The End of Bernanke's "End Game"

Interest-Rates / Central Banks May 13, 2011 - 08:58 AM GMTBy: William_Anderson

In a recent screed masquerading as the thoughts of a Nobel prize winner in economics, Paul Krugman excoriates those who speak of

In a recent screed masquerading as the thoughts of a Nobel prize winner in economics, Paul Krugman excoriates those who speak of

fear: fear of a debt crisis, of runaway inflation, of a disastrous plunge in the dollar. Scare stories are very much on politicians' minds.

As Krugman explains, such worries are irrational and certainly untrue:

As Krugman explains, such worries are irrational and certainly untrue:

None of these scare stories reflect anything that is actually happening, or is likely to happen. And while the threats are imaginary, fear of these imaginary threats has real consequences: an absence of any action to deal with the real crisis, the suffering now being experienced by millions of jobless Americans and their families.

In other words, there is no real inflation, and to even broach the subject is proof that one hates the poor and jobless.

The rise of prices for fuel, food, and other commodities is nothing more than a reflection of their "volatility." And the decline of the US dollar against other fiat currencies of the world is a good thing, because it will improve US manufacturing sales.

But while Krugman takes the move-along-folks-nothing-to-see-here approach to the real crises at hand, calling them "phantom menaces," others are looking at the horrific damage that Ben Bernanke and his allies in both the Bush and Obama administrations have created — and rightly seeing even more crises ahead. To make things even more ironic, we are seeing a situation akin to what occurred in the early 1930s; Bernanke and others claim they want to avoid the "mistakes" make by the Federal Reserve System at that time, and so they are following the same path the Fed took 80 years ago. We are at the end of the "end game" that Bernanke and his allies have been imposing upon the rest of us.

Forget for the moment the argument that Krugman and others have made, that the economy is in that "special case": the "liquidity trap," which requires an infusion of massive government spending in order to snap the economy back into prosperity. Instead, let us look at the actions the Fed took right after the failure of Lehman Brothers in September 2008, a failure that "convinced" Congress to bail out Wall Street.

Until that time, the Fed's portfolio consisted mostly of short-term Treasuries, something one would expect given the nature of the central bank's open-market activities, in which it would buy and sell government bonds in order to increase or shrink the economy's monetary base. However, the Wall Street crisis provided the fig leaf allowing the Fed to play the role of the rich uncle who bails out family members when they become financially overextended.

Thus, Bernanke's minions entered the financial marketplace with a bottomless checkbook, purchasing assets that had lost value (like mortgage securities, AIG stock, and the like) in the marketplace. However, in order to make it look as though the markets were fine, the Fed purchased these securities at prices close to their precollapse worth; Bernanke and company were playing the let's-pretend-this-worthless-paper-is-valuable game.

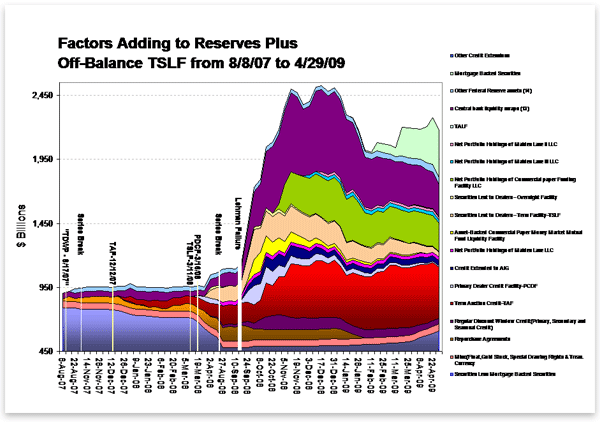

If you want a sense of just how reckless the Fed turned out to be in its rich-uncle role, the diagram below will help put things into perspective:

Source: Federal Reserve Bank of Atlanta

This was supposed to be Bernanke saving the economy, at least in the short term, but actually Bernanke's actions did no such thing. At this point, the gulf between the Austrians (who are unanimous in their criticism of Bernanke's actions) and the Keynesians (whose only regret is that Bernanke did not purchase even more worthless assets) is exposed. Let me explain.

In the Keynesian analysis, assets are held to be homogeneous, and the economy is believed to be a bland mixture of those assets that are fully employed when the amount of consumer and investment spending is high enough to continue to give the economy "traction."

When consumer and investment spending flag, however, Keynesians hold that the government must step in by borrowing and printing money in order to revive the spending circle. If the government spends enough, then the economy can move on its own to the point where consumers and investors keep it going — at least until the next crisis. Keynesians call this movement the "circular flow," although it is more like circular logic, in which the premise is the conclusion and the conclusion is the premise.

What must never happen is a large-scale liquidation of assets, because that would trigger deflation, which would be accompanied by an endless downward spiral and an economy stuck in a "liquidity trap" with falling prices and high unemployment. Thus, in the Keynesian view, the Fed was justified in purchasing these worthless assets, because it prevented their liquidation and preserved at least their "paper" values.

Austrians, however, take a much different view. What Keynesians call idle resources, which need only an injection of spending to be reemployed, Austrians call malinvested resources. The different is crucial, because Keynesians believe that the Fed's actions prevent an economic downward spiral, while Austrians hold that what the Fed has done furthers the economic downturn.

The difference in opinion centers on causality. Keynesians believe that the downturn is created simply by a reduction in spending, while Austrians hold that the recession is caused by the fact that the series of malinvestments created during the previous boom cannot be sustained. The drop in spending is the result of the downturn, not its cause. The difference in beliefs is crucial: in the Austrian paradigm, trying to sustain the boom conditions by injecting new government spending will always end in disaster.

The reason is simple: it takes real resources to prop up malinvestment, resources that should be going to those investments that fit within a sustainable structure of production. This point is absolutely crucial. Keynesians believe that because there are "idle" factors of production, directing them toward anything is better than letting them go unemployed; the opportunity cost of using them tends toward zero.

The Keynesian paradigm holds that if these idle factors are not directed by new government spending, they will be unemployed for an indefinite time period, as the system is locked into a "liquidity trap" and cannot move away from this perverse "equilibrium" without government help. Thus, massive new injections of government spending are absolutely necessary to keep the economy from imploding into deflation and depression.

To a Keynesian like Krugman, the only question one needs to ask is how much spending is needed. That the economy has not really moved in the direction of full employment is prima facie evidence to Krugman that spending has been too low, and he dismisses criticisms of his theory as the rantings of lunatics.

But here is the problem: despite Krugman's complaint that government spending is not high enough and despite his defense of Bernanke's actions against criticisms from people like Ron Paul (whom Krugman never misses a chance to smear with false allegations), the truth is that the Fed and the Obama administration are at the end of the tracks, and their train cannot go any farther. Even though the Fed and the government have thrown billions of dollars at the housing market to try to keep housing prices from falling, prices are falling.

Furthermore, even though Krugman admits the "recovery" is running out of steam, he blames people like Ron Paul because they don't believe the Fed should be in the money-printing business. What Krugman and Bernanke refuse to even acknowledge is that the scheme of diverting resources to prop up the failures of the last boom's malinvestments is a colossal failure, and until government policymakers stop trying to reflate the failed boom, there will be no recovery.

Ben Bernanke has opened the Fed's checkbook in an unprecedented fashion, and while he claims to be "saving" the financial system, in reality he is destroying it. He has kept the failed firms afloat, thus preventing the necessary transfers of resources from lower-valued uses to higher-valued uses. (Like Krugman and his boss, President Obama, Bernanke seems to believe that government can create wealth by transferring resources from higher-valued to lower-valued uses, the reason being that government can order any set of values into existence by sheer coercion.)

Although Bernanke and others arrogantly dismiss the rise in commodities like gold, silver, oil, and agricultural products as having nothing to do with the Fed's overt policies of inflation, it is clear that the markets are ignoring these "experts," paying no attention to the men behind the curtain. People are making their own decisions with their own money, and more and more they are voting Bernanke and his declining dollars off the island.[1]

So, trillions of dollars later, with the dollar hopelessly debased, we find we are no better off than when we started, and the necessary asset liquidation has barely begun (thanks to Bernanke). While Krugman and others claim that Bernanke has saved the economy from sliding into depression, I think he has merely guaranteed that things are going to get a lot worse.

William Anderson, an adjunct scholar of the Mises Institute, teaches economics at Frostburg State University. Send him mail. See William L. Anderson's article archives. Comment on the blog.![]()

© 2011 Copyright Ludwig von Mises - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.