The Seven Immutable Laws of Investing

InvestorEducation / Learning to Invest Mar 22, 2011 - 09:06 AM GMTBy: John_Mauldin

I am in London this morning, just a few miles (in theory) from the writer of this week's Outside the Box. James Montier, now with GMO, is one of my favorite analysts. I read everything he writes, and my only complaint is that he does not write enough. Today he offers us his thoughts on what he calls the "7 Immutable Laws of Investing."

I am in London this morning, just a few miles (in theory) from the writer of this week's Outside the Box. James Montier, now with GMO, is one of my favorite analysts. I read everything he writes, and my only complaint is that he does not write enough. Today he offers us his thoughts on what he calls the "7 Immutable Laws of Investing."

Co-hosting Squawk Box for two hours this morning with Geoff and Steve was fun. They took the time to have some thoughtful conversations on a wide variety of topics, as well as have some fun. Malta, Milan, and Zug/Zurich, and then back home. Book launch party in a few hours, so let's just jump into James's work.

Your wondering what time it is analyst,

John Mauldin, Editor

Outside the Box

The Seven Immutable Laws of Investing

James Montier

In my previous missive I concluded that investors should stay true to the principles that have always guided (and should always guide) sensible investment, but I left readers hanging as to what I believe those principles might actually be. So, now, for the moment of truth, I present a set of principles that together form what I call The Seven Immutable Laws of Investing.

They are as follows:

- Always insist on a margin of safety

- This time is never different

- Be patient and wait for the fat pitch

- Be contrarian

- Risk is the permanent loss of capital, never a number

- Be leery of leverage

- Never invest in something you don't understand

So let's briefly examine each of them, and highlight any areas where investors' current behavior violates one (or more) of the laws.

1. Always Insist on a Margin of Safety

Valuation is the closest thing to the law of gravity that we have in finance. It is the primary determinant of long-term returns. However, the objective of investment (in general) is not to buy at fair value, but to purchase with a margin of safety. This reflects that any estimate of fair value is just that: an estimate, not a precise figure, so the margin of safety provides a much-needed cushion against errors and misfortunes.

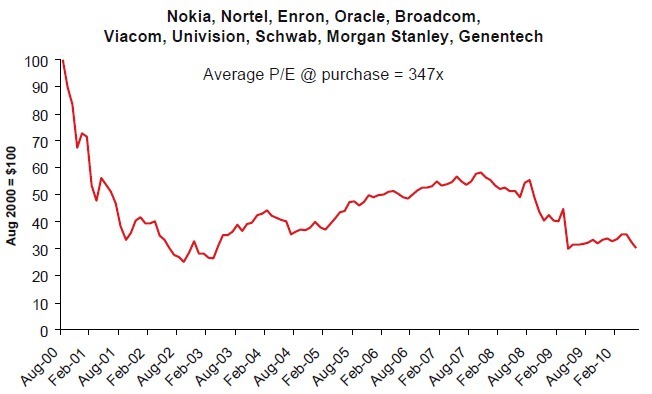

When investors violate Law 1 by investing with no margin of safety, they risk the prospect of the permanent impairment of capital. I've been waiting a decade to use Exhibit 1. It shows the performance of a $100 investment split equally among a list of stocks that Fortune Magazine put together in August 2000.

For the article, they used this lead: "Admit it, you still have nightmares about the ones that got away. The Microsofts, the Ciscos, the Intels. They're the top holdings in your ultimate 'coulda, woulda, shoulda' portfolio. Oh, what might have been, you tell yourself, had you ignored all the naysayers back in 1990 and plopped a modest $5,000 into, say, both Dell and EMC and then closed your eyes for the next ten years. That's $8.4 million you didn't make.

"Now, hold on a minute. This is no time for mea culpas. Okay, so you didn't buy the fastest growers of the past decade. Get over it. This is a new era - a new millennium, in fact - and the time for licking old wounds has passed. Indeed, the importance of stocks like Dell and EMC is no longer their potential as investments (which, though still lofty, is unlikely to compare with the previous decade's run). It's in their ability to teach us some valuable lessons about investing from here on out."

Rather than sticking with these "has been" stocks, Fortune put together a list of ten stocks that they described as "Ten Stocks to Last the Decade" - a buy and forget portfolio. Well, had you bought the portfolio, you almost certainly would wish that you could forget about it. The ten stocks were Nokia, Nortel, Enron, Oracle, Broadcom, Viacom, Univision, Schwab, Morgan Stanley, and Genentech. The average P/E at purchase for this basket was well into triple figures. If you had invested $100 in an equally weighted portfolio of these stocks, 10 years later you would have had just $30 left! That, dear reader, is the permanent impairment of capital, which can result when you invest with no margin of safety.

Exhibit 1: Fortune Magazine's Ten Stocks to Last the Decade

The securities identified above represent a selection of securities identified by GMO and are for informational purposes only. These specific securities are selected for presentation by GMO based on their underlying characteristics and are not selected solely on the basis of their investment performance. These securities are not necessarily representative of the securities purchased, sold or recommended for advisory clients, and it should not be assumed that the investment in the securities identified will be profitable. Source: Bloomberg, Datastream, GMO As of 6/30/10

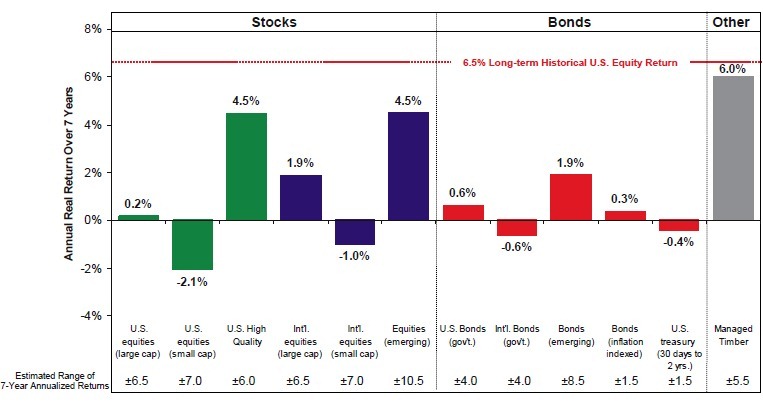

Today it appears that no asset class offers a margin of safety. Cast your eyes over GMO's current 7-Year Asset Class Forecast (Exhibit 2). On our data, nothing is even at fair value, so from an absolute perspective all asset classes are expensive! U.S. large cap equities are offering you a close to zero real return for the pleasure of parking your money in them. Small cap valuations indicate an even worse return. Even emerging market and high quality stocks don't look cheap on an absolute basis; they are simply the best relative places to hide.

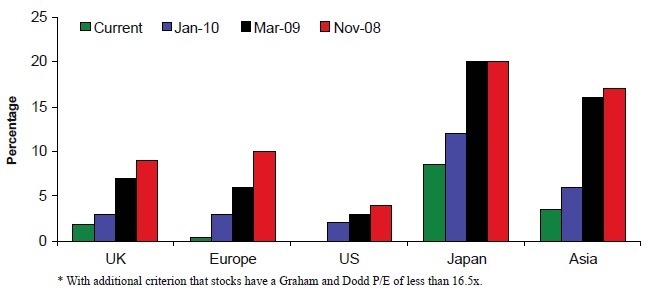

These projections are reinforced for equities when we investigate the number of stocks able to pass a deep value screen designed by Ben Graham. In order to pass this screen, stocks are required to have an earnings yield of twice the AAA bond yield, a dividend yield of at least two-thirds of the AAA bond yield, and total debt less then two-thirds of the tangible book value. I've added one extra criterion, which is that the stocks passing must have a Graham and Dodd P/E of less than 16.5x. As a cursory glance at Exhibit 3 reveals, there are very few deep value opportunities in global markets currently.

Bonds or cash often offer reasonable opportunities when equities look expensive but, thanks to the Fed's policy of manipulated asset prices, these look expensive too.

Exhibit 2: GMO 7-Year Asset Class Return Forecasts* as of January 31, 2011

* The chart represents real return forecasts1 for several asset classes. These forecasts are forward-looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Actual results may differ materially from the forecasts above. 1 Long-term inflation assumption: 2.5% per year. Source: GMO

Exhibit 3: % of Stocks Passing Graham's Deep Value Screen

* With additional criterion that stocks have a Graham and Dodd P/E of less than 16.5x. Source: GMO As of 3/29/10

In order to assess the margin of safety on bonds, we need a valuation framework. I've always thought that, in essence, bond valuation is a rather simple process (at least at one level). I generally view bonds as having three components: the real yield, expected inflation, and an inflation risk premium.

The real yield can either be measured in the market via inflation-linked bonds, or an estimate of equilibrium (or normal) real yield can be used. The TIPS market currently offers a real yield of 1% for 10-year paper. Rather than use this, I've chosen to impose a "normal" real yield of around 1.5%.

To gauge expected inflation we can use surveys. For instance, the First Quarter 2011 Survey of Professional Forecasters2 shows an expected inflation rate of just below 2.5% annually over the next decade. Other surveys show little variation.

The use of surveys of forecasts might seem a little at odds with my previously expressed disdain for forecasts. But because history has taught me that the economists will be wrong on their inflation estimates, I insist on including the final element of the bond valuation: the inflation (or term) risk premium. Estimates of this risk premium range, but I suggest it should be between 50-100 bps. Given the uncertainty surrounding the use and impact of quantitative easing, I would further suggest a figure closer to the upper range of that band currently.

Adding these inputs together gives a "fair value" of somewhere between 4.5-5%. The current 3.5% yield on U.S. 10- year bonds falls a long way short of offering investors even a minimal margin of safety.

Of course, the bond bulls and economic pessimists will retort that the market is just waking up to the impending reality that the U.S. is set to follow Japan's experience and spend a decade or two mired in a deflationary swamp. They may be correct, but we can assess the probability that the market is placing on this scenario.

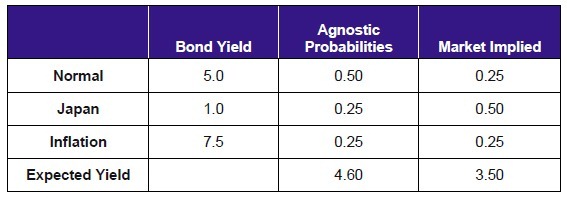

In constructing a simple scenario valuation, let's assume three possible states of the world (a gross simplification, but convenient). In the "normal" state of the world, bond yields sit close to their fair value at, say, 5%. Under a "Japanese" outcome, the yield would drop to 1%, and in a situation where the Fed loses control and inflation returns, yields rise to 7.5% (roughly speaking, a 5% inflation rate).

If we adopt an agnostic approach and say that we know nothing, then we could assign a 50% probability to the normal outcome, and 25% to each of the tails. This scenario would generate an expected yield of very close to 4.5%. We can tinker around with the probabilities in order to generate something close to the market's current pricing. In essence, this reveals that the market is implying a 50% probability that the U.S. turns into Japan.

This seems an extremely lopsided implied probability. There are certainly similarities between the U.S. and Japan (e.g., zombie banks), but there are marked differences as well (e.g., the speed and scale of policy response, demographics). A 50% probability seems excessively confident to me.

Exhibit 4: Bond Scenario Valuation

Source: GMO

Our concerns about the overvaluation of bonds have implications for both our portfolios and for relative valuation. Obviously, you won't find much fixed income exposure in our current asset allocation portfolios given the valuation case laid out above.

One of the "arguments" for owning equities that we regularly encounter is the idea that one should hold equities because bonds are so unattractive. I've described this as the ugly stepsisters' problem because it is akin to being presented with two ugly stepsisters and being forced to date one of them. Not a choice many would relish. Personally, I'd rather wait for Cinderella to come along.

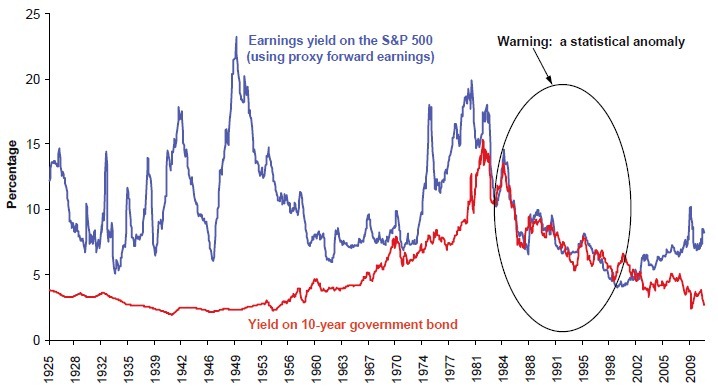

Of course, the argument to buy stocks because bonds are appalling is really just a version of the so-called Fed Model. This approach is flawed at just about every turn. It fails at the level of theoretical soundness as it compares real assets with nominal assets. It fails empirically as it simply doesn't work when attempting to predict long-run returns (never an appealing trait in a model). Moreover, proponents of the Fed Model often fail to remember that a relative valuation approach is a spread position. That is to say that if the Model says equities are cheap relative to bonds, it doesn't imply that one should buy equities outright, but rather that one should short bonds and go long equities. So the Model could well be saying that bonds are expensive rather than that equities are cheap! The Fed Model doesn't work and should remain on the ash heap.

Exhibit 5: What Relationship Between Bonds and Equities?

Source: GMO As of 1/12/11

Relative valuation holds little appeal to me and even less so when I consider that neither bonds nor equities are even vaguely stable assets. In general, when valuing an asset you want a stable anchor by which to assess the scale of the investment opportunities. For instance, one of the reasons that the Graham and Dodd P/E (current price over 10-year average earnings) works well as a valuation indicator is the slow, stable growth of 10-year earnings. In contrast, the bond market was happy to extrapolate the briefest peak of inflation to over 30 years in the early 1980s, and similarly was willing to extrapolate the deflationary risks of 2009 for over 10 years. Using such an unstable asset as the basis of any valuation seems foolhardy.

I'd rather consider the absolute merits of each investment independently. Unfortunately, as noted above, this currently reveals an unpleasant truth: nothing offers a good margin of safety.

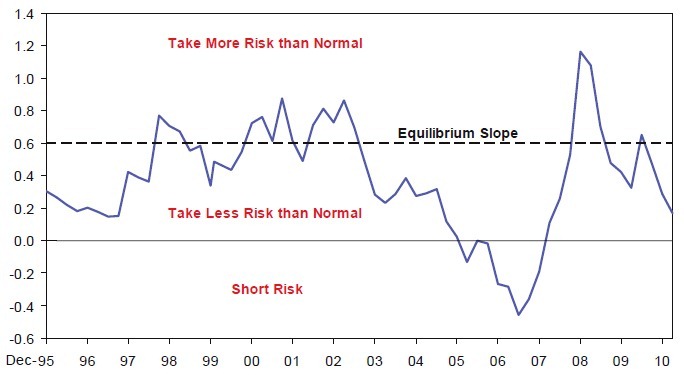

In fact, if we look at the slope of the risk return line (i.e., the 7-year forecasts measured against their volatility), we can see that investors are being paid a paltry return for taking on risk. Admittedly, Mr. Market is not yet as manic as he was in 2007 when we faced an inverted risk return trade-off - investors were willing to pay for the pleasure of holding risk - but at this rate, I believe it won't be long before we are once again facing such a perverse situation. Albeit this time it is officially-sponsored madness!

Exhibit 6: The Slope of the Risk Return Line

Source: GMO As of February 2011

This dearth of assets offering a margin of safety raises a conundrum for the asset allocation professional: what does one do in a world where nothing is cheap? Personally, I'd seek to raise cash. This is obvious not for its thoroughly uninspiring near-zero yield, but because it acts as dry powder - a store of value to deploy when the opportunity set offered by Mr. Market once again becomes more appealing. And this is likely, as long as the emotional pendulum of investors oscillates between the depths of despair and irrational exuberance as it always has done. Of course, the timing of these swings remains as nebulous as ever.

2. This Time Is Never Different

Sir John Templeton defined "this time is different" as the four most dangerous words in investment. Whenever you hear talk of a new era, you should behave as Circe instructed Ulysses to when he and his crew approached the Sirens: have a friend tie you to a mast.

Because I have discussed the latest notion of a new era in my recent "In Defense of the 'Old Always,'" I won't dwell on it here. I will point out, though, that when assessing the "this time is different" story, it is important to take the widest perspective possible. For instance, if one had looked at the last 30 years, one would have concluded that house prices had never fallen in the U.S. However, a wider perspective, drawing on both the long-run data for the U.S. and the experience of other markets where house prices had soared relative to income, would have revealed that the U.S. wasn't any different from the rest of the world, and that a house price fall was a serious risk.

3. Be Patient and Wait for the Fat Pitch

Patience is integral to any value-based approach on many levels. As Ben Graham wrote, "Undervaluations caused by neglect or prejudice may persist for an inconveniently long time, and the same applies to inflated prices caused by over-enthusiasm or artificial stimulants." (And there can be little doubt that Mr. Market's love affair with equities is based on anything other than artificial stimulants!)

However, patience is in rare supply. As Keynes noted long ago, "Compared with their predecessors, modern investors concentrate too much on annual, quarterly, or even monthly valuations of what they hold, and on capital appreciation... and too little on immediate yield ... and intrinsic worth." If we replace Keynes's "quarterly" and "monthly" with "daily" and "minute-by-minute," then we have today's world.

Patience is also required when investors are faced with an unappealing opportunity set. Many investors seem to suffer from an "action bias" - a desire to do something. However, when there is nothing to do, the best plan is usually to do nothing. Stand at the plate and wait for the fat pitch.

4. Be Contrarian

Keynes also said that "The central principle of investment is to go contrary to the general opinion, on the grounds that if everyone agreed about its merit, the investment is inevitably too dear and therefore unattractive."

Adhering to a value approach will tend to lead you to be a contrarian naturally, as you will be buying when others are selling and assets are cheap, and selling when others are buying and assets are expensive.

Humans are prone to herd because it is always warmer and safer in the middle of the herd. Indeed, our brains are wired to make us social animals. We feel the pain of social exclusion in the same parts of the brain where we feel real physical pain. So being a contrarian is a little bit like having your arm broken on a regular basis.

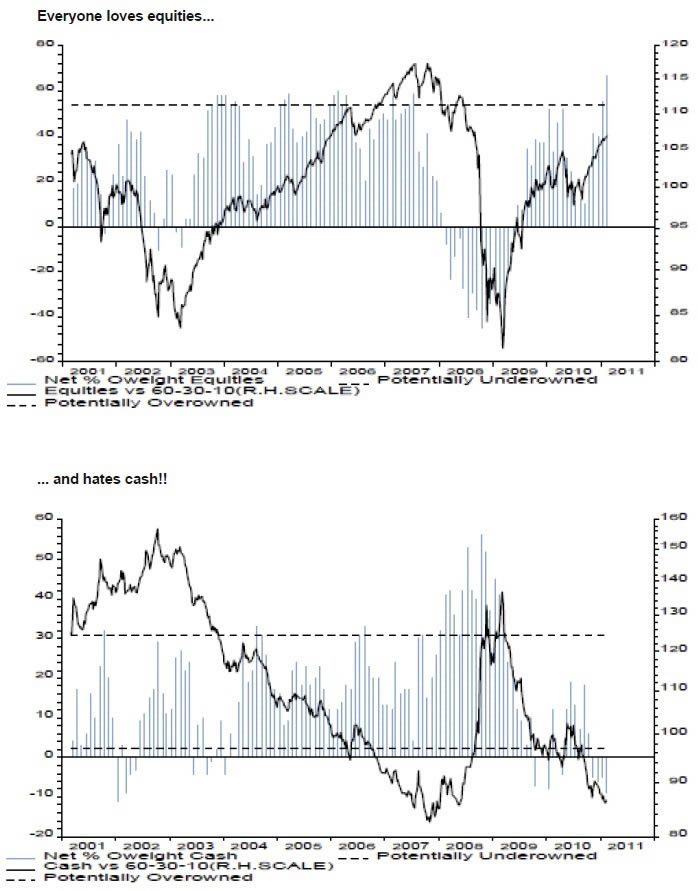

Currently, there is an overwhelming consensus in favor of equities and against cash (see Exhibit 7). Perhaps this is just a "rational" response to Fed policies that actively encourage gross speculation.

William McChesney Martin, Jr. observed long ago that it is usually the central bank's role to "take away the punch bowl just when the party starts getting interesting." The actions of today's Fed are surely more akin to spiking the punch and encouraging investors to view the markets through beer goggles. I can't believe that valuation-indifferent speculation will end in anything but tears and a massive hangover for those who insist on returning again and again to the punch bowl.

5. Risk Is the Permanent Loss of Capital, Never a Number

I have written on this subject many times.4 In essence, and regrettably, the obsession with the quantification of risk (beta, standard deviation, VaR) has replaced a more fundamental, intuitive, and important approach to the subject. Risk clearly isn't a number. It is a multifaceted concept, and it is foolhardy to try to reduce it to a single figure.

To my mind, the permanent impairment of capital can arise from three sources: 1) valuation risk - you pay too much for an asset; 2) fundamental risk - there are underlying problems with the asset that you are buying (aka value traps); and 3) financing risk - leverage.

By concentrating on these aspects of risk, I suspect that investors would be considerably better served in avoiding the permanent impairment of their capital.

6. Be Leery of Leverage

Leverage is a dangerous beast. It can't ever turn a bad investment good, but it can turn a good investment bad. Simply piling leverage onto an investment with a small return doesn't transform it into a good idea. Leverage has a darker side from a value perspective as well: it has the potential to turn a good investment into a bad one! Leverage can limit your staying power and transform a temporary impairment (i.e., price volatility) into a permanent impairment of capital.

Exhibit 7: BoAML Fund Manager Survey (Equities and Cash)

While on the subject of leverage, I should note the way in which so-called financial innovation is more often than not just thinly veiled leverage. As J.K. Galbraith put it, "The world of finance hails the invention of the wheel over and over again, often in a slightly more unstable version." Anyone with familiarity of the junk bond debacle of the late 80s/early 90s couldn't have helped but see the striking parallels with the mortgage alchemy of recent years! Whenever you see a financial product or strategy with its foundations in leverage, your first reaction should be skepticism, not delight.

7. Never Invest in Something You Don't Understand

This seems to be just good old, plain common sense. If something seems too good to be true, it probably is. The financial industry has perfected the art of turning the simple into the complex, and in doing so managed to extract fees for itself! If you can't see through the investment concept and get to the heart of the process, then you probably shouldn't be investing in it.

Conclusion

I hope these seven immutable laws help you to avoid some of the worst mistakes, which, when made, tend to lead investors down the path of the permanent impairment of capital. Right now, I believe the laws argue for caution: the absence of attractively priced assets with good margins of safety should lead investors to raise cash. However, currently it appears as if investors are following Chuck Prince's game plan that "as long as the music is playing, you've got to get up and dance."

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2011 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.