Deconstructing Meredith Whitney’s Municpal Bond Default Predictions

Politics / Mainstream Media Mar 19, 2011 - 11:17 AM GMTBy: Mike_Stathis

The Article Whitney Doesn’t Want You to Read - If I hired a full-time staff of 100 financial professionals specifically dedicated to the task of calling out all of the media’s so-called financial experts (largely comprised of lifelong snake oil salesmen and Wall Street hacks), pointing to their miserable track records, while setting the record straight on their exaggerations, drama-filled statements, bias, agendas, cheerleading and apocalyptic predictions, we would be unable to address even one-tenth of the propaganda that continues to invade the minds of Americans.

The Article Whitney Doesn’t Want You to Read - If I hired a full-time staff of 100 financial professionals specifically dedicated to the task of calling out all of the media’s so-called financial experts (largely comprised of lifelong snake oil salesmen and Wall Street hacks), pointing to their miserable track records, while setting the record straight on their exaggerations, drama-filled statements, bias, agendas, cheerleading and apocalyptic predictions, we would be unable to address even one-tenth of the propaganda that continues to invade the minds of Americans.

This speaks volumes about the level of deceit and misinformation propagated by all forms of media. It also says much about the lack of attempts by those who understand what is truly going on to set the record straight.

Working with limited time, I try to address those myths that affect the most people. And I do this without bias or agendas. This brings me to my latest myth buster report. A few months ago, the largely useless television show (disguised as a news program) 60 Minutes interviewed Meredith Whitney, a former Oppenheimer banking analyst to discuss her wild claims regarding a wave of municipal defaults expected across the U.S. in 2011.

Before I get into the details about Whitney, her predictions, her track record, her motives, and everything else you should know about the women embraced by America’s criminal financial media, I think it’s best to give you an overview of the municipal bond market.

As many of you know, municipal bonds are issued to fund a wide range of projects, from roads, bridges, airports and schools, to parks, libraries, sports stadiums, public works and many other facilities.

The structure of these bonds differs as do the risks. Some municipal bonds are extremely safe, while others are vulnerable to quite a bit more risk. Overall, municipal bonds have historically been viewed as one of the safest investments outside of U.S. Treasury securities. The well-deserved reputation of municipal bonds is backed by default rates that are significantly lower than the highest-rated corporate debt.

For instance, the average five-year cumulative default rate for investment-grade munis is less than 0.5%, which is one-third the default rate of similar rated corporate debt. As a result of their low default rate, nice coupons and exemption from federal income taxes, mutual funds and individual investors comprise up to 80% of invested assets in these bonds. Thus, the media can have a huge impact on municipal bond prices.

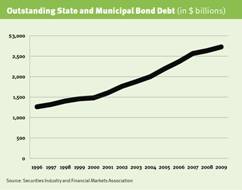

As you might imagine, the municipal bond market has grown by leaps and bounds over the past several years. Over the past decade, the market soared from $1.5 trillion to just over $2.8 trillion. Surely, with so much growth over this short time frame you are going to run into some debt that never should have been issued. That’s a given. But “50-100 sizable defaults totaling hundreds of billions of dollars in 2011,” as predicted by Whitney is absolutely a ridiculous scenario, even given the current state of the economy.

Despite their historically low default rate, there is no doubt that municipal defaults are on the rise. This trend is unlikely to subside anytime soon. In 2010, there were 183 defaults totaling losses of $6.4 billion. In 2009 there were only 31 defaults totaling $348 million (this data varies depending on the source and classification of default). Thus, as you can see defaults have soared. However, many of these defaults were not unexpected as they were tied to risky development projects in states hit hard by the housing correction, such as Florida and California.

What is the real source of these and other potential defaults?

Are they due to a collapse in state and local government revenues?

Well, kinda, sorta, but not really.

A collapse in government revenues would imply a collapse in sales and property tax revenues, licenses, fees and other income. While these revenues have certainly declined, they have not accounted for a significant share of the decline in total government revenues.

Due to the real estate-led financial crisis and resulting economic collapse, total state government revenue dropped from $1.6 trillion to $1.1 trillion between 2008 and 2009; a decline of more than 30 percent.

That sounds pretty bad, right?

However, the lion’s share of this drop was due to the collapse in social insurance trust revenue. In contrast, general revenues declined by a mere 1.4%.

How did insurance trust revenues fall by so much? I’ll give you two hints.

Look at the performance of the stock market between 2008 and 2009.

Now have a look at interest rates.

The insurance trust includes public employee retirement, unemployment compensation, workers compensation, and other insurance trusts. It’s somewhat similar to the federal insurance trust which includes Social Security and Medicare. To fund these benefit plans, you need two things; reasonable interest rates and a relatively healthy stock market. While the stock market has mounted a huge recovery since the March 2009 lows, it’s still about 20% below the October 2007 highs of around 14,200.

More important, interest rates have been artificially held down to near 0 percent in order to strengthen the balance sheets of the banking cartel. As I have mentioned in the past, this is the banking bailout no one in the media is talking about. Not only is this bailout destroying personal savings, it’s also adding to pension deficits and causing excessive inflation in emerging economies.

An extended duration of low interest rates is hits pensions hard because a good deal of the assets must generate a certain amount of monthly income in order to pay beneficiaries. And since the stock market has not fully recovered, some pension funds have been required to sell securities positions at lower prices in order to generate needed income.

As discussed in America’s Financial Apocalypse, the entire (private and public) public pension system was already underfunded prior to the financial crisis. In fact, the much larger public pension system was more underfunded than the private system. Both pension systems were still licking their wounds from the dotcom collapse even after Washington made radical changes to funding requirements. But additional factors have added to public pension deficits; demographics, inaccurate actuarial accounting estimates, and massive healthcare inflation.

The table below shows the balance sheet for the state of New York. Notice the huge deficit in the insurance trust revenue category. Next, notice the total cash and securities holdings versus the year-end debt. Finally, notice the interest on the general debt. This gives you a rough example of the situation seen in states, cities and counties across the nation.

The point? The interest on the debt is so small from a relative sense that defaulting on payments would do little to remedy the fiscal problems.

2010 State of New York Balance Sheet

Pointing to a collapse from insurance trust revenues as the main source of declining government revenues may not seem to paint a brighter picture of the economy now that state and local governments are trying to cut pensions and slash other costs. However, the decline in revenues from this category points to a demographic and stock market problem (in addition to artificially suppressed interest rates) as opposed to a complete shutdown of general revenues, which once again declined by a mere 1.4%.

What does all of this mean?

Despite what you may have heard from all of the snake oil salesmen who make their living preaching doom throughout their lives, the fact is that the economic engine in the U.S., while damaged, is not broken. Granted, the fundamental problems – healthcare and trade policy - remain as the largest long-term risks to the U.S. economy. But the point is that the drop off in total government revenues is largely due to stock market losses, poor planning and mismanagement of pension benefits.

By no means am I trying to downplay the state and local pension deficit issue. It is a problem of enormous magnitude. In fact, five years ago before few realized the U.S. even had a pension mess, I detailed the underfunded pension problem and forecast it to become a huge crisis in America’s Financial Apocalypse.

The point is that we need to distinguish the source of the budget shortfalls in order to accurately assess the risk of local government defaults.

With that overview, I’d like to get back to Meredith Whitney’s December 19th, 2010 appearance on 60 Minutes. It was the third-most watched show of the week, reaching nearly 13 million viewers. So you can imagine the effect it had on municipal bond investors.

First, let’s take a look how the interviewer, Steve Kroft introduces Whitney. Remember, the media always plays up its “experts,” exaggerating and even lying about their track record. This serves to add perceived credibility to the story.

“One of the most respected financial analysts on Wall Street.” – NOT TRUE

“One of the most influential women in American business.” – A PIPE DREAM

“She made a reputation by warning that the big banks were in big trouble long before the 2008 collapse.” – Notice the vague wording, meant to imply that she predicted the financial crisis, which is NOT TRUE.

Steve Kroft, you are a liar and a bum. This is precisely why you work in the media.

Now let’s get to Whitney’s punch line.

Whitney: There’s not a doubt in my mind that you will see a spate of municipal-bond defaults.

Kroft: How many is a spate?

Whitney: You could see 50 sizable defaults, 50 to 100 sizable defaults, more. This will amount to hundreds of billions of dollars' worth of defaults.

http://www.cbsnews.com/video/watch/?id=7166293n&tag=related;photovideo

Once again, all of this is supposed to happen this year.

You could also see castles in the sky if you smoke enough dope.

Let me begin by responding to Whitney’s claims. You won’t see hundreds of billions of dollars worth of defaults this year, next year, over the next five years, or over the next ten years; not in the U.S. anyway.

To give you an idea just how ridiculous Whitney’s claims are, in order to total around $200 billion dollars in defaults, the following cities would need to default on all of their debt:

New York City, Los Angeles, Chicago, Houston, Phoenix, Philadelphia, San Antonio, San Diego, Dallas, San Jose, Detroit, San Francisco, Jacksonville, Indianapolis, Austin, Columbus, Fort Worth, Charlotte, Memphis, Boston, Baltimore, El Paso, Seattle, Denver and Nashville – the 25 largest cities in the U.S.

AND we would also need to see the 25 largest counties default (in addition to the 25 largest U.S. cities) to encounter the level of defaults touted by Whitney.

This simply isn’t going to happen; not in 2011, not by 2012 and not by 2020.

The 60 Minutes segment claims Whitney and her colleagues spent “two years and thousands of man hours” researching the fiscal condition of the 15 largest states, as if this is supposed to add credibility to her prediction.

I don’t care if Whitney and her mental midgets spent 50 years and tens of thousands of “man hours” researching. At the end of the day, all it takes is one person who knows what they are doing; a person who has a good understanding of the big picture; a person who has good judgment. That person is NOT Meredith Whitney.

A few days before the 60 Minutes interview aired, Whitney appeared in a video interview with the Financial Times. She said defaults would spark “panic in the muni markets.”

Two days later, Whitney made an appearance on CNBC (December 21, 2010). She warned about indiscriminate selling. “It’s going to look like Europe in terms of when programs are cut.” Then she used the phrase “social unrest” twice.

Social unrest is what we have seen in the Middle East. At best, you’re going to see some really pissed off people in the U.S. in years to come, but you aren’t going to see much social unrest, although social unrest in the U.S. would actually help led to positive change.

Industry Experts React

Shortly after the 60 Minutes interview, industry professionals put Whitney in her place.

California Treasurer Bill Lockyer called the prediction “apocalyptic arm-waving.”

The National League of Cities' research director cited her “stunning lack of understanding.”

Thomas G. Doe, chief executive officer of Municipal Market Advisors said, “She's trying to shock the market into a panic mode. Nothing makes sense.”

Sound familiar?

Do the predictions of a worthless U.S. dollar, hyperinflation and $15,000/ounce gold preached by Peter Schiff, Nouriel Roubini, Marc Faber and others ring a bell?

Pacific Investment Management Co.'s Bill Gross was more diplomatic when responding publically to Whitney’s claims (as you might expect from a member of the media club, when criticizing one of his fellow media club members). Gross simply said he doesn't subscribe to the “theory.”

David Kotok, chief investment officer at Cumberland Advisors Inc. nailed the media-induced Whitney panic on the head…

“The Whitney virus can be seen replacing the bird flu virus. “We've got terrified clients who call constantly and want reassurance because Meredith said there's going to be hundreds of billions of dollars of defaults.”

We all know how the bird flu virus scare turned out.

The problem is that the media didn’t give much air time to Whitney’s critics. As a result, many retail investors sold their municipal bonds and funds in panic.

Whitney’s Cozy Relationship with the Media

The 60 Minutes interview propelled Whitney into the ranks of (financial) “celebrity” status, joining a long list of other bozos. And she provided 60 Minutes with exactly what it wanted; a fear-mongering “forecast” of hundreds of billions of dollars in defaults in 2011. The 60 Minutes segment with Whitney should serve as further evidence that the media is more interested in creating drama than presenting credible insights.

But Whitney’s rise to media fame hasn’t been instant. She has been embraced by the media establishment for several years. In addition to serving as a commentator on FOX, Whitney has made numerous appearances and given hundreds of interviews to print and broadcast media. In virtually every case that Whitney has tried to stir the pot with her claims, the media has failed to provide suitable rebuttal from credible experts.

Much like Nouriel Roubini and several other members of the media club, Whitney often finds herself on magazine cover and television features, regardless what she has to say. This would be acceptable if she had a good track record. However, much like Roubini and the others, her track record is questionable at best.

Did Whitney Really Predict the Financial Crisis?

Over the past couple of years Whitney’s “predictions” have been exaggerated and twisted by the media in a manner that resembles lies more than the truth. However, the media always positions its “chosen ones” as having predicted this and that, when the truth is much different. Other times, the media’s “experts” have been making the same predictions of doom for many years, which essentially removes all credibility these perpetual doomers claim to have earned. The same applies to the perma-bull Wall Street cheerleaders.

For instance, the media often credits Nouriel Roubini as having predicted the economic crisis as well. But Roubini knows deep down that the crisis took him by surprise. The fact is that he did not predict anything. If you examine his track record, you will see that he was merely waving his hands.

The media also claims that Robert Shiller and many other media favorites predicted the economic collapse. The fact is that if they did predict the collapse, they would have provided extensive documentation and analysis in a book BEFORE it occurred rather than AFTER.

Perhaps the most astonishing thing about the hindsight books written by these experts is that they lack any real insight or specific guidance. That is another matter that addresses the incompetency of the publishing industry; another segment of the media.

Likewise, when introduced by the media Whitney is praised for having predicted the financial crisis. However, this is not at all true. In fact, Whitney did not even predict the real estate collapse. Study her track if you want to understand just how behind the curve she was. The fact is that Whitney remained just as clueless as the rest of Wall Street. Only after the financial crisis had begun in mid-2008 did Whitney latch onto what was going on. But by that time, most of the juice was already gone.

Amazingly, other than the routine issuance of earnings shortfalls for a few banks, Whitney’s rise to media fame came from, get this… predicting Citigroup Inc.'s 2008 dividend cut, produced a report for clients called "Tragedy of the Commons."

Are you kidding me?

Let me get this straight. I predict a global collapse, advised investors to short Fannie, Freddie, the banks and homebuilders, I predicted Dow 6000, oil above $100, gold to at least $1400 and silver to at least $30, localize the timing in advance, advise investors to buy exactly at the market bottom, and much more, all written in two books published in late 2006 early 2007. And I advised clients to short the banks in October 2007, yet no one knows about me.

Meanwhile, Whitney predicts a dividend cut in 2008 for Citigroup and all of the sudden she predicted the financial collapse?? Are ******* kidding me?

You should be asking yourself why this is the case.

Once you realize how the media works, you will know the answer. The game is to provide Main Street with clowns, making sure to convince you they are experts. That way, Wall Street will more easily take your money.

Why would the media assist Wall Street in these criminal activities? Who do you think buys the ads for financial shows?

As long as you pay attention to the media, you won’t have a clue what’s really going on. America’s corporate-controlled media monopoly continues to be a circus show, largely without any notice by Main Street. This is specifically why America finds itself in costly unneeded wars in the Middle East. And it is specifically why most Americans have lost any chance of ever retiring before age 70.

Once you understand the design of the entire racket, you will realize that the media was at least equally responsible for the stock market losses, and resulting job losses as Wall Street because they continued to hide everything. Even when the least sophisticated viewers finally realized what was going on, the media continued to sugar-coat things.

However, since the media commanded an audience, it is ultimately Main Street who holds the blame for its losses. Fools continue to be taken by the same criminals over and over. Wise men realize the source of deceit and act accordingly. If you want things to change; if you want to stop losing money in the stock market; if you want the truth, the best to achieve these things is to stay away from the media. Otherwise, you will only have yourself to blame the next time you get screwed.

Fortune magazine called Whitney “the superstar analyst” during an interview to discuss her report. During an appearance on CNBC, the airhead bimbo hacks called her report “a very, very sophisticated and smart report.”

Wait a minute. Weren’t the clowns on CNBC referring to former Lehman CEO Fuld and Bear Stearn CEO Jimmy Cayne as “very, very smart”?

This is the same Jimmy Cayne that gets high regularly. I worked at Bear Stearns when Cayne was Commander-in-Chief, and as far as I could tell he did what most CEOs in America do; he spent most of his time playing golf, attending social outings, meeting with other elites for fancy dinners and showing up for PR events. But as far as doing anything that resembled running a company, like most of America’s CEOs he was MIA when it came time to take care of business.

A writer for Fortune magazine referred to Whitney as “The woman who called Wall Street's meltdown” in an August 2008 article with the same title. Among the BS about her husband the wrestler, the article discusses how she predicts a deep recession.

What a minute. It’s August 2008. Let’s assume the reporter interviewed Whitney in June 2008. Who in their right mind wasn’t aware that the U.S. was already in a recession by that time? This provides another example of the useless trash published by the media.

What about Whitney’s mysterious report she alluded to on 60 Minutes?

According to at least one individual who has read Whitney’s 43-page report and the addendum has stated that it doesn’t mention sizable defaults amounting to hundreds of billions of dollars.

Wait a minute; 43 pages? Okay so forget the short length of Whitney’s report. Supposedly, the full report (most of which includes the addendum, aka data copied from public documents) is 600 pages. Regardless of the length of the report, the most important thing to consider is that it doesn’t mention the kinds of defaults she has been talking about.

“We are not calling for any specific defaults within the scope of this report” (page 42).

The report merely mentions that there will be defaults. It does not discuss which cities or states will default, nor does it discuss the size of the defaults.

Is that the kind of forecast the merits an interview on a widely viewed program if the intent is to report credible insights?

Or is it the kind of forecast a media show would agree to air in order to create drama, or perhaps participate in securities manipulation?

Whitney’s predictions are starting to sound a lot like those of Gerald Celente, another media clown who makes Whitney seem like a genius. If you don’t realize what a clown Celente is by now, I’m not so sure you can be helped.

[Somehow, a few years ago Celente got some irresponsible journalist to believe that he predicted several events (despite no evidence of any real research based on any data) and ever since then, every media outlet has taken these claims as valid WITHOUT independently verifying them. His open-ended wording is about as similar to qualifying as a prediction as that used by Martin Weiss, but at least Weiss does some research (although nothing seems to help this guy's miserable performance). Have a look at this piece on Celente by Ed Champion.]

Reference: http://www.avaresearch.com/article_details-659.html

During a breakfast meeting held on January 30, Whitney attempted to respond to the lack of data to support her prediction.

“A lot of this is, You know it, but can you prove it? There are fifth-derivative dimensions that I don't think I need to spell out to my clients.”

“Fifth-derivative dimensions”? Good God.

So basically what Whitney is saying is, “I can’t prove my predictions. They’re too mysterious to prove. Check my crystal ball and you’ll understand.”

Perhaps we should all do as Jimmy Cayne might, and take few bong hits so we can understand what a fifth-derivative dimension is.

Maybe Whitney has a more advanced understanding of math and science than me because I don’t recall ever coming across a fifth-derivative dimension in any of my chemistry and physics courses; maybe I skipped class that day.

The Muni Panic Sets In

As you can imagine, the past few years have not been so kind to municipal bonds. A couple of years ago, the sell-off in munis was triggered by the implosion of the real estate bubble. However, the muni market recovered since then. More recently, the sell-off has been the result of persistent struggles of many cities to find ways to shore up their balance sheets.

Finally in November of 2010, much of the Street downgraded the muni sector causing a sell-off. This panic selling was further exacerbated by Whitney’s December 19th appearance on 60 Minutes, as well as continued follow-up interviews by the media.

The Federal Reserve added to the dumping of munis when it began buying U.S. government debt under its quantitative easing policy, which boosted Treasury yields.

Finally, the Build America Bonds program, which generated sales of $187 billion of securities, was set to expire at the end of 2010. The rush by state and local governments to issue the taxable securities shrunk demand for traditional tax-exempt debt. This added momentum to declining muni bond prices.

By the end of the 2010 fourth quarter the cost for AAA-rated issuers to borrow for 30 years climbed by almost a third, to 5.09% on Jan. 17, from 3.85% Nov. 1.

Thus far in 2011, the news hasn’t been much better.

For the week ended January 19, 2011, investors sold a net of $4 billion from municipal-bond mutual funds, making it the most since Lipper US Fund Flows started compiling the data in 1992. At the time, the withdrawals marked the 10th-straight week of net redemptions, totaling $20.6 billion. Since then the streak has continued, although it has lightened up a bit.

Finally, the first quarter is likely to set an 11-year record-low for issuance of municipal debt. This drop off in supply is adding to the liquidity pressures faced by municipal bond fund managers. Added with net redemptions, it is forcing many funds to sell bonds at big discounts; the precise time when they would normally be buying.

Whitney’s Damage Control

It should have been clear to anyone who wasted 20 minutes of their life watching her 60 Minutes interview that Whitney really didn’t have any hard numbers to go on. In fact, during a follow-up interview to discuss her report on January 30, 2011, she admitted what most industry experts already knew; she doesn't have specific numbers backing up her prediction.

“Quantifying is a guesstimate at this point. I was giving an approximation of a magnitude that will bear out to be correct.”

A “guesstimate”? Is this what you expect from a so-called professional analyst making bold claims of massive defaults? Come on. It’s clear that Whitney is pulling numbers out of her ass to fit her extremist views, similar to how Nouriel Roubini and other media whores have done in the past.

So where has the media been throughout this dog-and-pony show?

Has the media called Whitney out?

Of course not! That would bite the hand of drama that feeds the ratings machine.

On January 12th, 2011, Whitney made an appearance on the bubble network of baboons and stock manipulators (CNBC). During the interview, she downplayed the size of her prediction of hundreds of billions in defaults by replying that it’s “not that much” since there is almost $3 trillion in outstanding municipal debt.

So in other words, you have a banking analyst who measures the relative size of her default predictions based on the total outstanding municipal debt. Shouldn’t one compare the historical default rates as a better measure of the size of these expected defaults?

When responding to comments made by a very credible municipal bond fund manager and others who have been highly critical of her predictions, Whitney stated that her critics are “municipal-bond brokers” who have a lot to lose. Sure they have a lot to lose when someone creates panic to the extent that investors sell their bonds causing net redemptions.

Yes Whitney, if the types of defaults occur that you have predicted, they will lose. However, you are making them lose now because of the panic you’ve created which has pushed investors out of munis. Instead of pointing to what fund managers have to lose, why don’t you point to what you have to gain by creating drama? I’ll get to Whitney’s motives later.

As a result of Whitney’s baseless predictions, many fund managers have been forced to sell at losses in order to cover net redemptions. Just as fund managers managed to calm some of their clients, others have sold in mass forcing prices lower. This has caused fund managers to deal with net redemptions the only way possible. They have had to sell. This has caused prices to drop even lower. And when clients see rising muni yields, they actually believe it’s a reflection of Whitney’s predictions.

I certainly wouldn’t want to be a muni bond fund manager who has to deal with this ludicrous situation. There is no way to win because you’re dealing with sheep who actually think the media can be trusted. Muni fund managers have a right to be mad as hell when the strongest force threatening their fund returns comes not from the inherent risks of their municipal bond positions, but from the panic created by the media.

Moreover, Whitney has designed a good deal of wiggle room with which to weasel her way out of the corner of shame and onto the pedestal of fame. For instance, she does not use the formal definition of default. A default occurs when a borrower fails to make a payment due on a bond. Whitney uses the definition of a technical default, which occurs when a borrower fails to abide by a condition, or covenant, of the bond agreement. Most often, technical defaults have no affect on repayment.

From page 2 of Whitney’s report, it states, “debt service at the state level is not something we believe is at risk.”

The report continues…“states have and will continue to default on social contracts in the form of reduced spending on things including education and transportation.”

Then in a January 30th interview, Whitney adds that “a restructuring certainly counts as a default.”

Are you kidding me?

How does hundreds of billions of dollars in defaults turn into spending cuts?

Everyone is aware that spending will be cut. No one needs to hear this from Whitney.

As a media veteran and former salesman on Wall Street (as an analyst), Whitney had already begun preparing her backup plan prior to the airing of the 60 Minutes interview. She wanted to make sure she covered all angles from her dire prediction of “hundreds of billions of dollars in defaults.” For instance, on November 3rd, Whitney wrote a Wall Street Journal article saying state bailouts had already begun, because Build America Bonds were “subsidized by the federal government.”

This simply isn’t accurate. The Build America Bonds program was part of the American Recovery and Reinvestment Act of 2009 aimed at subsidizing bonds for infrastructure projects. Under the program the government covered 35% of the issuer’s interest costs. In return, the federal government received the tax returns on the bonds.

In other words, the tax-exempt status of these bonds was removed, so it’s wasn’t a free ride because the U.S. Treasury would recoup these subsidies through tax revenues.

In addition, if this program is to be considered a bailout, should we also not consider the $200 billion provided to states as a bailout? If so, this still does not account for “hundreds of billions of dollars in defaults.” And if this is considered a bailout, then it was known well before Whitney came out with her report.

It should be clear that Whitney is merely trying to make the key fit her lock of deceit.

Whitney’s Credibility Is About As Low as it Gets

A Fitch Ratings report released on November 16th, 2010 stated that while there is a good chance of a higher default rate relative to recent years, these defaults will continue to be isolated situations.” Fitch lists reasons like captive tax bases and bondholders' strong claims on revenue for most debt. The report made the commonsense point that debt service payments represent a relatively small percentage of most budgets so it serves very little benefit relative to the detriment to stop making payments (see New York State’s 2010 Balance Sheet, under interest on general debt shown above).

All of the Wall Street municipal research departments I’ve seen agree with Fitch.

At this point you might be thinking…why would I trust what a credit-rating agency says? After all, they were the ones who rubber-stamped AAA ratings on real estate junk bonds, right?

And why would I trust what a Wall Street firm says?

The fact of the matter is that since the real estate collapse, the credit-rating agencies have become very critical in their ratings due diligence and review process because they feel Washington and the SEC breathing down their back.

Moreover, just because Wall Street research cannot be blindly relied upon doesn’t mean that all Wall Street research is trash. You can always find value with even the most useless sources. What’s important is the ability to determine fact from fiction. This requires excellent judgment as well as a good deal of expertise. The problem is that most people lack the ability to make these determinations. Therefore, in the end these sources cause more detriment than benefit. In the end, most people base their opinions on what the media emphasizes.

When cities, counties and states get into financial trouble, defaults are rare. Only on rare occasions do municipalities fail to make principal and interest payments to creditors. What happens instead are cuts to programs, tax increases and other measures. This is precisely what we have already seen, and it is precisely what we will continue to see. That certainly does NOT fall into the category of hundreds of billions of dollars in defaults.

According to data by Moody’s, there were 54 bond defaults over a 39-year period as of 2010 from a list of securities it rates. Of these defaults, 42 were standalone housing and healthcare projects, while just three involved General Obligation debt, the safest of all municipal bonds.

Whitney’s Agendas

Despite the dire economic ramifications of Whitney’s predictions, she refuses to release her report to the media. Doesn’t that seem a bit strange?

If in fact she is so sure of her “analysis,” wouldn’t it make more sense to release the report to the media? If things panned out as she predicts, she would have tons of clients for life, right?

Moreover, with such a catastrophic scenario, why would she withhold this report when it could destroy the very nation where she lives?

None of this makes a bit of sense. After all, Whitney has gone on record stating that she’s “a good American. This is why I write op-ed pieces, why I go beyond servicing my clients to provide solutions. It's to be a good American," she told New York magazine in 2009.”

So if Whitney is such a “good American,” and if things are going to get as bad as she says, why won’t she release her report?

Perhaps the answer to this mystery can be solved once you realize that her company charges, at minimum $100,000 a year for its research. In my opinion, this is further evidence of Whitney’s real motives. I certainly hope that price tag includes an annual membership to the best brothels in the world because I can assure you that would be a much better way to spend the money than rely on Whitney’s research.

It is clear to me that Whitney is looking to generate revenues by selling panic and fear.

The rates charged for her research is further evidence that I am giving away my own research (which is much more credible and accurate) for next to nothing. It looks like price hikes are on the way.

Is there more to Whitney’s agenda?

On November 10th Whitney met with U.S. Securities and Exchange Commission Chairman Mary Schapiro to discuss her company's application to become a Nationally Recognized Statistical Ratings Organization (NRSRO). If approved, this would allow her firm to compete with Standard & Poor's, Moody’s Investors Service and the other NRSROs.

According to a regulatory filing, among key points at the SEC meeting brought up by Whitney was that the "construct of rating agencies has little to no credibility, is not trusted, and ineffective." On January 30th, 2011, when Whitney was asked what improved credibility she could bring to the ratings process, she said she has "an untarnished track record."

Without a doubt, Standard & Poor’s and Moody’s are broken. However, the fix is quite simple. All that is needed for these agencies to restore credibility and competence is for the Department of Justice to send several of the executives to prison for a very long time. This would remove the scum that cooperates in securities fraud with Wall Street, as well as serve as a precedent for others who might feel the temptations to step over to the dark side.

Of course this is pure fantasy, as not a single one of the Wall Street executives responsible for the destruction of the global economy has been indicted for securities fraud. Furthermore, much like their friends on Wall Street, Greenspan, Rubin, Summers and others continue to walk the streets wealthier than before after serving pivotal role in the collapse of the global economy.

The lack of any criminal prosecution whatsoever as a result of this historic Ponzi scheme truly represents a dark period for humanity. Meanwhile, the SEC continues to distract the public by focusing on small-time fraud and minor counts of insider trading, all while turning its back to massive fraud by Wall Street firms.

Whitney’s “Untarnished Track Record”

Whitney has established a long track record of all-talk and poor results, much like every good salesman, politician and media pundit. Despite having numerous strong ties to the media, in October 2010 before Whitney commenced her media campaign, Bloomberg News reported that about two-thirds of her stock picks since starting her company in 2009 had fared worse than market indexes. For example, Visa Inc. fell 14% after she named it her “single best buy.” And Capital One Financial Corp. soared by 300% after she urged clients to sell.

I wonder what her clients have to say about her “untarnished track record.”

During an interview on January 30th, 2011, when questioned about her disastrous calls since starting her firm, Whitney replied, “Those are not fundamental calls.”

Not fundamental calls? If you’re an analyst and you’re being paid $100,000 per year for access to your “research,” you’d better be one of the very best in the world.

And if you blow it, and try to cover your ass by later qualifying your disastrous stock recommendations as if they didn’t matter, that tells me a lot more about your honesty than I already know about your incompetence.

A 2008 Fortune cover story ranked Whitney 1,205th out of 1,919 equity analysts the previous year, based on stock picking. However, the author tried to wipe away her incredibly miserable track record by focusing on her (interesting) arguments…

“Evaluating Whitney solely on the timing of her buys and sells misses the point,” (because her arguments are interesting).

Interesting arguments? Save the interesting arguments for the debate team.

Investors care about one thing. RESULTS.

I’m not saying an analyst needs to be right 100 percent of the time, but hell Whitney, how about at least 50%. Even a monkey can be right half the time when flipping a coin.

I don’t think a focus on results is asking too much from an analyst. Story-telling is a great skill to have if you’re a salesman or politician. Apparently, Whitney is great at sales, but as an analyst she is completely clueless. In fact, I would say she’s a danger to anyone who invests using her “research.”

Just a few days before her 60 Minutes interview aired, on November 16th Whitney appeared on the bubble and stock manipulation network, CNBC.

Here is what she said…

“Stocks are overvalued and the US economy is likely to fall back into a recession next year, well-known analyst Meredith Whitney told CNBC.”

At the time of this interview, the Dow was just over 11,000. Since then it has risen by as much as 1400 points just weeks after the interview.

It appears as if Whitney has no idea how to value the stock market, nor has any idea about earnings trends. And clearly, she has no idea how to gauge market sentiment.

Once again, Whitney is going with the odds. After the stock market had soared by 70%, largely without interruption, clearly the odds are high that a correction is approaching. However, as Robert Prechter, Peter Schiff, Marc Faber, Nouriel Roubini, Gary Schilling, Martin Weiss, and the rest of the media clowns still haven’t learned, TIMING MATTERS. Even a broken clock is right once a day. But real experts are right many times over.

As far as her recession prediction, the fact is that the U.S. has still not left the recession that began in December of 2007, so this does not represent any real news.

It’s easy to be seen as a superstar when you are paired up against Washington and Wall Street cheerleaders. You don’t have to be too right about things. All you have to do is wave your arms around and rattle off your battle cry or sales pitch, and you will be viewed as a breath of fresh air because you aren’t swinging the same BS as the cheerleaders. But that isn’t going to make you money. As Peter Schiff found out, unless you get the fine details correct, you will get blown out as much if not more than the buy-and-hold boys who never sold their U.S. stocks.

Whitney continues…

“I haven’t been this bearish in a year. I look at the board and every single stock from Tiffany to Bank of America to Caterpillar is up. But there is no fundamental rooting as to why these names are up—particularly in the consumer space.”

What truly sophisticated investor would care whether this lady is bearish or bullish? First of all analysts have no clue about the strength of the stock market. They are lucky if they can figure out their industry. In short, analysts view things from a myopic perspective, so they are the last people I’d listen to regarding stock market direction.

Whitney just doesn’t get it. Timing DOES matter. While the risks to the economy are mounting, this does not take away from the fact that economic and earnings data has largely supported the rise in the stock market since her interview. Nor does it take away from the fund flow data, hedge fund margin levels and other data that has shown why the market has risen. It has taken historic events - recent turmoil in the Middle East and catastrophe in Japan – to defuse the market.

Whitney, my advice to you is to spend a few years managing assets, then go back to the drawing board and see if you can breach the disconnect between theoretical shoulda, woulda, couldas, and actually make some accurate calls that make people money.

Regarding the rise in shares of Bank of America, apparently Whitney fails to realize why interest rates remain near 0 percent. It certainly isn’t to slash credit card interest rates. And it certainly isn’t to help fund pension plans. The banks are using this free cash to collect bond spreads in Latin America and Asia. Combined with the ease of mark-to-market accounting, this has helped Bank of America (although the bank remains in a vulnerable position). I would expect even a novice banking analyst to understand this.

Whitney damages her credibility further by failing to understand basic the fundamentals accounting for the rise in shares of Caterpillar. Certainly the stock is ahead of itself. However, from earnings growth and other basic metrics, the current share price is largely backed by fundamentals. It’s quite simple. Caterpillar is generating a great deal of business from Asia, especially China.

The Deviant Psychology Underlying Media “Experts”

Whitney’s marketing campaign serves as a perfect example of similar campaigns used by other members of the perma-bear media club. Let’s have a look how it works. Once you understand the simplicity of this tactic, you will find yourself picking apart all of the clowns you choose watch in the media.

The strategy employed by those seeking to make a name for themselves is as simple to understand as it is to implement. It can be effectively executed by a child as much as by those the media positions as “experts.”

It works like this. When you spot a relentless trend, you extrapolate the trend when making predictions. Through this approach you are playing better odds. For instance, when a region experiences a period of harsh weather, an opportunist looking to position himself as a prophet will predict more bad weather to come.

We saw how this tactic was used a couple of years ago when several extremists began to predict that all banks would fail only after Bear Stearns, Fannie, Freddie, Washington Mutual, AIG and Lehman failed (although Washington Mutual did not really fail, as I have shown previously). Of course other banks did not fail because TARP was passed.

I liken this approach to jumping on the extremist band wagon. As a twist, you also throw in a bit of contrarian thinking when you see excessive cheerleading from Washington and Wall Street.

The key behind this approach is to never make specific forecasts. You keep things general and open-ended so you can later fill in the blanks and wiggle your way out of the corner if you are scrutinized.

Unfortunately, the results of this deceptive strategy are frequently inaccurate because the forecasts are not based on extensive research and analysis. Moreover, extreme extrapolation and irrational contrarian thinking often fails to consider intangible variables which often come into play and alter the course or severity of the trend that has been extrapolated.

In the end, individuals utilizing this manipulative strategy are doing nothing other than spewing hot air and having their hands. Not everyone is capable of executing this strategy because it requires a person to be inherently dishonest and deceitful.

It’s that simple. Yet for some strange reason, the deviant psychology underlying this manipulative strategy remains largely undetected by the public.

Whitney even hints at her tactic. She admits that her call is really nothing. She actually admits that she is playing the odds by making the more obvious call! Let’s have a look. On January 30th, Whitney said…

“I think folks that are saying I'm wrong are making a bigger call than I am because they're saying munis are safe. And that, I think, will prove to be a regrettable tack. That's a bigger call. That's a much bigger call.”

You see, Whitney is making the safe call because everything looks bad right now. So she’s going with the odds. It’s a low-risk strategy designed to win her fame and business because the media likes drama. Drama boosts ratings. But not everyone is able to attract media attention simply by providing them with needed drama. Although Whitney lacks the most important characteristic that is guaranteed to get you into the media spotlight (she’s not Jewish), she has been able to overcome this using her media connections.

Without a doubt there will be more defaults. But the real question is whether there will be 100 defaults totaling $200 billion in 2011.

The answer is NO. And when 2011 passes, she will do one of two things. She will either revise her forecast to 2012, then 2013 (similar to John Williams and his hyperinflation forecasts), or she will claim that defaults occurred because cities and counties failed to adhere to their covenants.

It’s really a win-win situation for Whitney because there are enough naive people out there who will be fooled into thinking that she was right. How do I know? We saw the same situation with Peter Schiff, despite the fact that he missed much more than he nailed. And the things he nailed were pretty obvious.

Details Peter; profits always lie in the details. That means specific forecasts and specific strategies that include active management. But Schiff is in sales, not research. All he needs is do is create the perception that he knows what’s going on. And the media enables him to achieve this. He is in the media club. That in itself tells you about his track record.

Likewise, details Meredith; that means specific forecasts. We want to see specific names. We want the details. We want to see your data. Similar to Schiff, Whitney is in the sales and marketing business. Assisted by the media, Whitney is perceived as an expert by the sheep, but only because the media says so. Once you carefully examine her track record, the picture looks very different than that painted by the media.

Whitney has done the same thing as many others who have been selected into the media club. The list of individuals who engage in the same behavior with similar disastrous results is virtually endless, as their track records reveal.

If Whitney had come out with her “hundreds of billions of dollars in defaults” prediction in 2007, it would have held a lot more credibility, but only if it had been backed by extensive data and analysis. Instead, she waited until the budget problems of states and cities have been made obvious to even teenagers. This tells me that she is doing nothing other than playing the odds. She’s extrapolating the trend to its fullest extent. And she is doing this as a marketing strategy.

Do not permit yourself to be fooled by Whitney’s motives and associated rhetoric. Her tactics are commonly used by other members of the media club. They are always positioned as experts with great track records; experts who predicted this and that. But the truth tells a vastly different story. All you have to do is spend the time researching track records and you will see for yourself.

Whitney: A Kid among Adults

It is with little debate that municipal bond managers, economists, and Wall Street analysts, and virtually everyone else absolutely missed the biggest crisis in U.S. history. This is to be expected, as Wall Street does a poor job measuring risk, and an even worse job managing it despite their delusional claims and complex mathematical equations. The complete lack of creative problem solving by Wall Street has created an army of robots, who are as much a part of the herd as Main Street. The focus of Wall Street is to make money and worry about risk after it appears. The insane compensation structure and lack of accountability (which continues to this day) ensure this to be the law of the land.

After missing the disaster, I am willing to bet that most municipal bond fund managers understand the risks that lay ahead. After witnessing the worst financial crisis in history, and an economy that has shown no real signs of recovery, fund managers continue to deploy large armies of analysts and economists focused on assessing the risks of their investments.

In fact, it should be obvious that muni fund managers have a much larger pool of resources and expertise at their disposal than Whitney and her staff. This aligns them in a much better position to understand the risks. Without a superior understanding of things, muni bong fund managers will be incapable of designing effective strategies for each scenario.

Regardless how much they may know, the one thing fund managers cannot defeat is the effect of panic selling, similar to what Whitney has spurred. Unexpected redemptions are the absolute worst enemy of every fund manager because it forces them to sell precisely when they would otherwise be buying; at the bottom. Once you remove the ability of fund managers to dollar-cost average and rebalance their portfolio, you have created a very big problem. For this, fund managers have Whitney and the media to blame.

In the end, it is the investor who stands to lose in the same manner after Wall Street issues sell signals only after stocks have bottomed. And after investors have sold in panic, Wall Street buys. It’s the age-old pump-and-dump scheme at work.

What Whitney fails to understand is the fact that Washington would never permit a large default, as it would threaten to halt the slow progress made towards an economic recovery. Apparently she has forgotten that Obama’s 2009 economic stimulus package included several hundred billion dollars for states and cities. Once these defaults fail to surface as she has predicts, she is likely to use the excuse that states and cities were bailed out by Washington. While one could argue this as a valid point, no one needs to spend $100,000 to hear it from Whitney. Furthermore, that’s a much different than “hundreds of billions of dollars in defaults.”

I see no evidence that Whitney understands the full gamut of the current economic situation. She certainly did not understand it a few years ago. If she had, she would have advised her clients to short the mortgage and bank stocks, rather than merely warn of a dividend cut from Citigroup.

Knowing that the real estate market will remain a lame duck for several years is insufficient to conclude it will lead to hundreds of billions of dollars in defaults over the next few years, much less in 2011. The question I have is whether Whitney truly intends to become a credible analyst, or gunner for short-side hedge funds. I think I know the answer.

So You Wanna Make Alotta Money?

Establishing an excellent track record doesn’t hold much weight as far as the media is concerned. Regardless of your track record or agendas, the media will position you as an expert so long as it fits within their own agendas.

It’s much easier to become a media “celebrity” than a credible analyst or investment strategist. Being elevated to “celebrity” sta

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.