financeable balances in the external payments and fiscal accounts, though only after many years of pain. In the eurozone, however, much of this borrowing flows via banks. When the crisis comes, liquidity-starved banking sectors start to collapse. Credit-constrained governments can do little, or nothing, to prevent that from happening. This, then, is a gold standard on financial sector steroids.

"The role of banks is central. Almost all of the money in a contemporary economy consists of the liabilities of financial institutions. In the eurozone, for example, currency in circulation is just 9 per cent of broad money (M3). If this is a true currency union, a deposit in any eurozone bank must be the equivalent of a deposit in any other bank. But what happens if the banks in a given country are on the verge of collapse? The answer is that this presumption of equal value no longer holds. A euro in a Greek bank is today no longer the same as a euro in a German bank. In this situation, there is not only the risk of a run on a bank but also the risk of a run on a national banking system. This is, of course, what the federal government has prevented in the US.

"At last month's Munich economic summit, Hans-Werner Sinn, president of the Ifo Institute for Economic Research, brilliantly elucidated the implications of the response to this threat of the European System of Central Banks (ESCB). The latter has acted as lender of last resort to troubled banks. But, because these banks belonged to countries with external deficits, the ESCB has been indirectly financing those deficits, too. Moreover, because national central banks have lent against discounted public debt, they have been financing their governments. Let us call a spade a spade: this is central bank finance of the state.

"The ESCB's finance flows via the euro system's real-time settlement system ('target-2'). Huge asset and liability positions have now emerged among the national central banks, with the Bundesbank the dominant creditor (see chart). Indeed, Prof Sinn notes the symmetry between the current account deficits of Greece, Ireland, Portugal and Spain and the cumulative claims of the Bundesbank upon other central banks since 2008 (when the private finance of weaker economies dried up).

"Government insolvencies would now also threaten the solvency of debtor country central banks. This would then impose large losses on creditor country central banks, which national taxpayers would have to make good. This would be a fiscal transfer by the back door. Indeed, that this is likely to happen is quite clear from the striking interview with Lorenzo Bini Smaghi, a member of the board of the European Central Bank, in the FT of May 29 2011.

"Prof Sinn makes three other points. First, this backdoor way of financing debtor countries cannot continue for very long. By shifting so much of the eurozone's money creation towards indirect finance of deficit countries, the system has had to withdraw credit from commercial banks in creditor countries. Within two years, he states, the latter will have negative credit positions with their national central banks - in other words, be owed money by them. For this reason, these operations will then have to cease. Second, the only way to stop them, without a crisis, is for solvent governments to take over what are, in essence, fiscal operations. Yet, third, when one adds the sums owed by national central banks to the debts of national governments, totals are now frighteningly high (see chart). The only way out is to return to a situation in which the private sector finances both the banks and the governments. But this will take many years, if it can be done with today's huge debt levels at all.

"Debt restructuring looks inevitable. Yet it is also easy to see why it would be a nightmare, particularly if, as Mr Bini Smaghi insists, the ECB would refuse to lend against the debt of defaulting states. In the absence of ECB support, banks would collapse. Governments would surely have to freeze bank accounts and redenominate debt in a new currency. A run from the public and private debts of every other fragile country would ensue. That would drive these countries towards a similar catastrophe. The eurozone would then unravel. The alternative would be a politically explosive operation to recycle fleeing outflows via public sector inflows.

"Events have, in short, thoroughly falsified the premises of the original design. If that is the design the dominant members still want, they must remove some of the existing members. Managing that process is, however, nigh on impossible. If, however, they want the eurozone to work as it is, at least three changes are inescapable. First, banking systems cannot be allowed to remain national. Banks must be backed by a common treasury or by the treasury of unimpeachably solvent member states. Second, cross-border crisis finance must be shifted from the ESCB to a sufficiently large public fund. Third, if the perils of sovereign defaults are to be avoided, as the ECB insists, finance of weak countries must be taken out of the market for years, perhaps even a decade. Such finance must be offered on manageable conditions in terms of the cost but stiff requirements in terms of the reforms. Whether the resulting system should be called a 'transfer union' is uncertain: that depends on whether borrowers pay everything back (which I doubt). But it would surely be a 'support union'.

"The eurozone confronts a choice between two intolerable options: either default and partial dissolution or open-ended official support. The existence of this choice proves that an enduring union will at the very least need deeper financial integration and greater fiscal support than was originally envisaged. How will the politics of these choices now play out? I truly have no idea. I wonder whether anybody does."

And It Just Gets Worse

It now appears that a "troika" of the ECB, the EU, and the IMF will bail out Greece yet again. They clearly cannot go to the private market. But what happens in 2013 when financing is once again needed? The lucky bond holders who have debt maturing in the next two years get 100% on the euro. Without another large bailout, the other bond holders will be lucky to get 30 cents on their debt. And this is just Greece.

The "troika" is doubling down on its losing bet in Greece and is playing with the dice loaded against them. With debt-to-GDP over 160% in just a few years, how can Greece work it out? And that is with very optimistic assumptions about GDP in a country whose government will be in severe austerity mode. GDP is likely to fall significantly, not rise slightly.

Martin Wolf is as wired in to the leadership of Europe as anyone. If he does not know how this plays out, you can bet the leaders don't either. Milton Friedman predicted (I think in 1999) that the euro would only last until the first real financial crisis. We are almost there. If it looks like the leaders of Europe are unsure what the game plan should be, it is because they have no idea beyond kicking the can down the road and hoping that something turns up.

The political winds in Europe are shifting. The crowd that runs the various member countries today, making decisions, etc., will not long survive the changes. I think there will be new politicians with different mandates as it becomes clear that the costs of the bailout are going to fall on the tax backs of the solvent countries and that austerity is going to mean hellishly bad deflation, high and rising employment, and depression in the indebted countries.

There is $600 trillion in derivatives now loose in the world. Who knows which banks have written them and to whom? Who are the counterparties? We did not fix this with the last political fix. The next crisis has the potential to be just as bad or worse than 2008, which is why I think Europe's leaders are so dead set on avoiding a day of reckoning. If you look under the hood, as they most assuredly have, it must be frightening. And with pushback from voters?

Contagion, thy name is Europe. And with the US economy slowing down, it might not take much to push us over the edge. We need to pay attention to European politics, which if anything is more arcane than that of the US. Stay tuned.

Tuscany

Five of my kids, three spouses or significant others, and a grandchild are here with me in Tuscany. Some of us have been a little under the weather, but are starting to feel better, and we did gamely go touring. I so love this part of the world, and the weather has been cool enough to be pleasant at night.

The next few weeks will see my kids (except for Trey) leave this weekend, and then friends from all over are coming to share the villa with us. Tiffani and Ryan and I will be working during the day and sharing company and good times with our guests in the evening. And now they are calling dinner.

... And what a dinner it was. We had a local chef come in with fresh food, homemade pasta, and all sorts of goodies. LOTS of Prosecco. Plus, Mother Nature put on a show for us. Sitting out eating under the canopy, we watched a lightning and rain storm worthy of West Texas spread out over the Tuscan hills. The French, in a 100-year drought and not that far away, must be jealous. So would West Texas today.

I am not sure I can remember when life has been better.

Night before last we went to a local destination restaurant, Il Conte Matto (The Mad Count), 100 meters from our house, and with the 600-year-old city wall running through it. I have to make a confession that is hard for this Texan to make. I normally do not order steak in Europe. In general, it is tough and tasteless. There are other dishes which are excellent that I can focus on. (Sorry, Scotland.) But the filet I had was as tender as any I have ever had. It is from a local breed called Chianina, which is a porcelain-white breed of cattle. They are huge, the largest cattle in the world. Average for a bull is 3,500 pounds, with the largest weighing in at 3,850. Taller than anyone but Dirk (who was awesome last night against Miami). Ten feet long. I would have bet something so large would be tougher than nails, but I would have lost that bet. (Google them.) I will take that walk down the street to Il Conte Matto a few more times. And the local Italians have learned how to do Chardonnay California style. Awesome.

Time to hit the send button. The kids are waiting for Dad to join them for the final night. Have a great week. I know I am.

Your wishing I could speak some Italian analyst,

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2011 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.