Sovereign Debt, The Biggest Bubble of Them All

Interest-Rates / Global Debt Crisis May 15, 2011 - 12:00 PM GMTBy: John_Mauldin

This week we turn from the crisis brewing in the US to the one that is coming to a slow boil in Europe. We visit our old friends Greece and Ireland and ponder how this will end. It is all well and good to kick the can down the road, but what happens when you come to the end of the road? The European answer seems to be to haul in the heavy equipment and extend the road.

This week we turn from the crisis brewing in the US to the one that is coming to a slow boil in Europe. We visit our old friends Greece and Ireland and ponder how this will end. It is all well and good to kick the can down the road, but what happens when you come to the end of the road? The European answer seems to be to haul in the heavy equipment and extend the road.

I am asked all the time what my biggest worry is, and I quickly answer, the European Sovereign Debt Crisis. Of course, then we have to think about the Japanese Sovereign Debt Crisis, followed by the one in the US; but today we will focus on Europe. The biggest bubble in history is the bubble of government debt. It is a bubble in a world full of pins. It will take a great deal of luck and crisis management to keep it afloat, without wreaking havoc on the financial system and markets of the world.

The rumors have been flying all this week. Greek is going to leave the euro. No, it won't. Germans are demanding debt restructuring, and then they say no. A German newspaper is reporting that the EU, IMF, and Germany want a Greek debt extension, while the ECB (holders of Greek debt) and France oppose it. Greek two-year bonds are now paying 25% if you care to buy them in the open market, which is effectively the market voting for some type of debt restructuring or outright default.

I sat down this week and read two lengthy reports on how Greek debt could be restructured in an orderly manner. One was from HSBC and the other from Roubini Global Economics. There are ways it can be done. But the costs of the various options may be more than the affected parties want to bear. It is not a matter of pain or no pain; it is a decision as to who will bear the pain.

The fundamental problem for Greece is that there is no sign of economic recovery, with GDP at -4.5% in 2010 and still likely to be -3.0% in 2011 (IMF). If your economy slows down by 10%, then your debt-to-GDP ratio rises by 11% without any new debt. And Greece is being asked to further reduce its deficit by what is in effect 15% of GDP, while taking on no more debt. Within two years Greece will have a debt-to-GDP ratio of 160% that can only come down under very optimistic growth scenarios. And that assumes that Greece can right its own house. I have mentioned the wonderful article by Michael Lewis in Vanity Fair last October (http://www.vanityfair.com/business/features/2010/10/greeks-bearing-bonds-201010). He refers to the massive corruption in Greece:

"The scale of Greek tax cheating was at least as incredible as its scope: an estimated two-thirds of Greek doctors reported incomes under 12,000 euros a year--which meant, because incomes below that amount weren't taxable, that even plastic surgeons making millions a year paid no tax at all. The problem wasn't the law--there was a law on the books that made it a jailable offense to cheat the government out of more than 150,000 euros--but its enforcement. 'If the law was enforced,' the tax collector said, 'every doctor in Greece would be in jail.' I laughed, and he gave me a stare. 'I am completely serious.' One reason no one is ever prosecuted--apart from the fact that prosecution would seem arbitrary, as everyone is doing it--is that the Greek courts take up to 15 years to resolve tax cases. 'The one who does not want to pay, and who gets caught, just goes to court,' he says. Somewhere between 30 and 40 percent of the activity in the Greek economy that might be subject to the income tax goes officially unrecorded, he says, compared with an average of about 18 percent in the rest of Europe.

"... The Greek state was not just corrupt but also corrupting. Once you saw how it worked you could understand a phenomenon which otherwise made no sense at all: the difficulty Greek people have saying a kind word about one another. Individual Greeks are delightful: funny, warm, smart, and good company. I left two dozen interviews saying to myself, 'What great people!' They do not share the sentiment about one another: the hardest thing to do in Greece is to get one Greek to compliment another behind his back. No success of any kind is regarded without suspicion. Everyone is pretty sure everyone is cheating on his taxes, or bribing politicians, or taking bribes, or lying about the value of his real estate. And this total absence of faith in one another is self-reinforcing. The epidemic of lying and cheating and stealing makes any sort of civic life impossible; the collapse of civic life only encourages more lying, cheating, and stealing. Lacking faith in one another, they fall back on themselves and their families.

"The structure of the Greek economy is collectivist, but the country, in spirit, is the opposite of a collective. Its real structure is every man for himself. Into this system investors had poured hundreds of billions of dollars. And the credit boom had pushed the country over the edge, into total moral collapse."

It is a seven-page article and worth reading, as it gives you the scale of the problem that is Greece.

This week has seen yet more rioting by Greek unions. In effect they are protesting the latest debt negotiations, because they mean even more austerity. The French and Finns are demanding about $50 billion in privatization of government-owned enterprises, which means the loss of public jobs. The Germans have their own demands.

Both HSBC and Roubini assume there are options that can work to extend the debt maturities, lower the interest rates, and give Greece some room to work out its problems. But the solution to too much debt is not to increase the debt. No country save Britain at the height of its empire has ever recovered from a debt-to-GDP ratio of over 150% without a default. None.

And the reason is simple arithmetic. Even a nominal interest rate of 6% means that it takes 10% of your national income just to pay the interest. Not 10% of tax revenues, mind you; 10% of your total domestic production. That is a huge burden on any country. It sucks up half your tax revenues (or more), leaving not enough to pay for ordinary government services like police, defense, education, pensions, health care, etc.

Greece runs a massive trade deficit with the rest of Europe, which just makes the problems worse. Unemployment in Greece is now 15% and rising. And everyone can clearly see that the current loan facility will run out at the beginning of 2010, yet Greece will need at least another 30 billion euros right after that. They clearly are not going to be able to access the private markets, so they are negotiating now to get more money to carry them into 2013, when the new European Stability Mechanism will in theory be in place (more below).

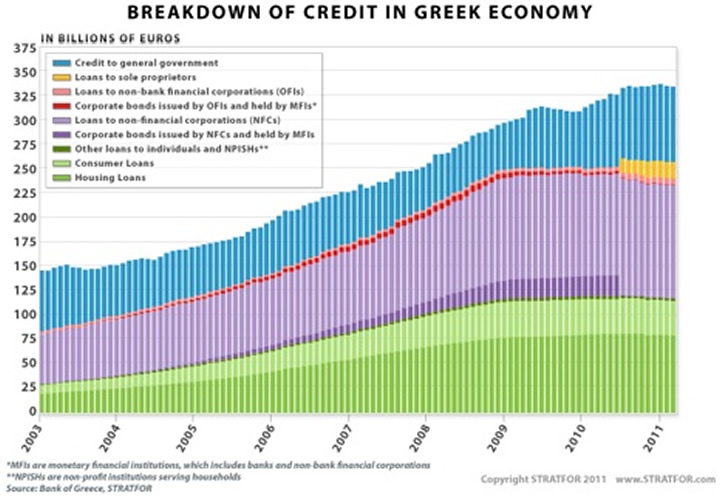

But an interesting thing is happening. Greece consumer and business debt is rising in the midst of what can rightfully be called a depression. How can that be? Don't consumers and businesses retrench in a recession? Look at this chart from Stratfor:

As they write:

"Despite further expected unemployment, the Greek household sector remains considerably indebted, with only marginal deleveraging occurring. This is a worrying sign because it shows that Greek consumers have not been able to cut down their debts and have not reduced their standards of living in light of severe economic crisis. They may be unable to reduce their debts precisely because many have lost jobs or had their public sector salaries significantly reduced and are therefore depending on consumer credit to maintain their levels of expenditure and to service their debts (paying credit card bills with more credit card debt, as an example). Meanwhile, the overall banking sector has actually increased the amount of credit it has extended to consumers, corporations and the government. The total amount of credit outstanding was more than 333 billion euros in February -- more than the 325 billion euros-worth of credit outstanding in May 2010, with the most significant increase in lending from banks going to the government itself.

"The problem, however, is that the government cannot decrease lending to consumers or force its banks to do so. That would not only throw Greece into an even deeper recession, it would also cause considerable pain to Greek citizens already frustrated to the point of protest."

I am not persuaded that it is all an inability of Greek consumers and businesses to pay down debt. The rumors that Greece will go back to the drachma are not without reason, as I will detail shortly. If they did, it makes real sense for someone who wants to buy a car to do so today, as the drachma will quickly fall 50%, which doubles the price of that German, French, or Italian car. If you are a business, you might be thinking it makes sense to move forward your capital investment, as any non-Greek equipment will become decidedly more expensive post leaving the euro.

Note: I am not saying that Greece will behave this way, just that it makes sense for those who want to make capital investments to hedge their bets, just in case.

Roubini writes:

"A haircut of 20-50% is required to achieve debt sustainability. To put things into perspective, it is worth considering the magnitude of haircut required to make debt clearly sustainable. For simplicity at this stage, we consider face-value haircuts in our debt sustainability analysis toolkit and find that a haircut of around 20% on the total stock of debt would allow Greece to achieve a debt-to-GDP ratio of 60% by 2030. This assessment is based on the macroeconomic projections in the IMF's April 2011 WEO; however, more conservative macroeconomic projections suggest a haircut of around 50% could be necessary."

But such a haircut would also mean that the Eurozone member countries would have to fund Greek debt for a long time, as the private markets would simply shut them out until real credibility was established. And that might take some time. The Greeks have long made a practice of defaulting on debt. The first recorded sovereign debt defaults were the Greek city-states, over 2,000 years ago. Greece has been in default 150 of the last 200 years.

Such perpetual funding will not be popular, and already one can see the rise of euro-skeptic parties all over Europe. Nothing can be done without Germany, and Angela Merkel is in danger of losing her coalition. One of her junior members, the right-of-center and very pro-euro Free Democratic Party, which is very necessary to Merkel, might not even get enough votes to qualify for representation in parliament if a new election were held today.

And the ESM mentioned above has to be voted on and approved by all 27 countries that are treaty members, as it requires a change to the treaty that created the EU. I think getting unanimous approval might be difficult if it means countries have to be responsible for Greek debt.

One of the reasons normally given for extending the debt to Greece is that it would avert a crisis of the euro. I am not so sure. If Greece were allowed to leave I think the euro would get stronger.

I think both Greece and the EU would be better off if Greece did default, but it's not my decision. Just saying.

Ireland is a Different Story

Morgan Kelly is professor of economics at University College Dublin. He is not popular at times with the establishment, as he points out their foibles, but he has a very good track record of being right. He recently wrote a devastating piece for the Irish Times, which has gone viral in Ireland. (http://www.irishtimes.com/newspaper/opinion/2011/0507/1224296372123_pf.html)

He basically points out that the Irish cannot afford to pay the debts of their banks. He suggests they simply walk away. His conclusion:

"The original bailout plan was that the loan portfolios of Irish banks would be sold off to repay these borrowings. However, foreign banks know that many of these loans, mortgages especially, will eventually default, and were not interested. As a result, the ECB finds itself with the Irish banks wedged uncomfortably far up its fundament, and no way of dislodging them.

"This allows Ireland to walk away from the banking system by returning the Nama assets to the banks, and withdrawing its promissory notes in the banks. The ECB can then learn the basic economic truth that if you lend €160 billion to insolvent banks backed by an insolvent state, you are no longer a creditor: you are the owner. At some stage the ECB can take out an eraser and, where "Emergency Loan" is written in the accounts of Irish banks, write "Capital" instead. When it chooses to do so is its problem, not ours.

"At a stroke, the Irish Government can halve its debt to a survivable €110 billion. The ECB can do nothing to the Irish banks in retaliation without triggering a catastrophic panic in Spain and across the rest of Europe. The only way Europe can respond is by cutting off funding to the Irish Government.

"So the second strand of national survival is to bring the Government budget immediately into balance. The reason for governments to run deficits in recessions is to smooth out temporary dips in economic activity. However, our current slump is not temporary: Ireland bet everything that house prices would rise forever, and lost. To borrow so that senior civil servants like me can continue to enjoy salaries twice as much as our European counterparts makes no sense, macroeconomic or otherwise.

"Cutting Government borrowing to zero immediately is not painless but it is the only way of disentangling ourselves from the loan sharks who are intent on making an example of us. In contrast, the new Government's current policy of lying on the ground with a begging bowl and hoping that someone takes pity on us does not make for a particularly strong negotiating position. By bringing our budget immediately into balance, we focus attention on the fact that Ireland's problems stem almost entirely from the activities of six privately owned banks, while freeing ourselves to walk away from these poisonous institutions. Just as importantly, it sends a signal to the rest of the world that Ireland - which 20 years ago showed how a small country could drag itself out of poverty through the energy and hard work of its inhabitants, but has since fallen among thieves and their political fixers - is back and means business.

"Of course, we all know that this will never happen. Irish politicians are too used to being rewarded by Brussels to start fighting against it, even if it is a matter of national survival. It is easier to be led along blindfolded until the noose is slipped around our necks and we are kicked through the trapdoor into bankruptcy.

"The destruction wrought by the bankruptcy will not just be economic but political. Just as the Lenihan bailout destroyed Fianna Fáil, so the Noonan bankruptcy will destroy Fine Gael and Labour, leaving them as reviled and mistrusted as their predecessors. And that will leave Ireland in the interesting situation where the economic crisis has chewed up and spat out all of the State's constitutional parties. The last election was reassuringly dull and predictable but the next, after the trauma and chaos of the bankruptcy, will be anything but."

I totally agree. I have been writing for a long time that Ireland should not bail out their banks. They simply cannot afford to. Tell the EU and British banks to go pound sand. Kelly is right, it will mean serious budget cuts; but like Iceland when it rejected baking its banks, it will mean a quick recession and then growth can start again. The Irish have a very different national character than Greece; and once things get righted, the markets would soon be willing to take Irish debt. Russia and Argentina other countries have defaulted and within a few years were back in the capital markets. Ireland could be too.

I am very seriously thinking of going to Ireland this summer to just talk to local people and see for myself what is going on. Ireland sounds a lot better than the Texas heat in August.

Kicking the Can to the End of the Road

European leaders will continue to try to kick the can down the road. I would not be surprised to see no real "crisis" this year. But there is an Endgame. And I think it involves voters and not just leaders. The guy in the street can see that bailing out countries is really just a back-door way to bail out banks on the backs of taxpayers and the currency. If it were just Greece, maybe. But it is Portugal and Spain. Especially Spain. Spain is too big to save. I love Spain; it is one of the most beautiful and gracious of countries. But there are real problems. The banks have maybe - maybe - written down their housing-related losses 10%. It should be more like 40%, which would make most Spanish banks insolvent, so they won't write them down. Unemployment is over 20% and rising. Like Ireland, they allowed their housing market to get away from them. They believed that someone was going to buy all those homes they were building. And now they are teetering on recession and likely to fall back soon, which makes collecting taxes and cutting spending more difficult. With each new data point this year, Spanish debt costs will rise.

Each new version of the crisis will spook the bond markets yet again. When you look at the economies of the euro-peripheral countries, it is hard to see how they can dig themselves out without a great deal of pain and serious spending cuts, which of course means slower economies and even more pain. But that is the only way through, short of the Eurozone basically guaranteeing all debt for a long time, which means you are asking Finnish and German and Dutch and French voters to agree to take on more taxes to pay that debt. Or it means a real loss of sovereignty and control for debtor nations. (Maybe I should take in a trip to Portugal as well. Another country I have yet to visit, and another crisis to take note of firsthand.) I cannot see European countries giving up their national sovereignty willingly.

In the end, this comes down to elections. It becomes not a matter of high finance and political will on the part of European leaders, but of how you convince the burghers in Germany and the practical Dutch (et al.) of the need to share some Greek pain. It requires convincing the Irish people to assume that bank debt, when they have already told their leaders no. I am glad that is not my job.

In short, we are watching the biggest bubble of all time, the bubble of government debt, try to keep from popping. My bet is that it can't. And while the ride will be bumpy, the world our kids get will be better off at the end of the process.

Philly, Boston, Trequanda, Kiev, Geneva, and London

Next Monday a week I head for Philadelphia for a night, then on to Boston, and then the next Sunday leave for Italy to catch up with my kids in Tuscany, in the small village of Trequanda. I will vacation for a few days with them, and then take a few weeks working vacation, working on my next book and visiting with friends who drop by. I am really looking forward to it.

Then I will take my youngest son, Trey, to Kiev for a few days, on to Geneva for some meetings and speeches, and a side trip to visit CERN. Then one day in London to guest host Squawk Box on CNBC. While flying in Europe is not especially pleasant (the seats are small and the baggage costs are high), the trips do sound nice.

The only down side to leaving is that my Dallas Mavericks may be poised to go back into the NBA Finals while I am in Europe. I have been blessed with good seats and do love professional basketball. I think it is the most beautiful of team sports. What these guys can do is simply not possible for mere mortals. This coming week Dallas will host two games for the Division Championship, and I will be there. I missed the Lakers series by being on the road. I watched the last Dallas-Lakers game from the Admirals Club in Los Angeles, where I was the only person at the bar who was happy. That was a true blowout. It was hard to believe. Can you think of a Dallas - Miami Heat final series again? Can they get past Chicago? You gotta love this game.

I am taking it a little easier, not setting the alarm clock and getting some much-needed rest. And the doctor says I can get back into the gym soon, as my heel is healing well. Enjoy your week.

Your trying to figure all this out analyst,

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2011 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.