What Happens When We Come to the End of QE2?

Interest-Rates / Quantitative Easing Mar 20, 2011 - 10:42 AM GMTBy: John_Mauldin

What happens when the Fed is finished with QE2? I have been letting that filter into my thinking lately as I look at the economic landscape and the data we have seen the past few weeks. Correlation is not causation, as I often say, but all we can do is look back at what happened last time and speculate about the future. A very dangerous occupation, but your fearless analyst will plunge on ahead into the jungle of a very hazy future. You come with me at your own risk!

What happens when the Fed is finished with QE2? I have been letting that filter into my thinking lately as I look at the economic landscape and the data we have seen the past few weeks. Correlation is not causation, as I often say, but all we can do is look back at what happened last time and speculate about the future. A very dangerous occupation, but your fearless analyst will plunge on ahead into the jungle of a very hazy future. You come with me at your own risk!

New York Times Bestseller

Quickly, a big Mauldin thanks to those who already bought my book, Endgame, as it made the New York Times bestseller list yesterday, earlier than I thought it would. That would be my 4th, and that and my kids are about my only small claims to fame. I have ruthlessly promoted the book to you, and so this week I resist my inner promotional demon and simply provide a link to http://www.amazon.com/... where you can read the reviews and buy the book if you have not, or get it in your local stores. At the end of the letter, I note that I will be at a book launch party in London Monday evening, and would love to have you stop by. Details below. And now to this week's letter.

The End of QE2?

The Fed committed to buying $600 billion of Treasuries between the beginning of QE2 in November and the end of June. June is 3 months away. What will happen when that buying goes away? The hope when QE2 kicked off was that it would be enough to get the economy rolling, so that further stimulus would not be deemed necessary. We'll survey how that is working out, with a quick look at some recent data, and then we go back and see what happened the last time the Fed stopped quantitative easing.

First, the guy on the street is getting squeezed. Real US consumer spending slowed in January and looks like it did only marginally better in February. The Fed argues that inflation is mild, as they prefer to look at "core" inflation (inflation without considering food and energy). If you look at it that way, they are right. And in normal times, I can kind of see why we strip out energy and food, as they are very volatile price points and can move a lot from month to month.

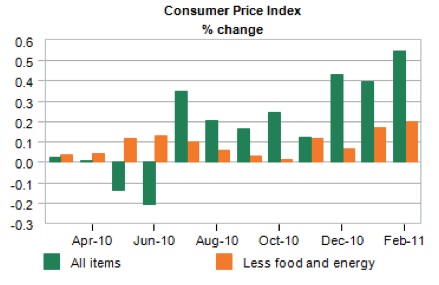

But that argument gets a lot weaker when your main policy, that of significant quantitative easing, is perhaps CAUSING the rise in food and energy (as well as weakening the dollar)! If the Fed policy is at least contributing to the cause of total inflation, arguing that food and energy don't count doesn't hold water. Let's look at the following chart from economy.com.

In particular, notice the rise in the last three months since the beginning of QE2. Inflation is running at over 5% on an annualized basis. Companies like Kimberly (diapers, etc.), Colgate, P&G, and others all announced 5-7% price increases this week. These are companies that provide staples we all buy. Those prices matter. Even Wal-Mart will have to pass those increases on. To say that food and energy don't matter misses the point. These items have real economic impact.

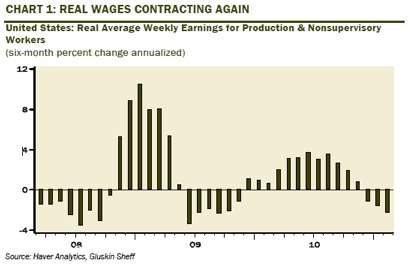

As my friend David Rosenberg wrote this morning:

"In February, there was no inflation at all in average weekly wage-based earnings but there was 0.5% inflation in consumer prices, meaning that real work-related income was crushed 0.5% and has now deflated in each of the past four months and in five of the past six months, during which it has contracted at a 2.3% annual rate. Once the effects of fiscal stimuli wear off, this negative income trend will show through in a much more visible slowing in real consumer spending that we doubt the markets have fully discounted. So far, what has happened in equities has been treated as a financial event - just wait until the economic event follows suit. And it's not only fiscal stimulus that is soon to subside. We still have that 86% correlation over the past two years between movements in the Fed balance sheet and the direction of the S&P 500 - this too will come home to roost before long, whether or not we end up seeing a resolution to the crises in Japan, Libya or Bahrain."

He goes on to give us this chart:

How's that QE2 thingy working for you, Mr./Ms. Average Worker? Prices up, income down? And remember, most workers got the equivalent of a 2% pay hike with the temporary boost in Social Security, which goes away at the end of the year (and without which the economy and consumer spending would be even worse!).

Maybe that's why New York Fed Chief William Dudley got heckled this week. (Courtesy of the Agora 5 Minute Forecast:)

"Dudley - a 21-year vet of Goldman Sachs - stepped out of his bubble to explain Fed policy to real people in Queens.

"It might not have been the first time Dudley attempted to gain the trust of the hoi polloi, but we're pretty sure it'll be the last. The details here were reported widely. We divined the scene from a Reuters report.

"First Dudley swore up and down that inflation was no problem. 'When was the last time, sir,' came a reply from the audience, 'that you went grocery shopping?'"

"Dudley boldly proceeded to explain the concept of 'core CPI' - the cost-of-living measure designed for people who don't eat or consume energy. Heh, we know firsthand how well that goes over...

"Then in a brilliant stroke, he pointed to Apple's shiny new iPad 2 to illustrate his point. 'Today you can buy an iPad 2 that costs the same as an iPad 1 that is twice as powerful,' he gamely explained. 'You have to look at the prices of all things.'

"'I can't eat an iPad,' someone yelled from the crowd."

Ouch. (For the record, I do go to the grocery store and Wal-Mart and Home Depot, as well as other less frugal venues.)

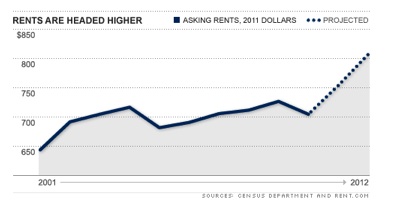

And core inflation may soon be under pressure. There were two articles yesterday, one from Yahoo and the other on Bloomberg. Both related to rising pressure on rental costs. (My recent lease renewal increase was significantly above core CPI!) (From http://realestate.yahoo.com/promo/rents-could-rise-10-in-some-cities.html)

"Already, rental vacancy rates have dipped below the 10% mark, where they had been lodged for most of the past three years. 'The demand for rental housing has already started to increase,' said Peggy Alford, president of Rent.com... By 2012, she predicts the vacancy rate will hover at a mere 5%. And with fewer units on the market, prices will explode."

Look at this graph showing their projections:

Here's what to pay attention to. Notice that since 2002 (or thereabouts) rental costs have been flat, and down of late (inflation-adjusted). If Rent.com projections are anywhere close, we could see a rise in rents of 15% by the end of 2012.

Let's remember that 23% of the CPI and 40% of core CPI is Owner Equivalent Rent. If they are right, that adds about 3% to total CPI and 6% to core CPI! Will the Fed be telling us to focus on core inflation in 12-18 months? And those prices will start to show up steadily.

"This is a sharp change from the recession, when many Americans couldn't afford to live on their own. More than 1.2 million young adults moved back in with their parents from 2005 to 2010, said Lesley Deutch of John Burns Real Estate Consulting. Many others doubled up together.

"As a result, landlords had to reduce prices and offer big incentives to snag renters. Now that the recession is easing, many of these young people are ready to find new digs, mostly as renters, not owners. Plus, the foreclosure crisis continues unabated, and the millions losing their homes are looking for new places to live."

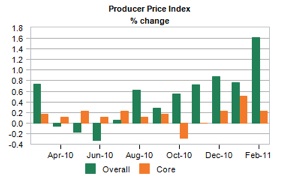

Producer Prices Up 35-40% in the Last Six Months

Then let's look at business. The Producer Price Index was out this week, and it was way up - 1.6% for the month, or an annualized 20%+. Even if you look at the last year, it was up a real 5.8%. That is inflation in the pipeline. Look at this chart from economy.com. Notice the trend since QE2 was announced in August and implemented in November.

I won't bore you with the details, but for those interested, go to www.bloomberg.com and search for "Japan supply issues" and further on "semiconductors." It is clear that, at least for a while, prices of electronics and tools are going to rise as one company after another is shutting its production lines down in Japan. Auto manufacturing plants in the US will have to close soon, as critical parts from Japan are not going to be forthcoming. Flat screen TVs? The iPad 2 I keep trying to find? All sorts of companies are going to get their costs squeezed even further. Remember, the above PPI numbers are from before the Japanese earthquake and tsunami and nuclear disaster.

(I was in Tokyo less than two weeks ago. I can't imagine the stress and anguish going on there. The scope of the disaster is just shattering. I encourage my readers to go to http://american.redcross.org and donate directly to their Japanese fund or the charity of your choice.

A few details from Japan, though, gleaned from here and there. Sony alone makes 10% of the world's laptop batteries. Japan is responsible for 30% of global flash memory, 20% of semi-conductors, and 40% of electronic components.

The point is that the Fed has created real pressure in the price pipeline, primarily on basic commodities and energy. "Crude" goods, which is basically materials before there is any value added, are up 28% from a year ago and pushing an annualized 35-40% for the last six months. Those costs are filtering in to final finished products. And when you add in the supply-related problems from the recent disaster? It is not a pretty picture for profits.

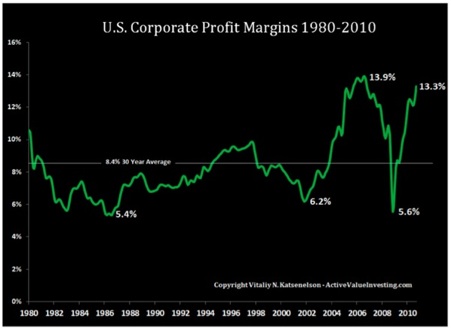

Let's go back and look at a graph from friend Vitaliy Katsenelson, from a few weeks ago. It points out that corporate profits are back close to all-time highs as a percentage of GDP.

As the brilliant Jeremy Grantham says, and I am paraphrasing, corporate profits are among the most mean-reverting of all statistics. And this makes sense unless capitalism is broke. High profits entice competitors to come in and take market share by selling for less.

If corporate profits went back (mean-reverted) to their longer-term average, P/E ratios would be close to 24 at today's prices. Corporations have some room to absorb some price increases, but at the expense of the bottom line.

What Happens When We Come to the End of QE2?

We have only one instance where the Fed cut back on quantitative easing, and that was last year. It is a data set of one, but it is all we have. So, let's look at what happened. As noted by several sources (but I am looking at Rosie's list right now), the Fed let its balance sheet contract by some 12% from late April to late August. Quoting:

"Now over that interval ... "The S&P 500 sagged from 1,217 to 1,064.... The S&P 600 small caps fell from 394 to 330.... The best performing equity sectors were telecom services, utilities, consumer staples, and health care. In other words -- the defensives. The worst performers were financials, tech, energy, and consumer discretionary.... Baa spreads widened +56bps from 237bps to 296bps... CRB futures dropped from 279 to 267.... Oil went from $84.30 a barrel to $75.20.... The VIX index jumped from 16.6 to 24.5.... The trade-weighted dollar index (major currencies) firmed to 76.5 from 75.5.... Gold was the commodity that bucked the trend as it acted as a refuge at a time of intensifying economic and financial uncertainty -- to $1,235 an ounce from $1,140 and even with a more stable-to-strong U.S. dollar too.... The yield on the 10-year U.S. Treasury note plunged to 2.66% from 3.84%..."

What will happen this time around? Is the economy strong enough to grow on its own without stimulus, or strong enough that the Fed will be reluctant to continue with QE3? My friends at Macroeconomic Advisors have reduced their first-quarter GDP projection to 2.5%. Morgan Stanley has dropped theirs from 4.5% less than six weeks ago to 2.9% today. That is a huge drop in a short time for a forecasting model. Forecasts at other economic shops are being slashed as well. States and local governments, as I have continuously noted, are cutting more than 1% of GDP from their budgets as I write. That translates into real-world pressure on the GDP (even if it'stemporary, which I believe it to be, we live in the present).

I am not ready to use the "R" word, but Muddle Through could show up with a true vengeance this summer, with higher inflation and slower growth. I lived through the '70s, and frankly, I would just as soon not go see that movie again.

The danger here is that the Fed (Bernanke) watches the economy slow and decides we need another round of quantitative easing. I have resisted that idea but, as I have noted, sometimes we need to think about the unthinkable.

And thus, I come to the end of the letter with a brief note on a very worrisome conversation I had yesterday with Martin Barnes, editor of the esteemed Bank Credit Analyst. Martin is one of the people I call when I want to know what the Fed might do. I guess I was looking for assurance that the Fed would not do QE3. I did not get it.

"Look, John" (insert Scottish brogue as I paraphrase), "if the Fed sees the economy rolling over into recession they will put their mandate for employment ahead of their mandate for stable prices."

"But that would mean higher inflation in the face of a slow economy."

"And?" he shot back. "That would just be the price of trying to increase employment, in their minds."

"But at some point you have to bring out your inner Volker!" I intoned. "What about the future?"

The conversation continued, but I never got my warm and fuzzy assurances. For the record, another round of QE, unless there is a true liquidity crisis (and the last QE did not qualify!), would be a disaster, at least from the cheap seats where I sit. There are all sorts of inflationary and stagflationary consequences, none of which I like.

Brief plug: This April, at my Strategic Investment Conference, the first two questions that each speaker will get at the end of their presentation will be, first, "What will happen when QE2 goes away?" and second, "Under what conditions will the Fed launch QE3?"

I will pose them to Martin Barnes, Marc Faber, Niall Ferguson, Louis-Vincent Gave, Paul McCulley, David Rosenberg, and Gary Shilling - and John Paulson has agreed to speak as well! They will be joined by Neil Howe (The Fourth Turning, and demographics guru) and George Friedman of Stratfor, as well as your humble analyst and Altegris partner Jon Sundt. I mean, really, is there a conference anywhere this year that has a line-up that powerful?

The conference is April 28-30 in La Jolla. It is filling up fast. You can register at https://hedge-fund-conference.com/2011/invitation.aspx?ref=mauldin. Sadly, it is for accredited investors only, but I will report back to you the answers from the speakers to those questions.

London, Malta, Milan, Zurich, Salt Lake, and New York

I am off to London tomorrow. I will be guest hosting Squawk Box on CNBC London at 7 AM (gasp!), then do various meetings, and that night will be with co-author Jonathan Tepper for our book-launch party at the Mint Hotels - Tower of London Hotel, 7 Pepys Street, City of London. If you can, RSVP to endgame@variantperception.com so we can have some idea of how many are coming. I know, last minute and all, but that's my life!

The next day I fly to Malta for board meetings, then on to Milan for a public presentation, then on to Zug and Zurich, before heading back. The next weekend I am off to Salt Lake for CMG partner Steve Blumenthal's 50th birthday bash, then to NYC on Sunday for three days of media and meetings. I will update you with the media schedule next Friday, but right now I know I am on Fast Money for the first time on Monday the 4th. That should be interesting. I am a little slower than those guys, but maybe they can slow down for the old man.

The Japanese disaster has gotten to me more than most similar tragedies. Maybe it is because I was there less than a week before the earthquake. Maybe it is the thought of all those elderly people who have lost everything, with no place to go back to, and enduring horrible weather conditions. I have had letters from readers who have friends there, and the stories they relate show a nation that has energy problems, with gas rationing, and that means that trucks have a hard time delivering food. Empty shelves are the norm, and reports of people running out of food keep coming to me.

For whatever reason, it has me thinking about how fragile life is, how short our time is, and how I need to focus on the important things, like family and friends. I do enjoy the business and my work (maybe too much!), but I need to make sure there is balance, as do we all.

The Japanese are a resilient people and will rebound, but they could use our help. Again, think about giving to the Red Cross or your own favorite charity. And let's pray that they can figure this nuclear thing out soon.

Your getting on yet another airplane analyst,

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2011 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.