Stock Market Uptrend Resuming

Stock-Markets / Stock Markets 2011 Apr 16, 2011 - 08:55 PM GMTBy: Tony_Caldaro

Last week the world indices did quite well while the US struggled. This week the US held its own while the world indices were solidly in the red. For the week the SPX/DOW were -0.45%, and the NDX/NAZ were -0.60%. Asian indices were -1.0%, Europe dropped 1.6%, the Commodity equity group lost 3.4%, and the DJ World was -1.1%. Bonds were +1.2%, Crude lost 2.8%, Gold added 0.8% and the USD was flat.

Last week the world indices did quite well while the US struggled. This week the US held its own while the world indices were solidly in the red. For the week the SPX/DOW were -0.45%, and the NDX/NAZ were -0.60%. Asian indices were -1.0%, Europe dropped 1.6%, the Commodity equity group lost 3.4%, and the DJ World was -1.1%. Bonds were +1.2%, Crude lost 2.8%, Gold added 0.8% and the USD was flat.

US economic reports for the week were strongly positive; 13:4. On the negative side: the Twin deficits remains solidly in the red, weekly jobless claims increased and the M1-multiplier made another new low. On the positive side: import/export prices remained positive, as did the PPI/CPI, retail sales and business inventories; the NY FED improved, along with industrial production, capacity utilization, consumer sentiment and the WLEI; the monetary base and excess reserves made new highs. Next week will be highlighted by Housing, the Philly FED and the BEA Leading indicators.

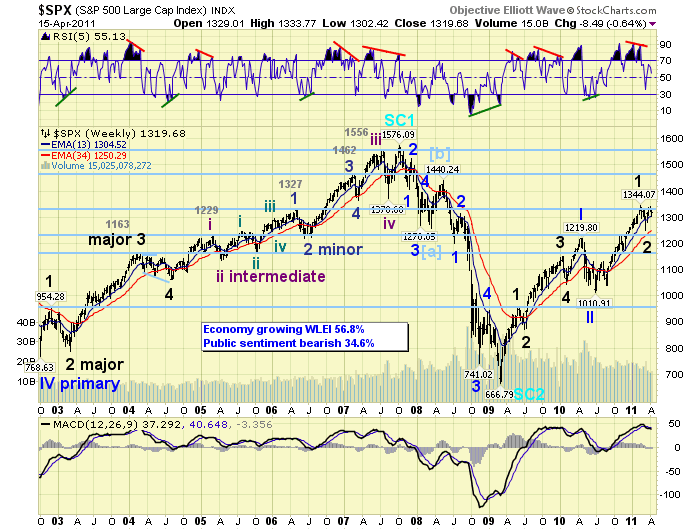

LONG TERM: bull market

The bull market of March 2009 continues, and we are counting it as a five Primary wave advance creating Cycle wave [1] of the next Supercycle wave. The first Primary wave concluded in Apr10 at SPX 1220. Primary wave II followed, bottoming in July10 at SPX 1011. Primary wave III has been underway since then.

Since Primary I consisted of five Major waves: Major 1 SPX 956, Major 2 SPX 869, Major 3 SPX 1150, Major 4 SPX 1045, Major 5 SPX 1220. Primary III should also unfold in five Major waves: Major 1 SPX 1344, Major 2 SPX 1249, Major 3 underway now. We’re targeting a Major wave 3 top around SPX 1450, and a Primary III top around SPX 1550 both this year.

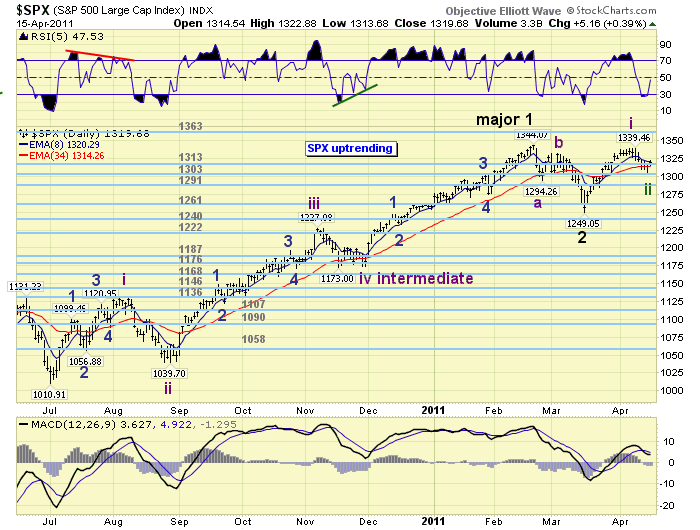

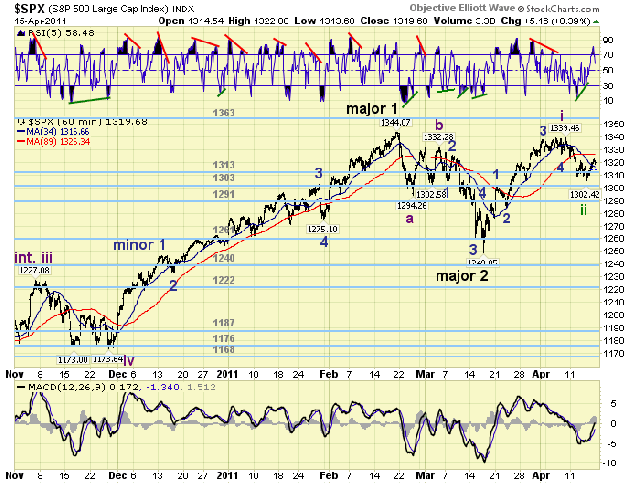

MEDIUM TERM: uptrend high SPX 1339

After getting within five points of the bull market high (SPX 1344) on April 6th the uptrend stalled and the market started to pullback last friday. The pullback lasted for most of the week as the SPX hit 1302 on thursday. Since this pullback is clearly the largest one of the new uptrend, (37 points), we have labeled the SPX 1339 high as Intermediate wave one, and the SPX 1302 low, tentatively as Intermediate wave two.

At the SPX 1302 low we observed a positive divergence on the hourly chart, and an oversold condition on the daily chart. Two things we look for at important lows. Then the OEW charts turned positive on friday when the SPX rallied above 1320. Should Intermediate wave three be underway, as expected, we should now observe a five Minor wave advance to between SPX 1386 and 1440 into May.

SHORT TERM

Support for the SPX remains at 1313 and then 1303, with resistance at 1363 and then 1372. Short term momentum hit overbought on friday and then headed toward neutral into the close. The completion of Intermediate wave one was a bit tricky as Minor wave 5 was only 12 spx points, and occurred while the market bounced off of 1338/1339 for four consecutive days. Nevertheless, we noted this possibility last weekend, posted the count on the DOW hourly chart, and provided some downside parameters.

The pullback initially found support at the 1313 pivot, but the gap down on thursday pushed the SPX to the 1303 pivot. After that low the market had its best rally, 21 spx points, since the pullback began. With the short term OEW charts positive we now have support at SPX 1318, then the 1313 and 1303 pivots. Overhead resistance is at 1339/1344, plus the 1363 and 1372 pivots. Best to your trading!

FOREIGN MARKETS

Asian markets were mostly lower on the week for a net loss of 1.0%. All but Japan’s NIKK are in confirmed uptrends.

European markets were all lower on the week -1.6%. Only England’s FTSE and Spain’s IBEX are in confirmed uptrends.

The Commodity equity group were all lower on the week -3.4%. All three indices remain in confirmed uptrends.

The uptrending DJ World index lost 1.1% on the week.

COMMODITIES

Bond prices continue to downtrend but had a good week +1.2%. 10YR yields remain between 3.14% and 3.74%. The 1YR remains in its multi-month trading range, and LIBOR is making new all time lows.

Crude had quite a volatile week -2.8%. After hitting $114 on monday it was sharp down to $106 by wednesday before a rebound to $110 friday. Crude is still in an uptrend, has not violated any wave patterns, and may not be done going higher. Always a tough market.

Gold followed Crude day by day but performed better +0.8%. On friday, uptrending Gold hit a new all time high at $1488. Silver, +5.0% on the week, hit $43 on friday.

The USD (0.0%) made new downtrend lows this week as it approaches support at 74.23. The uptrending Euro lost ground -0.4%, but the JPY rallied +1.9%.

NEXT WEEK

Monday kicks off the holiday shortened week with the NAHB index at 10:00. On tuesday, Housing starts and Building permits at 8:30. Wednesday we have Existing home sales. Then on thursday, weekly Jobless claims, the Philly FED, Leading indicators and the FHFA index. Nothing scheduled for the FED. Best to you and yours this holiday week!

CHARTS: http://stockcharts.com/...

http://caldaroew.spaces.live.com

After about 40 years of investing in the markets one learns that the markets are constantly changing, not only in price, but in what drives the markets. In the 1960s, the Nifty Fifty were the leaders of the stock market. In the 1970s, stock selection using Technical Analysis was important, as the market stayed with a trading range for the entire decade. In the 1980s, the market finally broke out of it doldrums, as the DOW broke through 1100 in 1982, and launched the greatest bull market on record.

Sharing is an important aspect of a life. Over 100 people have joined our group, from all walks of life, covering twenty three countries across the globe. It's been the most fun I have ever had in the market. Sharing uncommon knowledge, with investors. In hope of aiding them in finding their financial independence.

Copyright © 2011 Tony Caldaro - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.