Copper is Talking, Massive Infrastructure Projects to Boost Productivity Throughout the Economy

Economics / Infrastructure May 19, 2011 - 06:52 AM GMTBy: Richard_Mills

Pure gold deposits are increasingly difficult to find.

Pure gold deposits are increasingly difficult to find.

“What really bothers me is that in the 1980s or 1990s, we saw three to five discoveries of 5 to 20 million ounces each, and upwards of 30 to 50 million ounces a year. That is what makes or breaks the industry. There are no discoveries of that magnitude now.” Pierre Lassonde, veteran gold analyst, co-founder/chairman of Franco Nevada Mining Corp., former president of Newmont Mining Corp.

Each year the mining industry must come up with a major new gold discovery of five million ounces just to replace what one of the world’s top gold miner’s digs up. Because large pure gold deposits are so hard to find - the low hanging fruit has already been picked - gold miners are turning to deposits that contain other metals like copper.

"In the case of gold, the world is currently mining it faster than it is finding it. Furthermore the average size and grade of gold discoveries continues to decline.” Richard Schodde, Managing Director of MinEx Consulting

Mining is the story of depleting assets, that asset must be constantly replenished; miners that want to stay in business must replace every oz taken out of the ground and there isn’t a lot of the larger size gold deposits left to find or buy that would really affect most of these larger company’s bottom lines. Replacing what they’ve mined let alone finding more productivity/resources is getting harder and harder.

"It's not a bad time to diversify if you are a gold miner. There are lots of reasons to be bullish on gold, at the same time copper has a stronger long-term outlook. Over the next five years I am by and large bullish and wouldn't be surprised if copper saw an upper range between $10,000 to $12,000." William Adams, analyst at FastMarkets.com

Porphyry Copper/Gold Deposits

Porphyry copper/gold targets are becoming increasingly important in the global quest to replace declining copper and gold production. These kinds of deposits yield about two-thirds of the world’s copper and are therefore the world’s most important type of copper deposit.

Porphyry copper deposits are copper orebodies which are associated with porphyritic intrusive rocks and the fluids that accompany them. Porphyry orebodies typically contain between 0.4 and 1 % copper with smaller amounts of other metals such as molybdenum, silver and gold.

There are two factors that make these kinds of deposits so attractive to the world’s major mining companies – firstly by focusing on profitability and mine life instead of solely on grade your other inputs of scale/cost can offset the lower grade and this results in almost identical gross margins between high and low grade deposits. Low grade can mean big profits for mining companies – Copper/gold porphyries offer both size and profitability.

The second factor affecting profitability of these often immense deposits is the presence of more than one payable metal ie for gold miners using co-product (copper) accounting the cost of gold production is usually way below the industry average.

So not only are the traditional miners of these scarce and often immense ore bodies in competition for them but increasingly yesterdays gold only miners are becoming interested as well. These kinds of deposits are one of the few deposit types containing gold that have both the scale and the potential for decent economics that a major gold mining company can feel comfortable going after to replace and add to their gold reserves.

The Vancouver Sun newspaper said high copper demand combined with limited new supplies have made copper the new gold as far as profit margins are concerned.

Copper boasts a higher profit margin than gold – at US$4.29 (U.S.) per pound copper has a 68-per-cent profit margin over industry average break even costs, compared with gold's 52 per cent.

"As 2011 unfolds, we expect copper to touch $5, yielding an extraordinary 70 per cent profit margin over average world break-even costs including depreciation." Patricia Mohr Scotiabank economist

Supply and Demand

Copper is supported by:

- The growth in demand from Africa, China, India and other emerging markets

- Global infrastructure deficit

- A low interest rate environment bodes well for the whole resource sector

- The overall weakness in the U.S. dollar translates into support for dollar denominated metal prices

In the Scotiabank Commodity Price Index report for April Mohr said “Copper could still retest the previous US$4.60 record of February 14. Chinese copper fabricators destocked copper and produced 2.1% fewer copper semis in January and February due to credit restrictions and high prices. However a big seasonal pick-up in consumption in the second quarter will lift prices."

“We see renewed strength in the second half and you’ve got to be bullish copper for the next few years. The global recovery is becoming more broad-based and you’re not going to see any new mines coming on stream for at least this year.” Christin Tuxen, analyst at Danske Bank A/S

Australian equity research firm Resource Capital Research (RCR) said it expects the copper market to move from a small surplus in 2010 to a deficit of around 400,000 tonnes by 2011.

According to JPMorgan Securities Ltd, the world refined copper market will have a 500,000-metric-ton deficit in 2011.

BHP Billiton Ltd. (BHP), the world’s largest mining company, said in January that output from their Escondida mine in Chile, the world’s largest copper mine, would drop by as much as 10 percent in the year ending in June because of lower ore grades.

Codelco, based in Santiago and the world’s largest copper producer, said on March 25 that supply from its mines fell for the fifth time in six years.

London based Anglo American Plc and Kazakhmys Plc reported lower output this year.

Michael Jansen, metals strategist at JPMorgan Securities Ltd, predicts a deficit of 500,000 tons to 600,000 tons this year.

Macquarie expects a shortfall of 550,000 tons.

Morgan Stanley projects copper prices will average $4.45 a pound in 2011, up 24 percent from an earlier estimate.

Australia & New Zealand Banking Group Ltd expects copper to average $4.57 a pound this year, up 12.5 percent from a previous estimate.

European copper producer Aurubis said that the global economy continues to recover, according to the IMF, and should achieve a growth rate of 4.4% in 2011 followed by 4.5% in 2012. This indicates sustainably high copper demand that cannot even be harmed by China's restrictive interest rate policy or the economic weakness of certain countries.

The market will see a wider deficit because of steady demand growth in emerging markets, including China and Brazil, a gradual economic recovery in the US and Europe and tight mine supplies. This year's deficit will be the most since 2004, according to company data. Hidenori Kamoo, general manager of the marketing department at Pan Pacific Copper Co

Tom Albanese, CEO Rio Tinto Group, the world’s second largest mining company, said that the industry has struggled to maintain supply because of declining ore grades, delays to mine expansions and disruption from strikes.

Ore grades averaged 0.76 percent copper content in 2009, compared with 0.9 percent in 2002. CRU, a London based research company.

Chile mined 6.6 percent less copper in February than a year earlier, the fifth decline in the last six months. National Statistics Institute

“There are still reasons to be bullish on copper into next year. The market is still going to be tight.” David Wilson, analyst Societe Generale SA

Freeport-McMoRan Copper & Gold Inc., the world’s largest publicly traded copper producer, said in January that it would produce less metal than forecast this year.

Barclays Capital says copper demand growth will slow to 4.1 percent this year, down from 9.6 percent in 2010 - still more than twice the anticipated 1.7 percent expansion in supply. Barclays forecasts an 889,000 ton shortfall for 2011.

“We’re still seeing an incredibly tight market. China has to buy copper. They can’t find substitutes.” Kevin Norrish, managing director, Barclays Capital

RBS forecast average prices between $10,000 and $11,500 in 2012, 2013 and 2014.

Barclays Capital saw copper trading on average at $12,000 in 2012.

StanChart's Zhu saw prices at just under $12,000 in 2014.

Christine Meilton, chief consultant at CRU Group said there was a risk some copper projects, expected to come on stream in 2012 and 2013, will be delayed because of red tape, poor infrastructure and funding difficulties.

“We suggest the upcoming summer period could be a very exciting time for LME copper prices. The market is positioning for declining LME copper inventories during the June-July-August period. In response, we believe copper prices should move higher.” John Redstone, analyst Desjardins Securities Inc.

Redstone is maintaining his average copper price forecast of $4.50 per pound in 2011 and $5 in 2012.

Urbanization

"For at least the next three years we are still very bullish on copper as the market will remain in deficit over that period, even under the most conservative global demand forecasts, and there is a possibility that this deficit could be more prolonged if demand grows faster than expectations. Copper is highly exposed to Asia, and urbanization in China and India will provide upside momentum for at least the next 10 years and perhaps as long as 20 years." Judy Zhu, analyst Standard Chartered Bank

Urbanization is a macro-trend, in 1800 two percent of the global population was urban, by 1950 it was 30%. The UN projects that by the year 2030 there will be 1.5 billion more people living in cities. China has one fifth of the world’s population, India has another 1.2 billion people and Africa adds another billion. China and India consume a lot of copper, so increasingly will Africa.

Urbanization and the accompanying necessary infrastructure build out - power, construction, energy and transportation – needed to accomplish developing countries urbanization/industrialization plans are obviously key drivers in increased copper consumption.

Infrastructure Deficit

Equally as important is the fact we have a global crisis in existing infrastructure. The demand this crisis is going to place on copper might very well be more than the demand coming from developing countries to build new infrastructure.

The amount of money, commodities and effort required is going to be massive:

- The American Society of Civil Engineers (ASCE) estimated, in 2005, US infrastructure investment needed to be $1.6 trillion dollars over the following five years

- European Union Energy Sector alone requires - $1.2T over 20 years

In a 2007 report, Booz Allen Hamilton estimated that investment needed to “modernize obsolescent systems and meet expanding demand” for infrastructure worldwide between 2005 and 2030 was about US$ 41 trillion.

Infrastructure spending by sector:

- Water and wastewater $22.6 trillion

- Power $9.0 trillion

- Road and rail $7.8 trillion

- Airports/seaports $1.6 trillion

Infrastructure spending geographically:

- Middle East $0.9 trillion

- Africa $1.1 trillion

- US/Canada $6.5 trillion

- South America/Latin America $7.4 trillion

- Europe $9.1 trillion

- Asia/Oceania $15.8 trillion

In January of 2009 CIBC World Markets issued a study that said a sharp deterioration in existing infrastructure could lead to as much as $35 trillion in public works spending over the next 20 years.

Infrastructure spending geographically:

- North America $180 billion/year

- Europe $205 billion/year

- Asia $400 billion/year

- Africa $10 billion/year

The World Economic Forum’s report, Positive Infrastructure, released in May 2010 finds that the world faces a global physical, hard asset, infrastructure deficit of US$ 2 trillion per year over the next 20 years.

In 2009 the ASCE updated their 2005 report on US infrastructure - no area rates higher than a C+. Roads, aviation, and transit declined in score while dams, schools, drinking water, and wastewater held at D or lower. One category, energy, improved, from a D to a D+. Below are the 2009 grades and new spending requirement:

- Aviation D

- Bridges C

- Dams D

- Drinking Water D-

- Energy D+

- Hazardous Waste D

- Inland Waterways D-

- Levees D-

- Public Parks and Recreation C-

- Rail C-

- Roads D-

- Schools D

- Solid Waste C+

- Transit D

- Wastewater D-

- America's Infrastructure GPA: D

- Estimated 5 Year Investment: $2.2 Trillion

The 2009 fiscal stimulus package - the American Recovery and Reinvestment Act (ARRA) - included $72 billion for infrastructure upgrades - enough to cover six percent of the 5 year infrastructure deficit estimated by the ASCE. Half a percentage point in maintenance cost will cut the life span of an infrastructure asset by 10 years.

The 2009 fiscal stimulus package - the American Recovery and Reinvestment Act (ARRA) - included $72 billion for infrastructure upgrades - enough to cover six percent of the 5 year infrastructure deficit estimated by the ASCE. Half a percentage point in maintenance cost will cut the life span of an infrastructure asset by 10 years.

Electrical Grid

ASCE’s Report Card for America's Infrastructure gives the US Electric Grid a rating of D, its summary:

“The U.S. power transmission system is in urgent need of modernization. Growth in electricity demand and investment in new power plants has not been matched by investment in new transmission facilities. Maintenance expenditures have decreased 1% per year since 1992. Existing transmission facilities were not designed for the current level of demand, resulting in an increased number of "bottlenecks," which increase costs to consumers and elevate the risk of blackouts.”

“Our grids today are more stressed than they have been in the past three decades. If we don’t expand our capacity to keep up with an increase in demand of 40 percent over the next 25 years, we’re going to see healthy grids become increasingly less reliable.” Today, with the grid operating flat-out, any disruption—like the downed transmission line that sparked the 2003 blackout in the Northeast—can cripple the network.” Kevin Kolevar, assistant secretary for electricity delivery and energy reliability at the Department of Energy

April 15th 2011 the International Copper Study Group (ICSG) said “global growth in copper demand for 2011 is expected to exceed global growth in copper production and the annual production deficit, estimated at about 250,000 metric tons of refined copper in 2010, is expected to be about 380,000 t in 2011. In 2012, refined usage is again expected to increase in all major world markets, with global demand expected to rise by more than 4%.”

The ICSG does not forecast copper production catching up with demand anytime soon, certainly not in 2011 or 2012.

"The global economy is running a major infrastructure deficit as the cost of decades of under-investment is now surfacing." Benjamin Tal, analyst CIBC World Markets

High Speed Rail (HSR)

To attract new businesses to our shores, we need the fastest, most reliable ways to move people, goods, and information — from high-speed rail to high-speed internet. Excerpt from US President Obama’s recent State of the Union address

Obama is calling for eighty percent of Americans to have access to high speed rail by 2036 - currently no American has access to high speed rail.

A projection from rail proponents FourBillion.com indicates that building the 9,000 miles of high speed corridors identified by the U.S. Department of Transportation would:

- Create 4.5 million permanent jobs and 1.6 million construction jobs

- Save 125 million barrels of oil

- Eliminate 20 million pounds of CO2 per mile per year

- Reinvigorate U.S. manufacturing

- Generate $23 billion in economic benefits in the US Midwest alone

These new lines also require massive support infrastructure: stations, metro transport links in cities and modern signaling/safety systems.

Copper is the key to the increased speed of modern high speed trains. Today’s high speed trains do not have a motor located in the locomotive, instead they use a series of motors and transformers located under the length of the train. New high-speed trains with their electric traction engines use from 3 to 4 tonnes of copper per train.

Copper is the key to the increased speed of modern high speed trains. Today’s high speed trains do not have a motor located in the locomotive, instead they use a series of motors and transformers located under the length of the train. New high-speed trains with their electric traction engines use from 3 to 4 tonnes of copper per train.

An additional 10 tonnes is used in the power (catenary system – overhead cable made of copper or copper-alloy that is suspended horizontally above the track and supplies the trains electricity) and communications cables per kilometer of track.

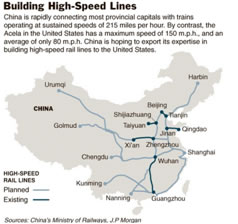

China’s already found an area where it could rapidly increase public investment to stimulate growth - rail construction.

China's total investment in high speed rail was first reported to be about US$300 billion - the Chinese planned a 12,000km high speed passenger network supplemented by 20,000km of mixed traffic lines capable of 200-250kph.

Recent reports indicate that over US$600 billion will be spent on rail construction during the 2011-2015 Five Year Plan. By 2020 there would be at least 16,000 km of passenger dedicated high speed rail. The total rail network by 2020 would be 120,000 km - 80% of it electrified.

By early fall 2010, the Ministry of Railways announced that China had more than doubled the length of high speed track to over 7000km.

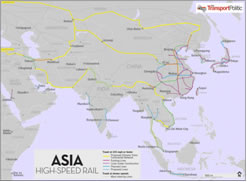

China has plans to construct its high speed rail line through Asia and Eastern Europe in order to connect to the existing infrastructure in the European Union (EU). Additional rail lines are planned into South East Asia as well as Russia – this will likely be the largest infrastructure project in history.

The project will include three major high speed lines:

- UK/Europe to Beijing (8,100 km) and then extend south to Singapore

- A second line will connect into Vietnam, Thailand, Burma and Malaysia

- The third line will connect Germany to Russia, cross Siberia and then back into China

Financing and planning for this monumental project is being provided by China – who is already in negotiations with 17 countries to develop the project . In return the partnering nation will provide natural resources to China.

Financing and planning for this monumental project is being provided by China – who is already in negotiations with 17 countries to develop the project . In return the partnering nation will provide natural resources to China.

"We will use government money and bank loans, but the railways may also raise financing from the private sector and also from the host countries. We would actually prefer the other countries to pay in natural resources rather than make their own capital investment." Wang Mengshu, a member of the Chinese Academy of Engineering and a senior consultant on China's domestic high-speed rail project

The exact route of the three lines has yet to be decided, but construction for the South East Asian line had already begun in the Chinese southern province of Yunnan and Burma is about to begin building its link. China offered to bankroll the Burmese line in exchange for the country's rich reserves of lithium, a metal widely used in batteries.

Russia and China have announced plans to build a new trans-Siberian link. Iran, Pakistan, and India are each negotiating with China to build domestic rail lines that would link into the overall transcontinental system.

China has mastered the art of building high speed rail lines quickly and inexpensively. “These guys are engineering driven — they know how to build fast, build cheaply and do a good job.” John Scales, the lead transport specialist in the Beijing office of the World Bank.

China hopes to complete this massive infrastructure project within 10 years

Conclusion

Major infrastructure projects typically boost productivity throughout the economy. Massive stimulus packages that focus on creating jobs at home - through public works projects – will, in this authors opinion, become very popular with governments looking to generate massive employment and restart the global economy.

Interest in the junior mining space is going to become intense but there is still time for investors to capitalize on the coming infrastructure boom.

Are junior resource companies, run by quality management teams with outstanding projects, on your radar screen?

If not maybe they should be.

By Richard (Rick) Mills

If you're interested in learning more about specific lithium juniors and the junior resource market in general please come and visit us at www.aheadoftheherd.com. Membership is free, no credit card or personal information is asked for.

Copyright © 2011 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Comments

|

Kent

25 May 11, 05:33 |

Dr. Copper

Copper has had its greatest bull run ever, and you write as if it's just getting started. There are a lot of reasons to think a bear is just getting started. |