Credit Crunch to Credit Crisis - Financial Sector Crash Continues

Stock-Markets / Credit Crunch Nov 10, 2007 - 01:28 AM GMTBy: John_Mauldin

In this issue:

In this issue:

- A Confidence Credit Crunch Credit Crisis

- How Much is That Dog in Your Net Capitalization?

- King Dollar Faces the Guillotine

- The Euro-Yen Cross

- The Consumer is Getting Tired

- New York, Philadelphia, Switzerland and Phoenix

Just when it felt like it was safe to get back in the water, a second and potentially much meaner version of this summer's credit crisis has reappeared. This week we look at why there are more mortgage write downs coming (in a self-fulfilling prophecy) in the financial sector, how an obscure new accounting rule is shedding light on a lot of risk in the world's banking system, how this is all tied to the consumer and is part of the reason for the fall in the dollar.

It's a complex world, and I am going to spend a considerable part of a beautiful Friday evening in Texas trying to make it simple for you, gentle reader. That's my job, and I love it. And since I can't think of my usual "but first" we'll jump right in.

A Confidence Credit Crunch Credit Crisis

I have written for some time that we are in a credit crisis brought on by a lack confidence which has the real possibility of devolving into a credit crunch which will make loans harder to get and has the potential to slow down the US economy, on top of a weakening consumer. Data released in the past few months, and again this week, have shown that banks and other lenders are tightening their standards for all sorts of loans. And it is not just that they are becoming more like an old-fashioned banker who actually wanted to know that he could get his money back. Their new found conservatism is being forced on them. But let's start at the beginning.

The Financial Accounting Standards Board (FASB) is the referee for accounting practices. They recently issued a new rule which will be implemented November 15. Essentially, Statement 157 requires a financial firm to divide its assets into three categories called simply enough, Level 1, Level 2 and Level 3.

Under FASB terminology, Level 1 means assets that can be marked-to-market, where an asset's worth is based on a real price, like a stock quote. Level 2 is mark-to-model, an estimate based on observable inputs which is used when no quoted prices are available. You can go get several bids and average them, or base your assumption on what similar assets sold for.

Level 3 values are based on "unobservable" inputs reflecting companies' "own assumptions" about the way assets would be priced. That would be market talk for best guess, or in some cases SWAG (as in Simple Wild-***ed Guess.)

Financial companies have never had to break out this information. As you might expect, there is particular interest in how much and what kind of Level 3 assets a bank or brokerage firm might have. It turns out, that there may be more problems lurking in those assets than we realize.

Nouriel Roubini gave us some numbers earlier this week. It seems that some companies have far more Level 3 assets than they have capital. Take a look at these six banks which have already posted their Level 3 assets ahead of the deadline:

| Citigroup | Goldman Sachs |

| Equity base: $128 billion | Equity base: $39 billion |

| Level three assets: $134.8 billion | Level 3 assets: $72 billion |

| Level 3 to equity ratio: 105% | Level 3 to equity ratio: 185% |

| Morgan Stanley | Bear Stearns |

| Equity base: $35 billion | Equity base: $13 billion |

| Level three assets: $88 billion | Level three assets: $20 billion |

| Level 3 to equity ratio: 251% | Level 3 to equity ratio: 154% |

| Lehman Brothers | Merrill Lynch |

| Equity base: $22 billion | Equity base: $42 billion |

| Level three assets: $35 billion | Level 3 assets: $35 billion |

| Level 3 to equity ratio: 159% | Level 3 to equity ratio: 38% |

Now just because something is illiquid does not mean that it has no value. Real estate may be considered illiquid and have no "observable" price, but there is some value. The same can be said for private equity holdings. There are often very good business reasons to hold such assets.

But as the Financial Times noted this week, valuing these assets is not easy.

"As the technology bubble imploded, fund managers stopped pretending to know what ethernet routers did and started asking what life would look like if all tech stocks halved in value. The structured credit market has yet to reach this moment of clarity. As is typical when the sky falls in, many specialists, obsessed with complexity, point to the impossibility of generalizing about the weather.

"It is true that in terms of the vintage and profile of the underlying collateral, and the priority of claims on it (subordination), a dazzling range of permutations exist for collateralized debt obligations. And the $23bn of subprime write-offs so far from the three banks worst hit suggest intellectual chaos: relative to their remaining exposure to "super- senior" CDOs, UBS wrote down 8 per cent, Merrill Lynch 41 per cent, while Citigroup's guidance is 19 per cent."

So we really do not know much more than what we have above. There is no break out (that I could find) that details what is in Level 3. Where are the mortgage CDOs and conduits? Are they Level 2 or Level 3? There is going to be a demand for yet more transparency as this information yields a lot of questions. Among other things, how much do Level 3 assets contribute to your net capital position? And that is important because your net capitalization (net cap from here on) determines how much you can lend.

How Much is That Dog in Your Net Capitalization? First off, there were some analysts who are writing that the sky is falling and that banks are going to have to write-down massive amounts of capital destroying their capital structure. Not true. Let me give you a simple analysis. Stay with me as this will be important later.

I own what may be the world's least complex broker-dealer (member FINRA) and a futures firm (member NFA). As 99% of my business is basically referral, I simply get a few checks each month, and pay expenses.

But even though I directly handle no client assets, I still have to have a certain minimum capitalization in the business, as is required by FINRA and the NFA. So, I simply keep my required capitalization in a CD (certificate of deposit) in a bank. But it is not that simple. I have to make sure (or Tiffani does) that at the end of the month we deduct all the liabilities against that CD (notice I did not say cash).

If for some reason revenues are less than projected and expenses (like legal bills) were more that anticipated, I would have to find capital to put into the company in order to keep my net capitalization ("net cap") above my required amount.

Now, in figuring the net cap, all assets are not equal. That CD, for example, is only worth 99.5 cents on the dollar toward my capital, because FINRA assumes that there could be a penalty for early withdrawal. That 1/2% deduction is called a haircut.

Different types of assets get different haircuts. Some haircuts on volatile or illiquid assets can be very steep. And I can guarantee you the regulators pay very close attention to your net capital reports. So, the Level 3 assets which are just now being reported have already been given an appropriate haircut. The fact that financial firms are disclosing the difference in the quality of assets has very little (or should have very little) to do with how those assets contributed to their net cap prior to the disclosures.

However, that does not mean that certain assets and specifically anything related to mortgages are not going to come under continued pressure. Estimates of $200-$250 billion in losses from subprime exposure are common. Royal Bank of Scotland Group chief credit strategist Bob Janjuah put out a report Wednesday estimating that the credit crunch will cause $250 billion to $500 billion of losses at banks and brokers around the world.

"This credit crisis, when all is out, will see $250 billion to $500 billion of losses," said Janjuah, who's based in London. "The heat is on and it is inevitable that more players will have to revalue at least a decent portion of assets they currently value using 'mark-to-make believe.'"

(I should note that the majority of these assets are not in banks but in pension funds, insurance portfolios, hedge funds, etc. Those losses have not yet been accounted for.)

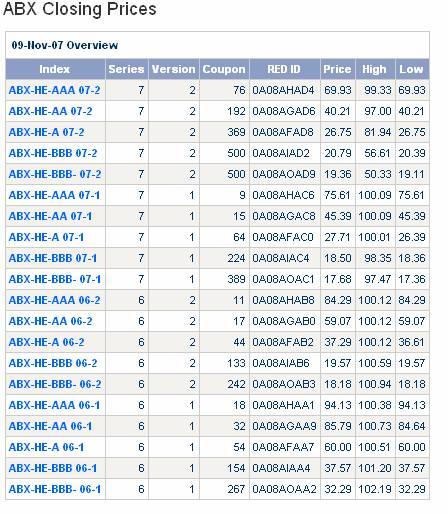

Below is a table from www.markit.com . It is a list of various mortgage asset backed indexes based on securities that were created in 2006 and 2007. The indexes are composed of 20 different asset backed securities from major investment houses. These securities are in turn comprised of loans that were made in 2005-2007. For instance, the top index is the ABX-HE-AAA 07-2, which means this is an Asset Backed Security, Home Equity and all the securities in the index are AAA rated tranches and the securities were put together in the second half of 2007. The securities have a potential life of 30 years, which by then all the loans would have been paid.

The first five indexes listed are the various tranches of the same 20 securities. The next five listed are for another series of indexes created from 20 different asset backed securities put together in the first part of 2007. The next five are from 2006. The bottom five are from a group put together in early 2006 comprised of loans from 2005.

Once again. Each of these represents an index comprised of 20 different asset backed securities with the same rating from various ratings agencies. These indexes are created so that investors can hedge their portfolios if they want to, and traders can speculate either long or short. You can view more details and the actual securities if you are morbidly curious at the website.

Now notice something interesting. The AAA tranche from the top index, the one created just a few months ago, has lost over 30% of its value. Yet the AAA tranche from the first index series (in 2006) is only down 5.87%. The same relationship holds with whatever rating you want. The older it is, the less the losses. Further, an A rated index from 2007 is not worth what a BBB-tranche is from just two years ago!

Clearly the market is saying that loans that were made in 2007 are not worth nearly as much as loans that were made in 2005. And guess which mortgages are more likely to be on investment bank books?

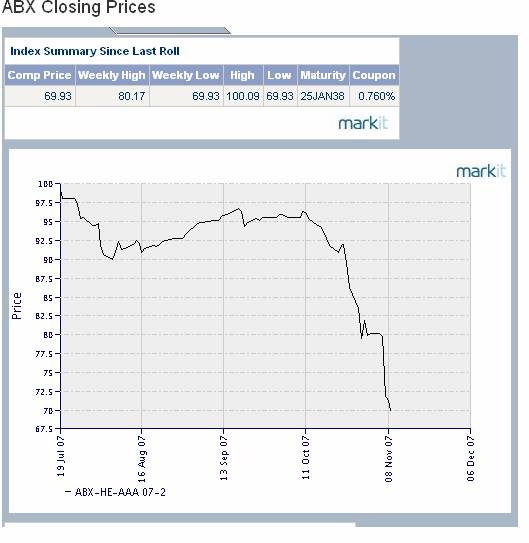

Now, for those of us who are visual, let's look at what that AAA tranche has done since its inception just five months ago. This index was trading at $.96 just a little over one month ago, and is now down to $.69!!! The drop in value has been in one month.

Many analysts are wondering why Merrill and Citigroup first stated losses to be one amount and then came back a few weeks later with another much larger amount. Looking at the above graph makes it at least partially clear. While the above chart is the steepest in terms of a drop in the last month, all the other indexes showed similar volatility in October.

Quite simply, assets that had one value at the beginning of the month had another value at the end.

Further, many of those assets have fallen further in the last week. This suggests that further write downs are around the corner. There is still pain in the days and weeks to come for many of the best known financial names.

Remember that net cap issue we discussed earlier? Now we come to the relevance of what would normally be an arcane and uninteresting subject. When you submit your net cap reports, you have to justify the value you place on the assets.

It used to be (and not so long ago) you could play some games, like taking the bid price on an asset one quarter and the ask price the next, depending on whether you wanted to increase your earnings or "bank" some earnings for the future. It allowed for some gaming of the numbers. Now you have to show a consistent methodology. Further, the accounting firms are far more rigorous in a Sarbanes-Oxley world. They are far more insistent that clients show realistic numbers.

You cannot go to a regulator and say, "We think the market is crazy and we are not going to mark this asset down." As my Dad used to say, "That dog won't hunt."

The ABX indexes create a price comparison that cannot be ignored when you are putting together your accounting for your net cap reports. If the index is dropping, you are going to have to mark your assets down if you have similar assets on your books. Period, end of story. You can lose a great deal if you don't. It is not worth it.

Let's take a side trip for a moment and look at a 2002 vintage AAA mortgage backed asset. It is probably still capable of being rated AAA. Why? Because the bad lending practices were not prevalent, any mortgages still in existence have been paid on for almost six years, and the underlying homes may have appreciated anywhere from 50-100%. It would take a disaster of biblical proportions for that AAA tranche to lose money. By that I mean that 60% of the loans would have to lose 50% of their 2002 value (or 75% of their 2007 value) for the investor to lose money. Not very likely.

So, to the extent that banks and investors have "seasoned" senior mortgage backed securities, they are just fine. Where they are losing money is on the recent vintage mortgages that they could not get off their books and into the hands of their clients in time as the asset backed market simply has ceased to function.

Looking at the graph suggests that because of the significant drop since the end of October there are further potentially large mark downs coming unless these indexes reverse themselves and go back up. Put another way, if the banks had to mark to market today, the losses they announced last week would be even higher. And potentially a lot higher.

Banks which have write downs and losses have to raise capital to meet net cap requirements. One of the ways you can do that is by making fewer loans. Thus banks are tightening up their lending standards.

But there is another reason that lending standards are higher. Many banks no longer function as what we think of as banks in the "old days" of 20 years ago. Today a bank uses its capital to make a number of loans and then packages them up and sells them as a security to another investor. Banks are now originators of loans rather than long term lenders.

But the institutions which are the ultimate market are demanding higher quality loans, and thus originators are responding to the market demand. So far, there is little new CDO issuance, and no subprime securities to speak of. But standards are going to get tighter for all sorts of paper. Capital One informed us today that credit card delinquencies are up over a full percentage point from this time last year to 4.75%. Do you think that investors will buy credit card paper at the same terms as last year? The market for credit card asset backed securities is almost $700 billion. Rates are going to go up, and credit will be harder to get for those with less than pristine credit.

There is a distinct lack of confidence in the ratings of asset backed securities of all types. We do not have a liquidity crisis. We have a confidence crisis. As we see capital implode and confidence erode, we are facing the real possibility of a full blown credit crunch.

(By the way, this is not just a US problem. You can bet similar problems are going to crop up in institutions all over Europe.)

King Dollar Faces the Guillotine

But there is yet another problem facing the credit markets and that is the erosion of the value of the US dollar. Some argue that a falling dollar is good for the US because it makes our exports cheaper, and indeed exports are rising. But there is more to the falling dollar than improving our exports.

Look at this chart provided me by South African partner Prieur du Plessis's Investment Postcards blog ( www.investmentpostcards.com ). It is what a European investor would have lost if they had invested in a ten year US treasury note, down an ugly 7% in a government bond after today's bond sell-off.

If you own the Dow, you are down more than 5% after today in terms of the euro. And that is pretty much the case for most currencies. It is why one prominent Chinese official suggested this week that China should start to put more of its assets in stronger currencies, touching off a very quick drop in the dollar. The euro and the pound are almost 5% higher than they were at the beginning of September when I was in Europe.

If you are a foreign investor, why would you want to invest in dollar denominated assets in which you are not totally confident? Sure, you can hedge your currency risk, but hedging is not without cost, and that cost will be born by the borrower which is to say American businesses and consumers.

Think about this for a moment. If you are China, you could reduce your energy bill by 20% just by letting your currency rise. Not to mention the cost of copper, steel, nickel and other commodities. And did I mention all the massive food imports China requires? Yes, keeping your currency low has helped you to get a competitive advantage in manufacturing all sorts of products. But at some point it will make more sense to have a stronger currency.

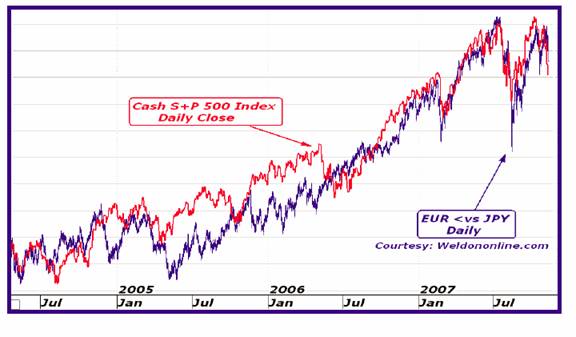

The Euro-Yen Cross Two quick notes before we close: Greg Weldon noted in Weldon's Money Monitor that came out tonight the very tight correlation between the US stock markets and what is known as the Euro-Yen cross, or the Euro as denominated in yen. ( www.weldononline.com )

This cross is a proxy for the yen carry trade. It is a clear example of the appetite in the world for risk. That appetite went away in August but came back in September and October. It is once again heading down, which does not bode well for the stock market if it continues.

The Consumer is Getting Tired Consumer sentiment is at a 15 year low, taking out the temporary spike down after Katrina. And it is showing up in consumer spending. Let's close with this note from friend Bill King (remove sharp objects from your vicinity).

"October US retail sales are at or near recession levels. Food inflation boosted warehouse sales. Wal-Mart sales increased 0.4% on heavy discounting; +1.1% was expected. WMT's sales are flat ex- Sam's Club (+4.2%, which is mostly from increased food sales) and are down 0.3% ex-gasoline. Nordstrom reports a decline of 2.4%; +1.3% was expected. Macy's sales declined 1.5%; -0.6% was expected. Gap same-store sales declined 8%; -4.7% was expected. Limited Brands (Victoria's Secret) reports same-store sales declined 6%; -1.5% was expected. Chico's sales declined 10.6%; -5.9% was expected. Abercrombie & Fitch same-store sales declined 2%; -0.6% was expected. Ann Taylor sales declined 4.2%; +1.2% was expected. Target same-store sales increased

4.1% (+2.4% exp). Costco same-store US sales jumped 7% (food).

"The National Retail Federation and TNS Retail both forecast the smallest holiday sales growth in five years. The NRF includes purchases in November and December in its forecast. TNS uses sales during October, November and December. The Int'l Council of Shopping Centers said October sales increased 1.6%, the worst October in 12 years.

"Bloomberg's Same-store Sales Index increased 1% in Oct; year-to-date sales are +1.5%. The only reason for being positive is the warehouse clubs index increased 5.3%. It's the food inflation, stupid!"

Jim Cramer used the "R" word on his show last night: recession. I think it is more likely than not. The Fed is going to cut and cut again. The dollar is going down some more. It is dangerous out there for relative return investing.

New York, Philadelphia, Switzerland and Phoenix I am off to New York tomorrow for a relaxing weekend with friends, and then on to Philadelphia to meet with Steve Blumenthal and friends at CMG, then an early flight home on Wednesday. I agreed this week to speak at a conference in Switzerland in April and another in Phoenix in January, more on those later. Looks like the travel schedule is going to heat back up. And my London partners are pressing me to go there and other parts of Europe in January.

We had a quiet and small birthday dinner for #2 daughter Melissa last Wednesday with just a few of her siblings. The family will gather next weekend for the "real" celebration. I see a Maverick's game in our future.

If it's good enough for Supermodel Giselle Bundchen, then maybe I should join. She is now demanding she be paid in any currency other than the dollar. I realized this week that I need to start pricing my speaking fees, at least in Europe, in euros. Like a lot of US assets, I realized that I am a bargain. Interestingly, my income from Europe went up 5% this quarter over last quarter just from currency appreciation. But then my expenses will rise even more.

Have a great week, and spend some time enjoying the fall (or spring if you are in the southern hemisphere) weather.

Your wishing for a stronger dollar analyst,

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2007 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.